Sallie Mae (SLM)

Sallie Mae catches our eye. Its market-beating ROE illustrates its ability to invest in highly profitable ventures.― StockStory Analyst Team

1. News

2. Summary

Why Sallie Mae Is Interesting

Originally created as a government-sponsored enterprise before privatizing in 2004, Sallie Mae (NASDAQ:SLM) is a financial services company that provides private education loans, savings products, and educational resources to help students and families pay for college.

- Stellar return on equity showcases management’s ability to surface highly profitable business ventures

- One pitfall is its 2% annual revenue growth over the last five years was slower than its financials peers

Sallie Mae shows some potential. If you like the stock, the valuation looks fair.

3. Sallie Mae (SLM) Research Report: Q4 CY2025 Update

Student loan provider Sallie Mae (NASDAQ:SLM) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 16.4% year on year to $454.1 million. Its GAAP profit of $1.12 per share was 19.7% above analysts’ consensus estimates.

Sallie Mae (SLM) Q4 CY2025 Highlights:

- Net Interest Income: $377.1 million vs analyst estimates of $381.9 million

- Revenue: $454.1 million vs analyst estimates of $449.7 million (16.4% year-on-year growth, 1% beat)

- Pre-tax Profit: $316 million (69.6% margin)

- EPS (GAAP): $1.12 vs analyst estimates of $0.94 (19.7% beat)

- EPS (GAAP) guidance for the upcoming financial year 2026 is $2.75 at the midpoint, missing analyst estimates by 1%

- Market Capitalization: $5.37 billion

Company Overview

Originally created as a government-sponsored enterprise before privatizing in 2004, Sallie Mae (NASDAQ:SLM) is a financial services company that provides private education loans, savings products, and educational resources to help students and families pay for college.

Sallie Mae operates primarily through its banking subsidiary, Sallie Mae Bank, which originates and services private education loans that bridge the gap between college costs and what students receive from family resources, scholarships, and federal aid. The company's flagship product is the Smart Option Student Loan, which offers three repayment options including two that require payments while students are still in school—a feature designed to reduce total loan costs and establish good repayment habits early.

Beyond traditional undergraduate loans, Sallie Mae offers specialized loan products for graduate programs in law, medicine, dentistry, and other professional fields, with features tailored to these students' unique needs, such as extended grace periods for medical students. The company maintains relationships with approximately 2,100 higher education institutions, with its relationship management team working directly with financial aid offices.

Sallie Mae has expanded beyond lending to become a broader education solutions provider. The company offers free college planning tools, scholarship search capabilities (following its acquisition of Scholly), and FDIC-insured deposit products including high-yield savings accounts and the goal-based SmartyPig savings platform. A student applying to college might use Sallie Mae's scholarship search to find funding opportunities, open a savings account to set aside money for expenses, and then take out a private education loan to cover remaining costs.

The company generates revenue primarily through interest income on its loan portfolio and fee income from its various financial products. Sallie Mae's business model relies on maintaining high credit quality in its loan portfolio, with most of its customers successfully managing their payments.

4. Student Loan

Student loan providers finance higher education expenses. Growth opportunities exist in private loan offerings, refinancing existing debt, and international education funding. Challenges include political uncertainty around potential loan forgiveness programs, default risk correlation with employment markets, and increasing scrutiny of educational outcomes relative to debt burdens.

Sallie Mae's main competitors include Discover Financial Services (NYSE:DFS), Citizens Financial Group (NYSE:CFG), PNC Financial Services (NYSE:PNC), and private companies like SoFi, Earnest, and College Ave Student Loans in the private student loan market.

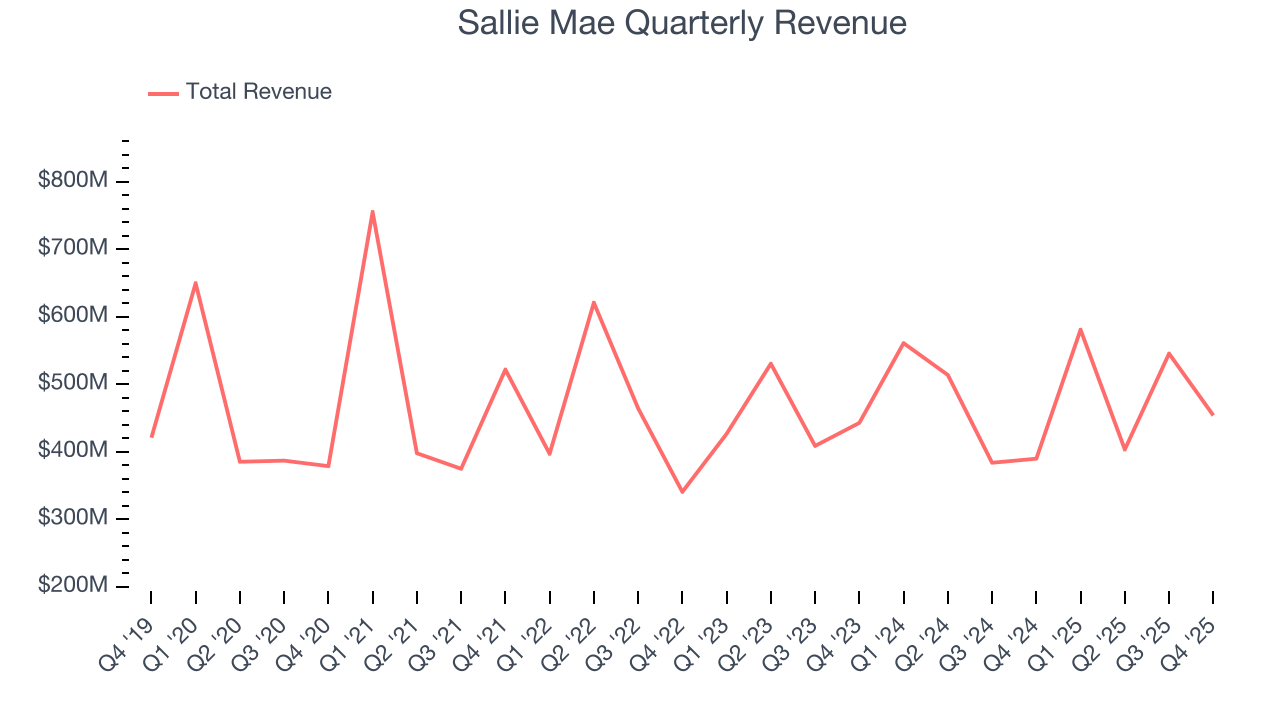

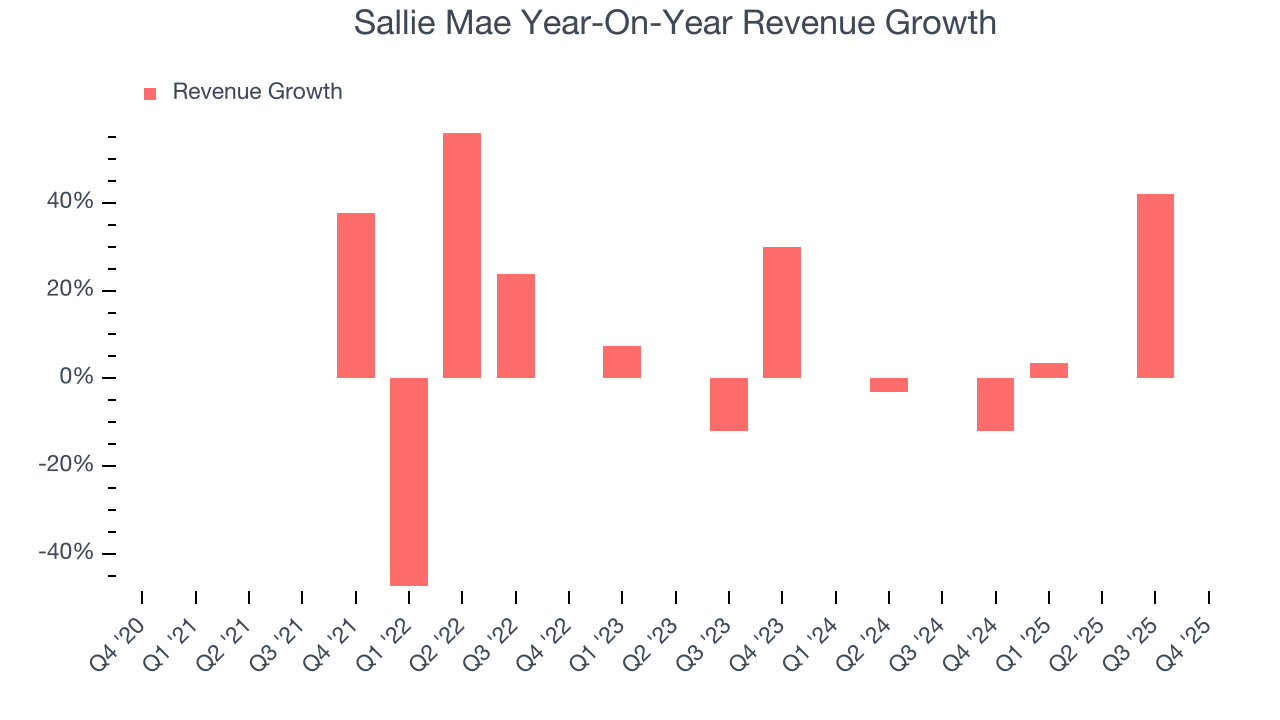

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Sallie Mae’s 2% annualized revenue growth over the last five years was sluggish. This wasn’t a great result, but there are still things to like about Sallie Mae.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Sallie Mae’s annualized revenue growth of 4.7% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Sallie Mae reported year-on-year revenue growth of 16.4%, and its $454.1 million of revenue exceeded Wall Street’s estimates by 1%.

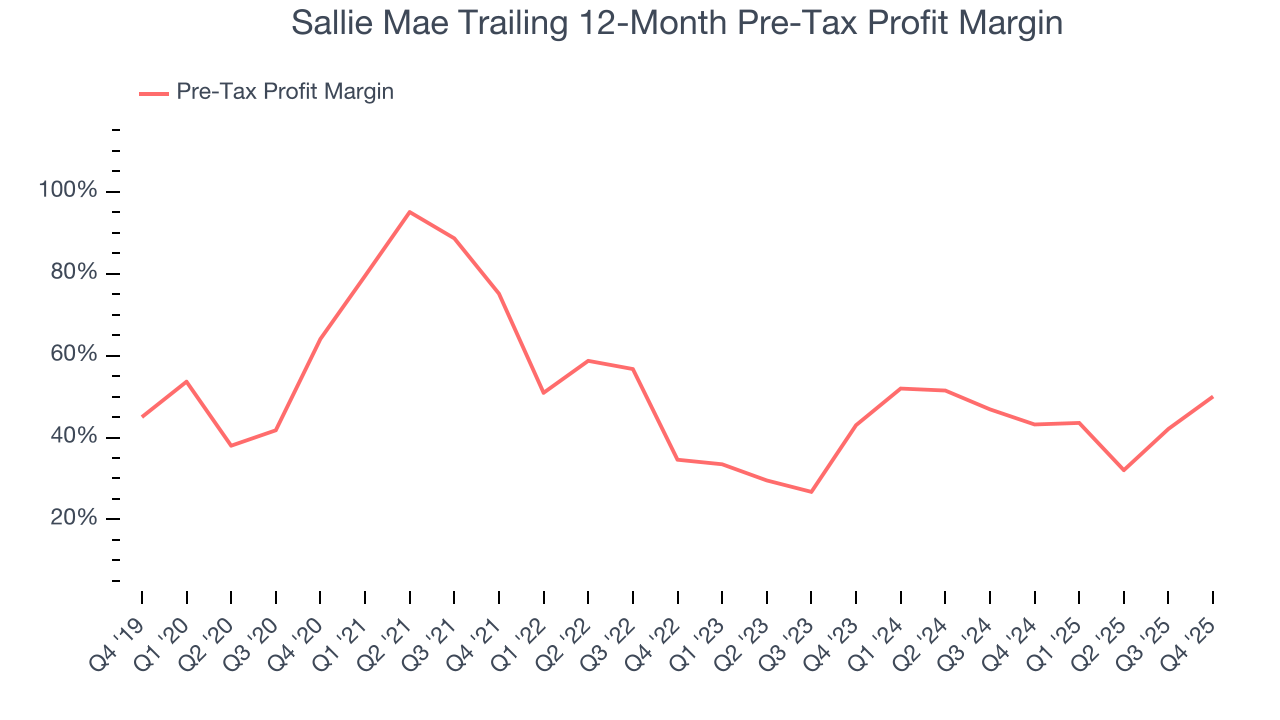

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Student Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Interest income and expenses play a big role in financial institutions' profitability, so they should be factored into the definition of profit. Taxes, however, should not as they are largely out of a company's control. This is pre-tax profit by definition.

Over the last five years, Sallie Mae’s pre-tax profit margin has risen by 14 percentage points, going from 75.1% to 50%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 7 percentage points on a two-year basis.

Sallie Mae’s pre-tax profit margin came in at 69.6% this quarter. This result was 35.7 percentage points better than the same quarter last year.

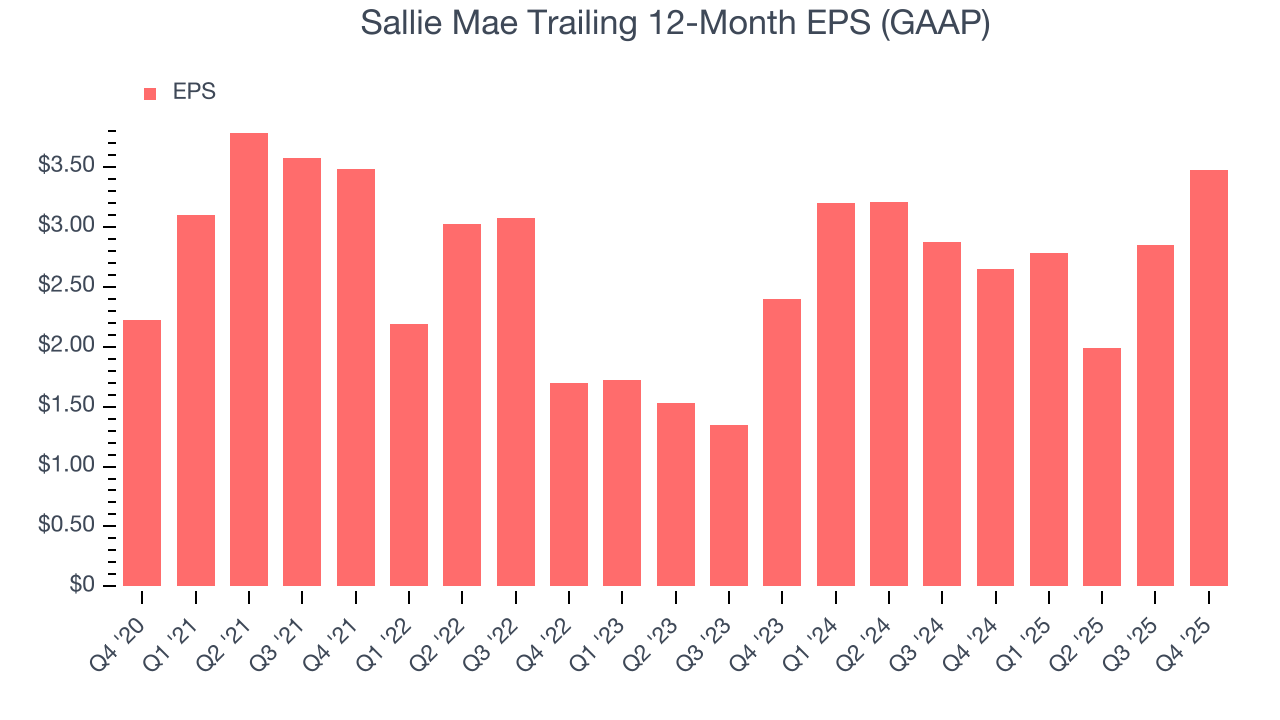

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sallie Mae’s EPS grew at an unimpressive 9.3% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its pre-tax profit margin didn’t improve.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Sallie Mae, its two-year annual EPS growth of 20.2% was higher than its five-year trend. This acceleration made it one of the faster-growing financials companies in recent history.

In Q4, Sallie Mae reported EPS of $1.12, up from $0.50 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Sallie Mae’s full-year EPS of $3.47 to shrink by 20.4%.

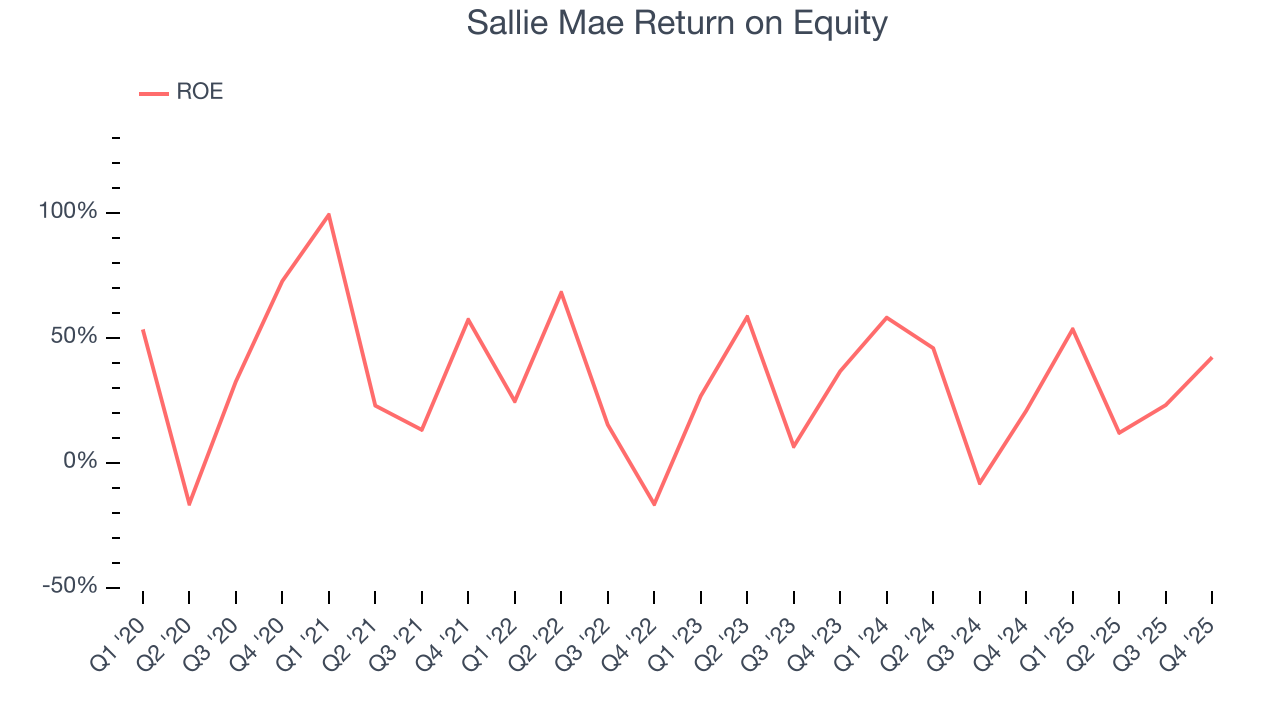

8. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Sallie Mae has averaged an ROE of 32.9%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This shows Sallie Mae has a strong competitive moat.

9. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, Sallie Mae has averaged a Tier 1 capital ratio of 11.9%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

10. Key Takeaways from Sallie Mae’s Q4 Results

It was good to see Sallie Mae beat analysts’ EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its net interest income slightly missed and its full-year EPS guidance fell slightly short of Wall Street’s estimates. Overall, we think this was still a decent quarter with some key metrics above expectations. The stock traded up 4.3% to $27.86 immediately after reporting.

11. Is Now The Time To Buy Sallie Mae?

Updated: March 23, 2026 at 1:03 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Sallie Mae.

There’s plenty to admire about Sallie Mae. Although its revenue growth was weak over the last five years and analysts expect growth to slow over the next 12 months, Sallie Mae’s stellar ROE suggests it has been a well-run company historically.

Sallie Mae’s P/E ratio based on the next 12 months is 7.2x. Looking at the financials space right now, Sallie Mae trades at a compelling valuation. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $30.73 on the company (compared to the current share price of $20.00), implying they see 53.6% upside in buying Sallie Mae in the short term.