Sleep Number (SNBR)

Sleep Number keeps us up at night. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sleep Number Will Underperform

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ:SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

- Store closures and disappointing same-store sales suggest demand is sluggish and it’s rightsizing its operations

- Sales tumbled by 12.6% annually over the last three years, showing consumer trends are working against its favor

- Short cash runway increases the probability of a capital raise that dilutes existing shareholders

Sleep Number is in the doghouse. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Sleep Number

Sleep Number is trading at $3.45 per share, or 11.9x forward EV-to-EBITDA. This multiple is quite expensive for the quality you get.

It’s better to pay up for high-quality businesses with strong long-term earnings potential rather than to buy lower-quality companies with open questions and big downside risks.

3. Sleep Number (SNBR) Research Report: Q4 CY2025 Update

Bedding manufacturer and retailer Sleep Number (NASDAQ:SNBR) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 7.8% year on year to $347.4 million. Its GAAP loss of $2.55 per share was significantly below analysts’ consensus estimates.

Sleep Number (SNBR) Q4 CY2025 Highlights:

- Revenue: $347.4 million vs analyst estimates of $328.7 million (7.8% year-on-year decline, 5.7% beat)

- EPS (GAAP): -$2.55 vs analyst estimates of -$0.55 (significant miss due to restructuring charges and a deferred tax valuation adjustment)

- Operating Margin: -2.3%, down from 0.7% in the same quarter last year

- Free Cash Flow was -$643,000 compared to -$29.97 million in the same quarter last year

- Locations: 600 at quarter end, down from 640 in the same quarter last year

- Same-Store Sales fell 8% year on year (-2% in the same quarter last year)

- Market Capitalization: $104.6 million

Company Overview

Known for mattresses that can be adjusted with regards to firmness, Sleep Number (NASDAQ:SNBR) manufactures and sells its own brand of bedding products such as mattresses, bed frames, and pillows.

The core customer is typically a homeowner who cares about quality sleep and has strong preferences when it comes to mattress feel. These customers can include a married couple where one spouse prefers a softer mattress whereas the other prefers a firmer one–Sleep Number offers mattresses where each half’s firmness can be adjusted. These customers can also include those who want more data on their sleep quality–Sleep Number offers smart mattress technology that can register movement and interpret sleep depth.

Sleep Number stores are fairly small, roughly 4,000 square feet. They are typically located in suburban shopping centers or retail districts. The stores feature products in bedroom-like settings to create an inviting atmosphere. Trying out mattresses is encouraged given how important it is for customers to find the right firmness and feel.

A dynamic unique to Sleep Number and other mattress retailers is how infrequently the average consumer is in the market for a new bed or mattress–roughly five to ten years. On the other hand, these purchases tend to be pretty big-ticket in nature, and Sleep Number products are on the more costly end of the price spectrum given the technology features.

4. Home Furniture Retailer

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

Bedding and mattress competitors include Tempur Sealy (NYSE:TPX), Leggett & Platt (NYSE:LEG), and Purple Innovation (NASDAQ:PRPL).

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

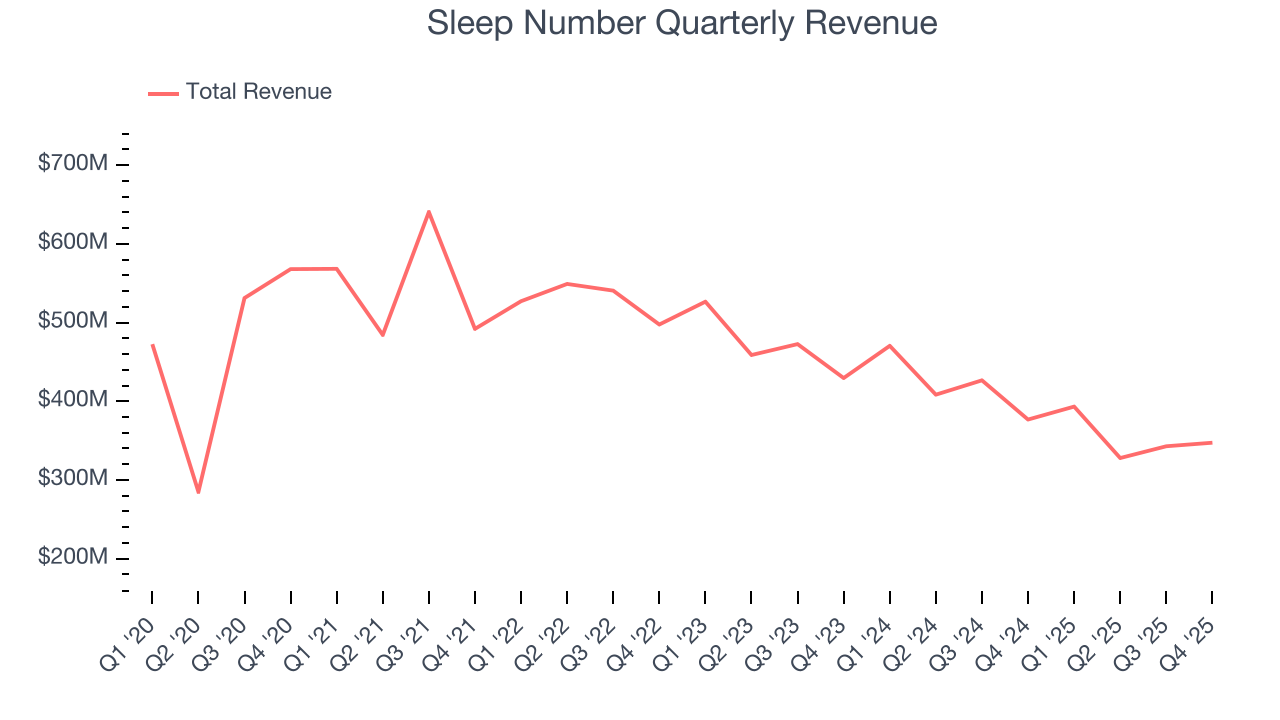

With $1.41 billion in revenue over the past 12 months, Sleep Number is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Sleep Number struggled to generate demand over the last three years. Its sales dropped by 12.6% annually as it closed stores and observed lower sales at existing, established locations.

This quarter, Sleep Number’s revenue fell by 7.8% year on year to $347.4 million but beat Wall Street’s estimates by 5.7%.

Looking ahead, sell-side analysts expect revenue to decline by 3.4% over the next 12 months. it’s hard to get excited about a company that is struggling with demand.

6. Store Performance

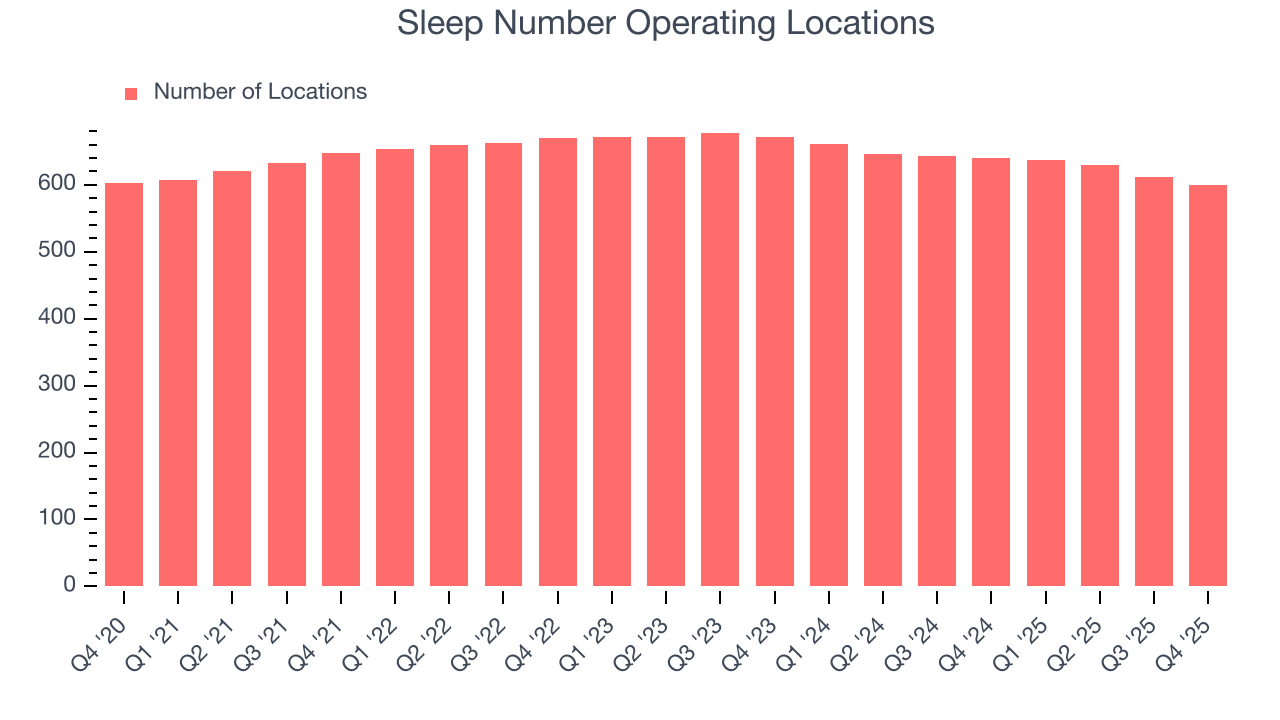

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Sleep Number operated 600 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 4.1% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales gives us insight into this topic because it measures organic growth for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year.

Sleep Number’s demand has been shrinking over the last two years as its same-store sales have averaged 1.7% annual declines. This performance isn’t ideal, and Sleep Number is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Sleep Number’s same-store sales fell by 8% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

7. Gross Margin & Pricing Power

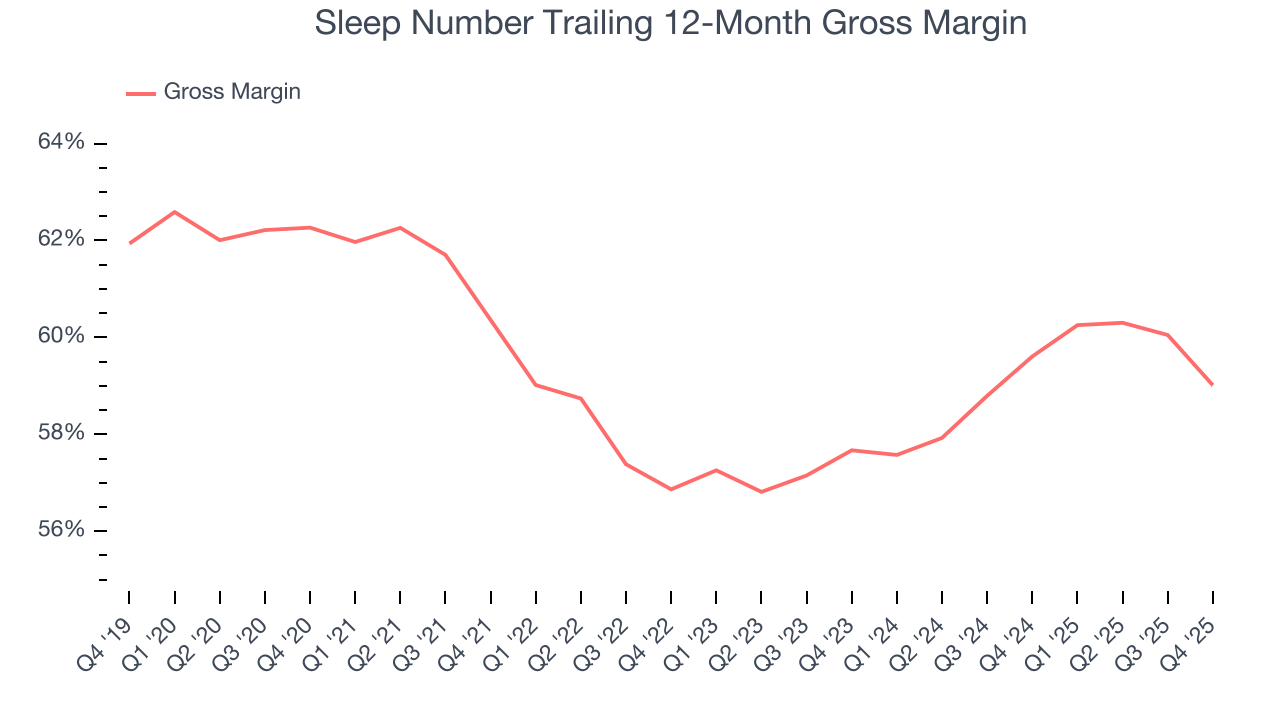

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Sleep Number has best-in-class unit economics for a retailer, enabling it to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an elite 59.3% gross margin over the last two years. That means Sleep Number only paid its suppliers $40.66 for every $100 in revenue.

Sleep Number’s gross profit margin came in at 55.6% this quarter , marking a 4.2 percentage point decrease from 59.9% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

8. Operating Margin

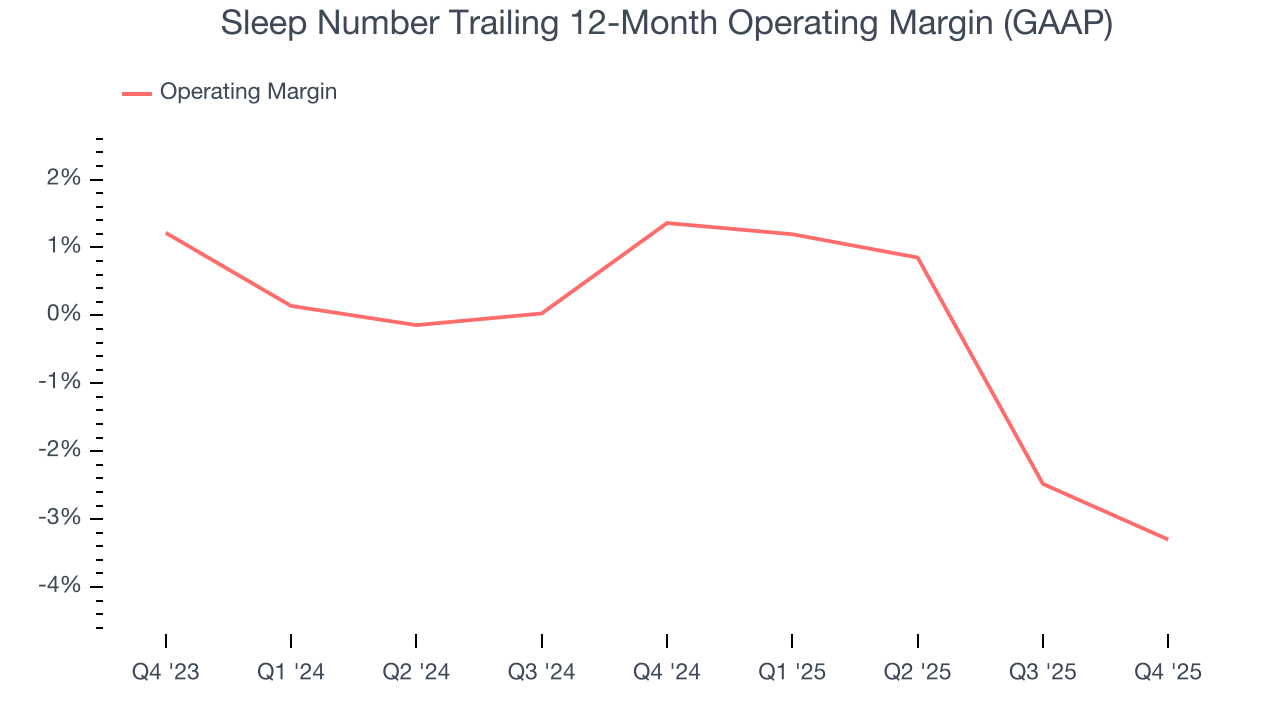

Sleep Number was roughly breakeven when averaging the last two years of quarterly operating profits, one of the worst outcomes in the consumer retail sector. This result is surprising given its high gross margin as a starting point.

Analyzing the trend in its profitability, Sleep Number’s operating margin decreased by 4.7 percentage points over the last year. Sleep Number’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Sleep Number generated a negative 2.3% operating margin. The company's consistent lack of profits raise a flag.

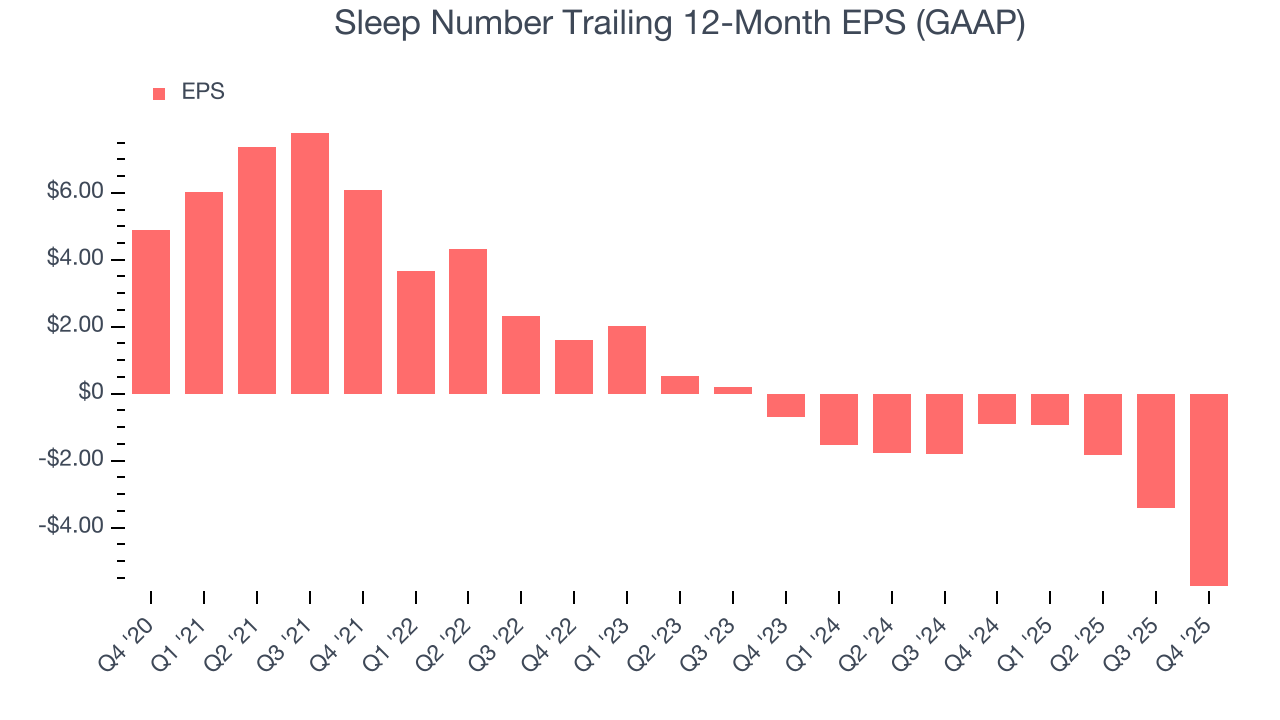

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Sleep Number, its EPS declined by 77.4% annually over the last three years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

In Q4, Sleep Number reported EPS of negative $2.55, down from negative $0.21 in the same quarter last year due to restructuring charges and a deferred tax valuation adjustment. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Sleep Number to improve its earnings losses. Analysts forecast its full-year EPS of negative $5.76 will advance to negative $0.66.

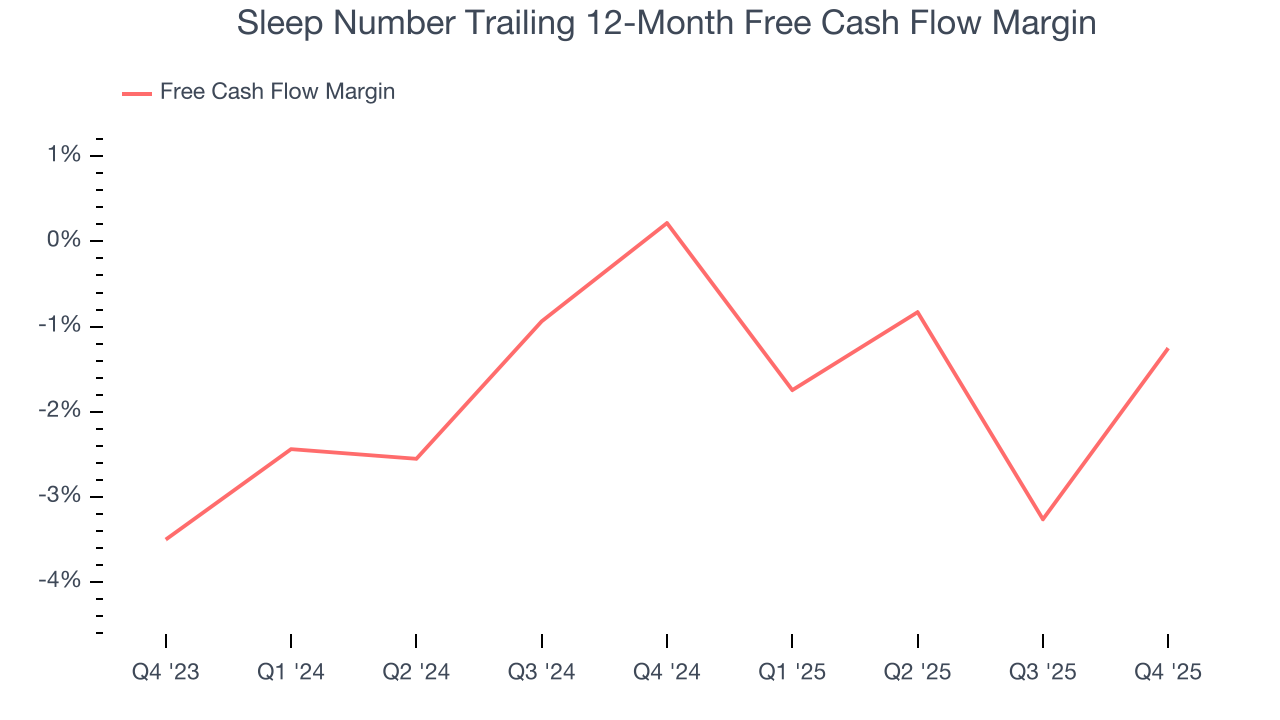

10. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Sleep Number broke even from a free cash flow perspective over the last two years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, we can see that Sleep Number’s margin dropped by 1.5 percentage points over the last year. This decrease warrants extra caution because Sleep Number failed to grow its same-store sales. Its cash profitability could decay further if it tries to reignite growth by opening new stores.

Sleep Number broke even from a free cash flow perspective in Q4. This result was good as its margin was 7.8 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends trump fluctuations.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Sleep Number historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 9.9%, somewhat low compared to the best consumer retail companies that consistently pump out 25%+.

12. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Sleep Number burned through $17.69 million of cash over the last year, and its $942.5 million of debt exceeds the $1.69 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

Unless the Sleep Number’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of Sleep Number until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

13. Key Takeaways from Sleep Number’s Q4 Results

We were impressed that Sleep Number beat analysts’ revenue and operating profit expectations this quarter. On the other hand, its EPS fell short of Wall Street’s estimates, but this was due to restructuring charges and a deferred tax valuation adjustment. Overall, this print leaned positive. The stock traded up 7.6% to $4.93 immediately following the results.

14. Is Now The Time To Buy Sleep Number?

Updated: March 15, 2026 at 10:45 PM EDT

Are you wondering whether to buy Sleep Number or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Sleep Number falls short of our quality standards. To kick things off, its revenue has declined over the last three years. While its admirable gross margins are a wonderful starting point for the overall profitability of the business, the downside is its declining EPS over the last three years makes it a less attractive asset to the public markets. On top of that, its operating margins reveal poor profitability compared to other retailers.

Sleep Number’s EV-to-EBITDA ratio based on the next 12 months is 11.9x. At this valuation, there’s a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $4.50 on the company (compared to the current share price of $3.45).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.