StepStone Group (STEP)

StepStone Group piques our interest. Its impressive revenue growth indicates the value of its offerings.― StockStory Analyst Team

1. News

2. Summary

Why StepStone Group Is Interesting

Operating as both an advisor and asset manager with over $100 billion in assets under management, StepStone Group (NASDAQ:STEP) is an investment firm that provides clients with access to private market investments across private equity, real estate, private debt, and infrastructure.

- Market share has increased this cycle as its 32.2% annual revenue growth over the last five years was exceptional

- Earnings per share grew by 20.4% annually over the last five years and easily exceeded the peer group average

- A downside is its ROE of 1.1% reflects management’s challenges in identifying attractive investment opportunities

StepStone Group has some noteworthy aspects. We’d wait until its quality rises or its price falls.

Why Should You Watch StepStone Group

At $43.33 per share, StepStone Group trades at 18.8x forward P/E. This valuation is richer than that of financials peers.

StepStone Group could improve its business quality by stringing together a few solid quarters. We’d be more open to buying the stock when that time comes.

3. StepStone Group (STEP) Research Report: Q4 CY2025 Update

Private markets investment firm StepStone Group (NASDAQ:STEP) announced better-than-expected revenue in Q4 CY2025, with sales up 140% year on year to $586.5 million. Its non-GAAP profit of $0.65 per share was 4.7% above analysts’ consensus estimates.

StepStone Group (STEP) Q4 CY2025 Highlights:

- Assets Under Management: $220 billion vs analyst estimates of $840.5 billion (22.9% year-on-year growth, 73.8% miss)

- Revenue: $586.5 million vs analyst estimates of $418.3 million (140% year-on-year growth, 40.2% beat)

- Pre-tax Profit: -$194.6 million (-33.2% margin)

- Adjusted EPS: $0.65 vs analyst estimates of $0.62 (4.7% beat)

- Market Capitalization: $5.06 billion

Company Overview

Operating as both an advisor and asset manager with over $100 billion in assets under management, StepStone Group (NASDAQ:STEP) is an investment firm that provides clients with access to private market investments across private equity, real estate, private debt, and infrastructure.

StepStone serves institutional investors such as pension funds, sovereign wealth funds, insurance companies, and high-net-worth individuals who seek exposure to private markets but may lack the resources or expertise to invest directly. The firm offers these clients customized portfolio management, specialized fund solutions, and advisory services tailored to their specific investment goals and risk profiles.

The company employs a multi-faceted approach to private markets investing. It creates funds-of-funds that invest across multiple underlying private equity or real estate funds, makes direct investments alongside fund managers in specific companies or assets, and provides secondary market solutions where it purchases existing private market investments from other investors. This flexibility allows clients to gain diversified exposure to private markets through a single relationship.

For example, a state pension fund might engage StepStone to build a customized private equity program that includes commitments to various fund managers, co-investments in specific companies, and opportunistic secondary purchases—all managed through StepStone's platform.

StepStone generates revenue through management fees based on committed or invested capital, performance-based fees (carried interest) when investments exceed certain return thresholds, and advisory fees for its consulting services. The firm's global footprint includes offices across North America, Europe, Asia, and Australia, allowing it to source investment opportunities worldwide and provide localized expertise to its global client base.

The company's proprietary technology platform, SPI (StepStone Private markets Intelligence), supports its investment process by collecting and analyzing data on thousands of fund managers and private market investments.

4. Custody Bank

Custody banks safeguard financial assets and provide services like settlement, accounting, and regulatory compliance for institutional investors. Growth opportunities stem from increasing global assets under custody, demand for data analytics, and blockchain technology adoption for settlement efficiency. Challenges include fee pressure from large clients, substantial technology investment requirements, and competition from both traditional players and fintech firms entering the space.

StepStone Group competes with other private markets investment firms including Blackstone (NYSE:BX), KKR (NYSE:KKR), Hamilton Lane (NASDAQ:HLNE), and Partners Group (SWX:PGHN), as well as the alternative asset management divisions of traditional asset managers like BlackRock (NYSE:BLK).

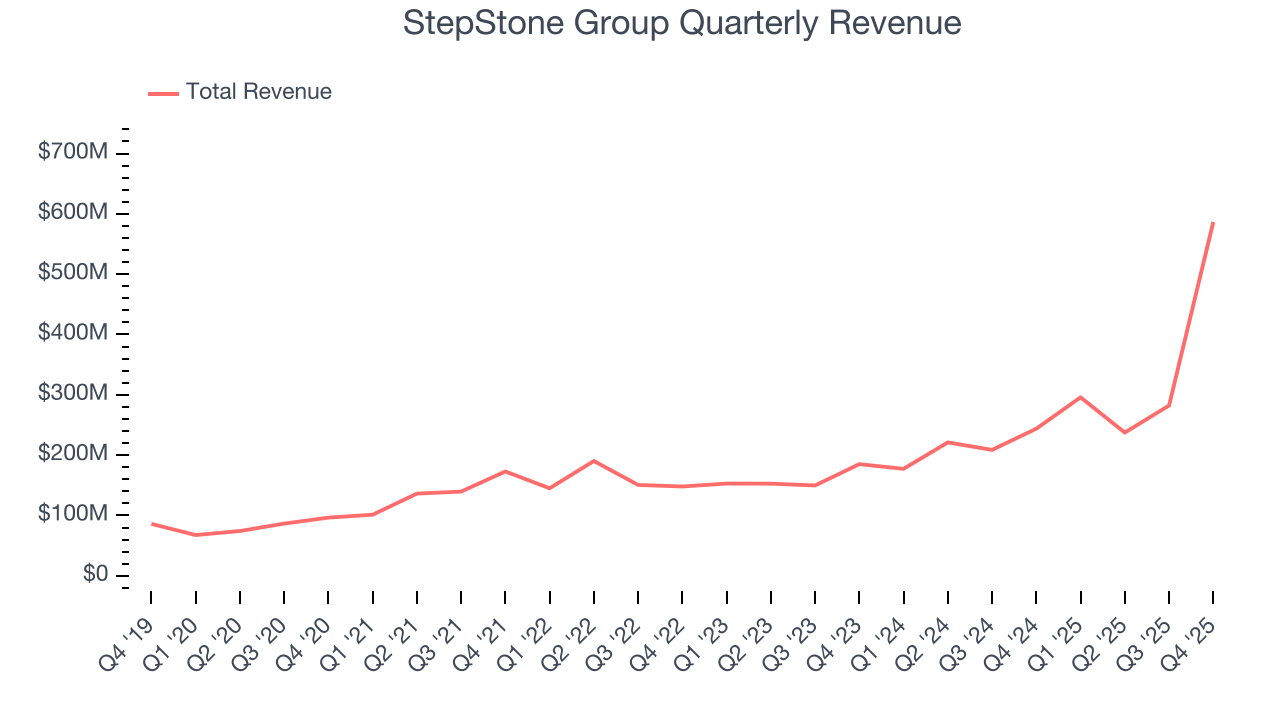

5. Revenue Growth

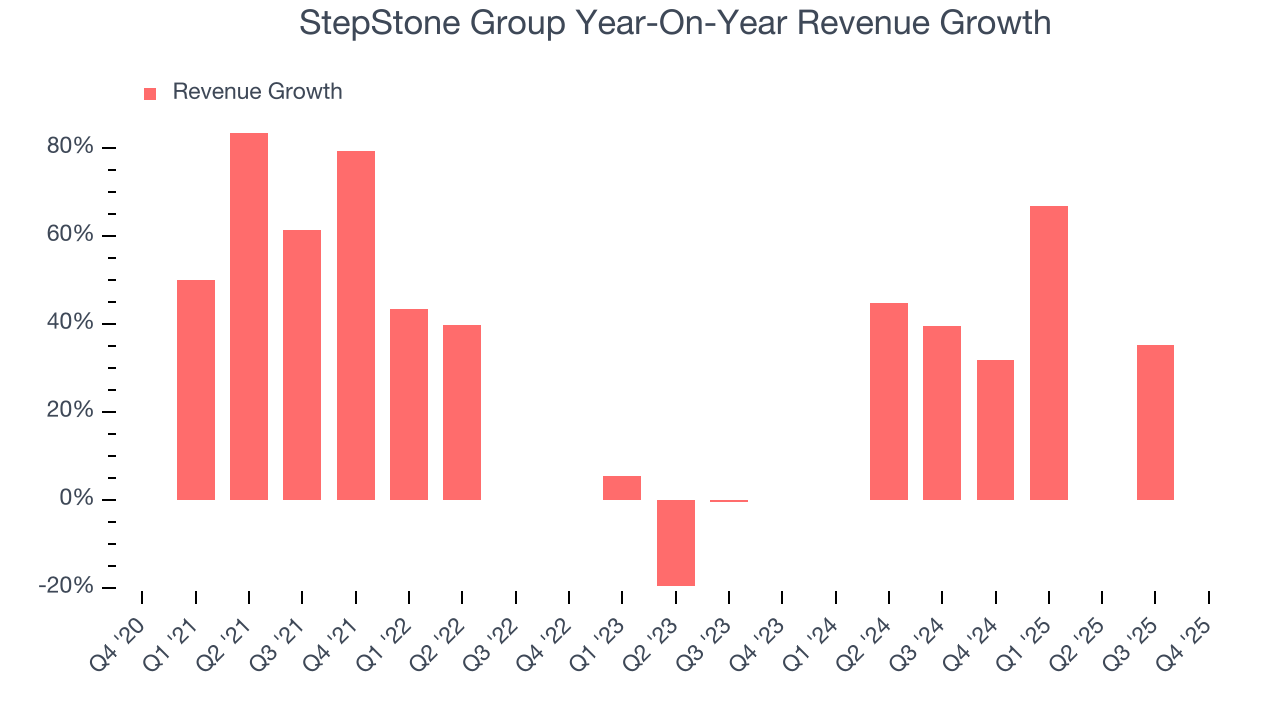

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Luckily, StepStone Group’s revenue grew at an incredible 34% compounded annual growth rate over the last five years. Its growth surpassed the average financials company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. StepStone Group’s annualized revenue growth of 47.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, StepStone Group reported magnificent year-on-year revenue growth of 140%, and its $586.5 million of revenue beat Wall Street’s estimates by 40.2%.

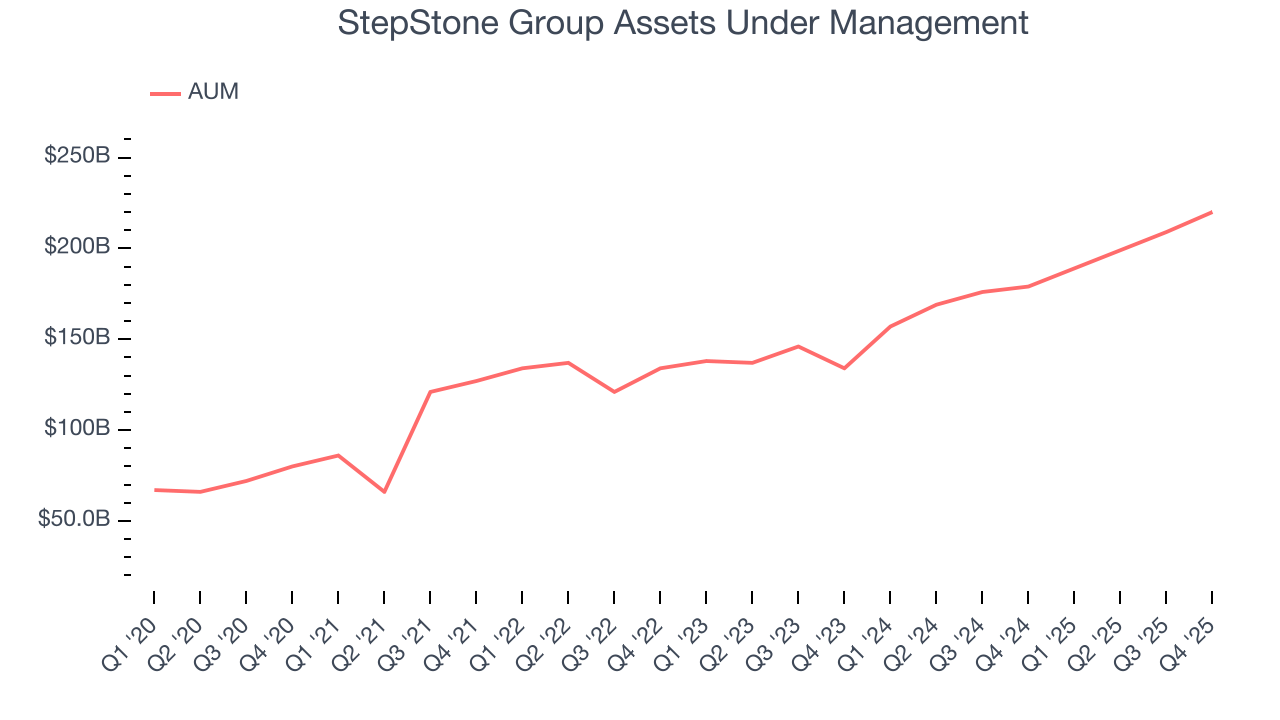

6. Assets Under Management (AUM)

Assets Under Management (AUM) is the cornerstone of a financial firm's investment division, representing all client capital under its stewardship. Management fees on this AUM create reliable, recurring revenue that maintains stability even when investment performance struggles, though prolonged poor returns can eventually affect asset retention and growth.

StepStone Group’s AUM has grown at an annual rate of 23.4% over the last five years, much better than the broader financials industry but slower than its total revenue. When analyzing StepStone Group’s AUM over the last two years, we can see that growth decelerated to 21.3% annually. Fundraising or short-term investment performance were net detractors to the company over this shorter period since assets grew slower than total revenue. But again, we put less weight on asset growth given how lumpy and cyclical it can be.

StepStone Group’s AUM punched in at $220 billion this quarter, falling 73.8% short of analysts’ expectations. This print was 22.9% higher than the same quarter last year.

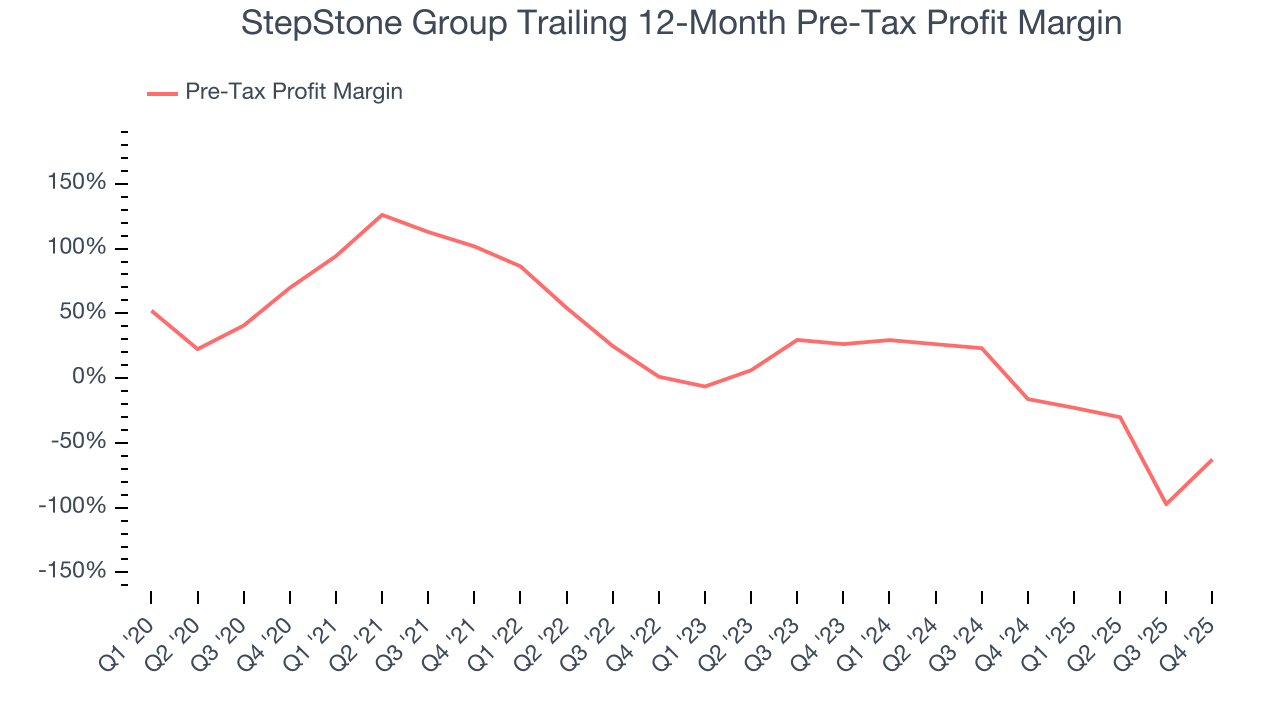

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Custody Bank companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Financials companies manage interest-bearing assets and liabilities, making the interest income and expenses included in pre-tax profit essential to their profit calculation. Taxes, being external factors beyond management control, are appropriately excluded from this alternative margin measure.

Over the last five years, StepStone Group’s pre-tax profit margin has risen by 132.5 percentage points, going from 102% to negative 62.8%. It has also declined by 89.1 percentage points on a two-year basis, showing its expenses have consistently increased at a faster rate than revenue. This usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

StepStone Group’s pre-tax profit margin came in at negative 33.2% this quarter. This result was 108.1 percentage points better than the same quarter last year.

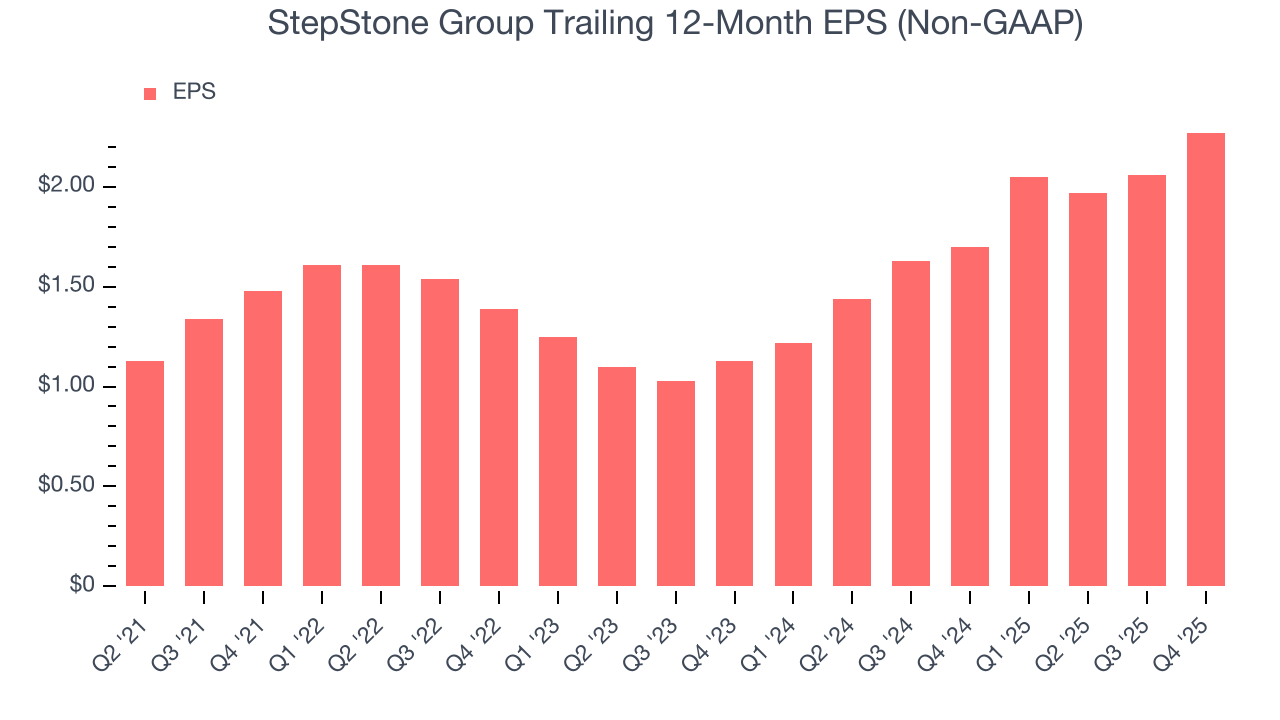

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

StepStone Group’s EPS grew at a remarkable 20.4% compounded annual growth rate over the last five years. However, this performance was lower than its 34% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For StepStone Group, its two-year annual EPS growth of 41.7% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, StepStone Group reported adjusted EPS of $0.65, up from $0.44 in the same quarter last year. This print beat analysts’ estimates by 8.8%. Over the next 12 months, Wall Street expects StepStone Group’s full-year EPS of $2.27 to grow 7.5%.

9. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, StepStone Group has averaged an ROE of 5.1%, uninspiring for a company operating in a sector where the average shakes out around 10%. We’re optimistic StepStone Group can turn the ship around given its success in other measures of financial health.

10. Balance Sheet Assessment

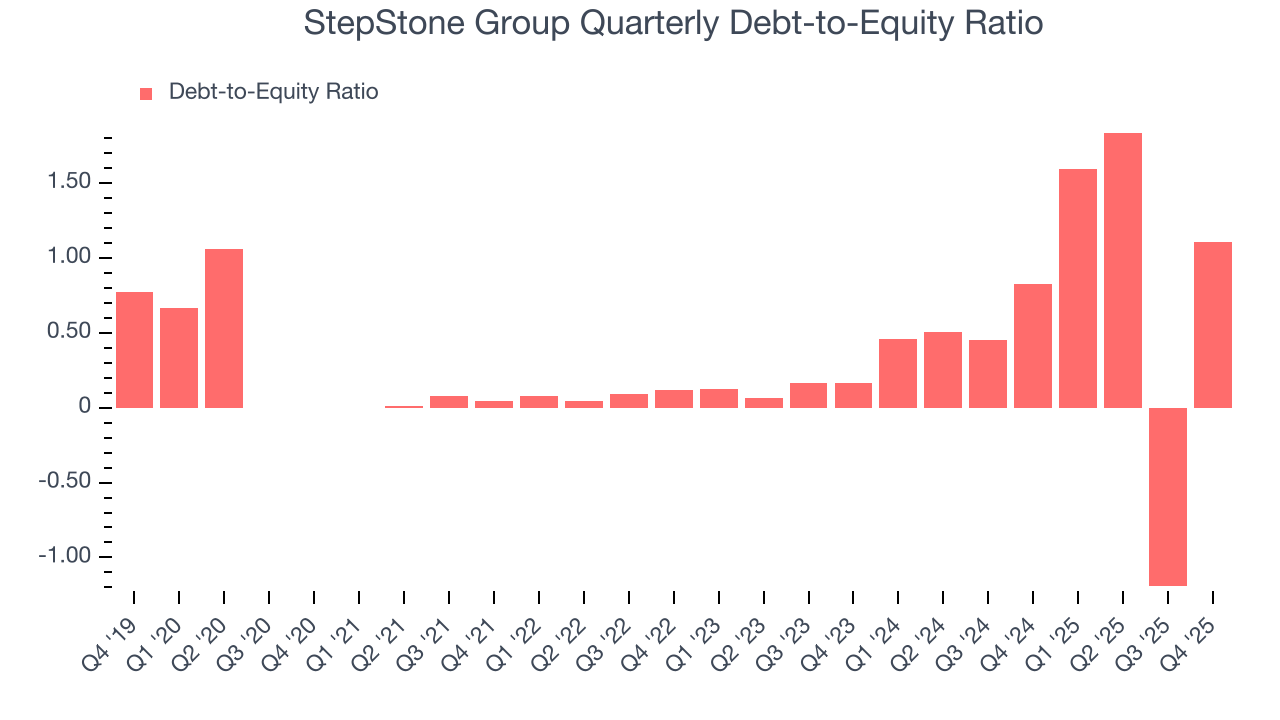

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

StepStone Group currently has $376.7 million of debt and $339.7 million of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.8×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

11. Key Takeaways from StepStone Group’s Q4 Results

We were impressed by how significantly StepStone Group blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its AUM missed. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $59.04 immediately after reporting.

12. Is Now The Time To Buy StepStone Group?

Updated: March 13, 2026 at 12:31 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in StepStone Group.

In our opinion, StepStone Group is a solid company. First off, its revenue growth was exceptional over the last five years. And while its declining pre-tax profit margin shows the business has become less efficient, its AUM growth was exceptional over the last five years. On top of that, its remarkable EPS growth over the last five years shows its profits are trickling down to shareholders.

StepStone Group’s P/E ratio based on the next 12 months is 18.8x. This multiple tells us that a lot of good news is priced in. This is a good one to add to your watchlist - there are better opportunities elsewhere at the moment.

Wall Street analysts have a consensus one-year price target of $79.71 on the company (compared to the current share price of $43.33).