Triumph Financial (TFIN)

Triumph Financial is up against the odds. Its weak sales growth and low returns on capital show it struggled to generate demand and profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Triumph Financial Will Underperform

Originally focused on traditional banking before pivoting to serve the transportation sector, Triumph Financial (NASDAQ:TFIN) provides specialized financial services to the trucking industry, including payments processing, factoring, banking, and data intelligence solutions.

- Flat sales over the last two years suggest it must find different ways to grow during this cycle

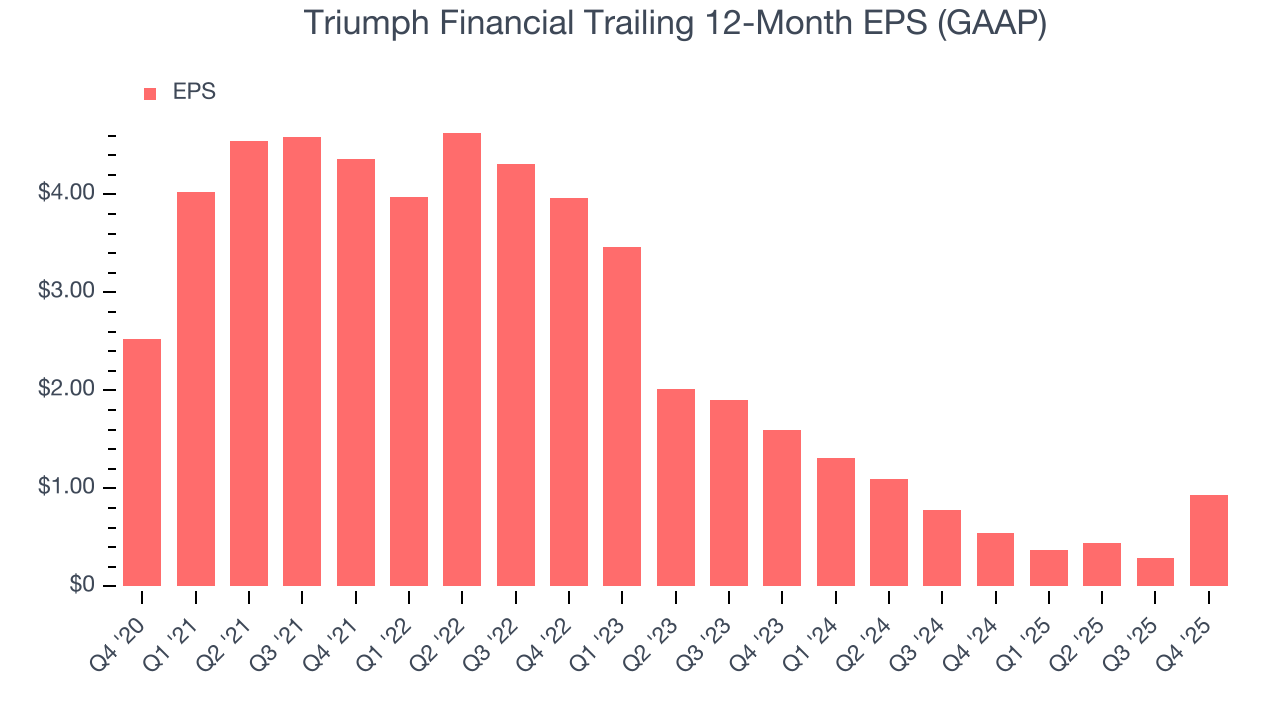

- Performance over the past five years shows its incremental sales were much less profitable, as its earnings per share fell by 22.1% annually

- Tangible book value per share stagnated over the last five years, limiting its ability to leverage its balance sheet to make additional investments

Triumph Financial’s quality doesn’t meet our hurdle. Our attention is focused on better businesses.

Why There Are Better Opportunities Than Triumph Financial

Triumph Financial’s stock price of $69.36 implies a valuation ratio of 1.9x forward P/B. This multiple is higher than that of banking peers; it’s also rich for the top-line growth of the company. Not a great combination.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Triumph Financial (TFIN) Research Report: Q4 CY2025 Update

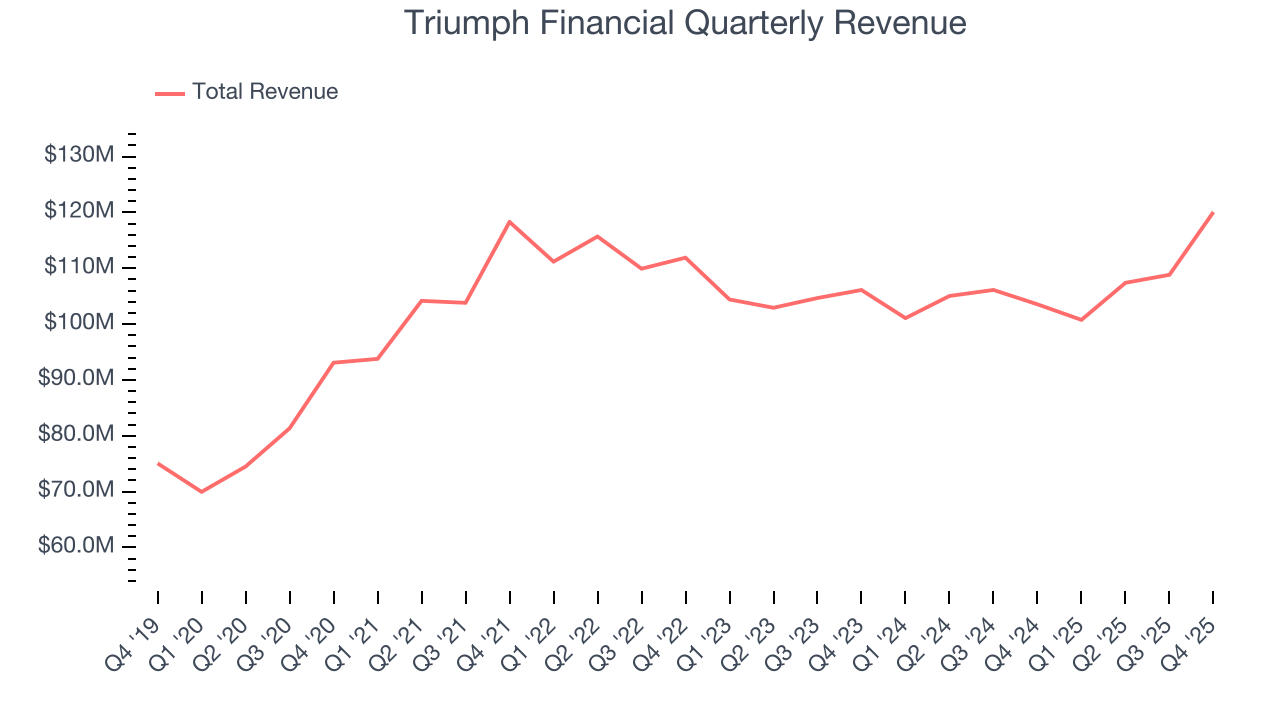

Financial services company Triumph Financial (NASDAQ:TFIN) announced better-than-expected revenue in Q4 CY2025, with sales up 16% year on year to $120.1 million. Its GAAP profit of $0.77 per share was significantly above analysts’ consensus estimates.

Triumph Financial (TFIN) Q4 CY2025 Highlights:

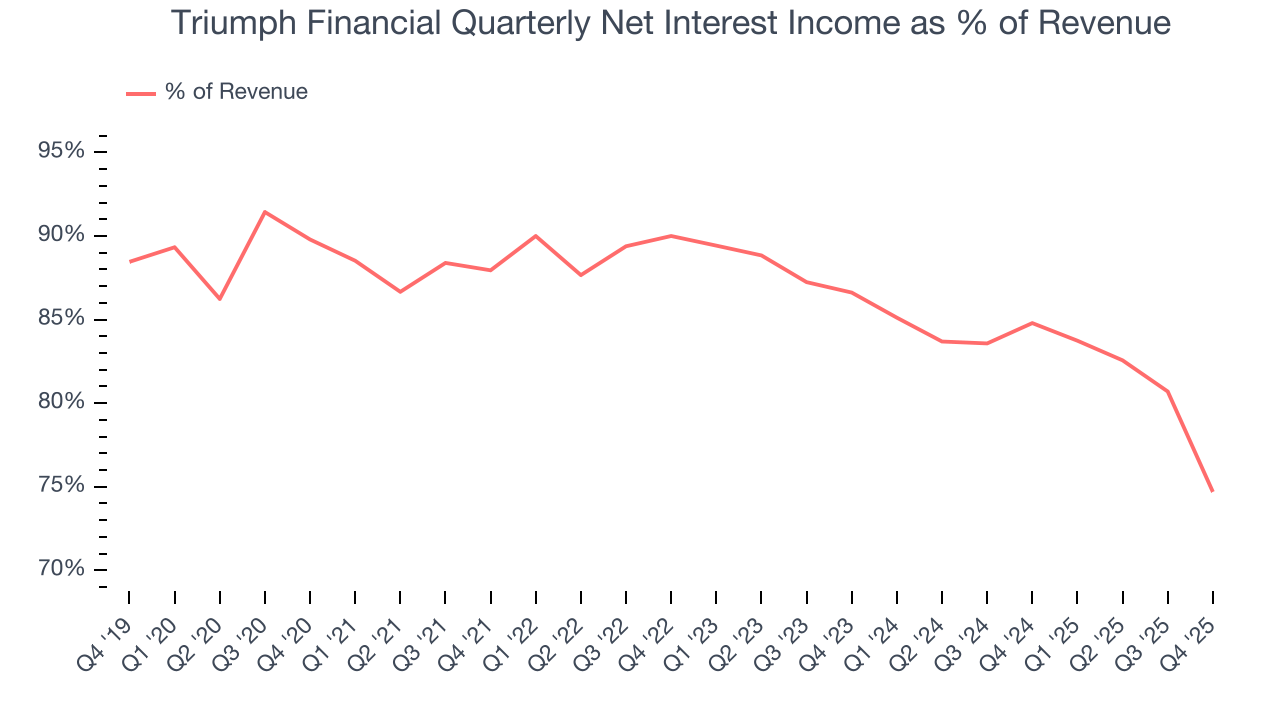

- Net Interest Income: $89.69 million vs analyst estimates of $89.13 million (2.1% year-on-year growth, 0.6% beat)

- Net Interest Margin: 6.4% vs analyst estimates of 6.3% (8.8 basis point beat)

- Revenue: $120.1 million vs analyst estimates of $110.4 million (16% year-on-year growth, 8.8% beat)

- EPS (GAAP): $0.77 vs analyst estimates of $0.30 (significant beat)

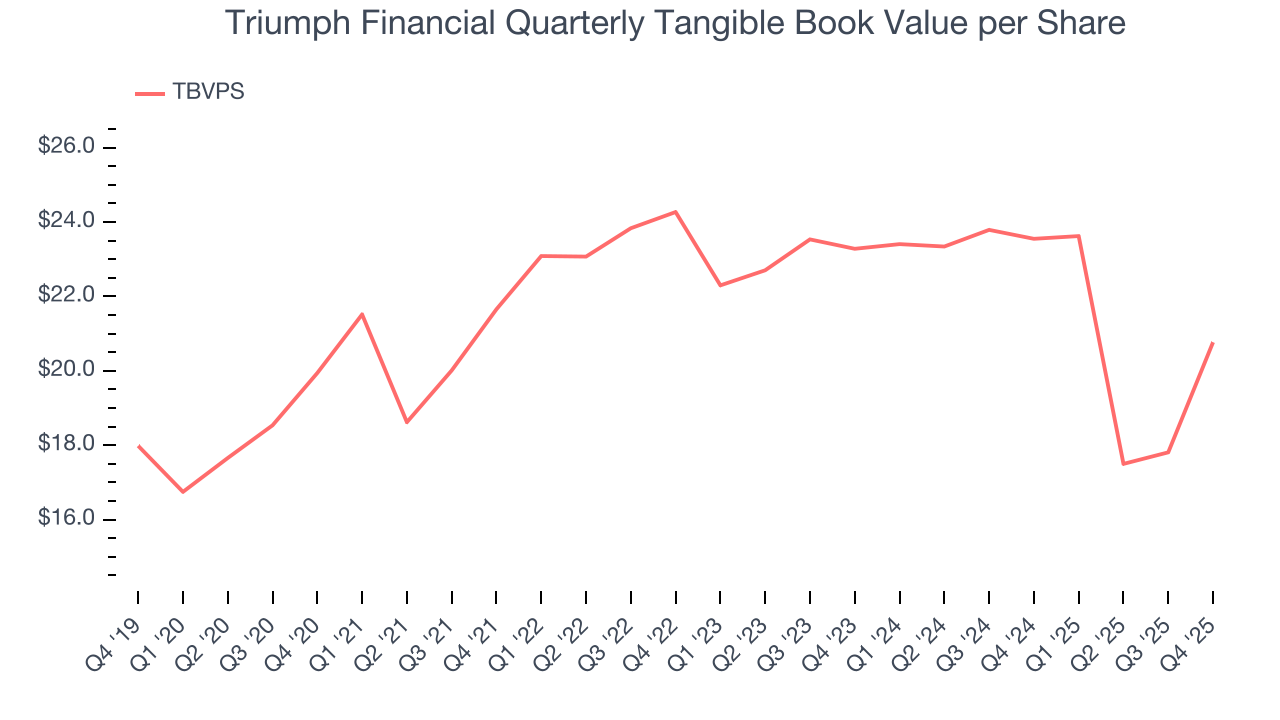

- Tangible Book Value per Share: $20.77 vs analyst estimates of $20.15 (11.8% year-on-year decline, 3.1% beat)

- Market Capitalization: $1.65 billion

Company Overview

Originally focused on traditional banking before pivoting to serve the transportation sector, Triumph Financial (NASDAQ:TFIN) provides specialized financial services to the trucking industry, including payments processing, factoring, banking, and data intelligence solutions.

Triumph Financial operates through four interconnected segments that create a comprehensive ecosystem for the trucking industry. The company's TriumphPay platform serves as a payment network connecting brokers, shippers, factors, and carriers to streamline invoice processing and payments. This platform handles the entire lifecycle from invoice presentment through audit to final payment, reducing friction in transportation payments.

The factoring segment purchases trucking invoices at a discount, providing immediate working capital to carriers who would otherwise wait 30-60 days for payment. This service is particularly valuable to small and mid-sized trucking companies that need consistent cash flow to cover fuel, maintenance, and other operating expenses. In 2024, the company expanded its offerings with Factoring as a Service (FaaS), allowing other businesses to leverage Triumph's back-office factoring infrastructure.

While the company maintains traditional banking operations with 63 branches across several states, its banking services increasingly cater to transportation industry participants. Triumph offers specialized loans for equipment financing, particularly for trucking fleets, alongside conventional commercial lending products. The company's newest segment, Intelligence, leverages data collected through its payment network to provide actionable insights to logistics providers.

Triumph's LoadPay product exemplifies its integrated approach—a digital banking account designed specifically for carriers that enables instant funding of approved invoices without traditional payment delays. This combination of specialized financial services, industry-specific technology, and data intelligence positions Triumph as more than just a bank, but as a financial technology partner to the trucking ecosystem.

4. Regional Banks

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

Triumph Financial competes with traditional banks offering transportation financing like Wells Fargo (NYSE:WFC) and Bank of America (NYSE:BAC), specialized factoring companies such as Crestmark (a division of MetaBank), and payment technology providers like AscendTMS and Truckstop.com in the freight technology space.

5. Sales Growth

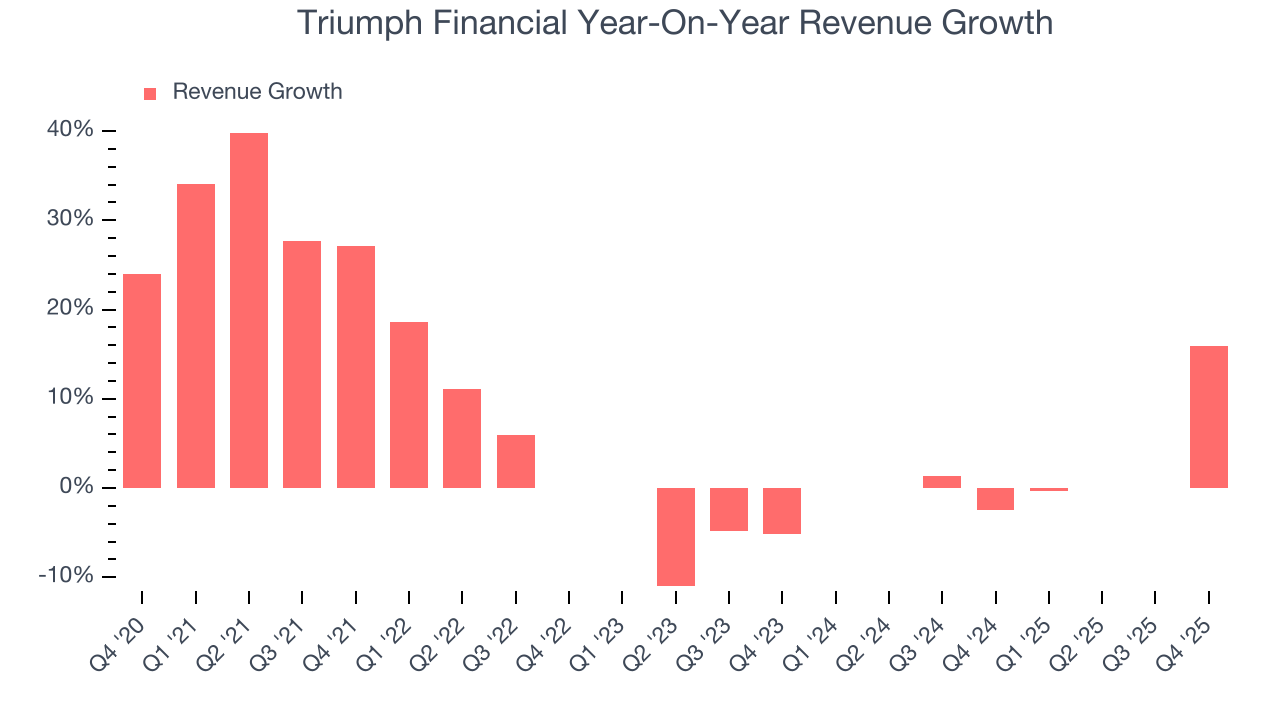

Two primary revenue streams drive bank earnings. While net interest income, which is earned by charging higher rates on loans than paid on deposits, forms the foundation, fee-based services across banking, credit, wealth management, and trading operations provide additional income. Regrettably, Triumph Financial’s revenue grew at a tepid 6.5% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Triumph Financial’s recent performance shows its demand has slowed as its annualized revenue growth of 2.2% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Triumph Financial reported year-on-year revenue growth of 16%, and its $120.1 million of revenue exceeded Wall Street’s estimates by 8.8%.

Net interest income made up 86% of the company’s total revenue during the last five years, meaning Triumph Financial barely relies on non-interest income to drive its overall growth.

Markets consistently prioritize net interest income growth over fee-based revenue, recognizing its superior quality and recurring nature compared to the more unpredictable non-interest income streams.

6. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Triumph Financial, its EPS declined by 18.1% annually over the last five years while its revenue grew by 6.5%. This tells us the company became less profitable on a per-share basis as it expanded due to factors such as interest expenses and taxes.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Triumph Financial’s two-year annual EPS declines of 23.8% were bad and lower than its 2.2% two-year revenue growth.

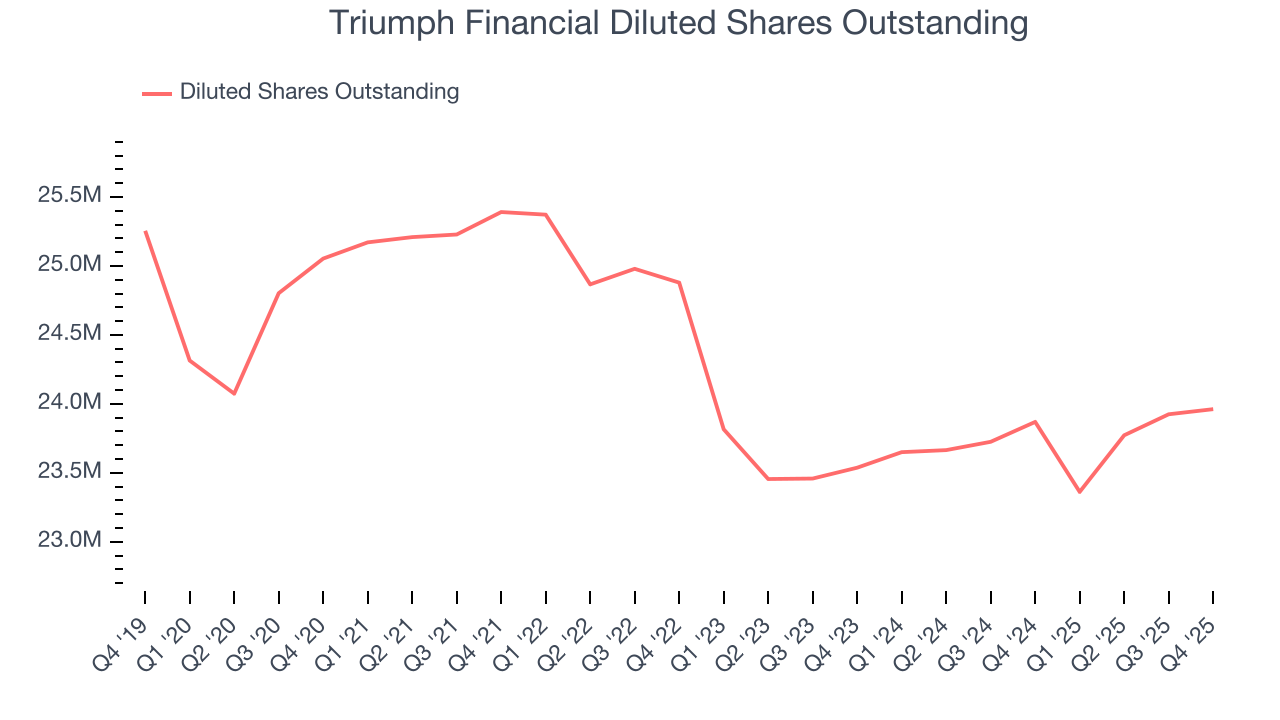

We can take a deeper look into Triumph Financial’s earnings to better understand the drivers of its performance. A two-year view shows Triumph Financial has diluted its shareholders, growing its share count by 1.8%. This has led to lower per share earnings. Taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Triumph Financial reported EPS of $0.77, up from $0.13 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Triumph Financial’s full-year EPS of $0.93 to grow 87.5%.

7. Tangible Book Value Per Share (TBVPS)

Banks operate as balance sheet businesses, with profits generated through borrowing and lending activities. Valuations reflect this reality, emphasizing balance sheet strength and long-term book value compounding ability.

When analyzing banks, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value by removing intangible assets of debatable liquidation worth. Traditional metrics like EPS are helpful but face distortion from M&A activity and loan loss accounting rules.

Triumph Financial’s TBVPS was flat over the last five years. A turnaround doesn’t seem to be in sight as its TBVPS also dropped by 5.6% annually over the last two years ($23.28 to $20.77 per share).

Over the next 12 months, Consensus estimates call for Triumph Financial’s TBVPS to grow by 8.1% to $22.46, paltry growth rate.

8. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, Triumph Financial has averaged a Tier 1 capital ratio of 10.5%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

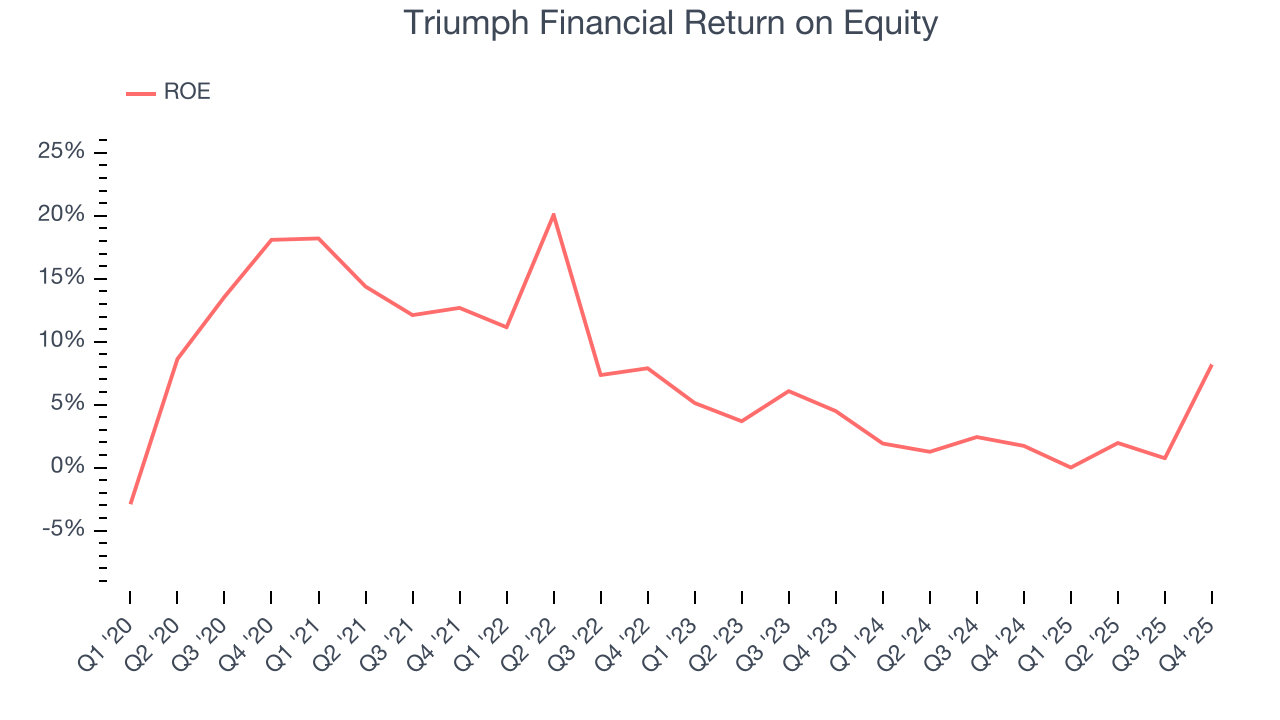

9. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Triumph Financial has averaged an ROE of 7.1%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

10. Key Takeaways from Triumph Financial’s Q4 Results

It was good to see Triumph Financial beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $70.55 immediately after reporting.

11. Is Now The Time To Buy Triumph Financial?

Updated: January 26, 2026 at 4:31 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Triumph Financial doesn’t pass our quality test. To kick things off, its revenue growth was uninspiring over the last five years, and analysts don’t see anything changing over the next 12 months. And while its admirable net interest margin a wonderful starting point for the overall profitability of the business, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its declining net interest margin shows its loan book is becoming less profitable.

Triumph Financial’s P/B ratio based on the next 12 months is 1.8x. This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $66 on the company (compared to the current share price of $70.55), implying they don’t see much short-term potential in Triumph Financial.