Tandem Diabetes (TNDM)

Tandem Diabetes is in for a bumpy ride. Not only has its sales growth been weak but also its negative returns on capital show it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think Tandem Diabetes Will Underperform

With technology that automatically adjusts insulin delivery based on continuous glucose monitoring data, Tandem Diabetes Care (NASDAQ:TNDM) develops and manufactures automated insulin delivery systems that help people with diabetes manage their blood glucose levels.

- Earnings per share fell by 18.5% annually over the last five years while its revenue grew, showing its incremental sales were much less profitable

- Negative returns on capital show that some of its growth strategies have backfired, and its decreasing returns suggest its historical profit centers are aging

- Negative earnings profile makes it challenging to secure favorable financing terms from lenders

Tandem Diabetes’s quality doesn’t meet our expectations. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Tandem Diabetes

At $21.59 per share, Tandem Diabetes trades at 26.7x forward EV-to-EBITDA. This multiple is higher than most healthcare companies, and we think it’s quite expensive for the quality you get.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Tandem Diabetes (TNDM) Research Report: Q4 CY2025 Update

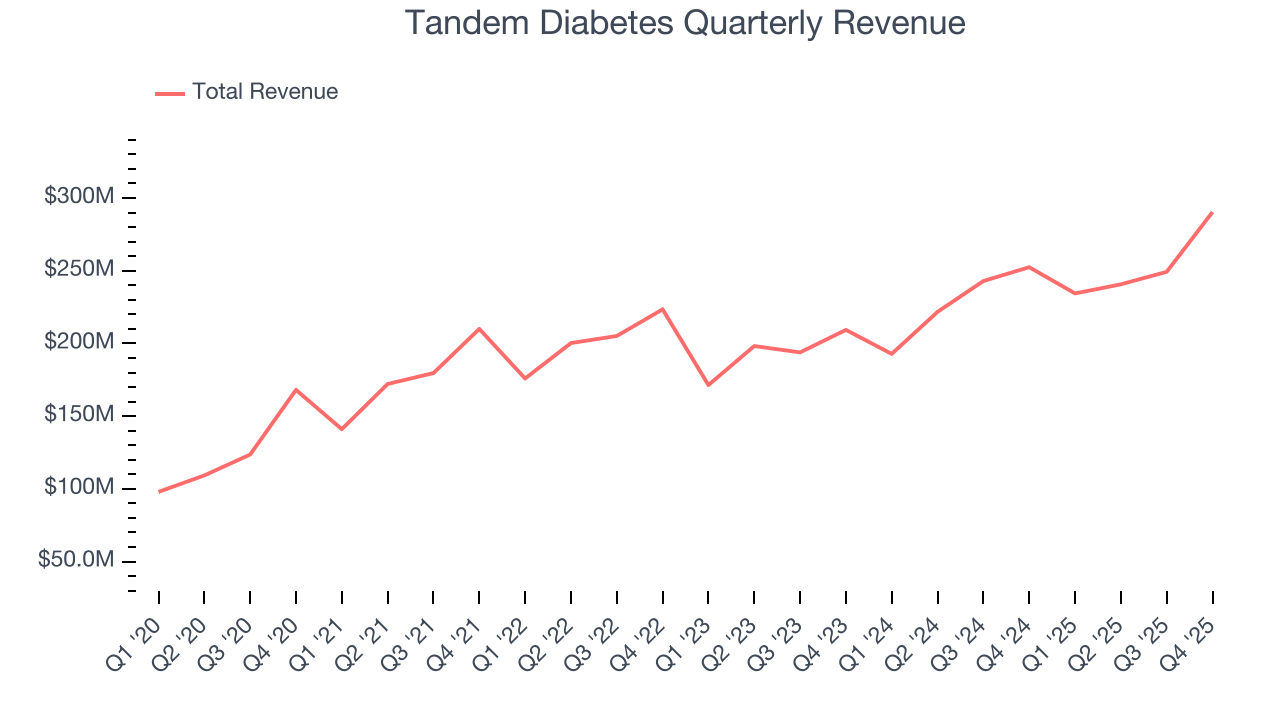

Diabetes technology company Tandem Diabetes Care (NASDAQ:TNDM) reported Q4 CY2025 results beating Wall Street’s revenue expectations, with sales up 15% year on year to $290.4 million. Its GAAP loss of $0.01 per share was 84.4% above analysts’ consensus estimates.

Tandem Diabetes (TNDM) Q4 CY2025 Highlights:

- Revenue: $290.4 million vs analyst estimates of $276.7 million (15% year-on-year growth, 4.9% beat)

- EPS (GAAP): -$0.01 vs analyst estimates of -$0.06 (84.4% beat)

- Operating Margin: 2.9%, up from -0.2% in the same quarter last year

- Market Capitalization: $1.28 billion

Company Overview

With technology that automatically adjusts insulin delivery based on continuous glucose monitoring data, Tandem Diabetes Care (NASDAQ:TNDM) develops and manufactures automated insulin delivery systems that help people with diabetes manage their blood glucose levels.

Tandem's flagship products include the t:slim X2 insulin pump and the newer, smaller Tandem Mobi system. Both devices feature the company's Control-IQ technology, an advanced hybrid closed-loop system that automatically adjusts insulin delivery based on readings from compatible continuous glucose monitors (CGMs). This technology helps users maintain their blood glucose within target ranges by increasing, decreasing, or suspending insulin delivery as needed, and can even deliver automatic correction doses when glucose levels rise too high.

The company's pumps are designed with user experience in mind, featuring touchscreen interfaces, Bluetooth connectivity, and software that can be updated remotely through a personal computer. This allows users to access new features without replacing their hardware. For example, existing t:slim X2 users can update their pumps to integrate with newer CGM sensors as they become available.

Tandem's revenue comes primarily from selling insulin pumps and the disposable supplies needed to use them, including insulin cartridges and infusion sets that need to be replaced every few days. A patient might use a Tandem pump to manage their diabetes by wearing the device (about the size of a small smartphone for the t:slim X2 or a car key fob for the Mobi), which delivers insulin through a thin tube connected to an infusion set attached to their body.

The company has expanded its CGM integration partnerships to include both Dexcom and Abbott sensors, giving patients more options for customizing their diabetes management systems. Tandem also offers digital tools like the Tandem Source data management platform, which allows users and healthcare providers to visualize diabetes data and identify trends.

Beyond its current product lineup, Tandem is developing new innovations including a tubeless patch pump option, extended-wear infusion sets, and enhancements to its Control-IQ algorithm. The company is also working to expand its addressable market by conducting clinical trials to support the use of its technology in people with type 2 diabetes who require intensive insulin therapy.

4. Healthcare Technology for Patients

The consumer-focused healthcare technology sector leverages digital platforms to make healthcare more accessible and affordable, offering services like telemedicine and prescription discounts. Looking forward, growth is supported by increasing consumer comfort with telehealth and the demand for cost-saving tools amidst rising healthcare expenses. AI-powered diagnostics and personalized digital care also present significant opportunities. However, the sector faces headwinds from heightened competition as large technology and established healthcare companies expand their digital presence.

Tandem Diabetes Care competes with Insulet Corporation (NASDAQ:PODD), which makes the tubeless Omnipod insulin delivery system, Medtronic (NYSE:MDT), a medical device giant with a diabetes division that produces insulin pumps, and privately-held Ypsomed, a European medical technology company that manufactures insulin pumps and injection systems.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.01 billion in revenue over the past 12 months, Tandem Diabetes is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

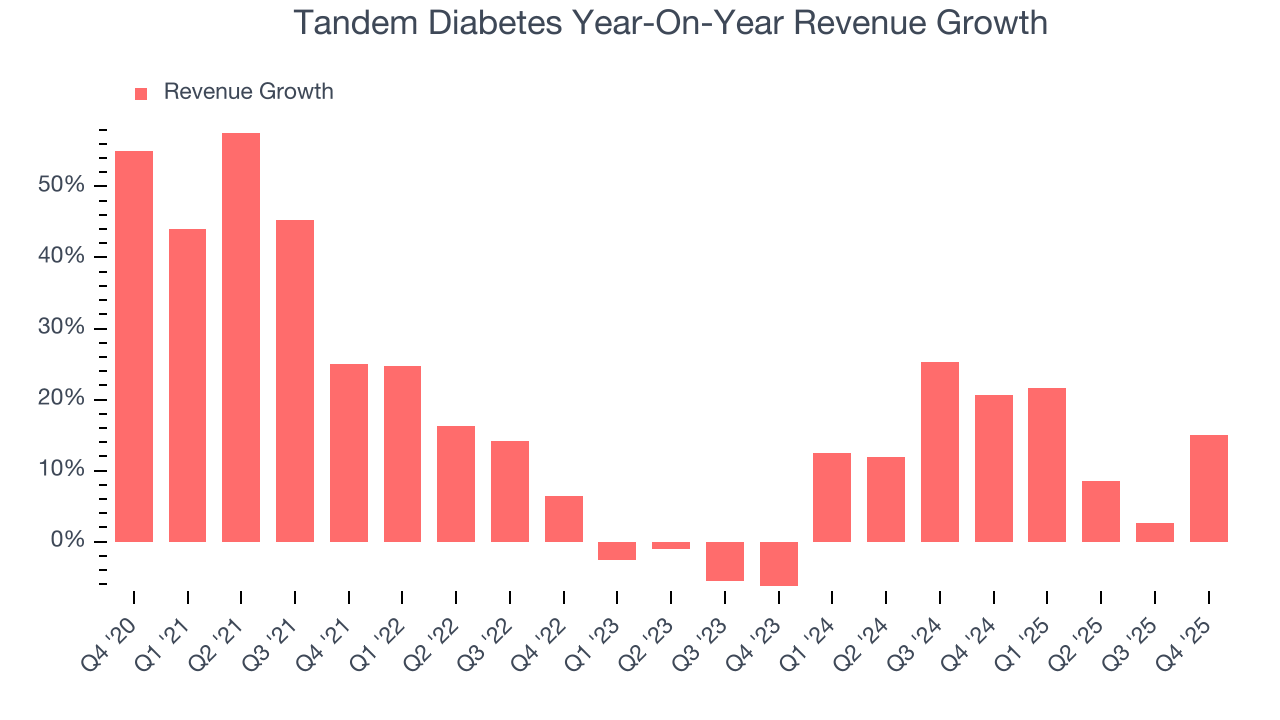

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Luckily, Tandem Diabetes’s sales grew at a solid 15.3% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Tandem Diabetes’s annualized revenue growth of 14.6% over the last two years aligns with its five-year trend, suggesting its demand was predictably strong.

This quarter, Tandem Diabetes reported year-on-year revenue growth of 15%, and its $290.4 million of revenue exceeded Wall Street’s estimates by 4.9%.

Looking ahead, sell-side analysts expect revenue to grow 8.4% over the next 12 months, a deceleration versus the last two years. Still, this projection is admirable and indicates the market is baking in success for its products and services.

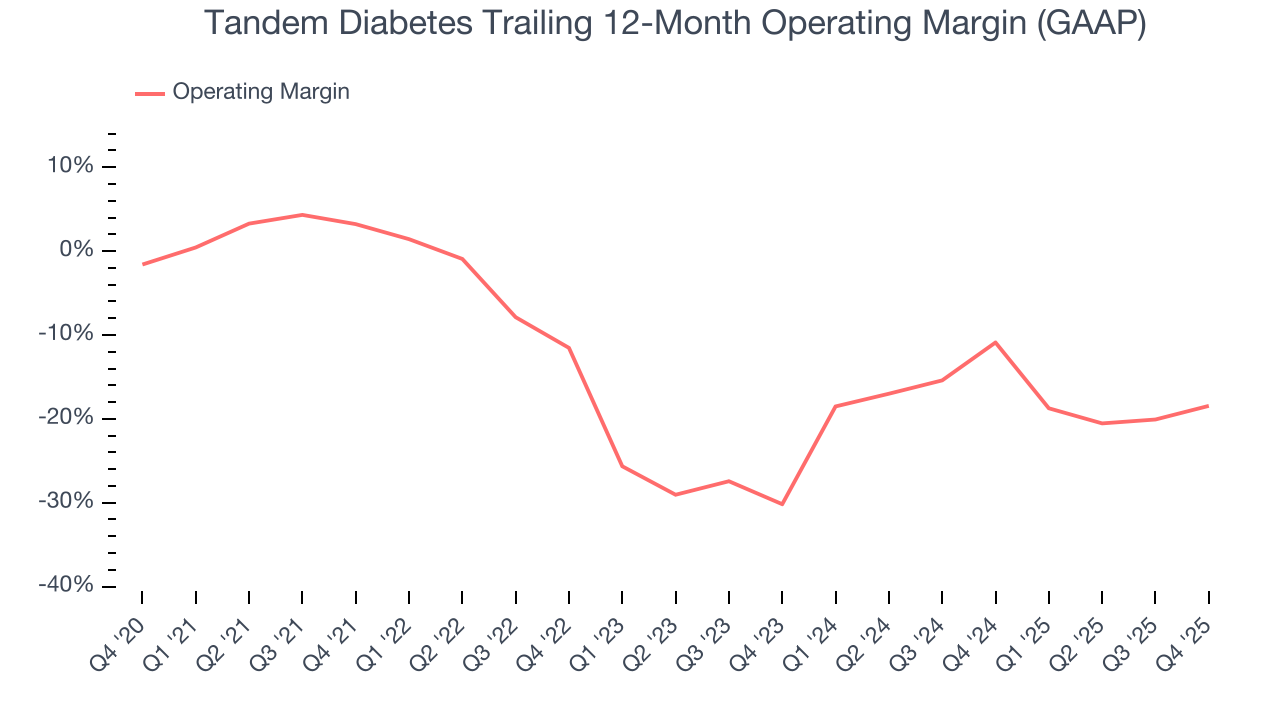

7. Operating Margin

Although Tandem Diabetes was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 14% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Tandem Diabetes’s operating margin decreased by 21.7 percentage points over the last five years, but it rose by 11.7 percentage points on a two-year basis. Still, shareholders will want to see Tandem Diabetes become more profitable in the future.

This quarter, Tandem Diabetes generated an operating margin profit margin of 2.9%, up 3.1 percentage points year on year. This increase was a welcome development and shows it was more efficient.

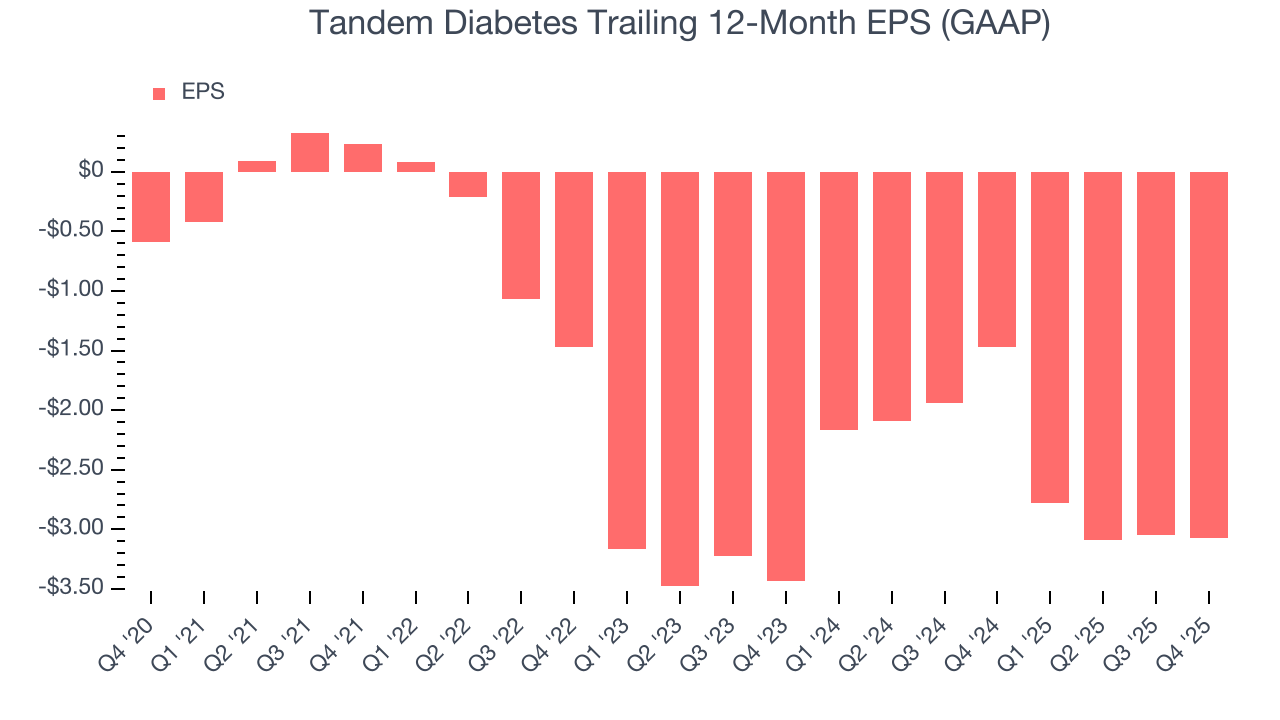

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Tandem Diabetes’s earnings losses deepened over the last five years as its EPS dropped 39% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Tandem Diabetes’s low margin of safety could leave its stock price susceptible to large downswings.

In Q4, Tandem Diabetes reported EPS of negative $0.01, down from $0.01 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Tandem Diabetes to improve its earnings losses. Analysts forecast its full-year EPS of negative $3.07 will advance to negative $1.00.

9. Cash Is King

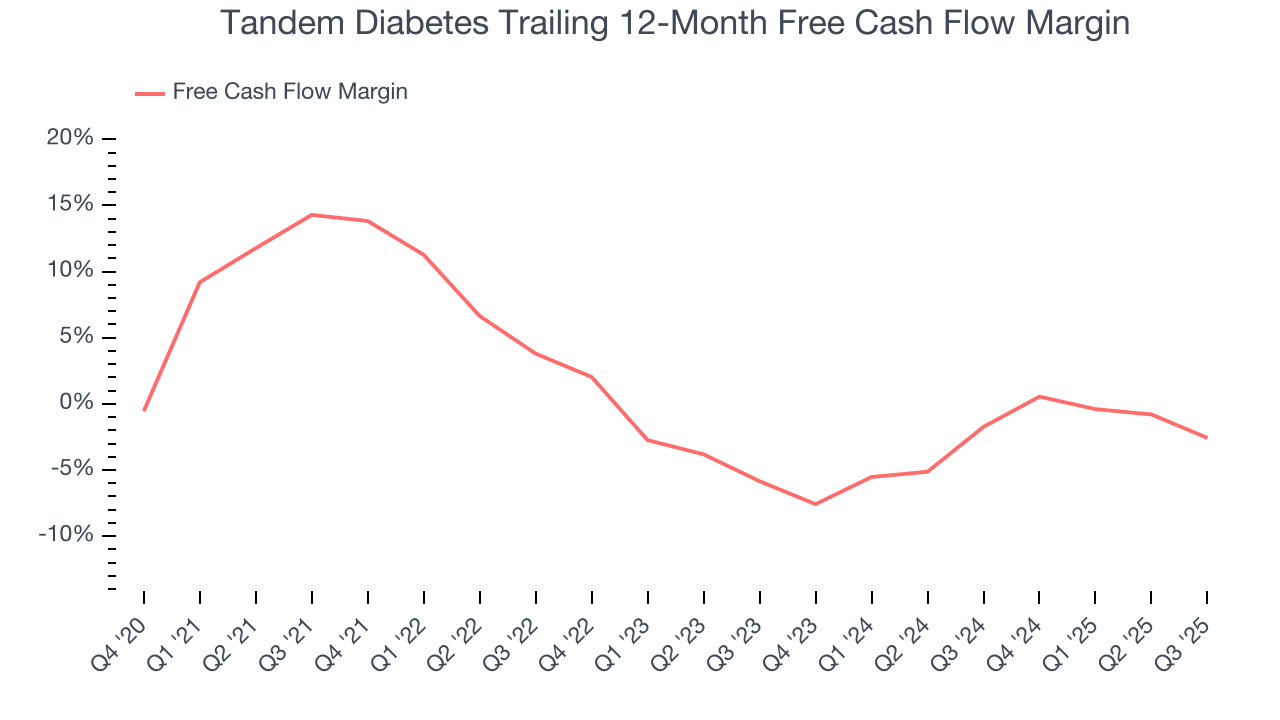

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Tandem Diabetes broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, we can see that Tandem Diabetes’s margin dropped by 21.4 percentage points during that time. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s in the middle of a big investment cycle.

10. Return on Invested Capital (ROIC)

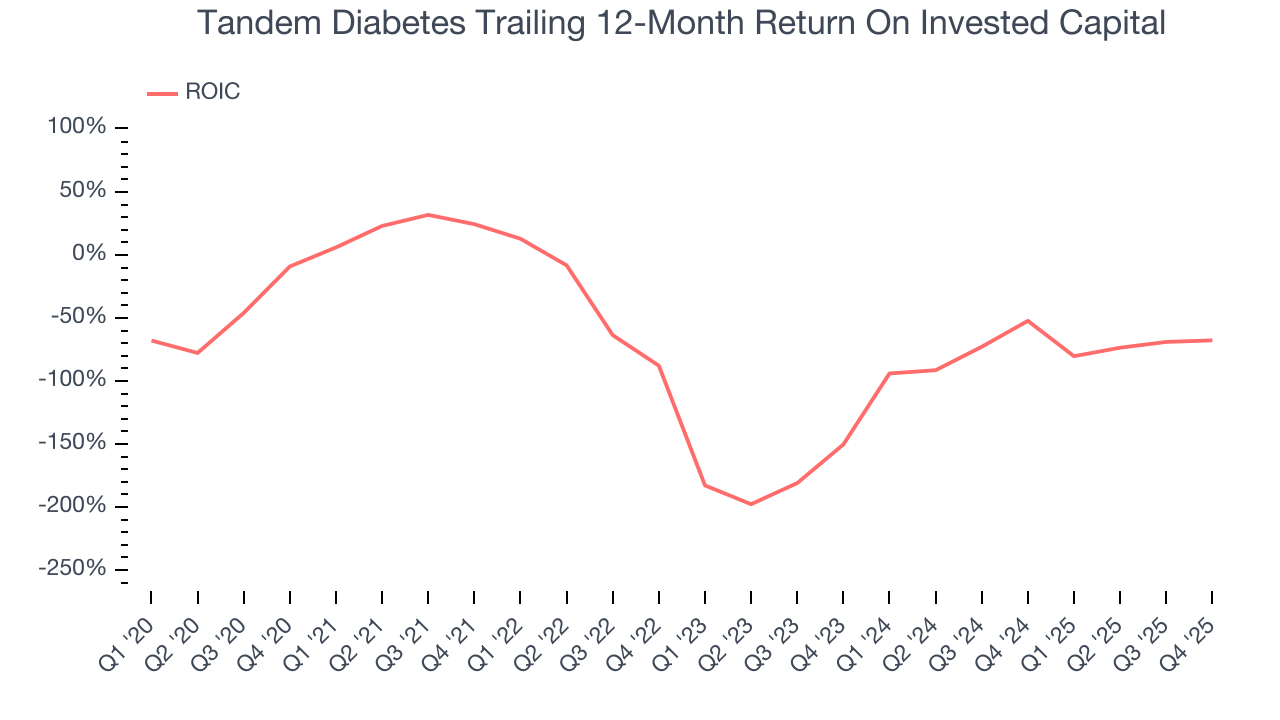

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Tandem Diabetes’s five-year average ROIC was negative 45.9%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Tandem Diabetes’s ROIC has decreased significantly over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

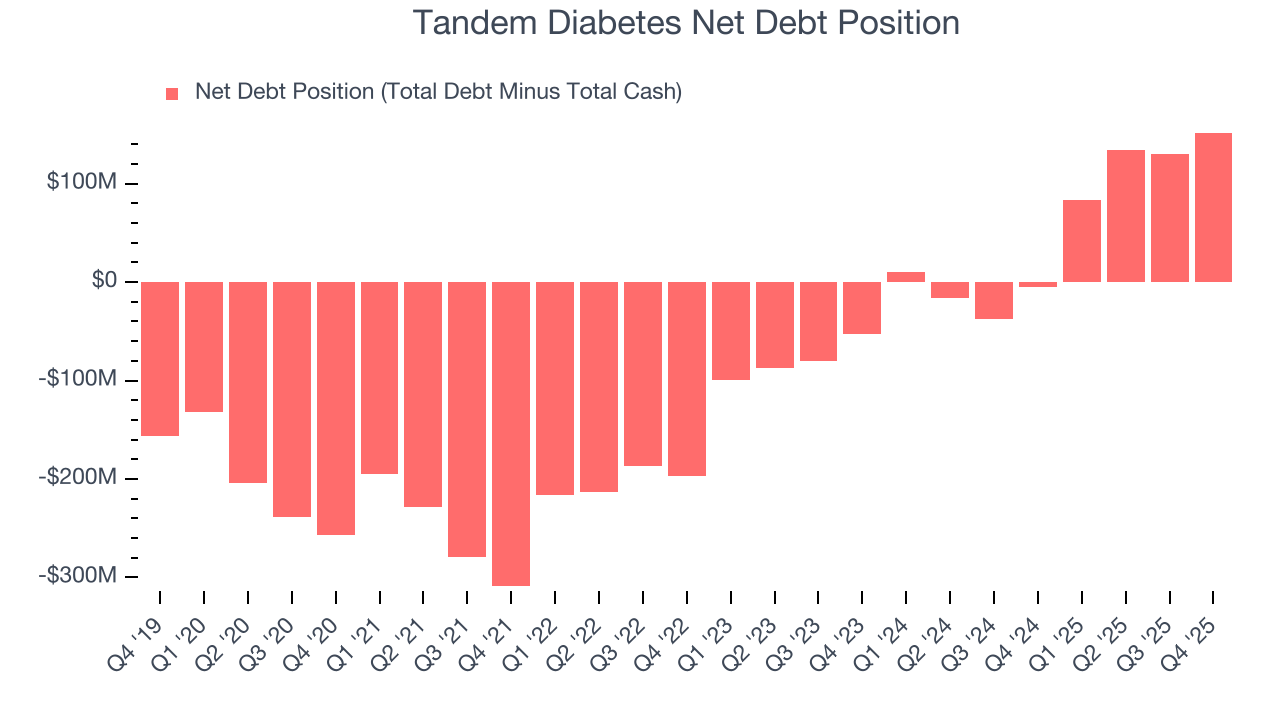

Tandem Diabetes posted negative $46.09 million of EBITDA over the last 12 months, and its $444.5 million of debt exceeds the $292.7 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Tandem Diabetes if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Tandem Diabetes can improve its profitability and remain cautious until then.

12. Key Takeaways from Tandem Diabetes’s Q4 Results

It was good to see Tandem Diabetes beat analysts’ EPS expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance missed. Overall, this print had some key positives. The stock traded up 1.5% to $18.81 immediately after reporting.

13. Is Now The Time To Buy Tandem Diabetes?

Updated: March 15, 2026 at 11:48 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Tandem Diabetes.

We see the value of companies making people healthier, but in the case of Tandem Diabetes, we’re out. Although its revenue growth was solid over the last five years, it’s expected to deteriorate over the next 12 months and its diminishing returns show management's prior bets haven't worked out. And while the company’s growth in pump shipments was surging, the downside is its relatively low ROIC suggests management has struggled to find compelling investment opportunities.

Tandem Diabetes’s EV-to-EBITDA ratio based on the next 12 months is 26.7x. This valuation tells us a lot of optimism is priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $29.59 on the company (compared to the current share price of $21.59).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.