LendingTree (TREE)

LendingTree is up against the odds. Its lack of sales growth shows demand is soft, a concerning sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why We Think LendingTree Will Underperform

Using the same comparison model that revolutionized travel booking, LendingTree (NASDAQ:TREE) operates an online platform that connects consumers with financial service providers across mortgages, personal loans, credit cards, insurance, and other financial products.

- Expensive marketing campaigns hurt its profitability and make us wonder what would happen if it let up on the gas

- Flat sales over the last three years suggest it must innovate and find new ways to grow

- Estimated sales growth of 8.5% for the next 12 months is soft and implies weaker demand

LendingTree falls short of our quality standards. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than LendingTree

LendingTree’s stock price of $37.34 implies a valuation ratio of 6.2x forward EV/EBITDA. This is a cheap valuation multiple, but for good reason. You get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. LendingTree (TREE) Research Report: Q4 CY2025 Update

Financial marketplace platform LendingTree (NASDAQ:TREE) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 22.3% year on year to $319.7 million. On top of that, next quarter’s revenue guidance ($321 million at the midpoint) was surprisingly good and 16.5% above what analysts were expecting. Its non-GAAP loss of $0.39 per share was significantly below analysts’ consensus estimates.

LendingTree (TREE) Q4 CY2025 Highlights:

- Revenue: $319.7 million vs analyst estimates of $286.8 million (22.3% year-on-year growth, 11.5% beat)

- Adjusted EPS: -$0.39 vs analyst estimates of $0.87 (significant miss)

- Adjusted EBITDA: $36.67 million vs analyst estimates of $30.68 million (11.5% margin, 19.5% beat)

- Revenue Guidance for Q1 CY2026 is $321 million at the midpoint, above analyst estimates of $275.6 million

- EBITDA guidance for the upcoming financial year 2026 is $155 million at the midpoint, above analyst estimates of $143.9 million

- Operating Margin: 7%, in line with the same quarter last year

- Market Capitalization: $510.9 million

Company Overview

Using the same comparison model that revolutionized travel booking, LendingTree (NASDAQ:TREE) operates an online platform that connects consumers with financial service providers across mortgages, personal loans, credit cards, insurance, and other financial products.

The company positions itself as a neutral marketplace where consumers can shop for financial products by submitting a single application and receiving multiple offers from competing providers. This approach allows consumers to compare rates, terms, and conditions side-by-side before making financial decisions. LendingTree earns revenue primarily through match fees when it connects consumers with its network of approximately 430 financial partners.

For example, a homebuyer seeking mortgage options can submit their information once and receive conditional loan offers from multiple lenders, allowing them to compare interest rates and terms without individually contacting each bank. Similarly, someone seeking auto insurance can receive quotes from various insurers after completing a single form.

LendingTree's business is organized into three primary segments: Home (mortgage loans and home equity products), Consumer (credit cards, personal loans, auto loans, and deposit accounts), and Insurance (comparison shopping for various insurance types). The company monetizes these connections primarily through upfront match fees, pay-per-click arrangements, and in some cases, commissions on policy sales through its agency businesses. LendingTree also offers supplementary tools like free credit scores to facilitate comparison shopping and build user engagement.

4. Financial Technology

Financial technology companies benefit from the increasing consumer demand for digital payments, banking, and finance. Tailwinds fueling this trend include e-commerce along with improvements in blockchain infrastructure and AI-driven credit underwriting, which make access to money faster and cheaper. Despite regulatory scrutiny and resistance from traditional financial institutions, fintechs are poised for long-term growth as they disrupt legacy systems by expanding financial services to underserved population segments.

LendingTree's competitors include other financial comparison platforms such as Credit Karma (owned by Intuit, NASDAQ:INTU), NerdWallet (NASDAQ:NRDS), and Bankrate (owned by Red Ventures), as well as specialized mortgage marketplaces like Rocket Companies (NYSE:RKT).

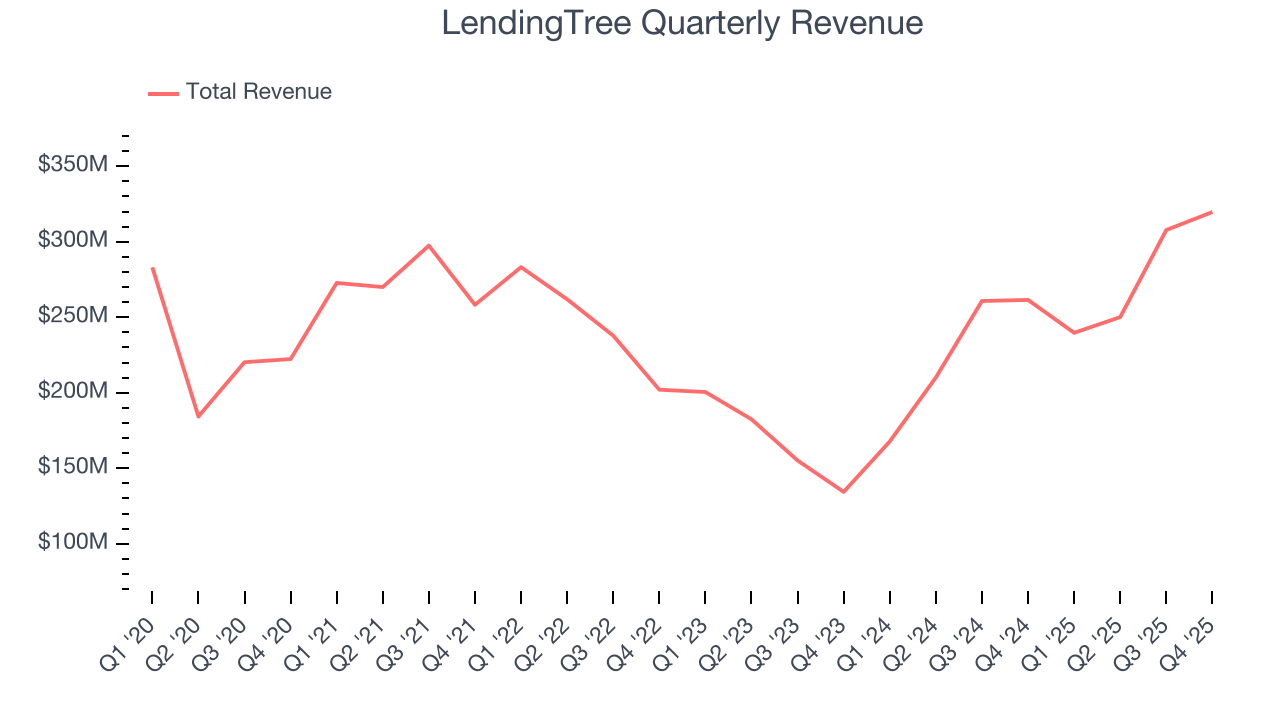

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, LendingTree’s sales grew at a sluggish 4.3% compounded annual growth rate over the last three years. This fell short of our benchmark for the consumer internet sector and is a rough starting point for our analysis.

This quarter, LendingTree reported robust year-on-year revenue growth of 22.3%, and its $319.7 million of revenue topped Wall Street estimates by 11.5%. Company management is currently guiding for a 33.9% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 3.5% over the next 12 months, similar to its three-year rate. This projection is underwhelming and indicates its newer products and services will not lead to better top-line performance yet.

6. Gross Margin & Pricing Power

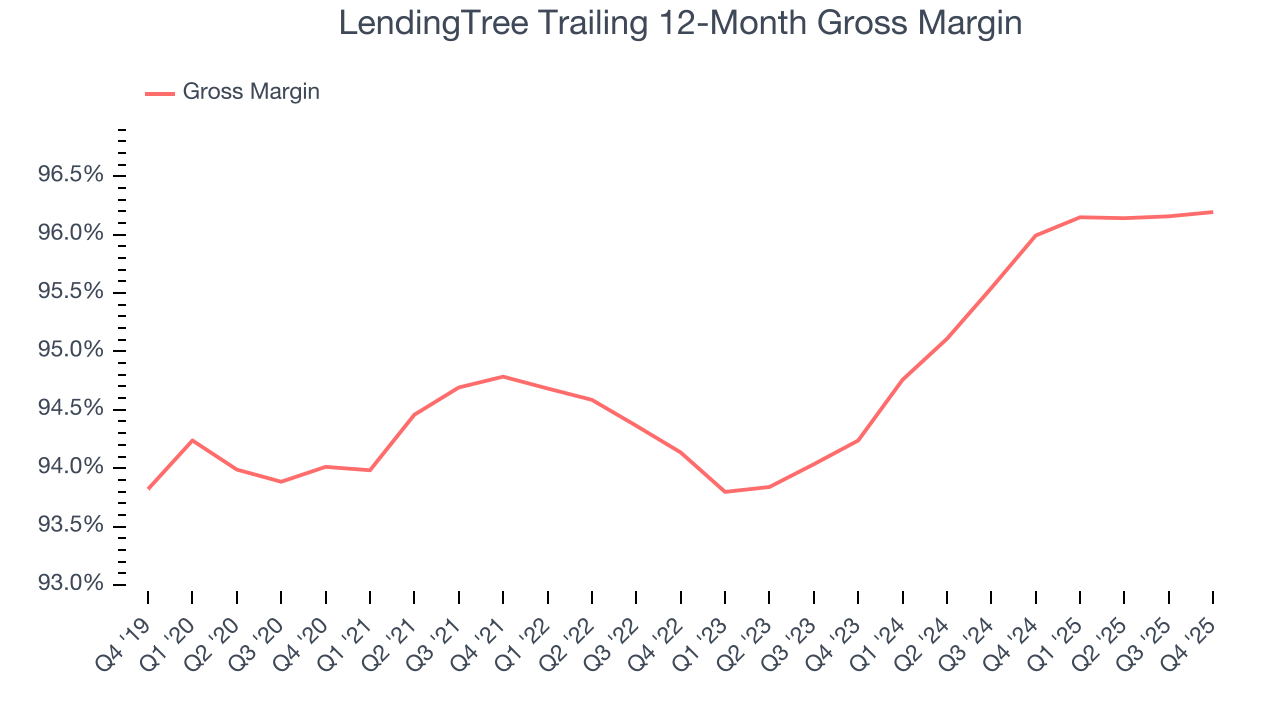

For fintech businesses like LendingTree, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include transaction/payment processing, hosting, and bandwidth fees in addition to the costs necessary to onboard customers, such as identity verification.

LendingTree’s gross margin is one of the highest in the consumer internet sector, an output of its asset-lite business model and strong pricing power. It also enables the company to fund large investments in product and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an elite 96.1% gross margin over the last two years. That means LendingTree only paid its providers $3.90 for every $100 in revenue.

LendingTree’s gross profit margin came in at 96.4% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

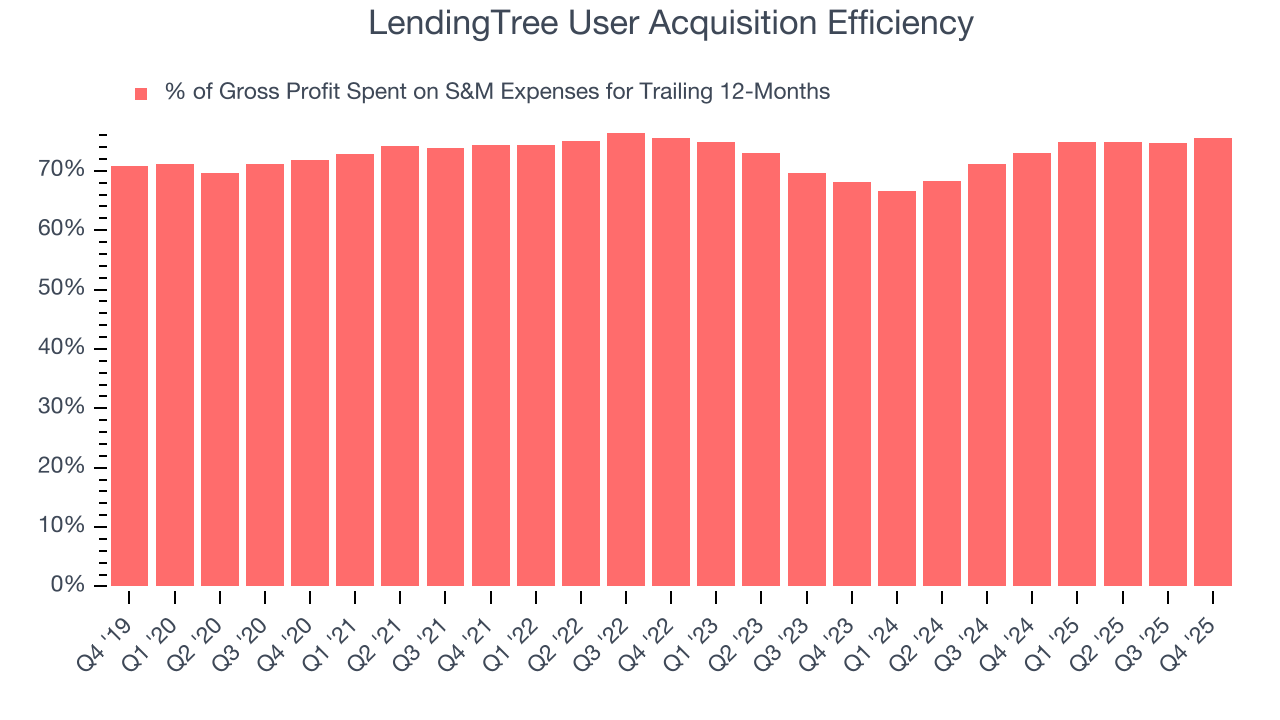

7. User Acquisition Efficiency

Consumer internet businesses like LendingTree grow from a combination of product virality, paid advertisement, and incentives (unlike enterprise software products, which are often sold by dedicated sales teams).

It’s very expensive for LendingTree to acquire new users as the company has spent 75.5% of its gross profit on sales and marketing expenses over the last year. This inefficiency indicates a highly competitive environment with little differentiation between LendingTree and its peers.

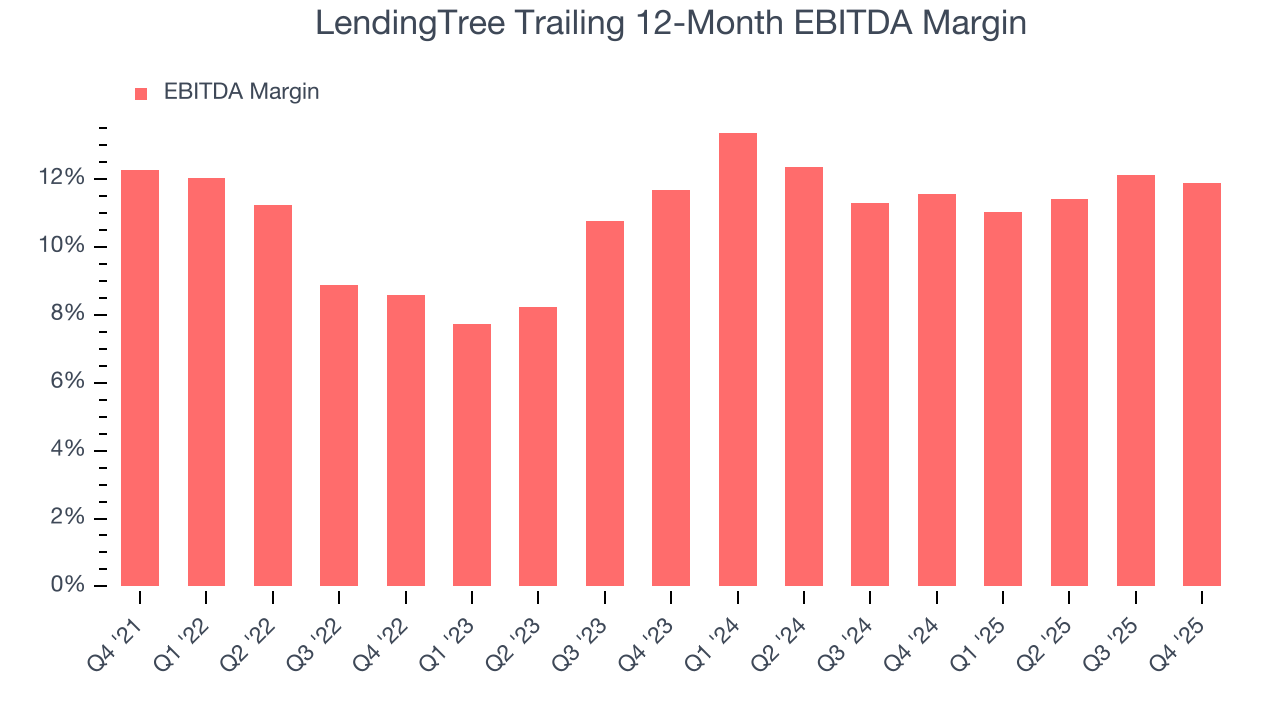

8. EBITDA

Investors regularly analyze operating income to understand a company’s profitability. Similarly, EBITDA is a common profitability metric for consumer internet companies because it excludes various one-time or non-cash expenses, offering a better perspective of the business’s profit potential.

LendingTree has been an efficient company over the last two years. It was one of the more profitable businesses in the consumer internet sector, boasting an average EBITDA margin of 11.7%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, LendingTree’s EBITDA margin rose by 3.3 percentage points over the last few years, as its sales growth gave it operating leverage.

This quarter, LendingTree generated an EBITDA margin profit margin of 11.5%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

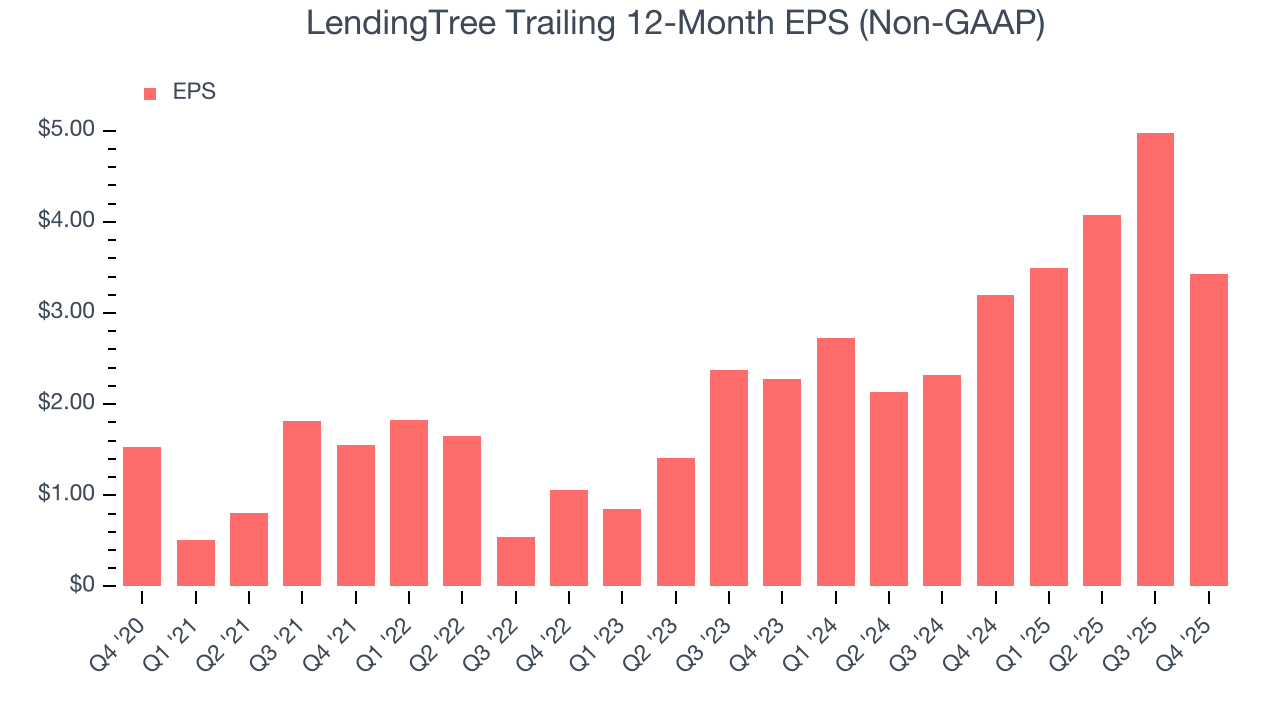

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

LendingTree’s EPS grew at an astounding 47.9% compounded annual growth rate over the last three years, higher than its 4.3% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into LendingTree’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, LendingTree’s EBITDA margin was flat this quarter but expanded by 3.3 percentage points over the last three years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, LendingTree reported adjusted EPS of negative $0.39, down from $1.16 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects LendingTree’s full-year EPS of $3.43 to grow 42.7%.

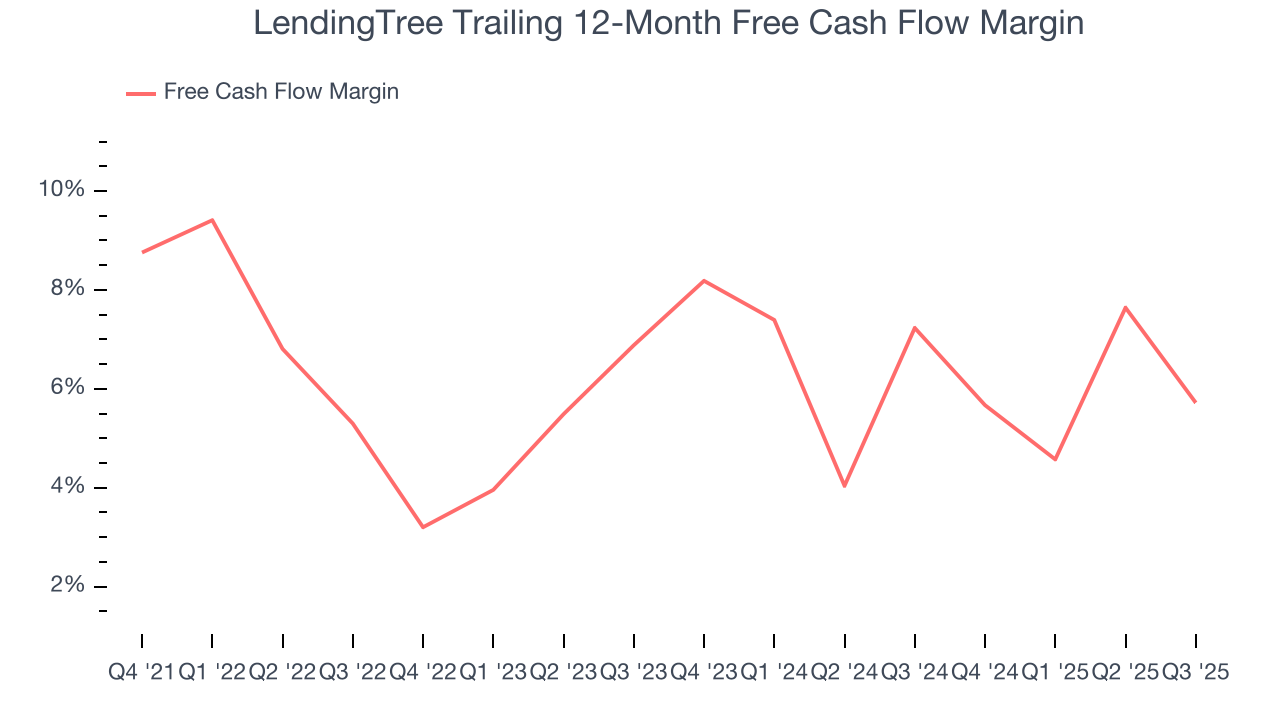

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

LendingTree has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.8% over the last two years, slightly better than the broader consumer internet sector.

Taking a step back, we can see that LendingTree’s margin expanded by 3.7 percentage points over the last few years. This is encouraging because it gives the company more optionality.

11. Balance Sheet Assessment

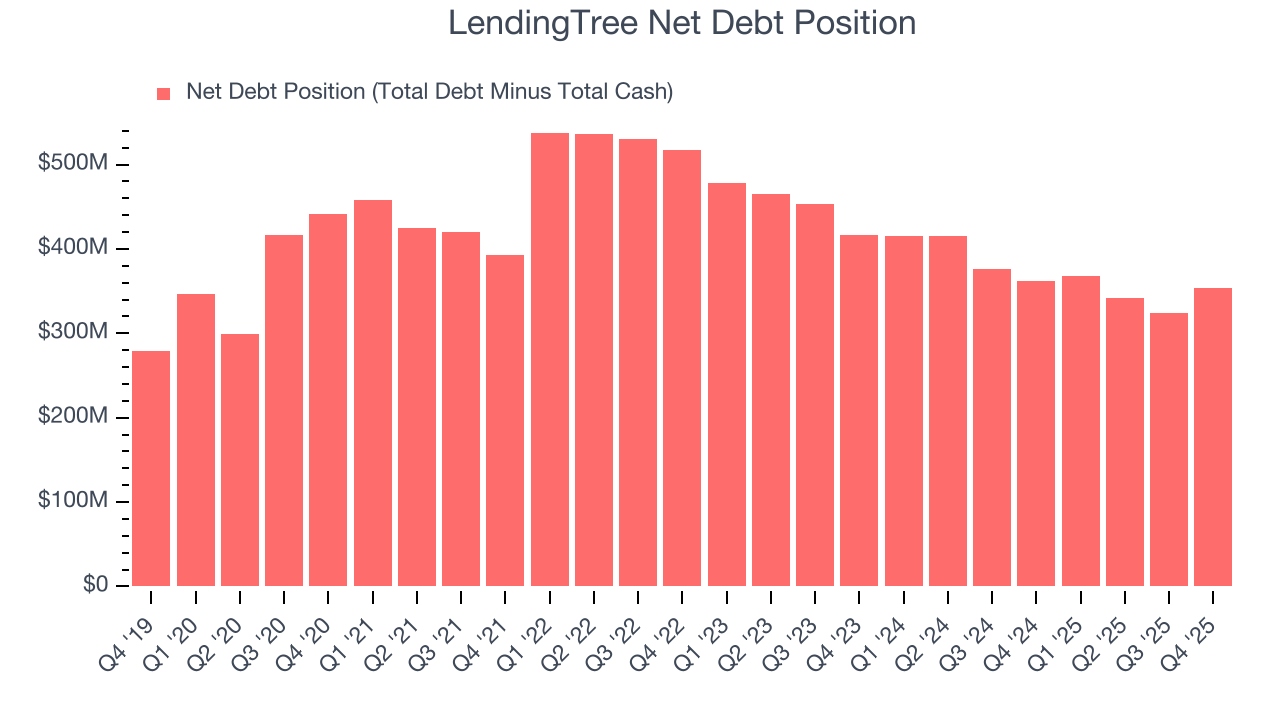

LendingTree reported $81.07 million of cash and $435.2 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $132.9 million of EBITDA over the last 12 months, we view LendingTree’s 2.7× net-debt-to-EBITDA ratio as safe. We also see its $47.39 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from LendingTree’s Q4 Results

We were impressed by LendingTree’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its EBITDA outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 14.7% to $43.29 immediately following the results.

13. Is Now The Time To Buy LendingTree?

Updated: March 2, 2026 at 4:48 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in LendingTree.

LendingTree isn’t a terrible business, but it doesn’t pass our quality test. For starters, its revenue growth was weak over the last three years, and analysts don’t see anything changing over the next 12 months. And while LendingTree’s admirable gross margins are a wonderful starting point for the overall profitability of the business, its sales and marketing spend is very high compared to other consumer internet businesses.

LendingTree’s EV/EBITDA ratio based on the next 12 months is 6.1x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $81.33 on the company (compared to the current share price of $43.29).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.