United Bankshares (UBSI)

United Bankshares is in for a bumpy ride. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think United Bankshares Will Underperform

With roots dating back to 1982 and a strong presence in the Mid-Atlantic region, United Bankshares (NASDAQ:UBSI) is a bank holding company that provides commercial and retail banking services through its United Bank subsidiary across multiple states.

- Earnings growth over the last five years fell short of the peer group average as its EPS only increased by 4.6% annually

- Annual net interest income growth of 4.8% over the last five years was below our standards for the banking sector

- 3.4% annual revenue growth over the last five years was slower than its banking peers

United Bankshares’s quality isn’t great. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than United Bankshares

United Bankshares’s stock price of $39.93 implies a valuation ratio of 1x forward P/B. Yes, this valuation multiple is lower than that of other banking peers, but we’ll remind you that you often get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. United Bankshares (UBSI) Research Report: Q4 CY2025 Update

Regional banking company United Bankshares (NASDAQ:UBSI) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 20.9% year on year to $318.4 million. Its non-GAAP profit of $0.91 per share was 6.1% above analysts’ consensus estimates.

United Bankshares (UBSI) Q4 CY2025 Highlights:

- Net Interest Income: $287.5 million vs analyst estimates of $284 million (23.6% year-on-year growth, 1.2% beat)

- Net Interest Margin: 3.8% vs analyst estimates of 3.8% (5 basis point beat)

- Revenue: $318.4 million vs analyst estimates of $315.7 million (20.9% year-on-year growth, 0.9% beat)

- Efficiency Ratio: 47.7% vs analyst estimates of 48.4% (71 basis point beat)

- Adjusted EPS: $0.91 vs analyst estimates of $0.86 (6.1% beat)

- Tangible Book Value per Share: $24.63 vs analyst estimates of $24.49 (7.4% year-on-year growth, 0.6% beat)

- Market Capitalization: $5.99 billion

Company Overview

With roots dating back to 1982 and a strong presence in the Mid-Atlantic region, United Bankshares (NASDAQ:UBSI) is a bank holding company that provides commercial and retail banking services through its United Bank subsidiary across multiple states.

United Bank, the company's primary subsidiary, offers a comprehensive range of banking services including deposit accounts, commercial and real estate loans, and consumer lending products. The bank serves both individual and business customers, providing everything from basic checking accounts and personal loans to complex commercial financing and treasury management services.

For businesses, United Bank provides working capital loans, equipment financing, and commercial real estate lending. A business owner might use United's services to secure financing for expanding operations, purchasing inventory, or acquiring commercial property. For individual customers, the bank offers mortgage loans, home equity lines of credit, auto loans, and credit cards.

Beyond traditional banking, United operates several specialized subsidiaries. George Mason Mortgage and Crescent Mortgage focus on residential mortgage origination and sales to the secondary market. United Brokerage Services provides investment advisory services and securities brokerage, allowing customers to manage their investments alongside their banking relationships.

The company generates revenue primarily through interest income on loans and investments, as well as through fees for various banking services. United's digital banking platform enables customers to conduct transactions, pay bills, and manage accounts remotely, complementing its physical branch network. As a financial holding company, United operates under the regulatory oversight of the Federal Reserve, the FDIC, and various state banking authorities.

4. Regional Banks

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

United Bankshares competes with other regional banks such as WesBanco (NASDAQ:WSBC), F.N.B. Corporation (NYSE:FNB), and S&T Bancorp (NASDAQ:STBA), as well as larger national institutions like JPMorgan Chase (NYSE:JPM) and Bank of America (NYSE:BAC) in its operating markets.

5. Sales Growth

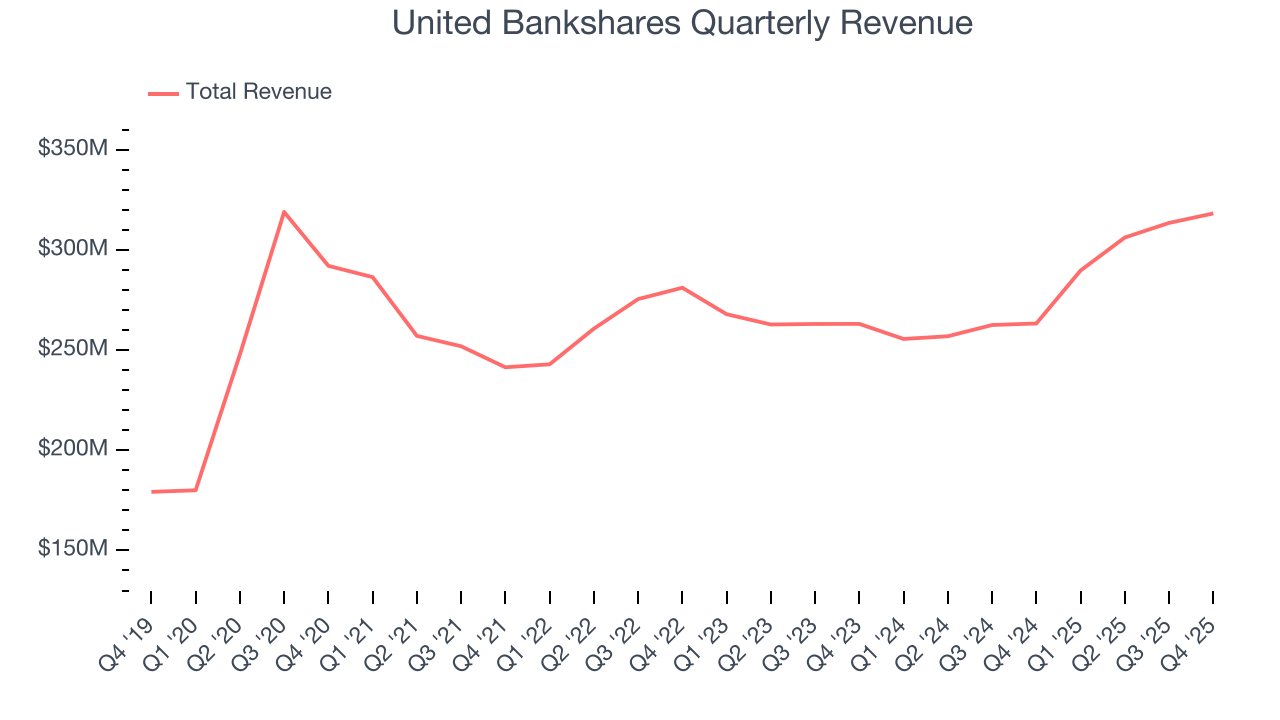

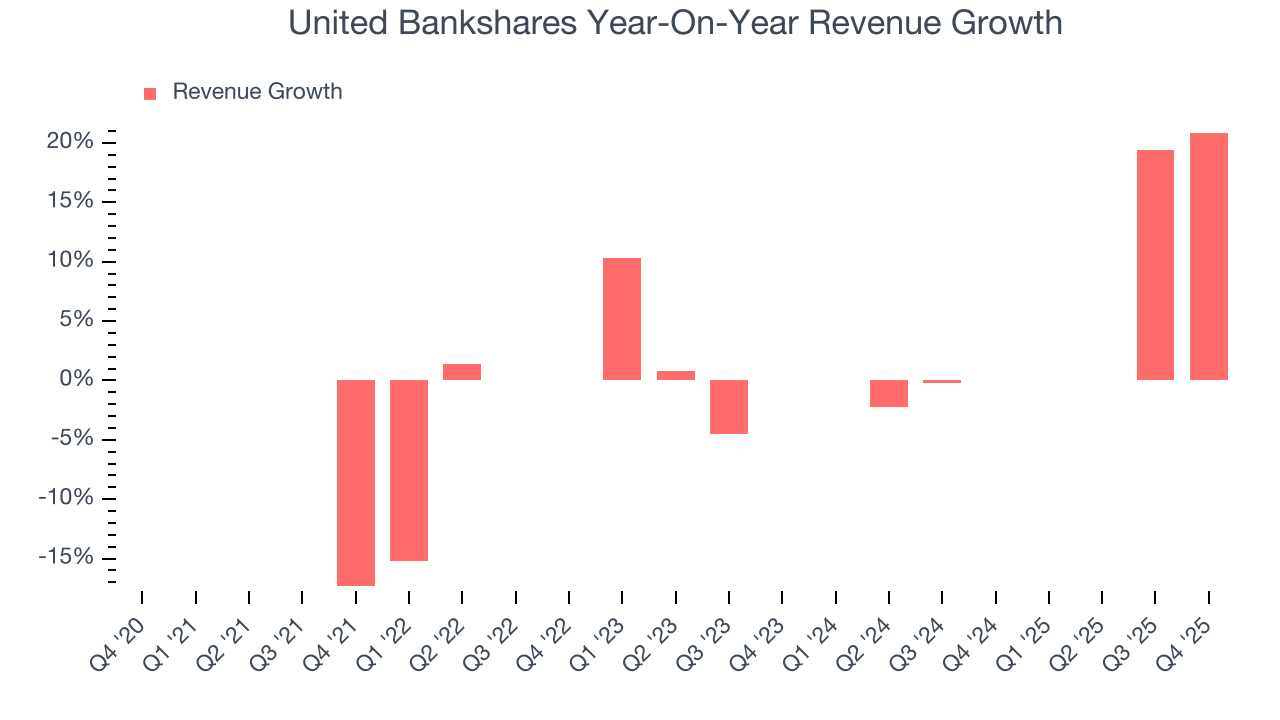

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Regrettably, United Bankshares’s revenue grew at a sluggish 3.4% compounded annual growth rate over the last five years. This fell short of our benchmark for the banking sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. United Bankshares’s annualized revenue growth of 7.8% over the last two years is above its five-year trend, but we were still disappointed by the results.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, United Bankshares reported robust year-on-year revenue growth of 20.9%, and its $318.4 million of revenue topped Wall Street estimates by 0.9%.

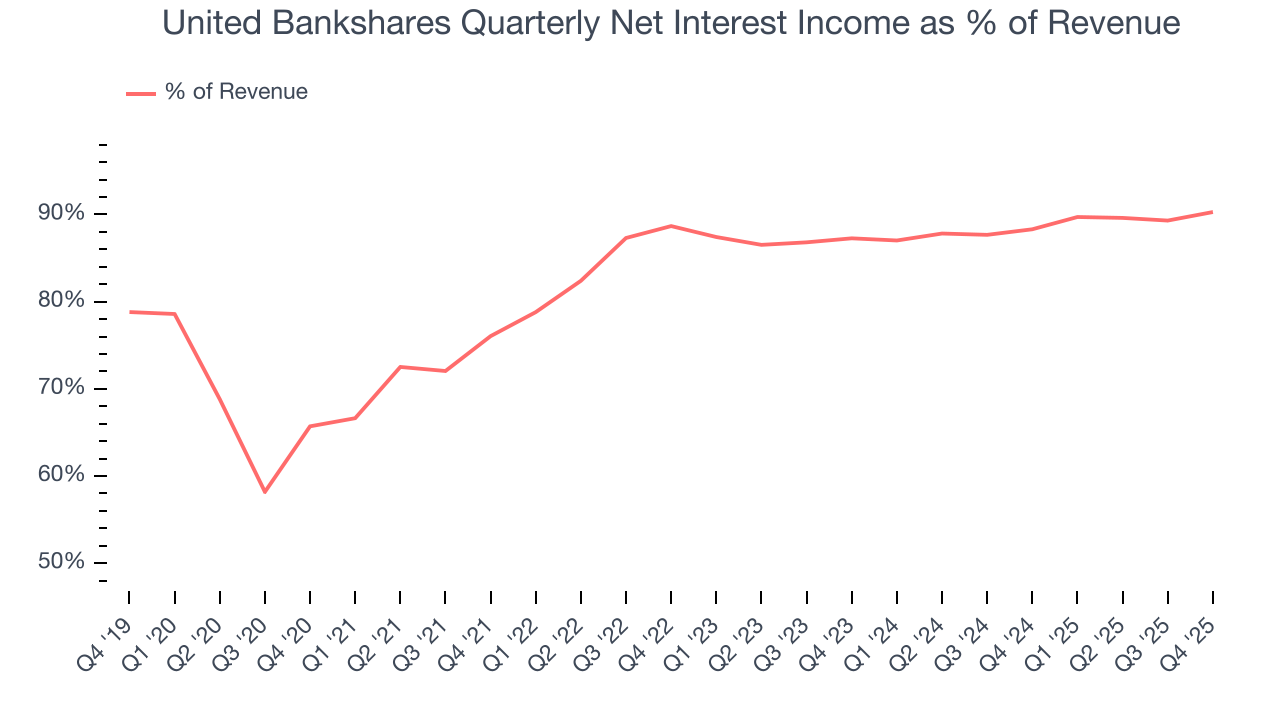

Net interest income made up 84.1% of the company’s total revenue during the last five years, meaning United Bankshares barely relies on non-interest income to drive its overall growth.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

6. Earnings Per Share

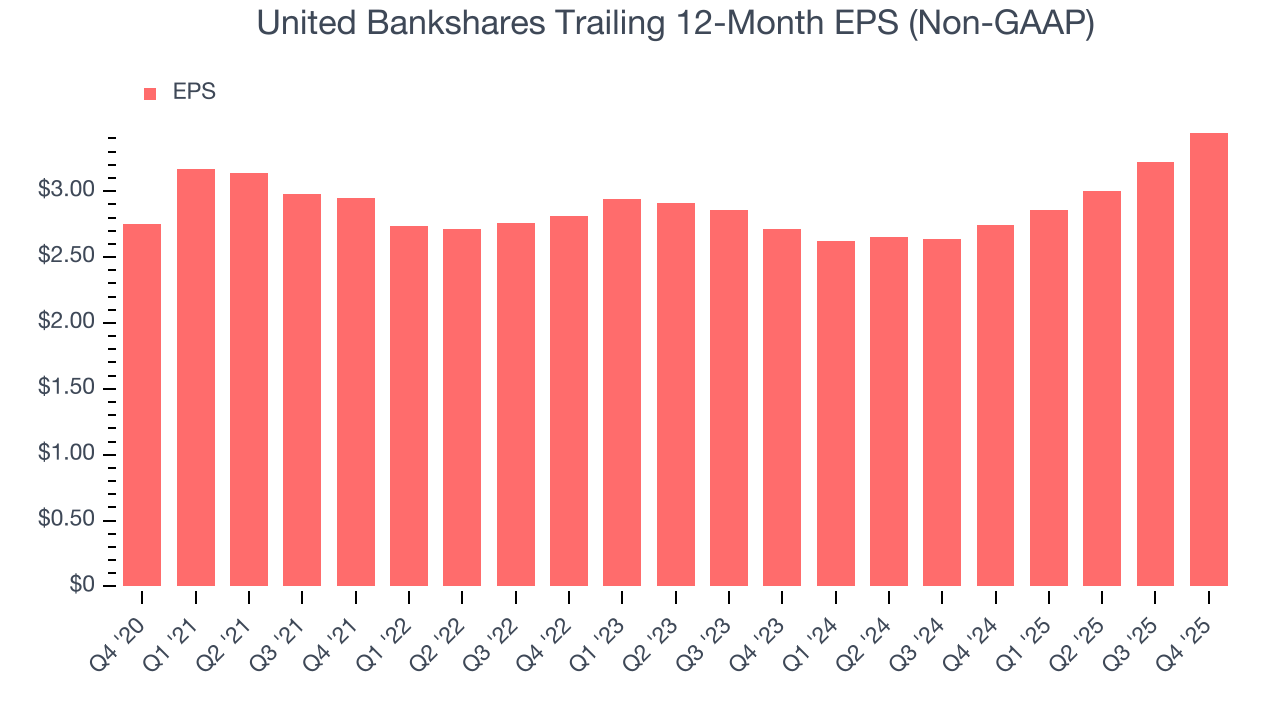

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

United Bankshares’s weak 4.6% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For United Bankshares, its two-year annual EPS growth of 12.7% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.

In Q4, United Bankshares reported adjusted EPS of $0.91, up from $0.69 in the same quarter last year. This print beat analysts’ estimates by 6.1%. Over the next 12 months, Wall Street expects United Bankshares’s full-year EPS of $3.44 to shrink by 1.2%.

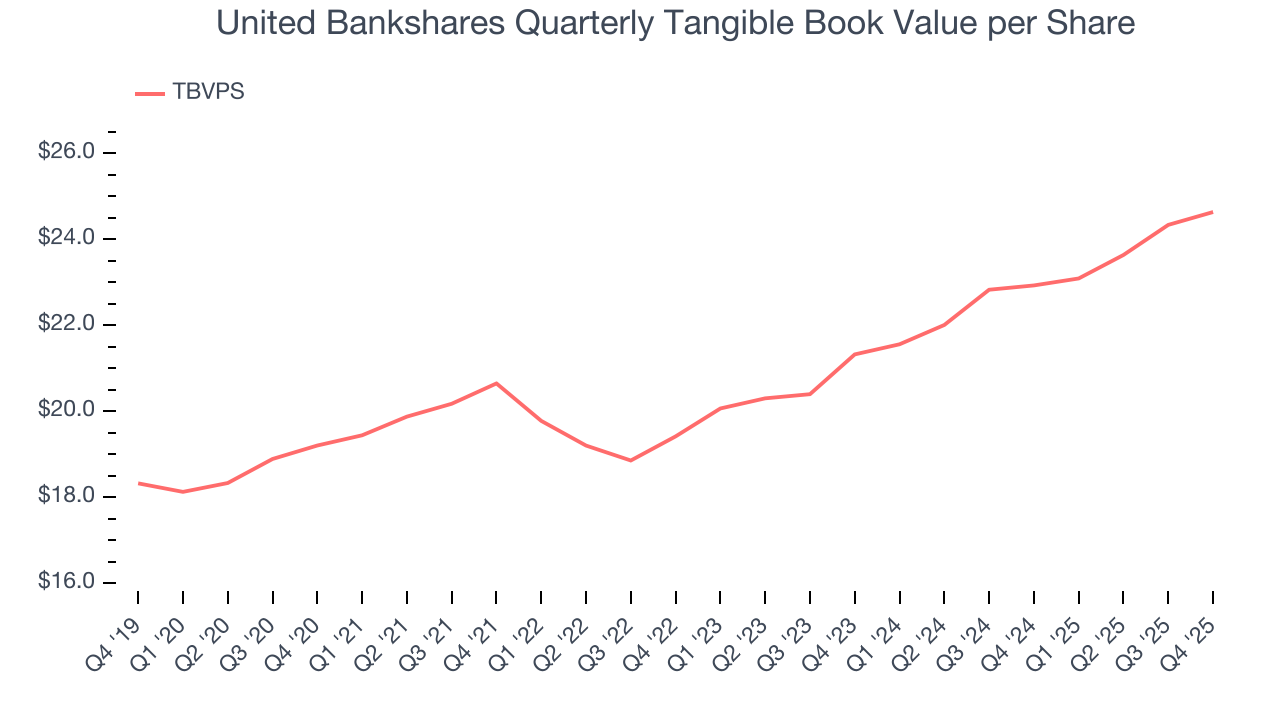

7. Tangible Book Value Per Share (TBVPS)

Banks profit by intermediating between depositors and borrowers, making them fundamentally balance sheet-driven enterprises. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these institutions.

This is why we consider tangible book value per share (TBVPS) the most important metric to track for banks. TBVPS represents the real, liquid net worth per share of a bank, excluding intangible assets that have debatable value upon liquidation. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

United Bankshares’s TBVPS grew at a decent 5.1% annual clip over the last five years. TBVPS growth has accelerated recently, growing by 7.5% annually over the last two years from $21.32 to $24.63 per share.

Over the next 12 months, Consensus estimates call for United Bankshares’s TBVPS to grow by 6.9% to $26.33, lousy growth rate.

8. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, United Bankshares has averaged a Tier 1 capital ratio of 13.5%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

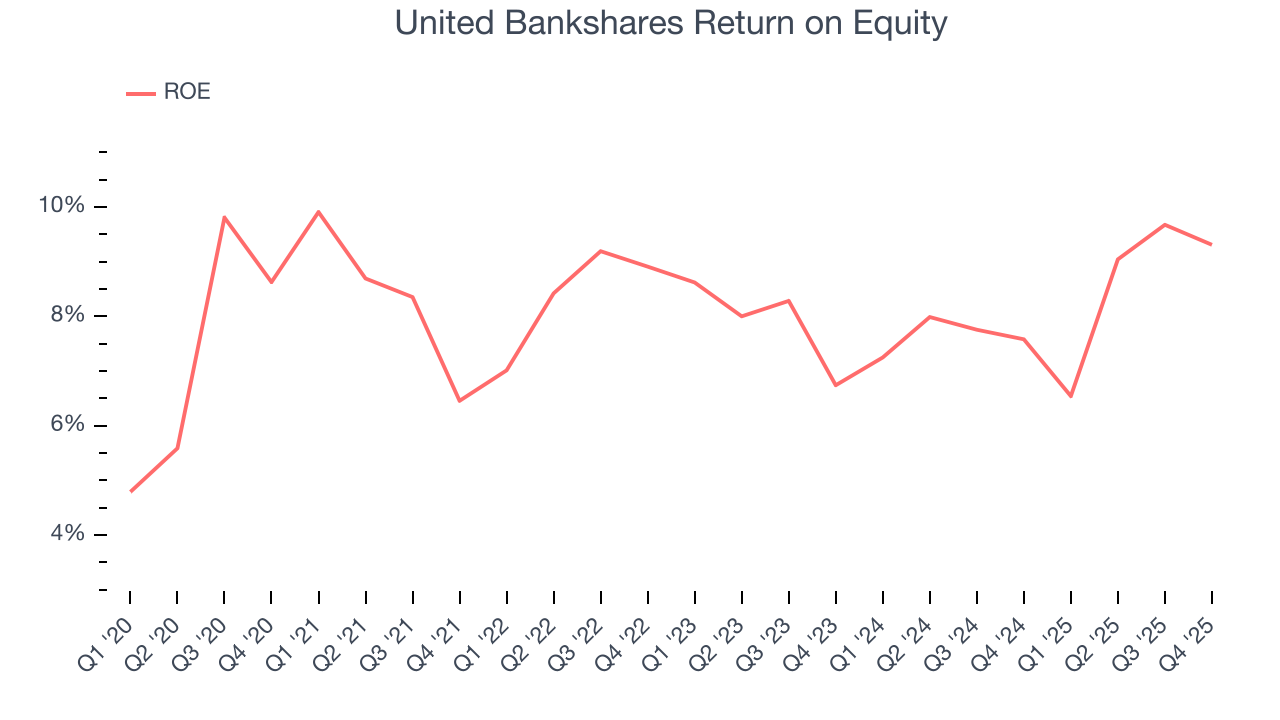

9. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, United Bankshares has averaged an ROE of 8.2%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

10. Key Takeaways from United Bankshares’s Q4 Results

It was good to see United Bankshares narrowly top analysts’ net interest income expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $43.07 immediately after reporting.

11. Is Now The Time To Buy United Bankshares?

Updated: March 10, 2026 at 12:56 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in United Bankshares.

We see the value of companies driving economic growth, but in the case of United Bankshares, we’re out. To begin with, its revenue growth was weak over the last five years. While its estimated net interest income growth for the next 12 months is great, the downside is its weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders. On top of that, its net interest income growth was weak over the last five years.

United Bankshares’s P/B ratio based on the next 12 months is 1x. This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $45.80 on the company (compared to the current share price of $39.93).