Vertex Pharmaceuticals (VRTX)

Vertex Pharmaceuticals is interesting. Its high free cash flow margin and returns on capital show it can produce cash and invest it wisely.― StockStory Analyst Team

1. News

2. Summary

Why Vertex Pharmaceuticals Is Interesting

Founded in 1989 with a mission to create medicines that treat the underlying causes of disease rather than just symptoms, Vertex Pharmaceuticals (NASDAQ:VRTX) develops and markets transformative medicines for serious diseases, with a focus on cystic fibrosis, sickle cell disease, and pain management.

- Healthy adjusted operating margin shows it’s a well-run company with efficient processes

- Market-beating returns on capital illustrate that management has a knack for investing in profitable ventures

- The stock is slightly expensive, and we suggest waiting until its quality rises or its valuation falls

Vertex Pharmaceuticals shows some signs of a high-quality business. This is a good company to add to your watchlist.

Why Should You Watch Vertex Pharmaceuticals

At $465.00 per share, Vertex Pharmaceuticals trades at 24.5x forward P/E. Vertex Pharmaceuticals’s valuation represents a premium to other names in the healthcare sector.

Vertex Pharmaceuticals can improve its fundamentals over time by putting up good numbers quarter after quarter, year after year. Once that happens, we’ll be happy to recommend the stock.

3. Vertex Pharmaceuticals (VRTX) Research Report: Q4 CY2025 Update

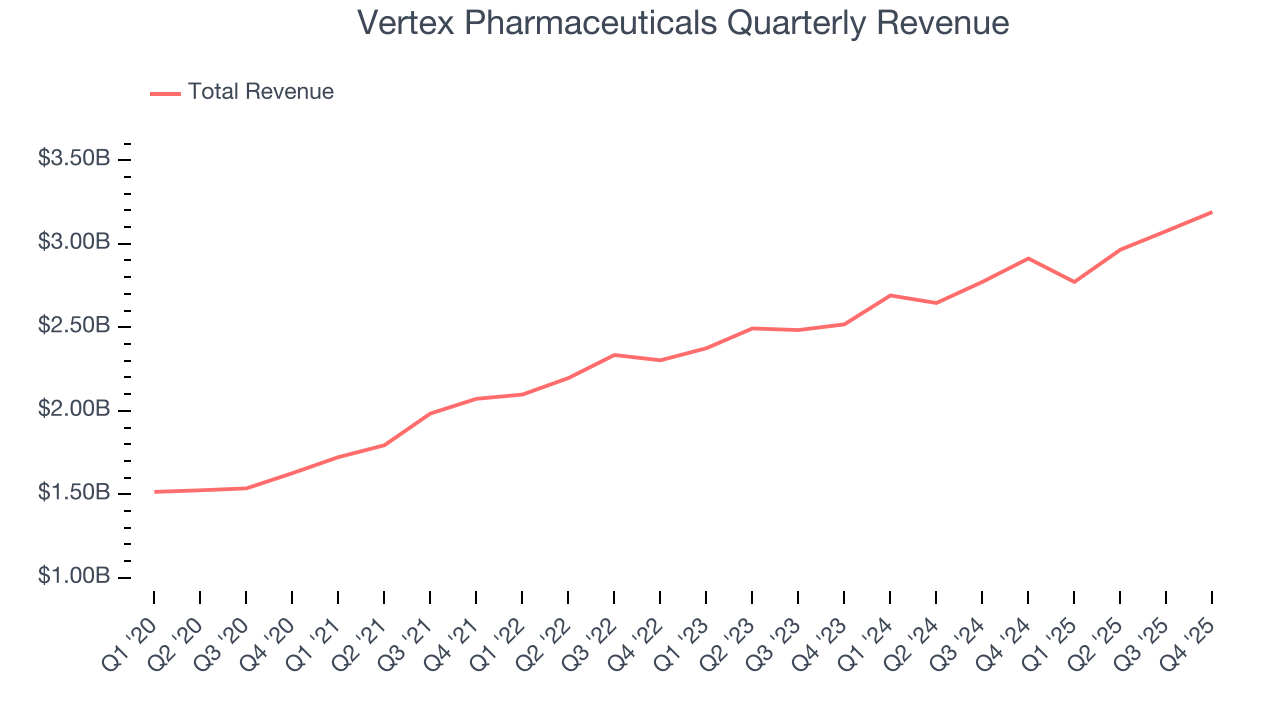

Biotech company Vertex Pharmaceuticals (NASDAQ:VRTX) announced better-than-expected revenue in Q4 CY2025, with sales up 9.5% year on year to $3.19 billion. The company expects the full year’s revenue to be around $13.03 billion, close to analysts’ estimates. Its non-GAAP profit of $5.03 per share was 2.3% below analysts’ consensus estimates.

Vertex Pharmaceuticals (VRTX) Q4 CY2025 Highlights:

- Revenue: $3.19 billion vs analyst estimates of $3.16 billion (9.5% year-on-year growth, 1.1% beat)

- Adjusted EPS: $5.03 vs analyst expectations of $5.15 (2.3% miss)

- Adjusted Operating Income: $1.37 billion vs analyst estimates of $1.47 billion (43% margin, 6.8% miss)

- Operating Margin: 37.8%, up from 35.2% in the same quarter last year

- Market Capitalization: $117 billion

Company Overview

Founded in 1989 with a mission to create medicines that treat the underlying causes of disease rather than just symptoms, Vertex Pharmaceuticals (NASDAQ:VRTX) develops and markets transformative medicines for serious diseases, with a focus on cystic fibrosis, sickle cell disease, and pain management.

Vertex has built its reputation on developing precision medicines that address the root causes of diseases rather than just managing symptoms. The company's most established franchise is in cystic fibrosis (CF), where it has five approved medicines that treat the underlying genetic defect in approximately three-quarters of the 94,000 CF patients in the U.S., Europe, Australia, and Canada.

The company's CF treatments work by modulating the defective CFTR protein that causes the disease. Its flagship product, TRIKAFTA/KAFTRIO, has transformed CF care by dramatically improving lung function and quality of life for patients. In late 2024, Vertex expanded its CF portfolio with ALYFTREK, its newest triple combination therapy.

Beyond CF, Vertex has successfully diversified into other serious genetic diseases. In 2023, the company received approval for CASGEVY, a groundbreaking CRISPR/Cas9 gene-editing therapy developed with CRISPR Therapeutics for sickle cell disease and transfusion-dependent beta thalassemia. This therapy represents the first approved CRISPR-based treatment and works by editing a patient's own stem cells to produce functional hemoglobin.

In early 2025, Vertex entered the pain management market with JOURNAVX, a non-opioid treatment for moderate-to-severe acute pain that works by inhibiting specific pain signals. The company is also advancing this compound for chronic neuropathic pain conditions.

Vertex's pipeline includes promising candidates for several other serious diseases. The company is developing treatments for APOL1-mediated kidney disease, IgA nephropathy, type 1 diabetes, myotonic dystrophy type 1, and autosomal dominant polycystic kidney disease. Its type 1 diabetes program, which uses stem cell-derived insulin-producing islet cells, aims to potentially cure the disease rather than just manage it.

The company employs a "serial innovation" strategy, advancing multiple compounds for each disease area and using various therapeutic modalities including small molecules, cell therapies, and genetic approaches. This approach has allowed Vertex to build a diverse pipeline while maintaining focus on diseases with clear biological targets and significant unmet needs.

Vertex generates revenue primarily through sales of its medicines to specialty pharmacies and distributors. The company invests heavily in research and development, typically reinvesting a substantial portion of its revenue into discovering and developing new treatments.

4. Therapeutics

Over the next few years, therapeutic companies, which develop a wide variety of treatments for diseases and disorders, face strong tailwinds from advancements in precision medicine (including the use of AI to improve hit rates) and growing demand for treatments targeting rare diseases. However, headwinds such as rising scrutiny over drug pricing, regulatory unknowns, and competition from larger, more resourced pharmaceutical companies could weigh on growth.

Vertex's competitors vary by therapeutic area. In cystic fibrosis, it faces limited competition due to its dominant position, though companies like AbbVie (NYSE:ABBV) and Pfizer (NYSE:PFE) have programs in development. For gene therapies like CASGEVY, competitors include bluebird bio (NASDAQ:BLUE) and CRISPR Therapeutics (NASDAQ:CRSP). In pain management, Vertex competes with traditional pharmaceutical companies like Pfizer, Eli Lilly (NYSE:LLY), and various makers of opioid and non-opioid pain medications.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $12 billion in revenue over the past 12 months, Vertex Pharmaceuticals has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

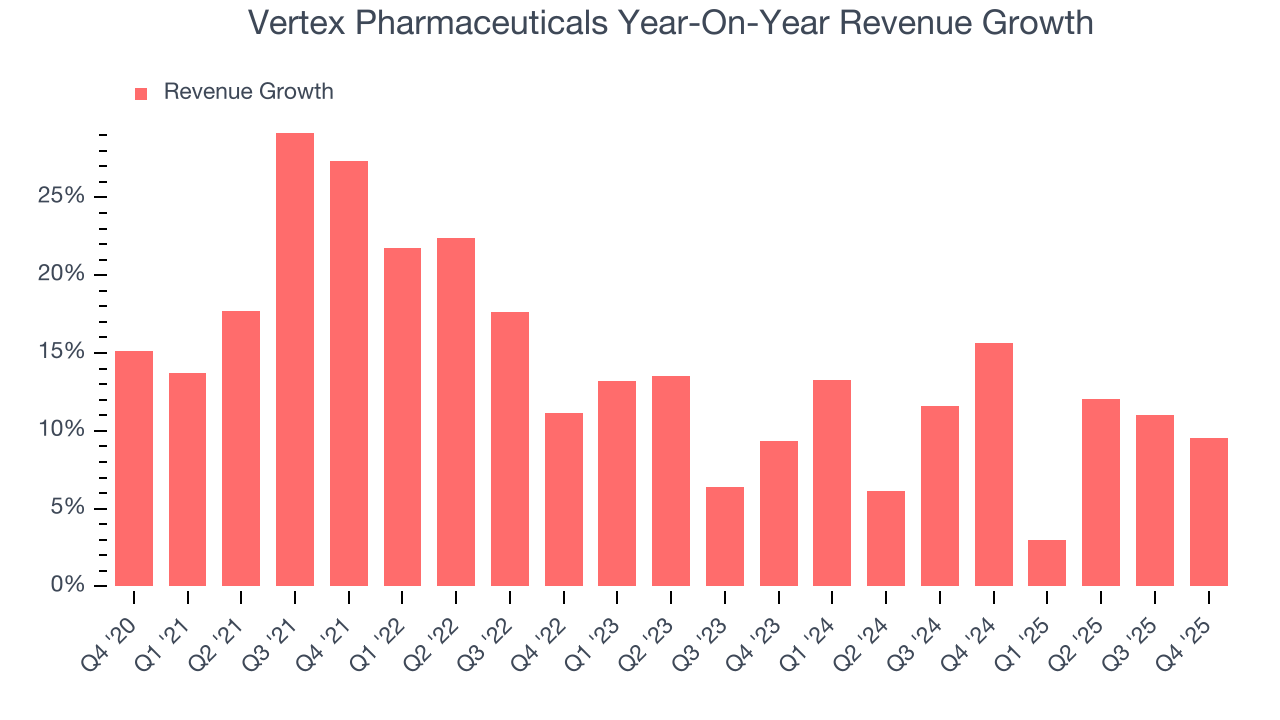

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Vertex Pharmaceuticals’s 14.1% annualized revenue growth over the last five years was solid. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Vertex Pharmaceuticals’s annualized revenue growth of 10.3% over the last two years is below its five-year trend, but we still think the results were respectable.

This quarter, Vertex Pharmaceuticals reported year-on-year revenue growth of 9.5%, and its $3.19 billion of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is satisfactory given its scale and implies the market is baking in success for its products and services.

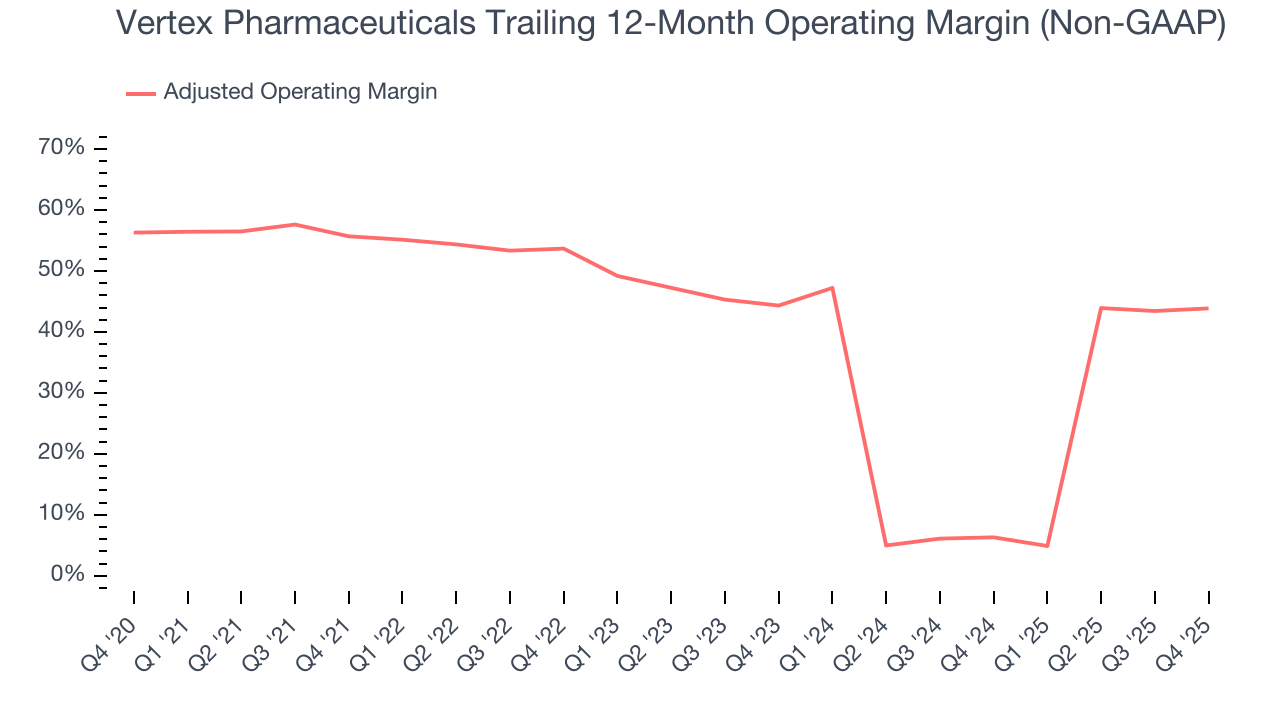

7. Adjusted Operating Margin

Vertex Pharmaceuticals has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average adjusted operating margin of 39.2%.

Analyzing the trend in its profitability, Vertex Pharmaceuticals’s adjusted operating margin decreased by 11.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, Vertex Pharmaceuticals generated an adjusted operating margin profit margin of 43%, up 1.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

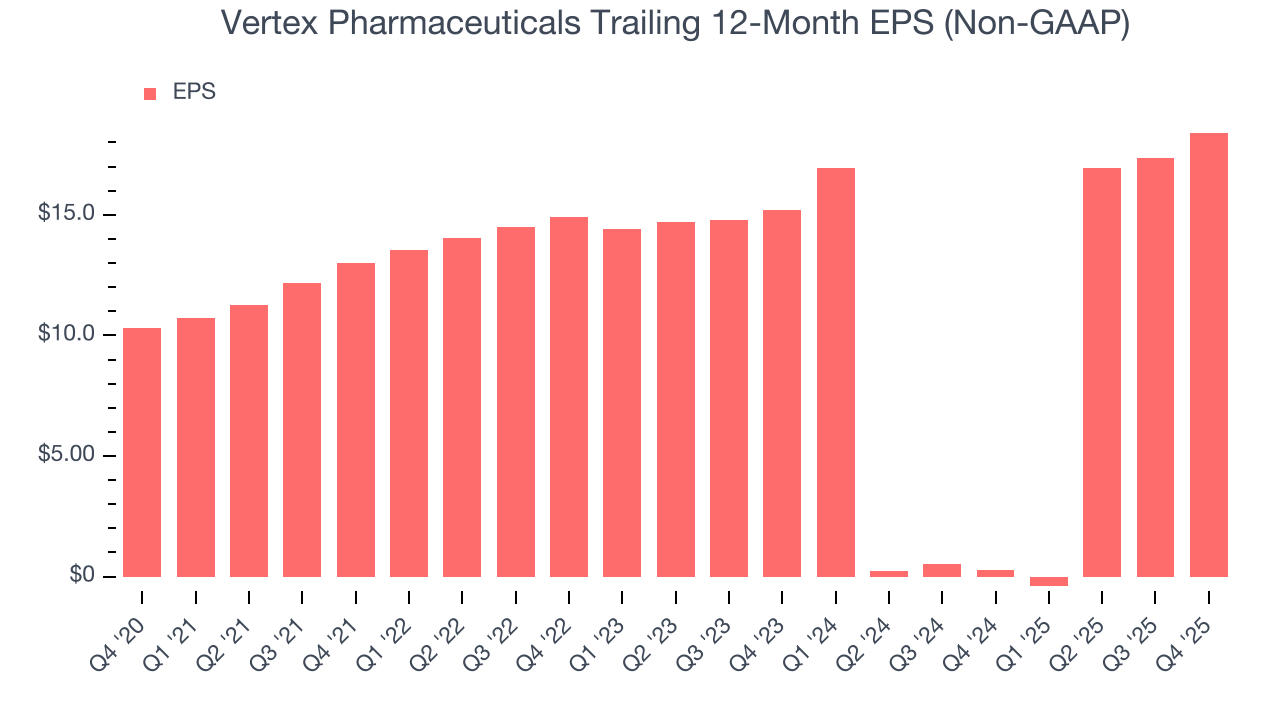

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Vertex Pharmaceuticals’s spectacular 12.3% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q4, Vertex Pharmaceuticals reported adjusted EPS of $5.03, up from $3.98 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Vertex Pharmaceuticals’s full-year EPS of $18.41 to grow 8.2%.

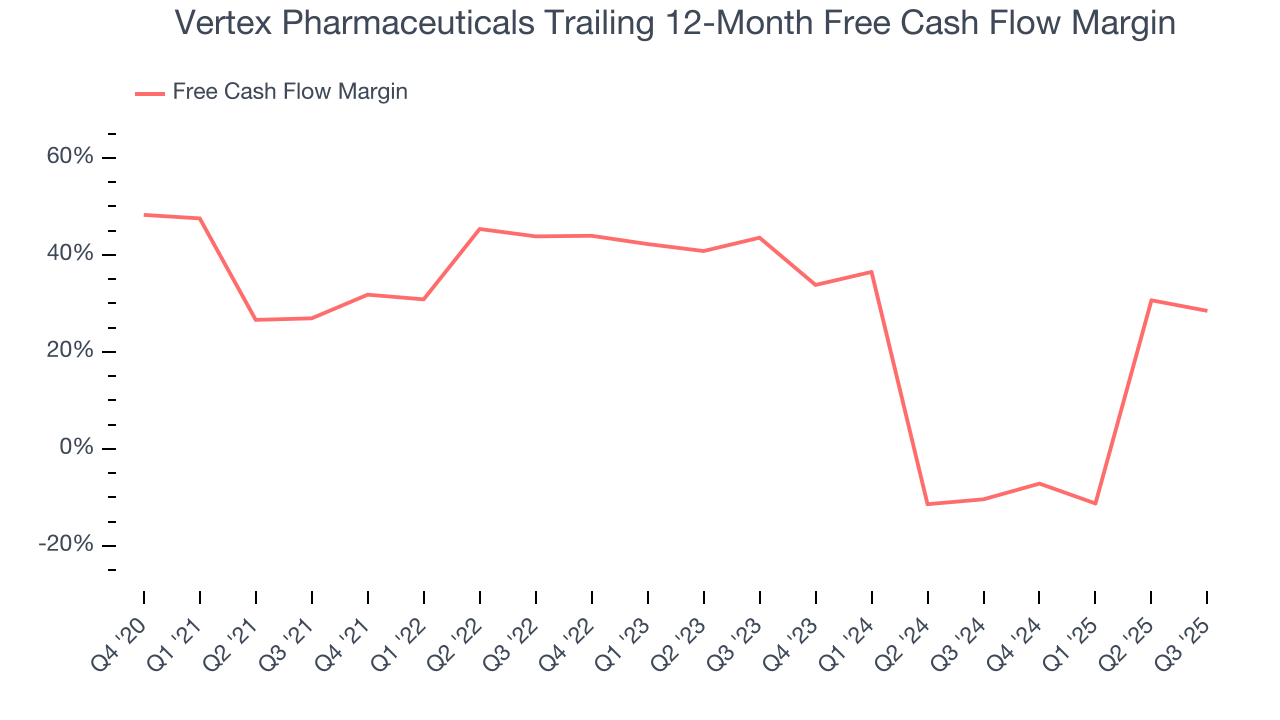

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Vertex Pharmaceuticals has shown terrific cash profitability, enabling it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the healthcare sector, averaging 25.4% over the last five years.

Taking a step back, we can see that Vertex Pharmaceuticals’s margin expanded by 5.5 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

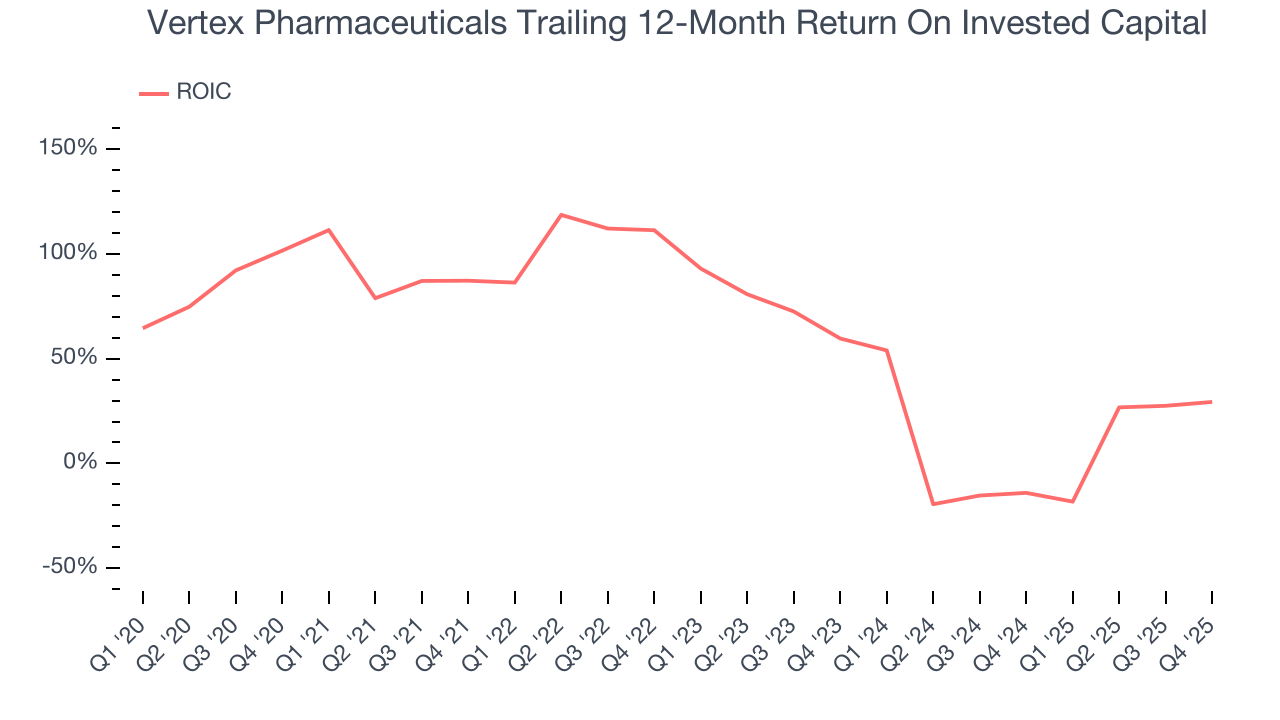

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Vertex Pharmaceuticals’s five-year average ROIC was 40.6%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Vertex Pharmaceuticals’s ROIC has unfortunately decreased significantly. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

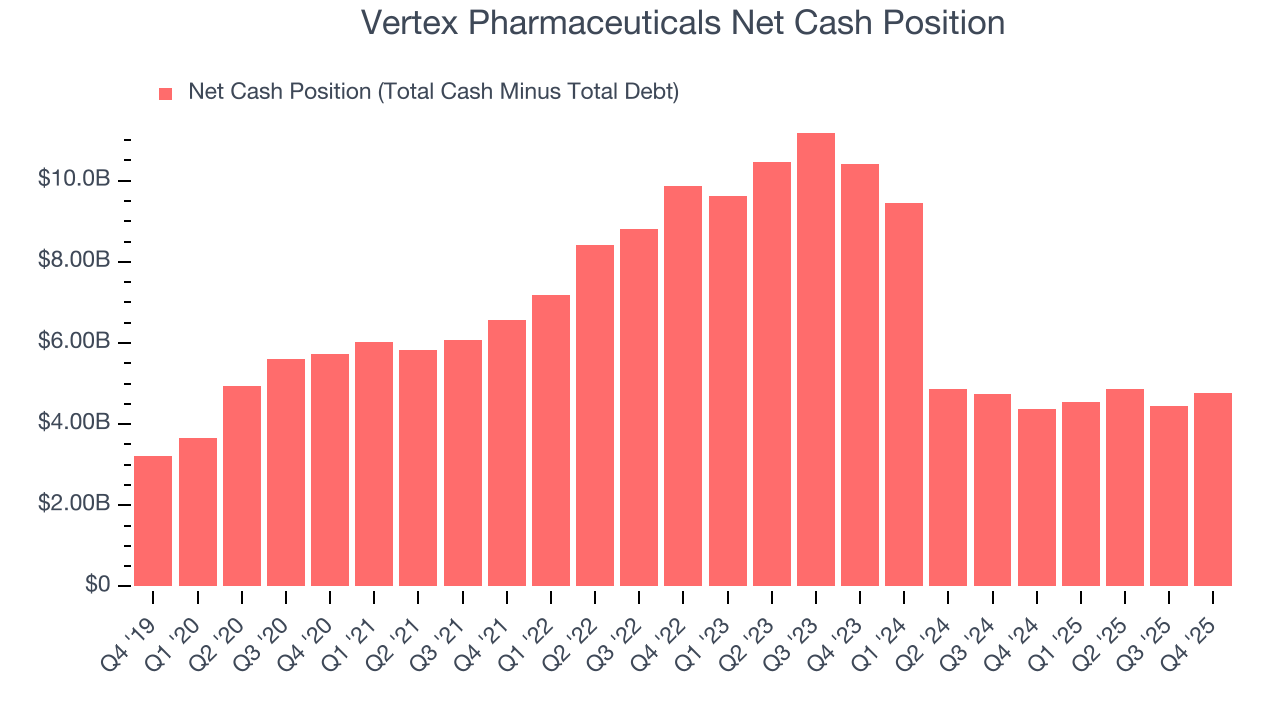

11. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Vertex Pharmaceuticals is a profitable, well-capitalized company with $6.61 billion of cash and $1.85 billion of debt on its balance sheet. This $4.76 billion net cash position is 3.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Vertex Pharmaceuticals’s Q4 Results

It was good to see Vertex Pharmaceuticals narrowly top analysts’ revenue expectations this quarter. On the other hand, its EPS missed. Overall, this was a softer quarter. The stock remained flat at $463.49 immediately after reporting.

13. Is Now The Time To Buy Vertex Pharmaceuticals?

Updated: March 16, 2026 at 11:58 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Vertex Pharmaceuticals.

In our opinion, Vertex Pharmaceuticals is a good company. First off, its revenue growth was solid over the last five years. And while its diminishing returns show management's recent bets still have yet to bear fruit, its impressive operating margins show it has a highly efficient business model. On top of that, its stellar ROIC suggests it has been a well-run company historically.

Vertex Pharmaceuticals’s P/E ratio based on the next 12 months is 24.5x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in. This is a good one to add to your watchlist - there are better opportunities elsewhere at the moment.

Wall Street analysts have a consensus one-year price target of $545.50 on the company (compared to the current share price of $465.00).