Western Digital (WDC)

Western Digital is interesting. Although its sales growth has been weak, its profitability gives it the flexibility to ride out cycles.― StockStory Analyst Team

1. News

2. Summary

Why Western Digital Is Interesting

Founded in 1970 by a Motorola employee, Western Digital (NASDAQ: WDC) is a leading producer of hard disk drives, SSDs and flash memory.

- Demand for the next 12 months is expected to accelerate above its two-year trend as Wall Street forecasts robust revenue growth of 31.9%

- Healthy operating margin shows it’s a well-run company with efficient processes, and its rise over the last five years shows it refined its expense structure

- One risk is its annual sales declines of 8% for the past five years show its products and services struggled to connect with the market during this cycle

Western Digital is close to becoming a high-quality business. If you’ve been itching to buy the stock, the valuation looks fair.

Why Is Now The Time To Buy Western Digital?

Western Digital’s stock price of $271.91 implies a valuation ratio of 23.1x forward P/E. The current valuation is below that of most semiconductor companies, but this isn’t a bargain. Instead, the price is appropriate for the quality you get.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Western Digital (WDC) Research Report: Q4 CY2025 Update

Leading data storage manufacturer Western Digital (NASDAQ: WDC) reported revenue ahead of Wall Streets expectations in Q4 CY2025, with sales up 25.2% year on year to $3.02 billion. On top of that, next quarter’s revenue guidance ($3.2 billion at the midpoint) was surprisingly good and 6.8% above what analysts were expecting. Its non-GAAP profit of $2.13 per share was 10.5% above analysts’ consensus estimates.

Western Digital (WDC) Q4 CY2025 Highlights:

- Revenue: $3.02 billion vs analyst estimates of $2.95 billion (25.2% year-on-year growth, 2.2% beat)

- Adjusted EPS: $2.13 vs analyst estimates of $1.93 (10.5% beat)

- Adjusted Operating Income: $1.02 billion vs analyst estimates of $931.9 million (33.8% margin, 9.4% beat)

- Revenue Guidance for Q1 CY2026 is $3.2 billion at the midpoint, above analyst estimates of $3.00 billion

- Adjusted EPS guidance for Q1 CY2026 is $2.30 at the midpoint, above analyst estimates of $1.99

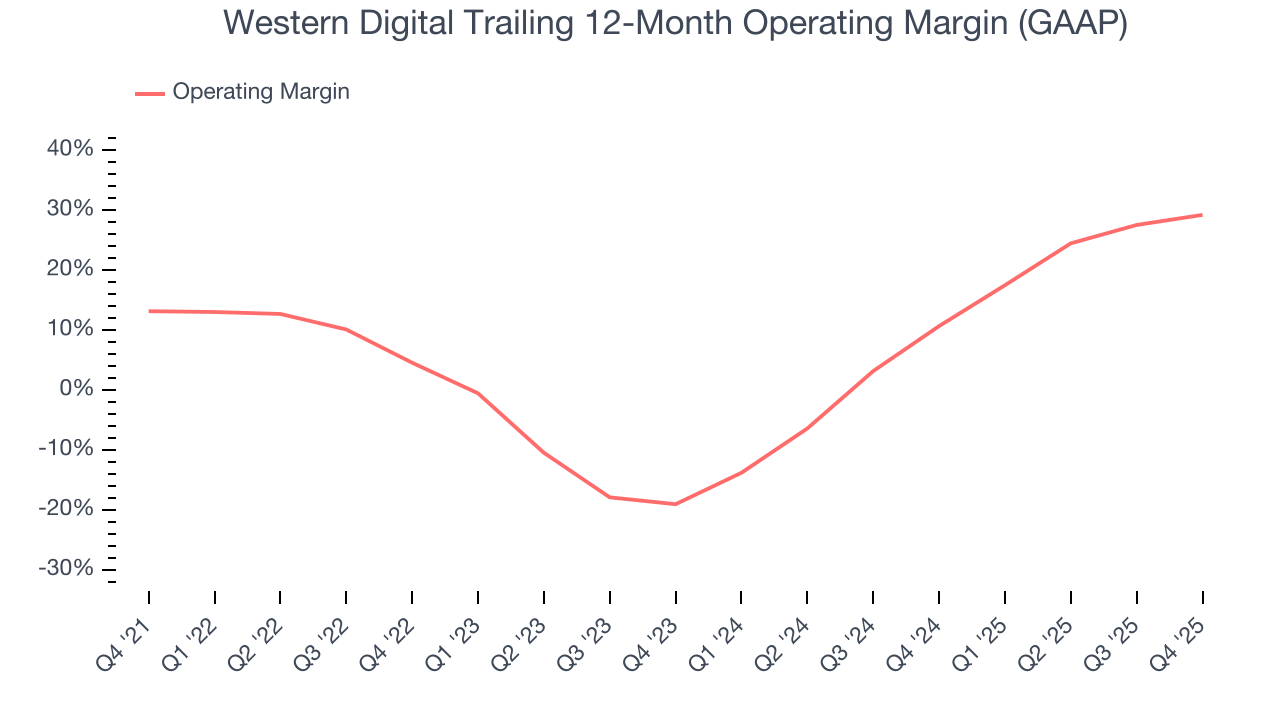

- Operating Margin: 30.1%, up from 23.2% in the same quarter last year

- Free Cash Flow Margin: 21.6%, up from 12% in the same quarter last year

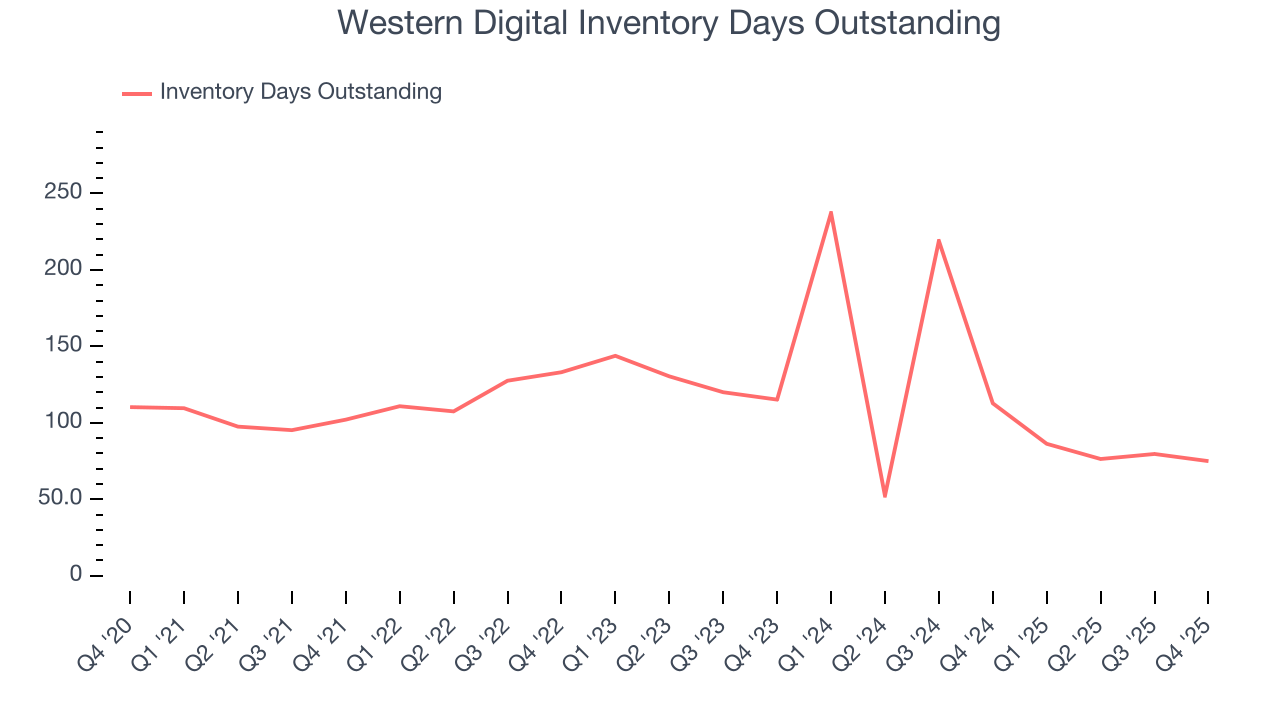

- Inventory Days Outstanding: 75, down from 80 in the previous quarter

- Market Capitalization: $95.63 billion

Company Overview

Founded in 1970 by a Motorola employee, Western Digital (NASDAQ: WDC) is a leading producer of hard disk drives, SSDs and flash memory.

Originally a producer of calculator chips, Western Digital refocused on hard disk drives in 1978, and created the original ATA hard disk drive standard used in PCs. HDDs were one of the most competitive, low margin, tech markets for decades until a wave of consolidation shrank the market to two main players; Western Digital and Seagate, following Western Digital’s acquisition of Hitachi Global Storage in 2015. That same year the company acquired SanDisk, one of the largest producers of flash memory.

The SanDisk acquisition brought Western Digital into a partnership with Toshiba (now named Kioxia) in Flash Ventures, the largest producer of flash memory semiconductors in the world, and diversified Western Digital’s revenues equally across HDD and flash memory, each of which today account for roughly half of its revenues.

Western Digital’s peers and competitors include Seagate (NASDAQ:STX), SK Hynix (KOSI:000660), and Samsung (KOSI:005930).

4. Memory Semiconductors

The global memory chip market has become concentrated due to the highly commoditized nature of these semiconductors. Despite the market consolidation, DRAM and NAND are subject to wide pricing swings as supply and demand ebbs and flows. This plays itself out in the business models of memory producers, where the large, fixed cost bases required to produce memory chips in volume can become very profitable during times of rising prices due to high demand and tight supply but also can result in periods of low profitability when more supply is brought online or demand drops.

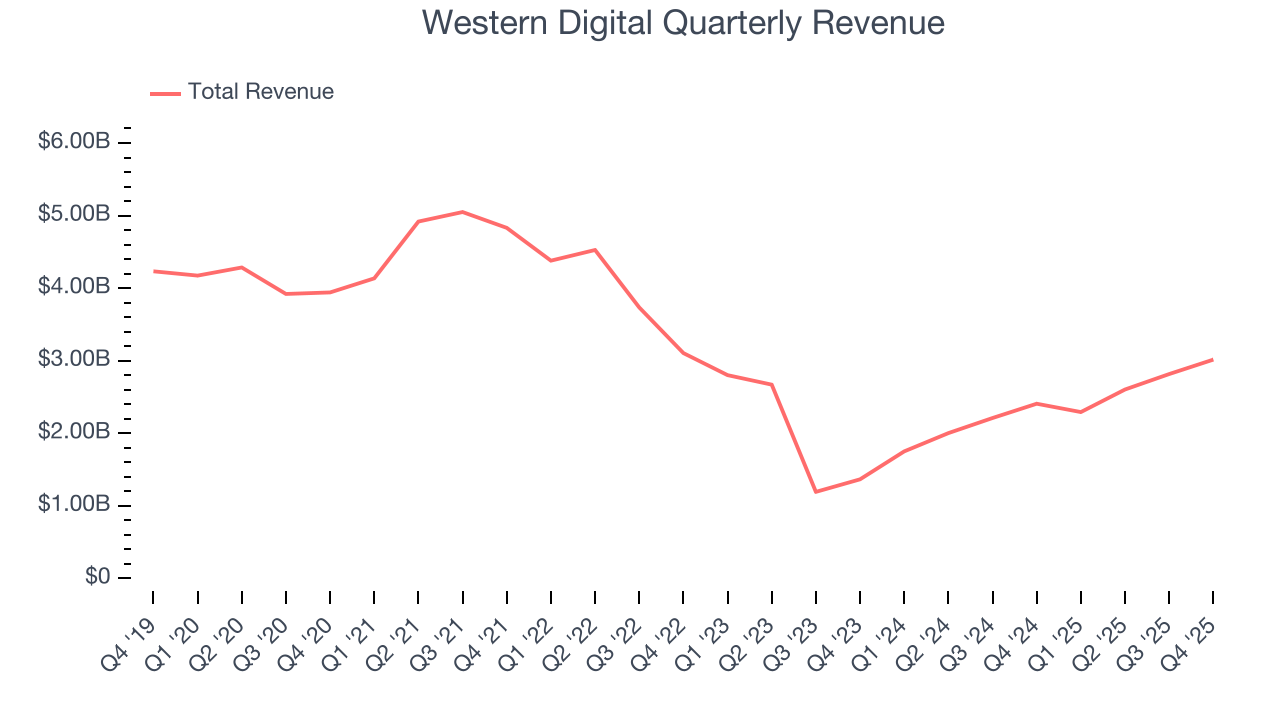

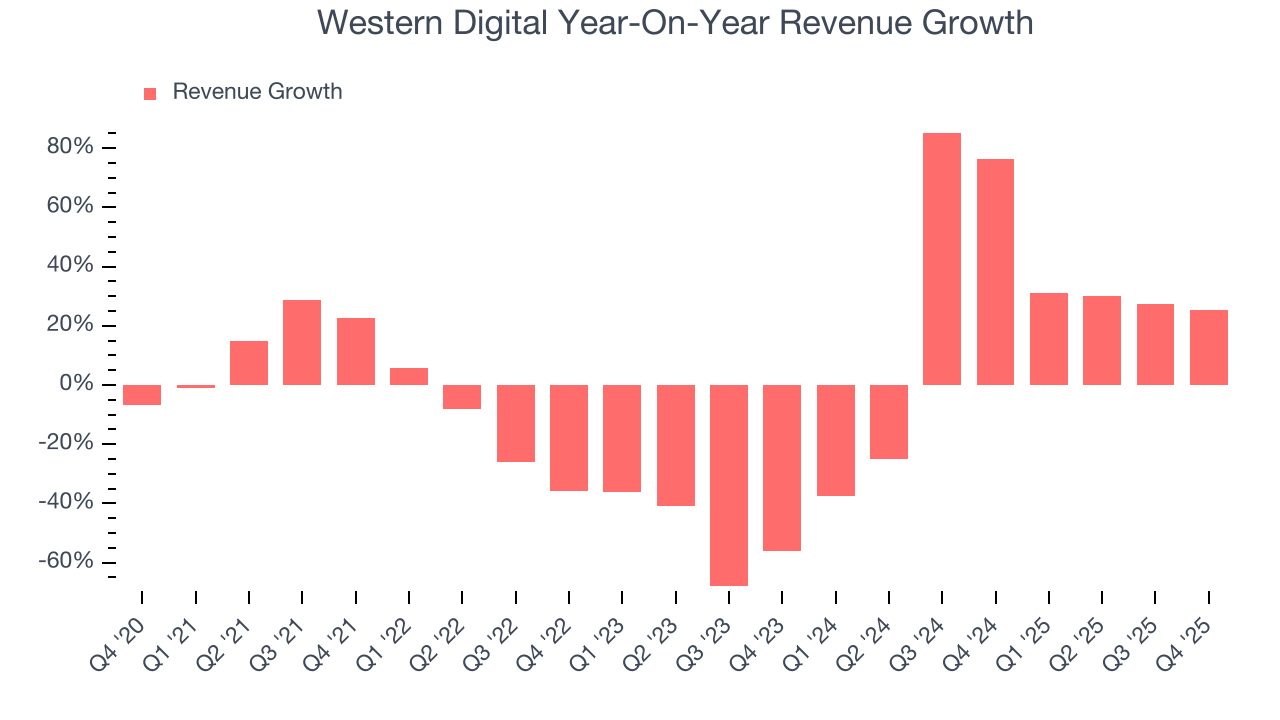

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Western Digital struggled to consistently generate demand over the last five years as its sales dropped at a 8% annual rate. This was below our standards and is a poor baseline for our analysis. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

Long-term growth is the most important, but short-term results matter for semiconductors because the rapid pace of technological innovation (Moore's Law) could make yesterday's hit product obsolete today. Western Digital’s annualized revenue growth of 15.6% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

This quarter, Western Digital reported robust year-on-year revenue growth of 25.2%, and its $3.02 billion of revenue topped Wall Street estimates by 2.2%. Beyond the beat, this marks 6 straight quarters of growth, showing that the current upcycle has had a good run - a typical upcycle usually lasts 8-10 quarters. Company management is currently guiding for a 39.5% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 20.6% over the next 12 months, an improvement versus the last two years. This projection is particularly healthy for a company of its scale and suggests its newer products and services will catalyze better top-line performance.

6. Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business’ capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Western Digital’s DIO came in at 75, which is 42 days below its five-year average. At the moment, these numbers show no indication of an excessive inventory buildup.

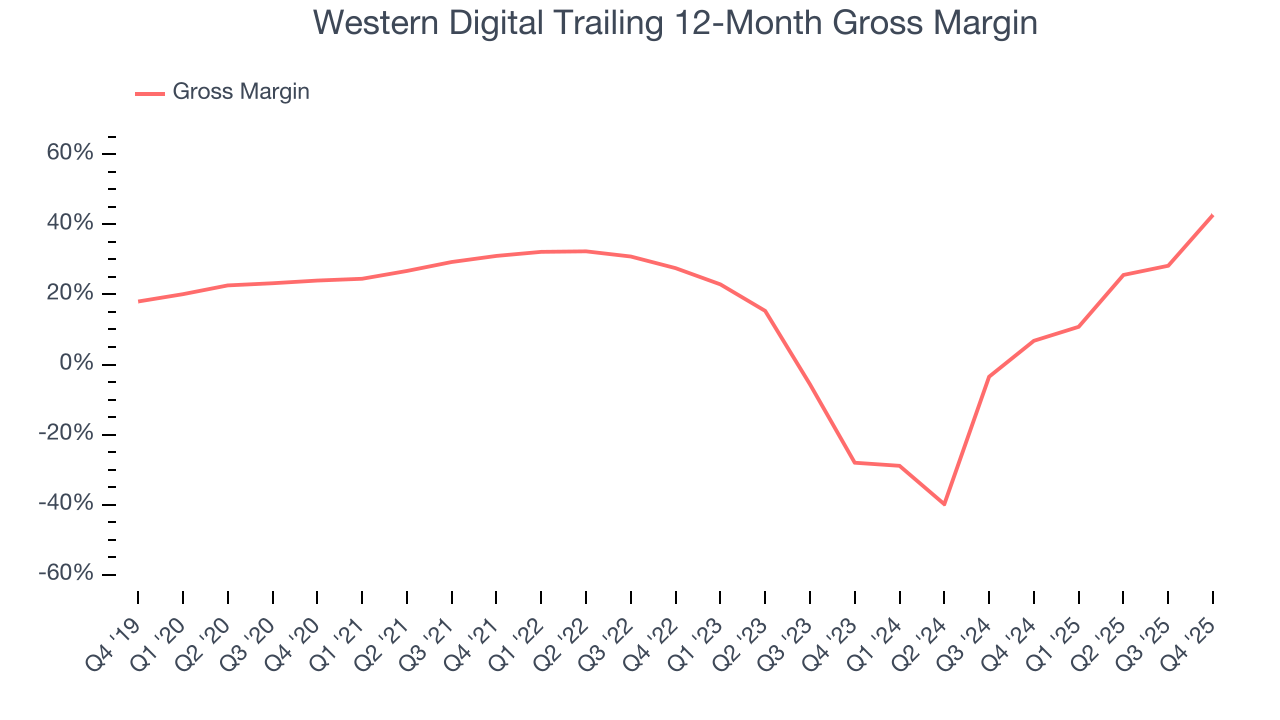

7. Gross Margin & Pricing Power

Gross profit margin is a key metric to track because it shows how much money a semiconductor company gets to keep after paying for its raw materials, manufacturing, and other input costs.

Western Digital’s gross margin is one of the worst in the semiconductor industry, signaling it operates in a competitive market and lacks pricing power. As you can see below, it averaged a 27% gross margin over the last two years. Said differently, Western Digital had to pay a chunky $73.03 to its suppliers for every $100 in revenue.

In Q4, Western Digital produced a 45.7% gross profit margin, up 60.3 percentage points year on year. Western Digital’s full-year margin has also been trending up over the past 12 months, increasing by 35.9 percentage points. If this move continues, it could suggest a less competitive environment where the company has better pricing power and leverage from its growing sales on the fixed portion of its cost of goods sold (such as manufacturing expenses).

8. Operating Margin

Western Digital has managed its cost base well over the last two years. It demonstrated solid profitability for a semiconductor business, producing an average operating margin of 21.1%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, Western Digital’s operating margin rose by 16.1 percentage points over the last five years, showing its efficiency has meaningfully improved.

This quarter, Western Digital generated an operating margin profit margin of 30.1%, up 6.8 percentage points year on year. The increase was driven by stronger leverage on its cost of sales (not higher efficiency with its operating expenses), as indicated by its larger rise in gross margin.

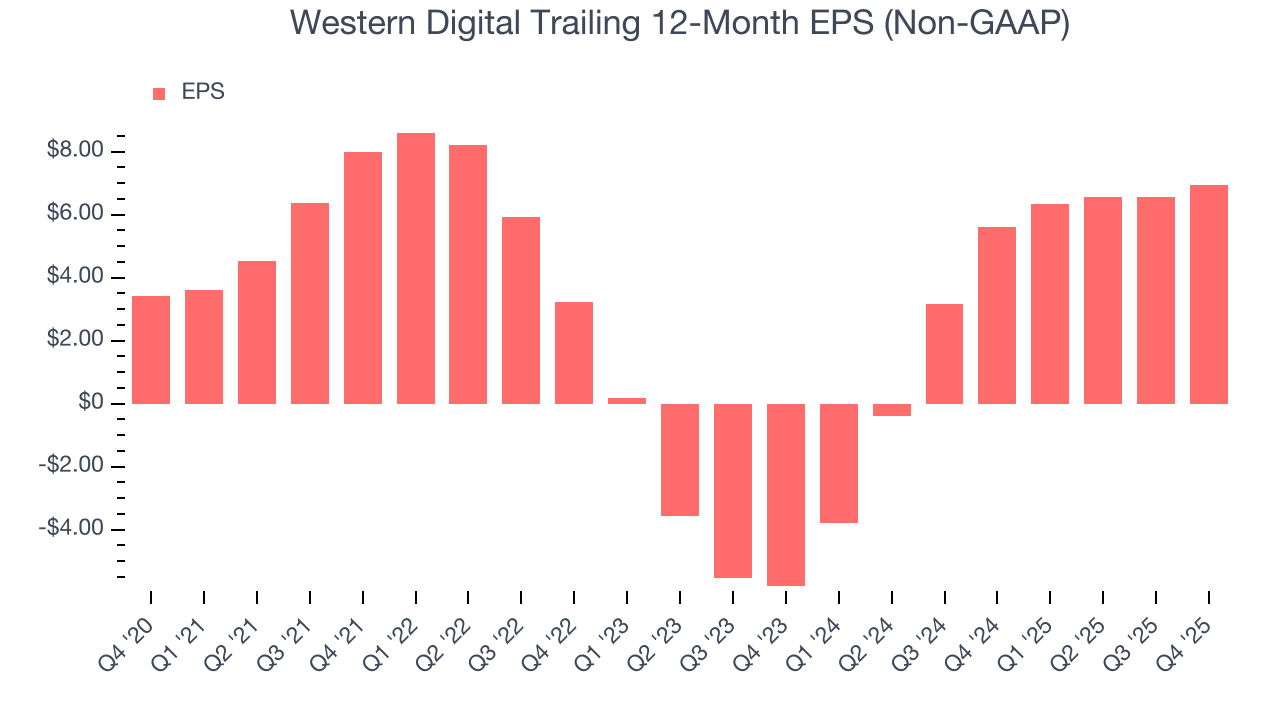

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Western Digital’s EPS grew at an unimpressive 15.2% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 8% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

Diving into the nuances of Western Digital’s earnings can give us a better understanding of its performance. As we mentioned earlier, Western Digital’s operating margin expanded by 16.1 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Western Digital reported adjusted EPS of $2.13, up from $1.77 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Western Digital’s full-year EPS of $6.93 to grow 34.9%.

10. Cash Is King

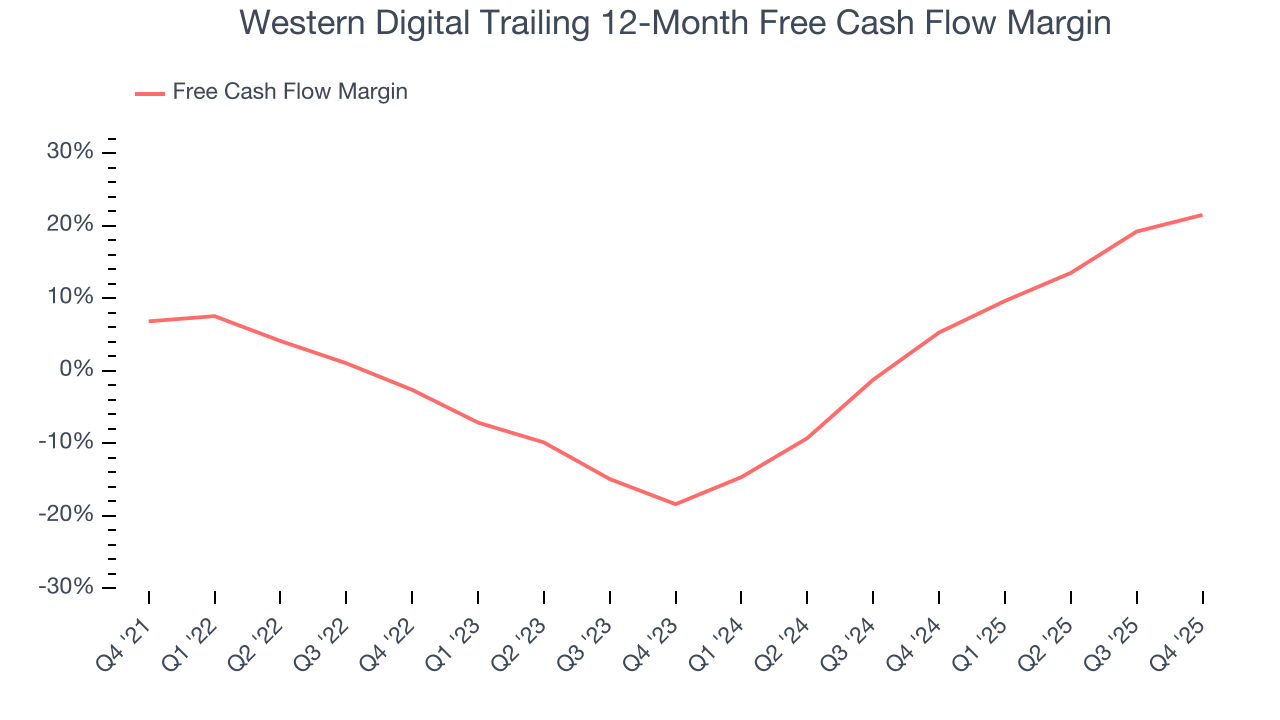

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Western Digital has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 14.4%, subpar for a semiconductor business.

Taking a step back, an encouraging sign is that Western Digital’s margin expanded by 14.7 percentage points over the last five years. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Western Digital’s free cash flow clocked in at $653 million in Q4, equivalent to a 21.6% margin. This result was good as its margin was 9.6 percentage points higher than in the same quarter last year, building on its favorable historical trend.

11. Return on Invested Capital (ROIC)

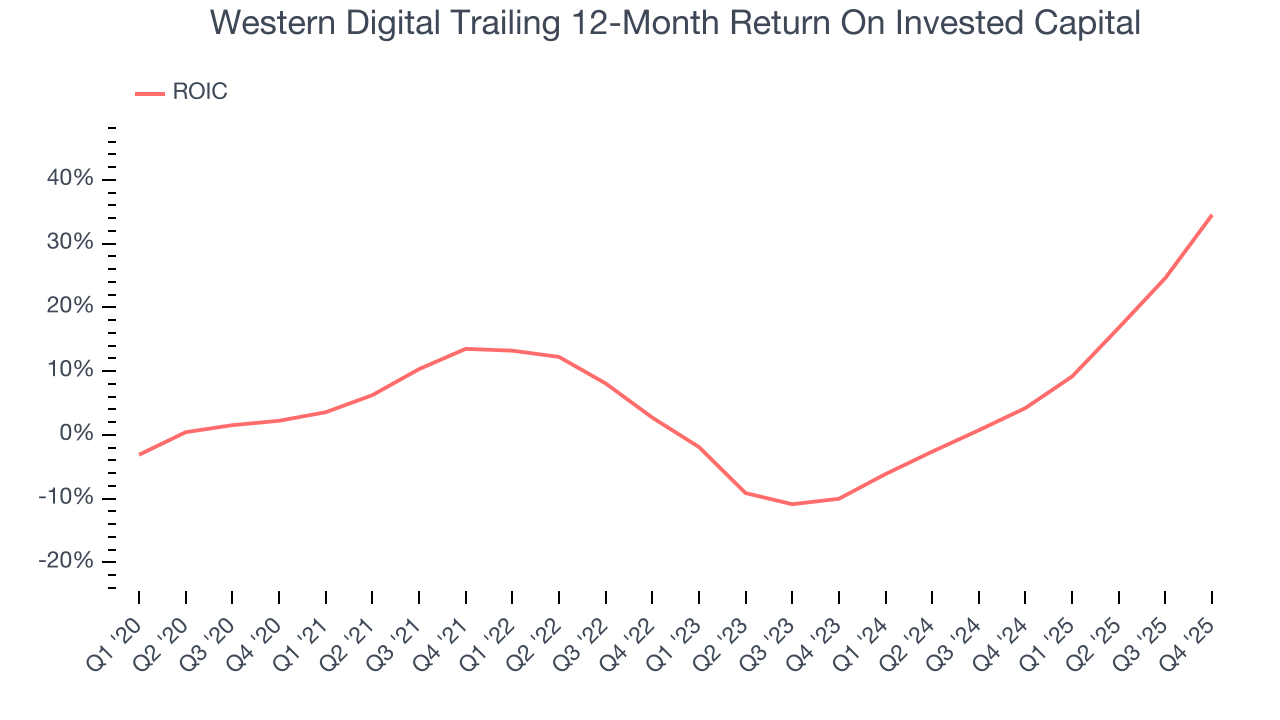

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Western Digital historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 9%, somewhat low compared to the best semiconductor companies that consistently pump out 35%+.

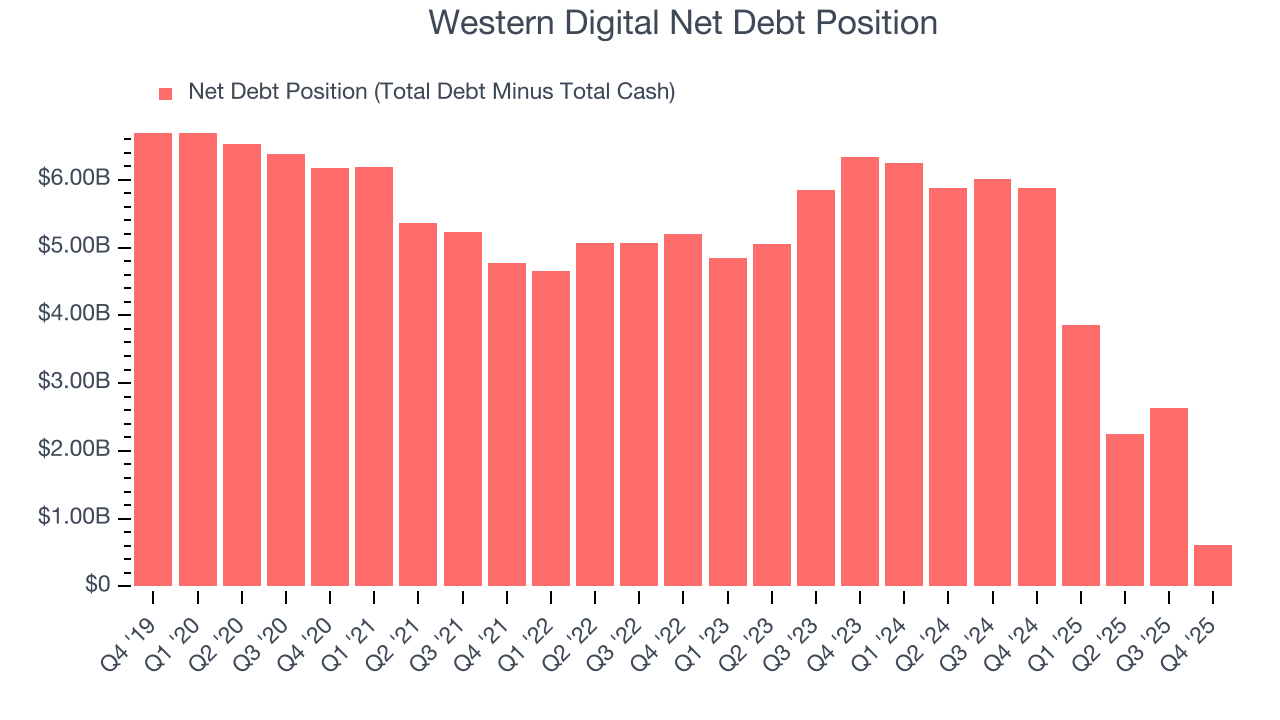

12. Balance Sheet Assessment

Western Digital reported $4.04 billion of cash and $4.66 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $3.55 billion of EBITDA over the last 12 months, we view Western Digital’s 0.2× net-debt-to-EBITDA ratio as safe. We also see its $877 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Western Digital’s Q4 Results

It was good to see Western Digital beat analysts’ EPS expectations this quarter. We were also excited its adjusted operating income outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock remained flat at $279.65 immediately following the results.

14. Is Now The Time To Buy Western Digital?

Updated: March 14, 2026 at 10:25 PM EDT

Before deciding whether to buy Western Digital or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Western Digital possesses a number of positive attributes. Although its revenue has declined over the last five years, its growth over the next 12 months is expected to be higher. And while Western Digital’s low gross margins indicate some combination of pricing pressures or rising production costs, its rising cash profitability gives it more optionality. On top of that, its expanding operating margin shows the business has become more efficient.

Western Digital’s P/E ratio based on the next 12 months is 23.1x. When scanning the semiconductor space, Western Digital trades at a fair valuation. If you trust the business and its direction, this is an ideal time to buy.

Wall Street analysts have a consensus one-year price target of $321 on the company (compared to the current share price of $271.91), implying they see 18.1% upside in buying Western Digital in the short term.