Ameris Bancorp (ABCB)

We’re wary of Ameris Bancorp. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Ameris Bancorp Is Not Exciting

Tracing its roots back to 1971 and expanding significantly through both organic growth and strategic acquisitions, Ameris Bancorp (NYSE:ABCB) is a financial holding company that provides a full range of banking services to retail and commercial customers across select markets in the southeastern United States.

- Annual revenue growth of 3.2% over the last five years was below our standards for the banking sector

- 7.7% annual net interest income growth over the last five years was slower than its banking peers

- A consolation is that its impressive 13.9% annual tangible book value per share growth over the last five years indicates it’s building equity value this cycle

Ameris Bancorp lacks the business quality we seek. There are better opportunities in the market.

Why There Are Better Opportunities Than Ameris Bancorp

Ameris Bancorp is trading at $76.81 per share, or 1.3x forward P/B. We acknowledge that the current valuation is justified, but we’re passing on this stock for the time being.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Ameris Bancorp (ABCB) Research Report: Q3 CY2025 Update

Regional banking company Ameris Bancorp (NYSE:ABCB) reported Q3 CY2025 results topping the market’s revenue expectations, with sales up 25.1% year on year to $355 million. Its non-GAAP profit of $1.53 per share was 4.1% above analysts’ consensus estimates.

Ameris Bancorp (ABCB) Q3 CY2025 Highlights:

- Net Interest Income: $238 million vs analyst estimates of $234.9 million (11.2% year-on-year growth, 1.3% beat)

- Net Interest Margin: 3.8% vs analyst estimates of 3.7% (7.5 basis point beat)

- Revenue: $355 million vs analyst estimates of $305.4 million (25.1% year-on-year growth, 16.3% beat)

- Efficiency Ratio: 49.5% vs analyst estimates of 51.4% (190.5 basis point beat)

- Adjusted EPS: $1.53 vs analyst estimates of $1.47 (4.1% beat)

- Tangible Book Value per Share: $42.90 vs analyst estimates of $42.50 (13.9% year-on-year growth, 0.9% beat)

- Market Capitalization: $5.06 billion

Company Overview

Tracing its roots back to 1971 and expanding significantly through both organic growth and strategic acquisitions, Ameris Bancorp (NYSE:ABCB) is a financial holding company that provides a full range of banking services to retail and commercial customers across select markets in the southeastern United States.

Ameris operates primarily through its banking subsidiary, Ameris Bank, which serves customers through numerous branches across Georgia, Alabama, Florida, North Carolina, and South Carolina. The bank offers a diverse portfolio of financial products, including commercial real estate loans, residential mortgages, agricultural financing, business loans, and consumer credit options.

The company's commercial lending activities support various sectors, from manufacturers and wholesalers to municipalities and service companies. For instance, a local retail business might secure an Ameris loan to expand operations or manage inventory, while a regional developer might obtain financing for commercial property construction. Ameris also participates in specialized lending programs, including SBA-guaranteed loans and agricultural financing that supports farmers with seasonal cash flow needs.

Beyond traditional banking, Ameris has expanded its revenue streams through strategic acquisitions and specialized services. The bank originates residential mortgages for both its portfolio and secondary market sales, and provides equipment financing, premium finance services, and government-guaranteed lending through national business lines that extend beyond its core southeastern footprint.

Ameris generates revenue primarily through interest income on loans and investments, as well as fees from deposit accounts and services. The company utilizes various funding sources, including traditional customer deposits, brokered deposits for specific maturity needs, and access to Federal Home Loan Bank advances secured by qualifying assets.

4. Regional Banks

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

Ameris Bancorp competes with other regional banks operating in the southeastern United States, including Synovus Financial (NYSE:SNV), United Community Banks (NASDAQ:UCBI), South State Corporation (NASDAQ:SSB), and Regions Financial Corporation (NYSE:RF), as well as national banking institutions with significant presence in its markets.

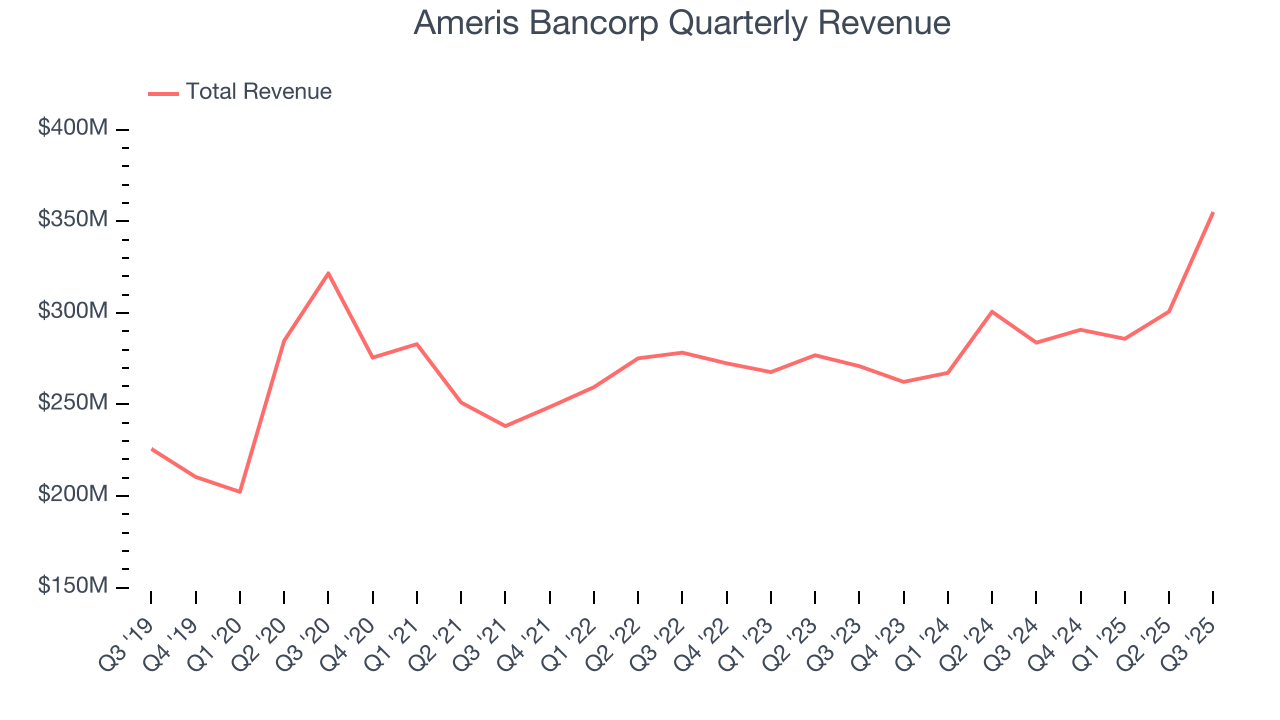

5. Sales Growth

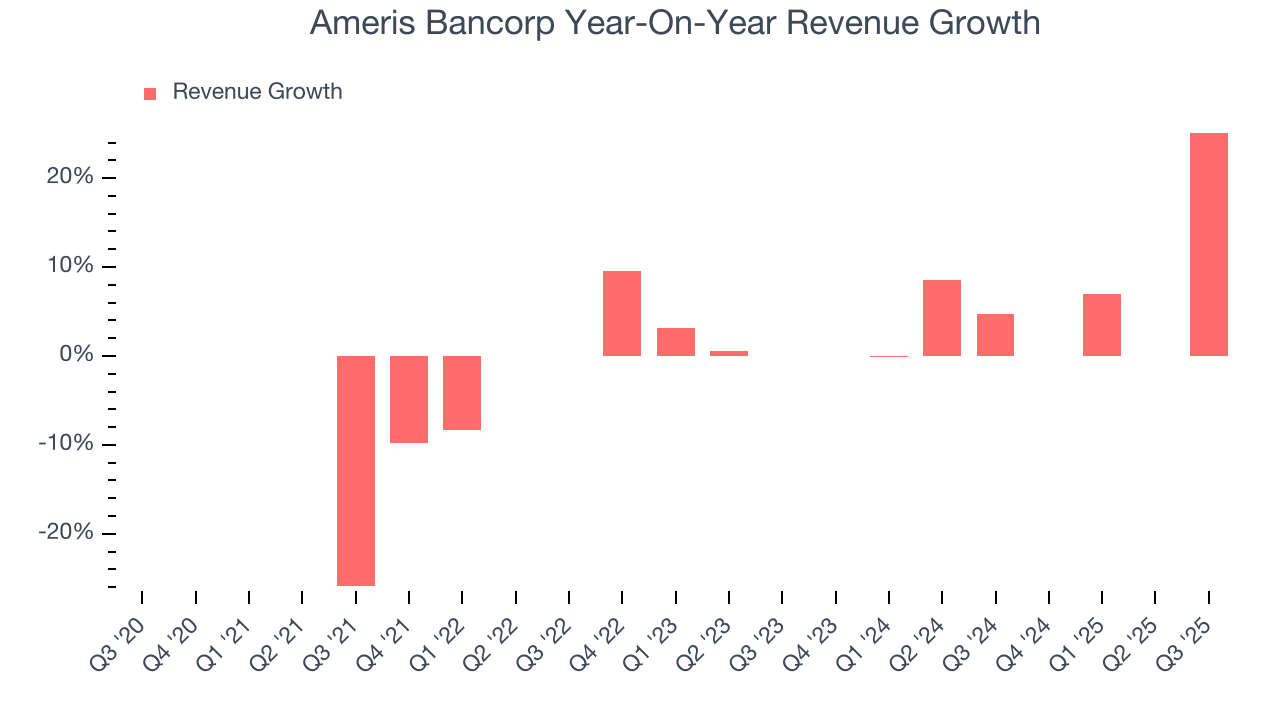

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Regrettably, Ameris Bancorp’s revenue grew at a mediocre 3.9% compounded annual growth rate over the last five years. This wasn’t a great result compared to the rest of the banking sector, but there are still things to like about Ameris Bancorp.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Ameris Bancorp’s annualized revenue growth of 6.4% over the last two years is above its five-year trend, suggesting some bright spots.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Ameris Bancorp reported robust year-on-year revenue growth of 25.1%, and its $355 million of revenue topped Wall Street estimates by 16.3%.

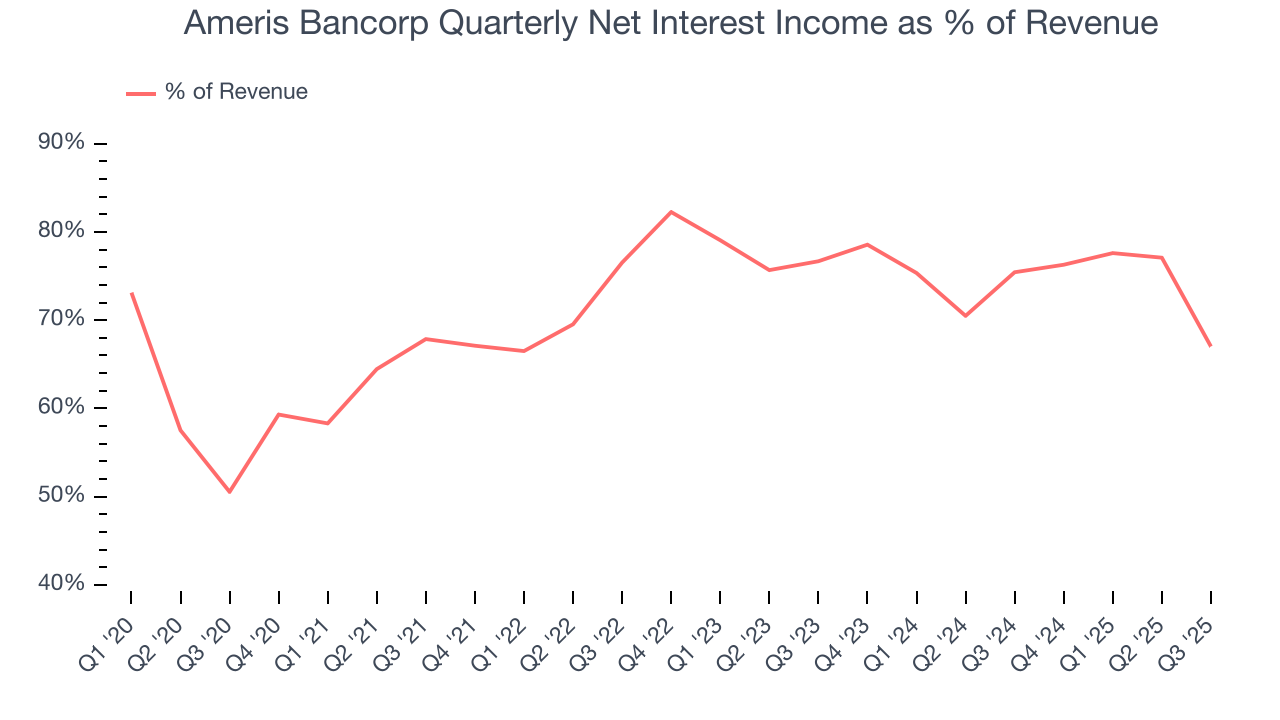

Net interest income made up 72.1% of the company’s total revenue during the last five years, meaning lending operations are Ameris Bancorp’s largest source of revenue.

While banks generate revenue from multiple sources, investors view net interest income as the cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of non-interest income.

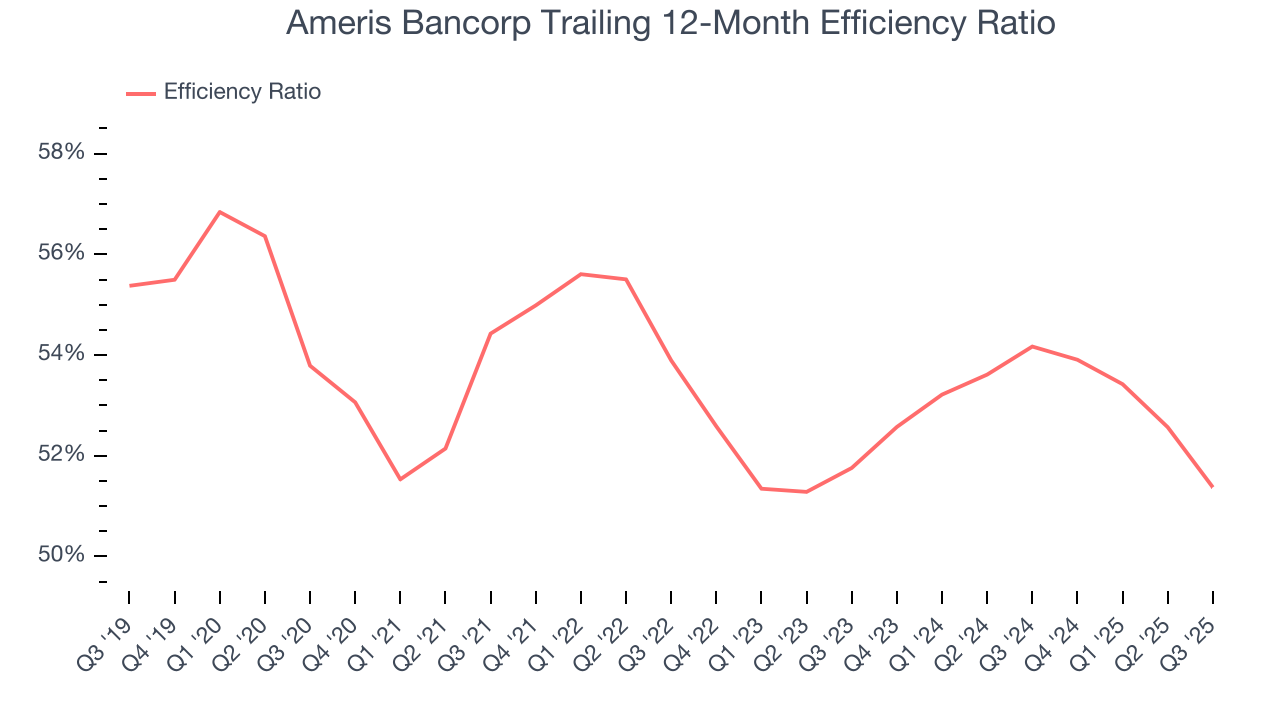

6. Efficiency Ratio

Topline growth alone doesn't tell the complete story - the profitability of that growth shapes actual earnings impact. Banks track this dynamic through efficiency ratios, which compare non-interest expenses such as personnel, rent, IT, and marketing costs to total revenue streams.

Investors focus on efficiency ratio changes rather than absolute levels, understanding that expense structures vary by revenue mix. Counterintuitively, lower efficiency ratios indicate better performance since they represent lower costs relative to revenue.

Over the last five years, Ameris Bancorp’s efficiency ratio has swelled by 2.4 percentage points, going from 54.4% to 51.4%. Said differently, the company’s expenses have grown at a slower rate than revenue, which typically signals prudent management.

Ameris Bancorp’s efficiency ratio came in at 49.5% this quarter, beating analysts’ expectations by 190.5 basis points (100 basis points = 1 percentage point). This result was 4.8 percentage points better than the same quarter last year.

For the next 12 months, Wall Street expects Ameris Bancorp to maintain its trailing one-year ratio with a projection of 51.2%.

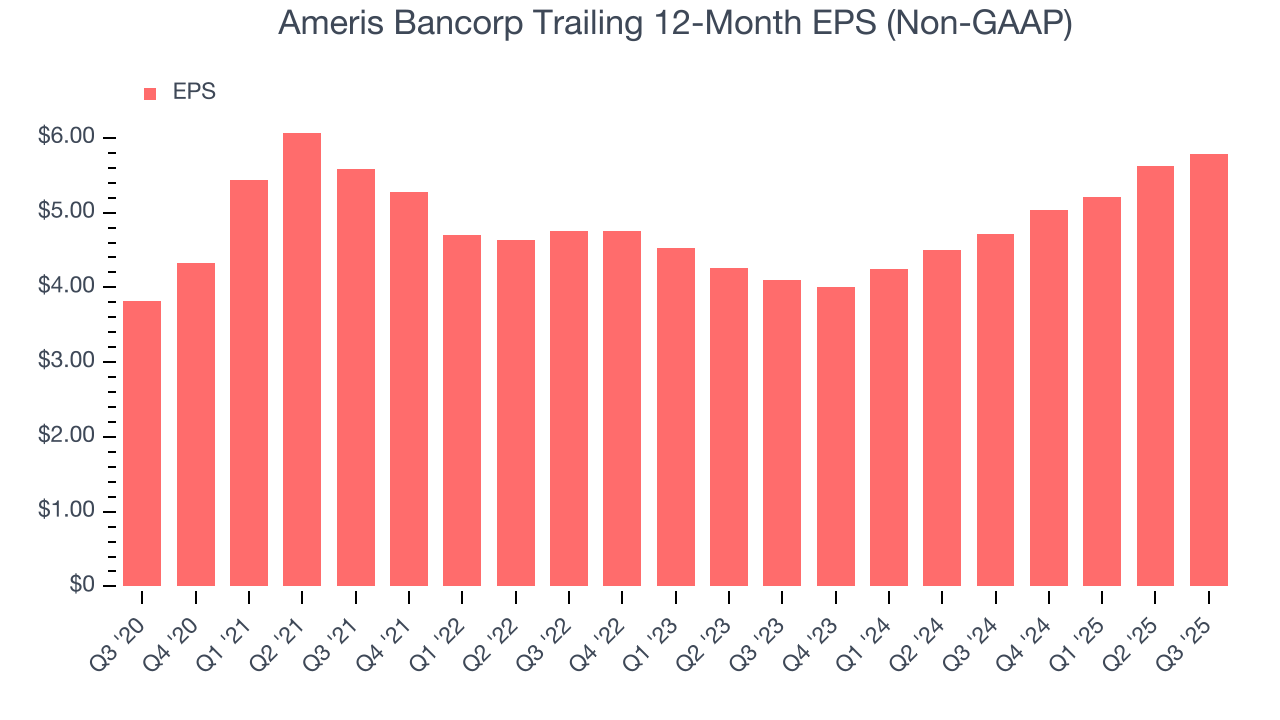

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Ameris Bancorp’s EPS grew at a spectacular 8.6% compounded annual growth rate over the last five years, higher than its 3.9% annualized revenue growth. However, we take this with a grain of salt because its efficiency ratio didn’t improve and it didn’t repurchase its shares, meaning the delta came from factors we consider non-core or less sustainable over the long term.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Ameris Bancorp, its two-year annual EPS growth of 18.7% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, Ameris Bancorp reported adjusted EPS of $1.53, up from $1.38 in the same quarter last year. This print beat analysts’ estimates by 4.1%. Over the next 12 months, Wall Street expects Ameris Bancorp’s full-year EPS of $5.78 to grow 3%.

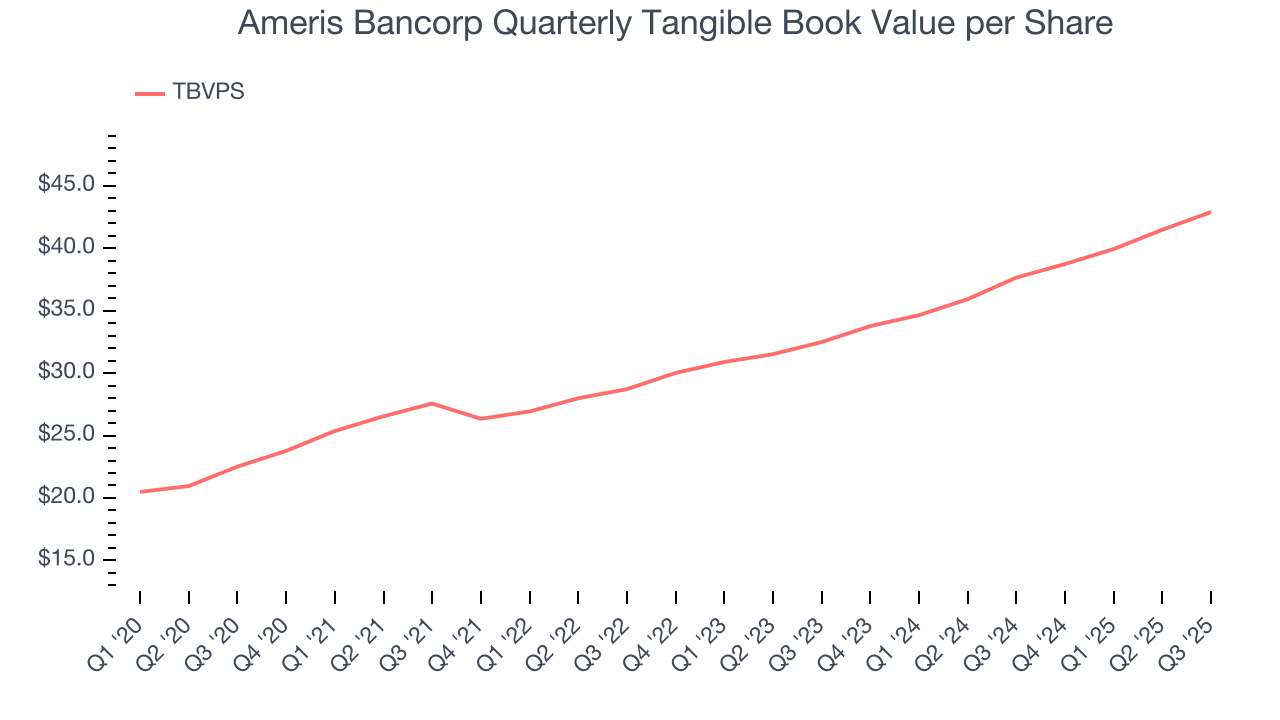

8. Tangible Book Value Per Share (TBVPS)

Banks are balance sheet-driven businesses because they generate earnings primarily through borrowing and lending. They’re also valued based on their balance sheet strength and ability to compound book value (another name for shareholders’ equity) over time.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. EPS can become murky due to acquisition impacts or accounting flexibility around loan provisions, and TBVPS resists financial engineering manipulation.

Ameris Bancorp’s TBVPS grew at an incredible 13.8% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 14.9% annually over the last two years from $32.49 to $42.90 per share.

Over the next 12 months, Consensus estimates call for Ameris Bancorp’s TBVPS to grow by 11.1% to $47.67, solid growth rate.

9. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, Ameris Bancorp has averaged a Tier 1 capital ratio of 12.1%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

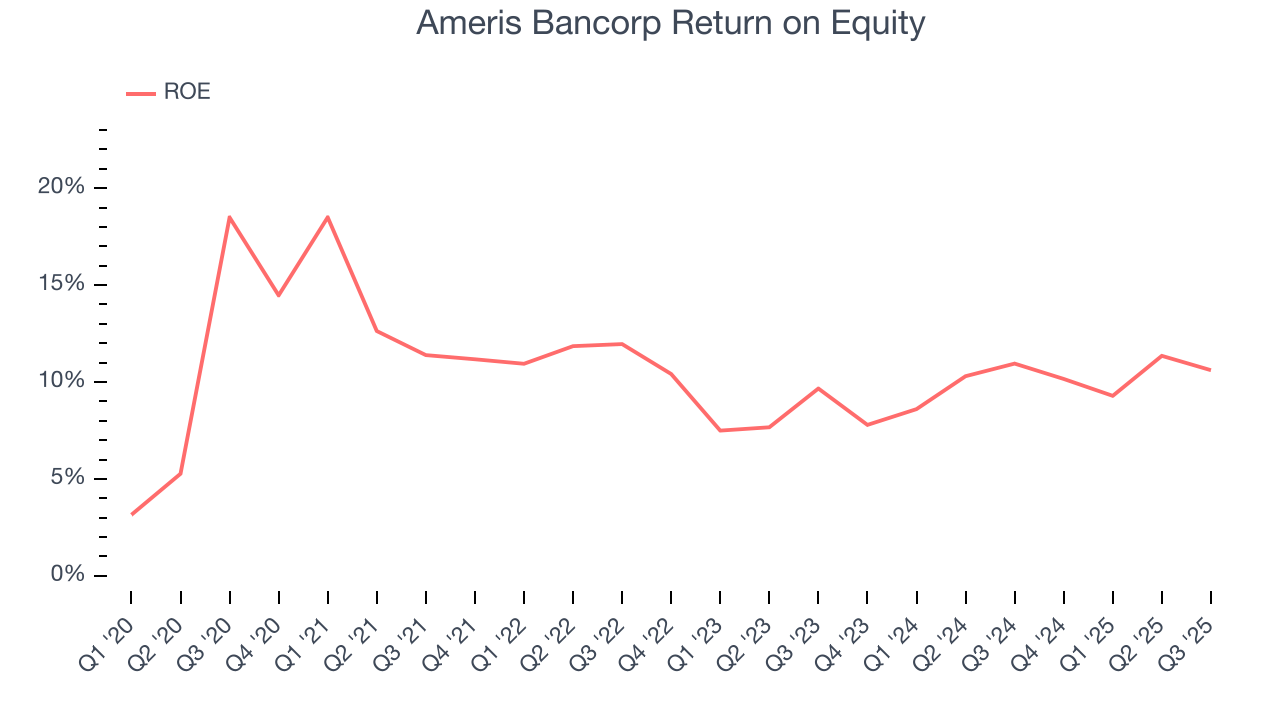

10. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Ameris Bancorp has averaged an ROE of 10.9%, impressive for a company operating in a sector where the average shakes out around 7.5% and those putting up 15%+ are greatly admired. This shows Ameris Bancorp has a strong competitive moat.

11. Key Takeaways from Ameris Bancorp’s Q3 Results

We were impressed by how significantly Ameris Bancorp blew past analysts’ revenue expectations this quarter. We were also happy its net interest income narrowly outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $74.48 immediately after reporting.

12. Is Now The Time To Buy Ameris Bancorp?

Updated: December 4, 2025 at 11:38 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Ameris Bancorp.

Ameris Bancorp isn’t a terrible business, but it doesn’t pass our bar. First off, its revenue growth was weak over the last five years. And while its TBVPS growth was exceptional over the last five years, the downside is its net interest income growth was uninspiring over the last five years. On top of that, its estimated net interest income for the next 12 months are weak.

Ameris Bancorp’s P/B ratio based on the next 12 months is 1.3x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $82.14 on the company (compared to the current share price of $76.81).