Abbott Laboratories (ABT)

Abbott Laboratories piques our interest. Although its sales growth has been weak, its profitability gives it the flexibility to ride out cycles.― StockStory Analyst Team

1. News

2. Summary

Why Abbott Laboratories Is Interesting

With roots dating back to 1888 when founder Dr. Wallace Abbott began producing precise, dosage-form medications, Abbott Laboratories (NYSE:ABT) develops and sells a diverse range of healthcare products including medical devices, diagnostics, nutrition products, and branded generic pharmaceuticals.

- Sizeable revenue base of $44.33 billion gives it economies of scale and advantages over new entrants due to the industry’s regulatory complexity

- Disciplined cost controls and effective management have materialized in a strong adjusted operating margin

- One risk is its large revenue base makes it harder to increase sales quickly, and its annual revenue growth of 5.1% over the last five years was below our standards for the healthcare sector

Abbott Laboratories has the potential to be a high-quality business. If you like the company, the price seems fair.

Why Is Now The Time To Buy Abbott Laboratories?

At $109.17 per share, Abbott Laboratories trades at 19.5x forward P/E. Compared to other healthcare companies, we think this multiple is fair for the quality you get.

It could be a good time to invest if you see something the market doesn’t.

3. Abbott Laboratories (ABT) Research Report: Q4 CY2025 Update

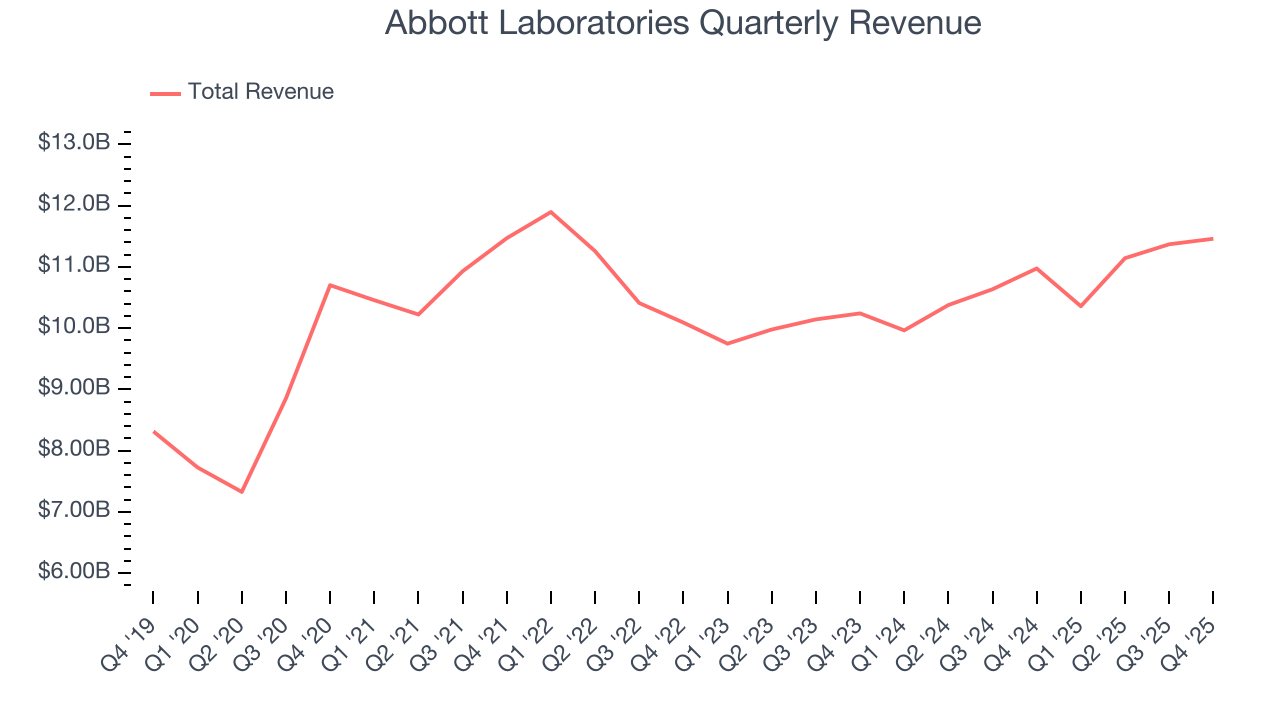

Healthcare product and device company Abbott Laboratories (NYSE:ABT) fell short of the markets revenue expectations in Q4 CY2025 as sales rose 4.4% year on year to $11.46 billion. Its non-GAAP profit of $1.50 per share was in line with analysts’ consensus estimates.

Abbott Laboratories (ABT) Q4 CY2025 Highlights:

- Revenue: $11.46 billion vs analyst estimates of $11.8 billion (4.4% year-on-year growth, 2.9% miss)

- Adjusted EPS: $1.50 vs analyst estimates of $1.49 (in line)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.68 at the midpoint, in line with analyst estimates

- Operating Margin: 19.6%, up from 17.4% in the same quarter last year

- Organic Revenue rose 3% year on year (miss)

- Market Capitalization: $209.9 billion

Company Overview

With roots dating back to 1888 when founder Dr. Wallace Abbott began producing precise, dosage-form medications, Abbott Laboratories (NYSE:ABT) develops and sells a diverse range of healthcare products including medical devices, diagnostics, nutrition products, and branded generic pharmaceuticals.

Abbott operates through four main business segments, each serving different healthcare needs. The Medical Devices segment produces cardiovascular and diabetes care products, including the FreeStyle Libre continuous glucose monitoring system, which allows diabetes patients to check glucose levels without painful fingersticks. This segment also offers heart devices like pacemakers, defibrillators, and the MitraClip system for repairing leaky heart valves.

The Diagnostics Products segment provides testing systems used by hospitals, laboratories, and other healthcare settings. These range from large automated laboratory instruments that can run hundreds of tests per hour to rapid point-of-care tests like the BinaxNOW platform, which gained prominence during the COVID-19 pandemic for detecting SARS-CoV-2.

In the Nutritional Products segment, Abbott manufactures infant formulas like Similac and adult nutritional products like Ensure. A hospital might use Abbott's specialized nutritional formulas like Glucerna for patients with diabetes or Nepro for those with kidney disease, while parents might choose Similac for infant feeding at home.

The Established Pharmaceutical Products segment focuses on selling branded generic medications in emerging markets. These include treatments for conditions ranging from digestive disorders to cardiovascular diseases, primarily sold outside the United States.

Abbott generates revenue through direct sales to healthcare institutions, distributors, retailers, and government agencies. The company maintains a global presence with manufacturing facilities and distribution networks spanning numerous countries, allowing it to serve healthcare needs across developed and developing markets alike.

4. Medical Devices & Supplies - Diversified

The medical devices industry operates a business model that balances steady demand with significant investments in innovation and regulatory compliance. The industry benefits from recurring revenue streams tied to consumables, maintenance services, and incremental upgrades to the latest technologies. However, the capital-intensive nature of product development, coupled with lengthy regulatory pathways and the need for clinical validation, can weigh on profitability and timelines. In addition, there are constant pricing pressures from healthcare systems and insurers maximizing cost efficiency. Over the next several years, one tailwind is demographic–aging populations means rising chronic disease rates that drive greater demand for medical interventions and monitoring solutions. Advances in digital health, such as remote patient monitoring and smart devices, are also expected to unlock new demand by shortening upgrade cycles. On the other hand, the industry faces headwinds from pricing and reimbursement pressures as healthcare providers increasingly adopt value-based care models. Additionally, the integration of cybersecurity for connected devices adds further risk and complexity for device manufacturers.

Abbott Laboratories competes with diversified healthcare companies like Johnson & Johnson (NYSE:JNJ) and Medtronic (NYSE:MDT) in medical devices, Roche (OTC:RHHBY) and Danaher (NYSE:DHR) in diagnostics, Nestlé (OTC:NSRGY) and Mead Johnson (owned by Reckitt Benckiser, OTC:RBGLY) in nutrition, and various pharmaceutical companies including Pfizer (NYSE:PFE) and Novartis (NYSE:NVS) in its established pharmaceuticals business.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $44.33 billion in revenue over the past 12 months, Abbott Laboratories boasts impressive economies of scale. It may not be as large as heavyweights such as UnitedHealth Group and The Cigna Group from a topline perspective, but its heft is still an important advantage in a healthcare industry that is heavily regulated, complex, and resource-intensive.

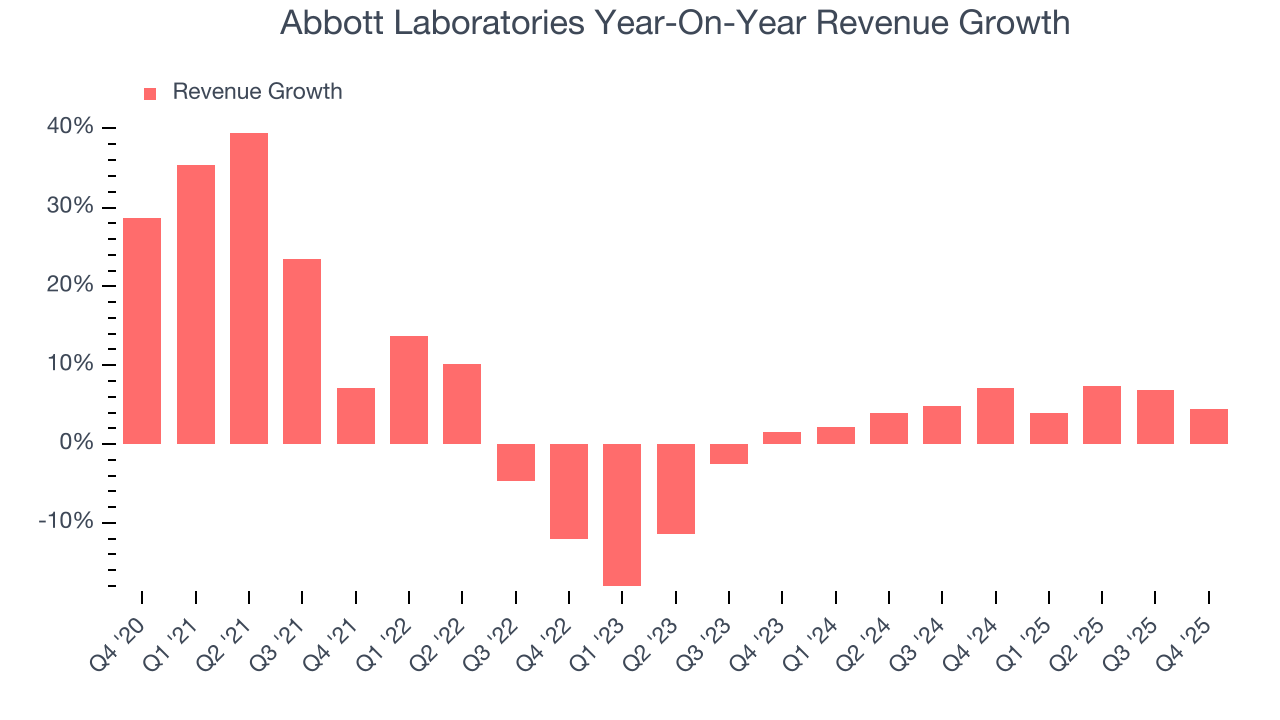

6. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Abbott Laboratories grew its sales at a mediocre 5.1% compounded annual growth rate. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Abbott Laboratories.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Abbott Laboratories’s annualized revenue growth of 5.1% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

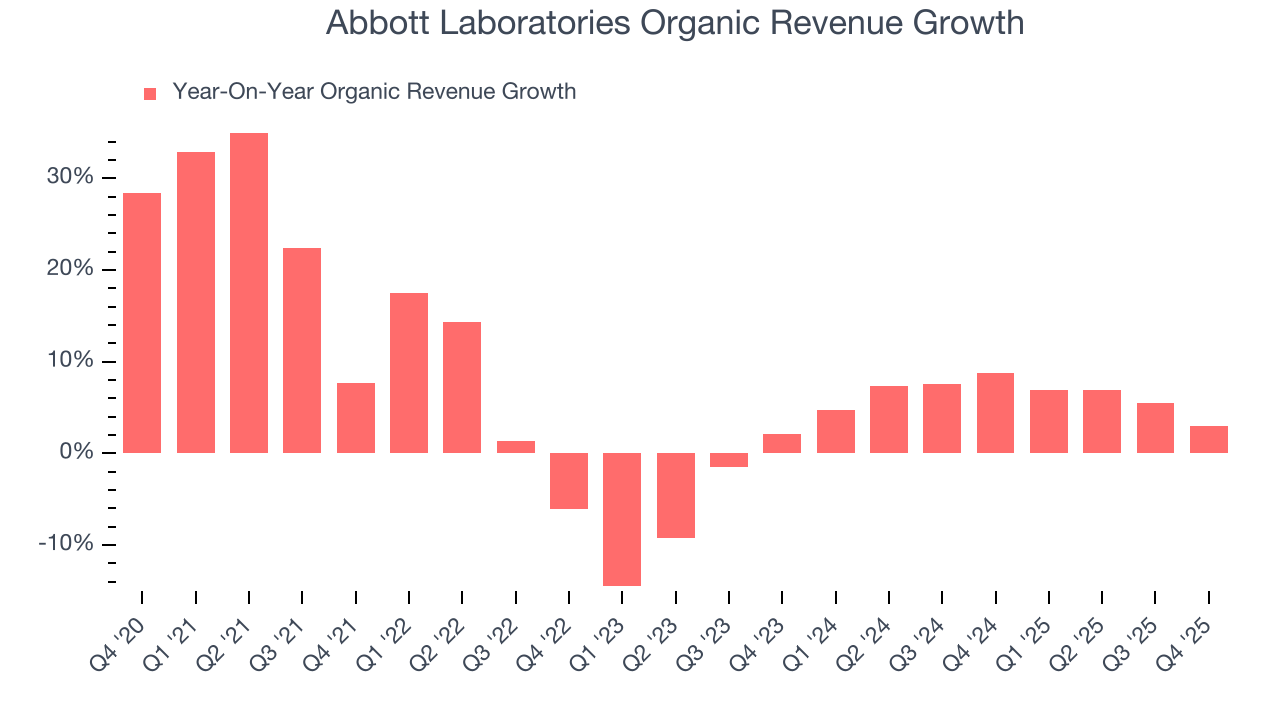

We can better understand the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Abbott Laboratories’s organic revenue averaged 6.4% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Abbott Laboratories’s revenue grew by 4.4% year on year to $11.46 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.8% over the next 12 months, an improvement versus the last two years. This projection is particularly noteworthy for a company of its scale and indicates its newer products and services will spur better top-line performance.

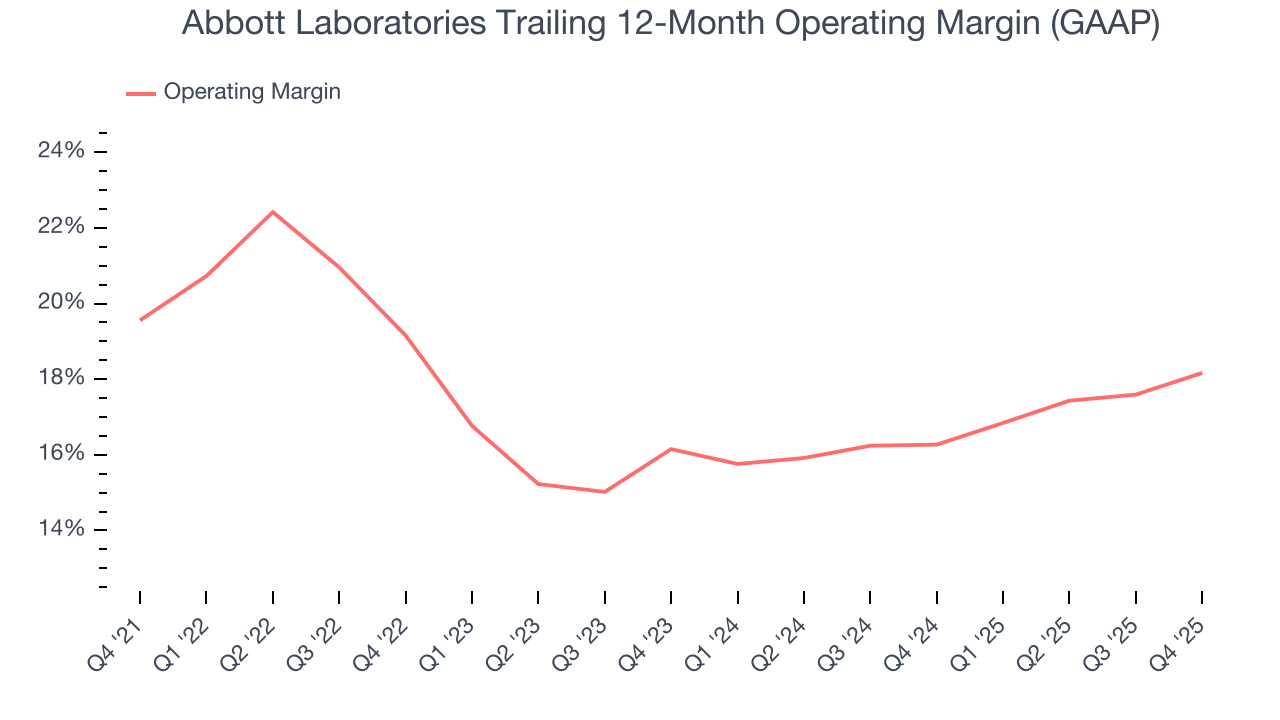

7. Operating Margin

Abbott Laboratories has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 17.9%.

Analyzing the trend in its profitability, Abbott Laboratories’s operating margin decreased by 1.4 percentage points over the last five years, but it rose by 2 percentage points on a two-year basis. We like Abbott Laboratories and hope it can right the ship.

This quarter, Abbott Laboratories generated an operating margin profit margin of 19.6%, up 2.2 percentage points year on year. This increase was a welcome development and shows it was more efficient.

8. Earnings Per Share

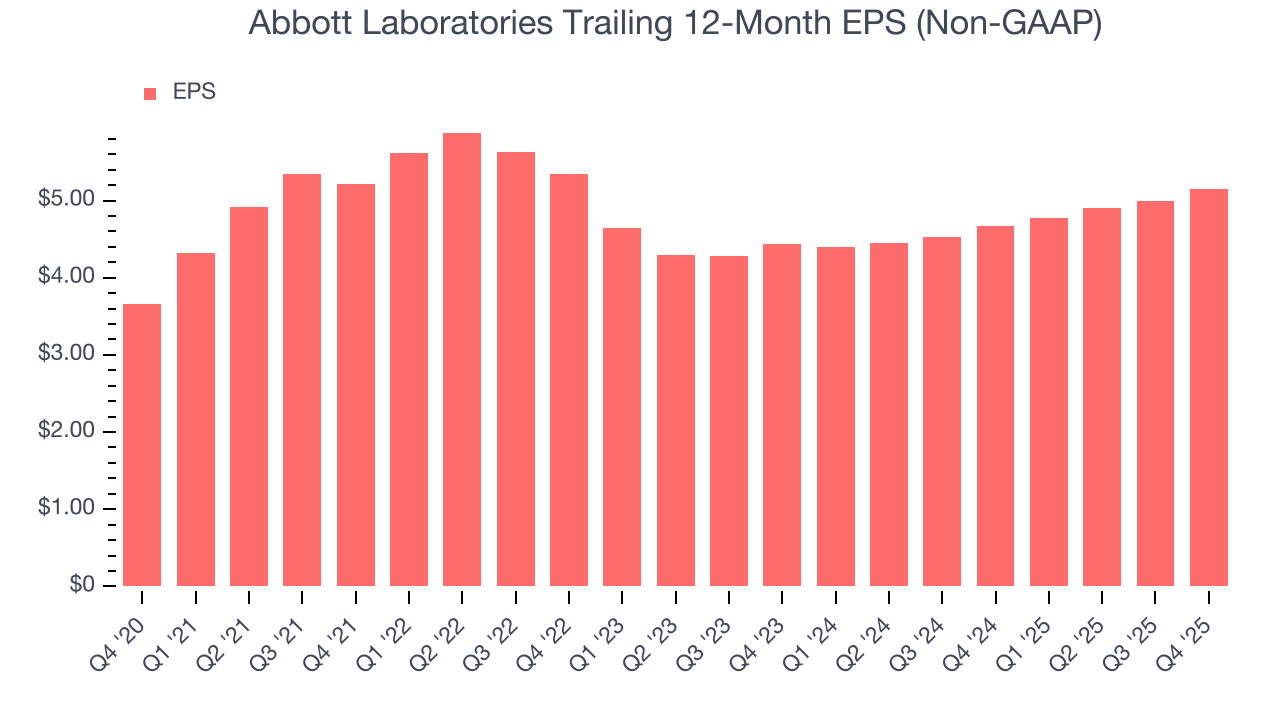

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Abbott Laboratories’s EPS grew at a solid 7.1% compounded annual growth rate over the last five years, higher than its 5.1% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

Diving into Abbott Laboratories’s quality of earnings can give us a better understanding of its performance. A five-year view shows that Abbott Laboratories has repurchased its stock, shrinking its share count by 2.3%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Abbott Laboratories reported adjusted EPS of $1.50, up from $1.34 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Abbott Laboratories’s full-year EPS of $5.15 to grow 9.9%.

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

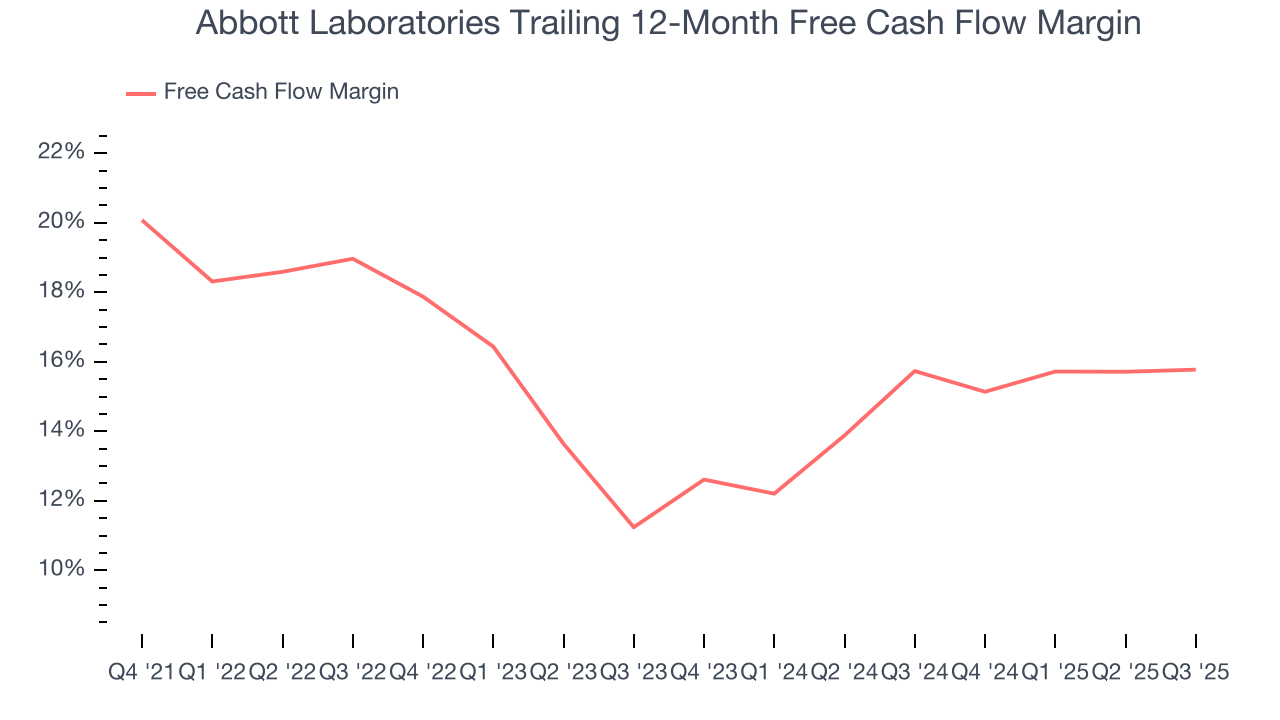

Abbott Laboratories has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 16.2% over the last five years, quite impressive for a healthcare business.

Taking a step back, we can see that Abbott Laboratories’s margin dropped by 5.1 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Abbott Laboratories’s five-year average ROIC was 13.6%, higher than most healthcare businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Abbott Laboratories’s ROIC averaged 3.9 percentage point decreases each year. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

11. Balance Sheet Assessment

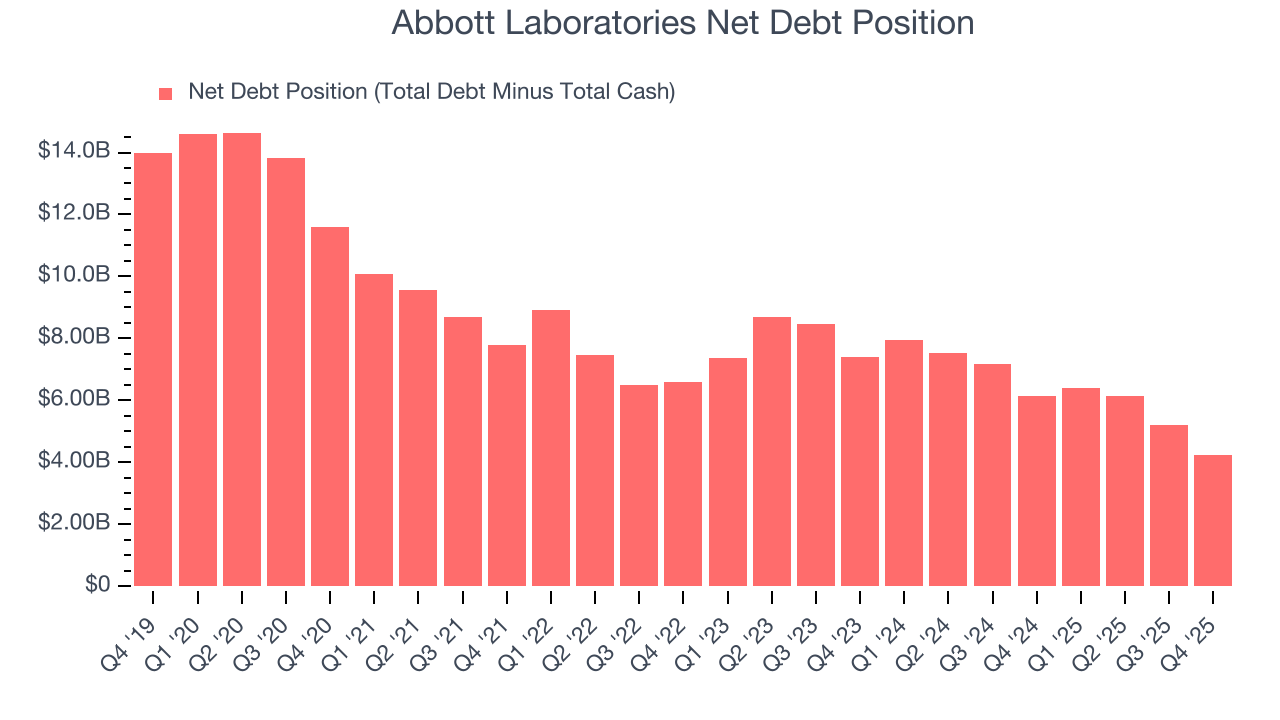

Abbott Laboratories reported $8.25 billion of cash and $12.49 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $11.73 billion of EBITDA over the last 12 months, we view Abbott Laboratories’s 0.4× net-debt-to-EBITDA ratio as safe. We also see its $185 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Abbott Laboratories’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its organic revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 5.5% to $114.10 immediately after reporting.

13. Is Now The Time To Buy Abbott Laboratories?

Updated: March 12, 2026 at 12:08 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Abbott Laboratories, you should also grasp the company’s longer-term business quality and valuation.

Abbott Laboratories is a fine business. Although its revenue growth was mediocre over the last five years, its growth over the next 12 months is expected to be higher. And while Abbott Laboratories’s diminishing returns show management's recent bets still have yet to bear fruit, its scale makes it a trusted partner with negotiating leverage. On top of that, its strong operating margins show it’s a well-run business.

Abbott Laboratories’s P/E ratio based on the next 12 months is 19.5x. Looking at the healthcare space right now, Abbott Laboratories trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $133.17 on the company (compared to the current share price of $109.17), implying they see 22% upside in buying Abbott Laboratories in the short term.