Artivion (AORT)

Artivion doesn’t excite us. Its underwhelming returns on capital show it struggled to generate meaningful profits for shareholders.― StockStory Analyst Team

1. News

2. Summary

Why We Think Artivion Will Underperform

Formerly known as CryoLife until its 2022 rebranding, Artivion (NYSE:AORT) develops and manufactures medical devices and preserves human tissues used in cardiac and vascular surgical procedures for patients with aortic disease.

- Subscale operations are evident in its revenue base of $441.3 million, meaning it has fewer distribution channels than its larger rivals

- Low returns on capital reflect management’s struggle to allocate funds effectively

- On the plus side, its incremental sales significantly boosted profitability as its annual earnings per share growth of 22.3% over the last five years outstripped its revenue performance

Artivion falls short of our quality standards. We’ve identified better opportunities elsewhere.

Why There Are Better Opportunities Than Artivion

Artivion’s stock price of $36.39 implies a valuation ratio of 44.7x forward P/E. This valuation multiple seems a bit much considering the quality you get.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Artivion (AORT) Research Report: Q4 CY2025 Update

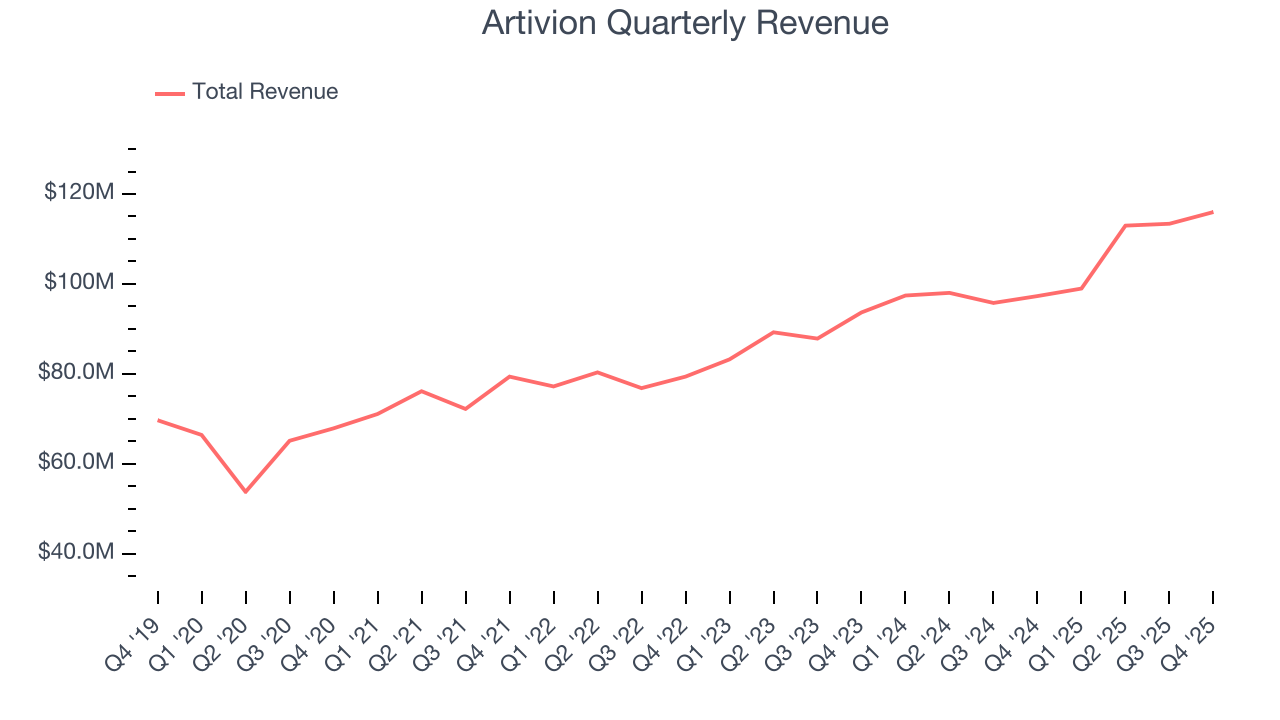

Medical device company Artivion (NYSE:AORT) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 19.2% year on year to $116 million. On the other hand, the company’s full-year revenue guidance of $495 million at the midpoint came in 1% above analysts’ estimates. Its non-GAAP profit of $0.17 per share was in line with analysts’ consensus estimates.

Artivion (AORT) Q4 CY2025 Highlights:

- Revenue: $116 million vs analyst estimates of $117 million (19.2% year-on-year growth, 0.8% miss)

- Adjusted EPS: $0.17 vs analyst estimates of $0.18 (in line)

- Adjusted EBITDA: $22.72 million vs analyst estimates of $22.67 million (19.6% margin, in line)

- EBITDA guidance for the upcoming financial year 2026 is $107.5 million at the midpoint, above analyst estimates of $106.5 million

- Operating Margin: 9.2%, up from 2.7% in the same quarter last year

- Free Cash Flow was -$7.95 million, down from $8.71 million in the same quarter last year

- Market Capitalization: $1.9 billion

Company Overview

Formerly known as CryoLife until its 2022 rebranding, Artivion (NYSE:AORT) develops and manufactures medical devices and preserves human tissues used in cardiac and vascular surgical procedures for patients with aortic disease.

Artivion's product portfolio focuses on four major families: aortic stent grafts, surgical sealants, mechanical heart valves, and implantable human tissues. The company's aortic stent grafts include highly specialized devices like the E-vita Open NEO and the Ascyrus Medical Dissection Stent (AMDS) for treating complex aortic conditions such as aneurysms and dissections. Its BioGlue surgical adhesive provides stronger bonding than competing products, making it valuable for sealing surgical wounds in cardiac procedures.

The company's On-X mechanical heart valves feature a unique pyrolytic carbon coating that provides a smooth microstructure surface, designed to reduce complications like blood clotting. For patients requiring tissue-based solutions, Artivion preserves human cardiac and vascular tissues that more closely mimic the patient's own tissue compared to synthetic alternatives.

Surgeons might use Artivion's products in various scenarios – for example, a cardiac surgeon could implant an On-X mechanical heart valve in a patient with severe aortic stenosis, or use the AMDS hybrid prosthesis during emergency surgery for a life-threatening aortic dissection. A vascular surgeon might use Artivion's preserved human saphenous veins for peripheral bypass procedures to restore blood flow to a patient's leg.

Artivion generates revenue through direct sales to hospitals and healthcare facilities in the US and Canada, while using a combination of direct sales and distributors in international markets. The company maintains manufacturing operations in Austin, Texas; Hechingen, Germany; and Kennesaw, Georgia, with additional contract manufacturing partnerships.

Artivion invests significantly in research and development, spending approximately $28.7 million in 2023 to advance its product pipeline. The company also provides extensive physician education, including workshops and training programs to help surgeons master techniques for using its specialized products.

4. Medical Devices & Supplies - Cardiology, Neurology, Vascular

The medical devices and supplies industry, particularly in the fields of cardiology, neurology, and vascular care, benefits from a business model that balances innovation with relatively predictable revenue streams. These companies focus on developing life-saving devices such as stents, pacemakers, neurostimulation implants, and vascular access tools, which address critical and often chronic conditions. The recurring need for these devices, coupled with growing global demand for advanced treatments, provides stability and opportunities for long-term growth. However, the industry faces hurdles such as high research and development costs, rigorous regulatory approval processes, and reliance on reimbursement from healthcare systems, which can exert downward pressure on pricing. Looking ahead, the industry is positioned to benefit from tailwinds such as aging populations (which tend to have higher rates of disease) and technological advancements like minimally invasive procedures and connected devices that improve patient monitoring and outcomes. Innovations in robotic-assisted surgery and AI-driven diagnostics are also expected to accelerate adoption and expand treatment capabilities. However, potential headwinds include pricing pressures stemming from value-based care models and continued complexity changing from navigating regulatory frameworks that may prioritize further lowering healthcare costs.

Artivion competes with several major medical device companies across its product lines. In mechanical heart valves, its main competitors include Abbott Laboratories, Medtronic, and Corcym. For aortic stent grafts, it competes with Medtronic, Gore, Terumo, Cook, and BD. In the surgical sealants market, Artivion faces competition from Baxter, Ethicon, and Integra LifeSciences.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $441.3 million in revenue over the past 12 months, Artivion is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

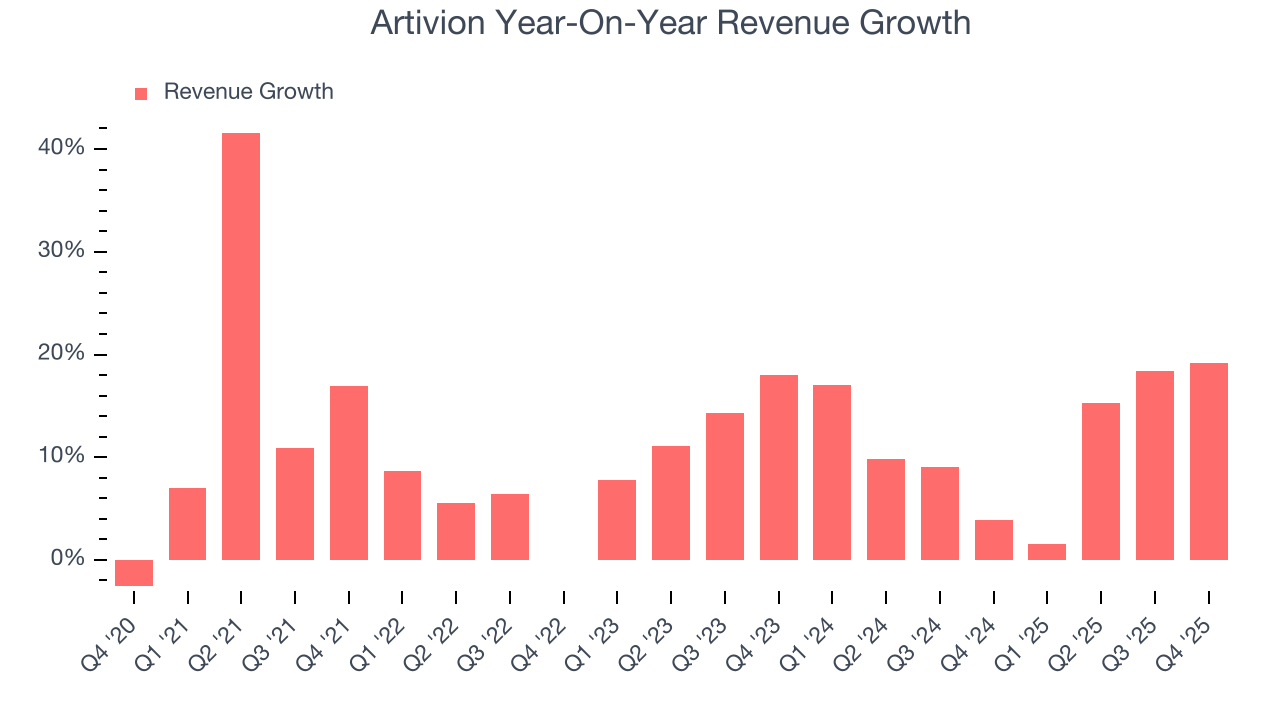

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Thankfully, Artivion’s 11.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Artivion’s annualized revenue growth of 11.7% over the last two years aligns with its five-year trend, suggesting its demand was stable.

This quarter, Artivion’s revenue grew by 19.2% year on year to $116 million but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 11.3% over the next 12 months, similar to its two-year rate. This projection is noteworthy and suggests the market is forecasting success for its products and services.

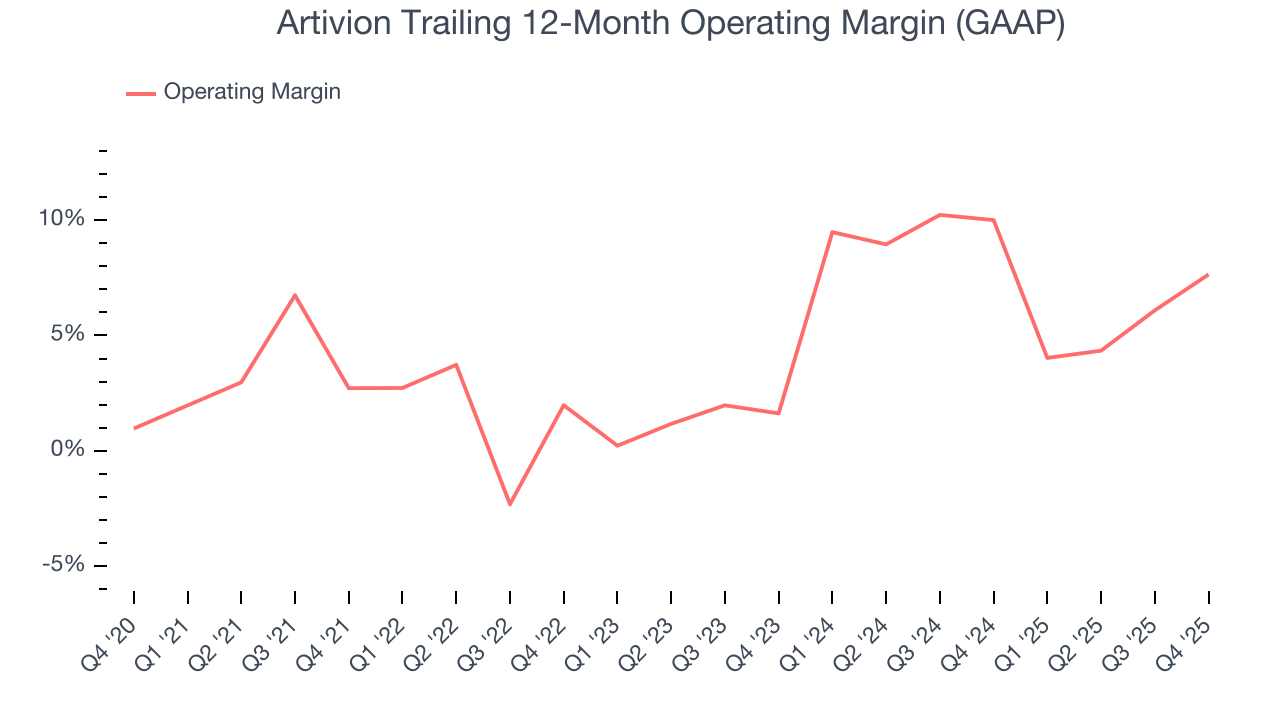

7. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Artivion was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.2% was weak for a healthcare business.

On the plus side, Artivion’s operating margin rose by 4.9 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 6 percentage points on a two-year basis.

In Q4, Artivion generated an operating margin profit margin of 9.2%, up 6.5 percentage points year on year. This increase was a welcome development and shows it was more efficient.

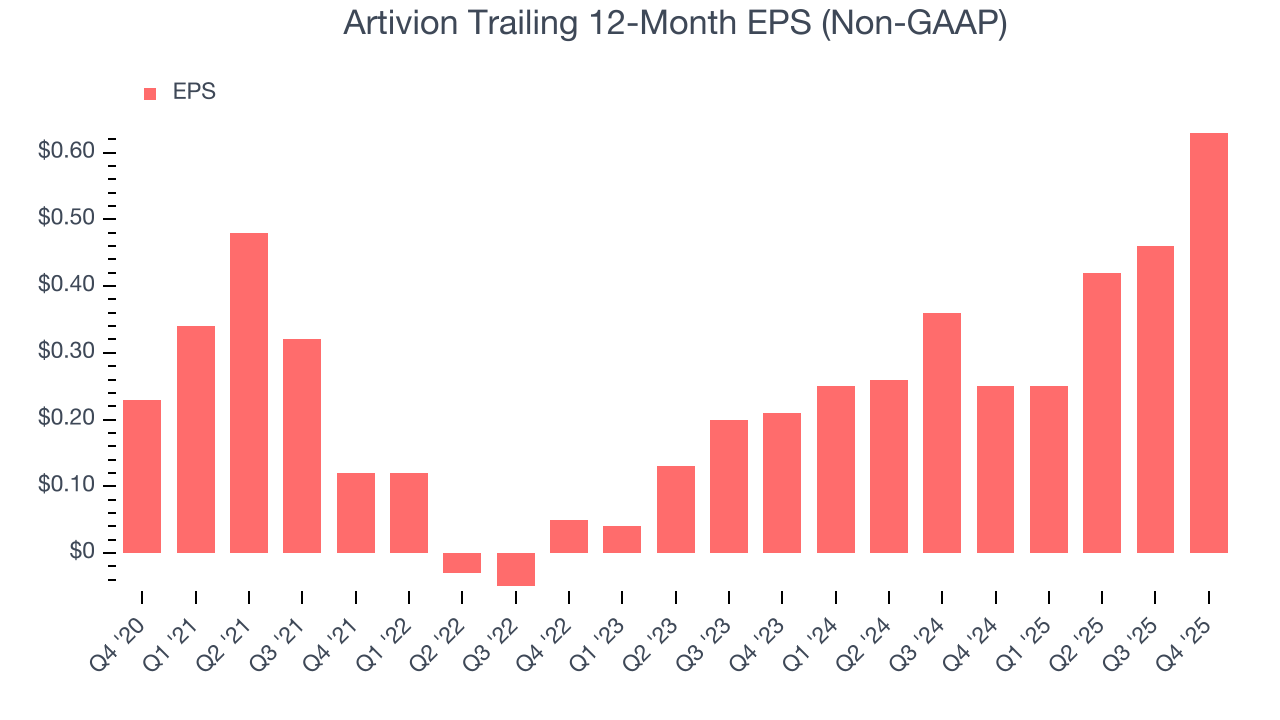

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Artivion’s EPS grew at an astounding 22.3% compounded annual growth rate over the last five years, higher than its 11.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of Artivion’s earnings can give us a better understanding of its performance. As we mentioned earlier, Artivion’s operating margin expanded by 4.9 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Artivion reported adjusted EPS of $0.17, up from $0 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Artivion’s full-year EPS of $0.63 to grow 35.7%.

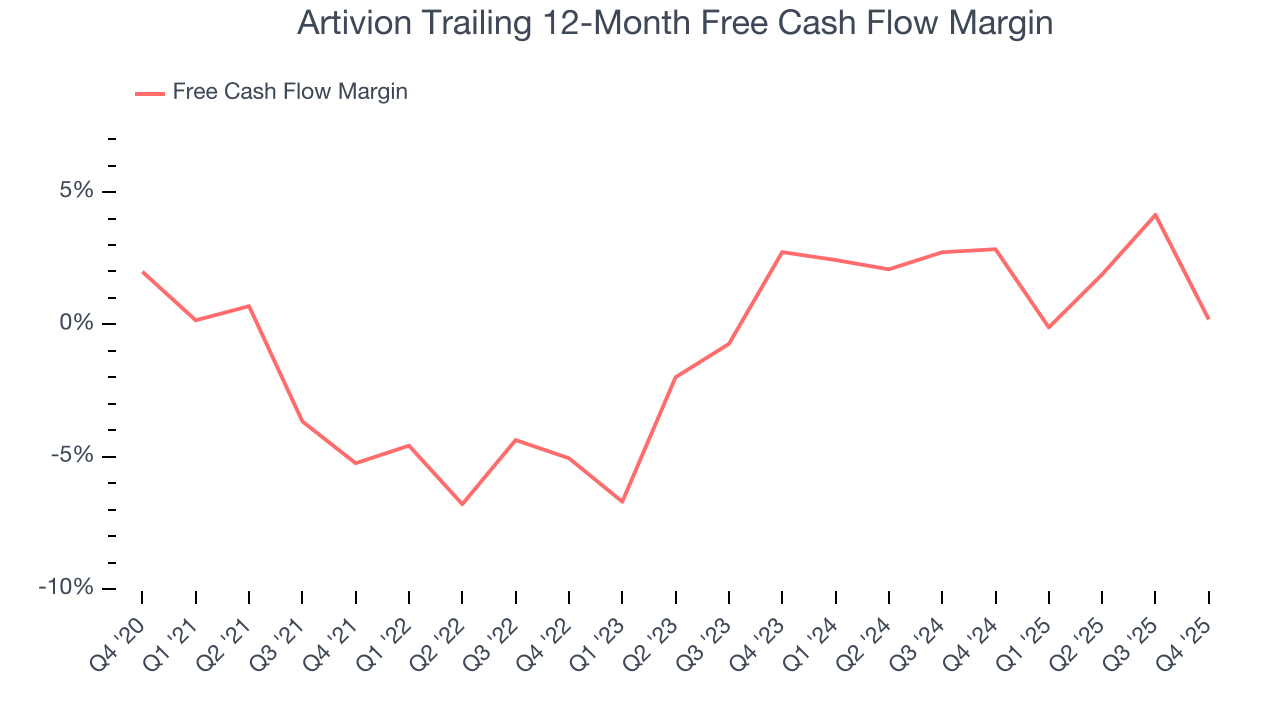

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Artivion broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, an encouraging sign is that Artivion’s margin expanded by 5.4 percentage points during that time. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Artivion burned through $7.95 million of cash in Q4, equivalent to a negative 6.9% margin. The company’s cash flow turned negative after being positive in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

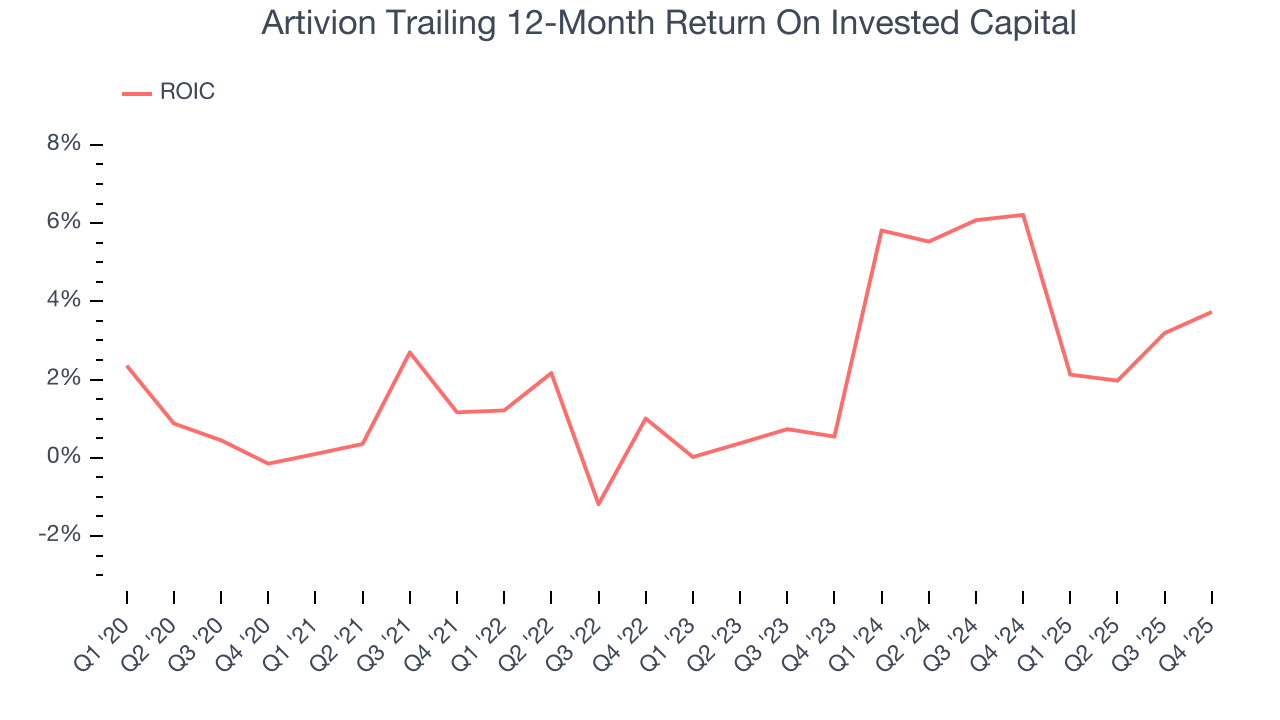

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Artivion historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 2.5%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Artivion’s ROIC averaged 3.9 percentage point increases each year over the last few years. This is a good sign, and we hope the company can continue improving.

11. Balance Sheet Assessment

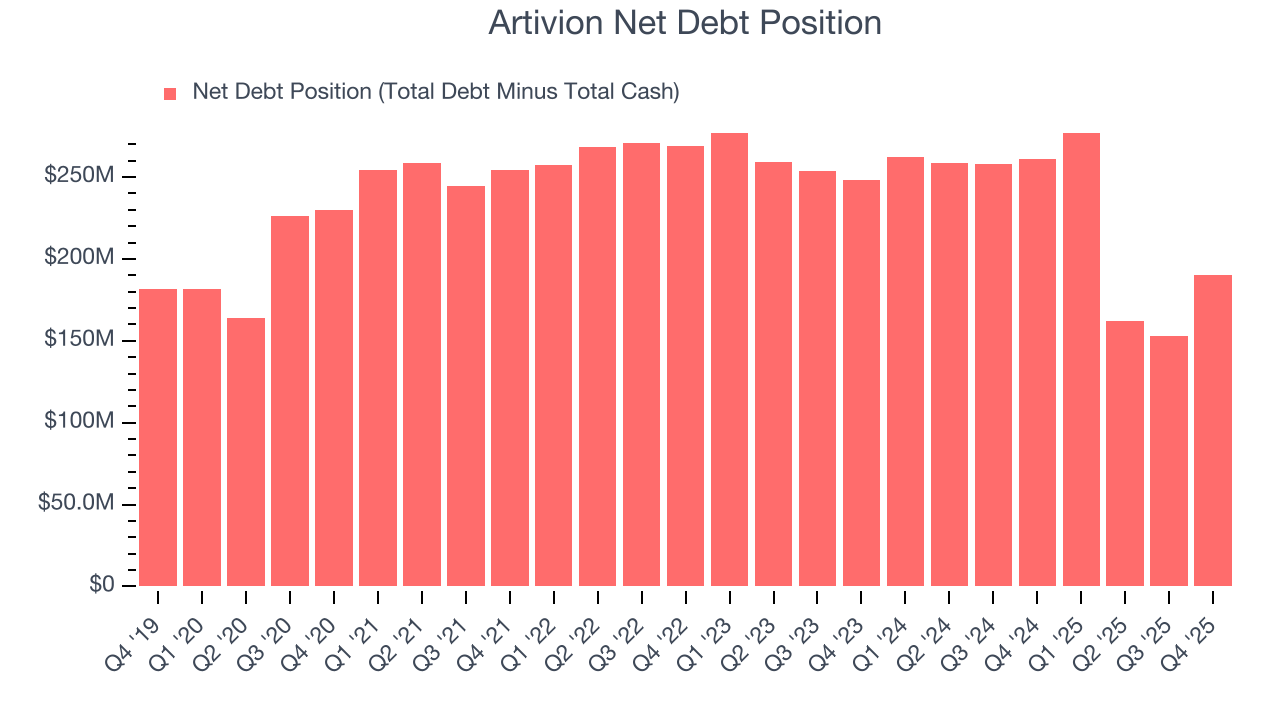

Artivion reported $64.91 million of cash and $254.9 million of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $89.6 million of EBITDA over the last 12 months, we view Artivion’s 2.1× net-debt-to-EBITDA ratio as safe. We also see its $15.38 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Artivion’s Q4 Results

It was good to see Artivion provide full-year revenue guidance that slightly beat analysts’ expectations. On the other hand, its EPS was in line and its revenue fell slightly short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.6% to $39.61 immediately following the results.

13. Is Now The Time To Buy Artivion?

Updated: March 14, 2026 at 11:44 PM EDT

Are you wondering whether to buy Artivion or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Artivion isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was good over the last five years and Wall Street believes it will continue to grow, its subscale operations give it fewer distribution channels than its larger rivals. And while the company’s rising cash profitability gives it more optionality, the downside is its mediocre ROIC lags the market and is a headwind for its stock price.

Artivion’s P/E ratio based on the next 12 months is 44.7x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $51.43 on the company (compared to the current share price of $36.39).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.