Artisan Partners (APAM)

We’re skeptical of Artisan Partners. Its revenue and earnings have underwhelmed, suggesting weak business fundamentals.― StockStory Analyst Team

1. News

2. Summary

Why We Think Artisan Partners Will Underperform

Founded in 1994 with a focus on autonomous investment teams and a "high-value-added" approach, Artisan Partners (NYSE:APAM) is an investment management firm that offers actively managed equity and fixed income strategies to institutional and individual investors.

- Performance over the past five years shows its incremental sales were less profitable, as its 3.4% annual earnings per share growth trailed its revenue gains

- Muted 5.9% annual revenue growth over the last five years shows its demand lagged behind its financials peers

Artisan Partners’s quality is not up to our standards. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Artisan Partners

Artisan Partners’s stock price of $38.43 implies a valuation ratio of 9.3x forward P/E. This sure is a cheap multiple, but you get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Artisan Partners (APAM) Research Report: Q4 CY2025 Update

Asset management firm Artisan Partners (NYSE:APAM) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 13% year on year to $335.5 million. Its non-GAAP profit of $1.26 per share was 15.9% above analysts’ consensus estimates.

Artisan Partners (APAM) Q4 CY2025 Highlights:

- Assets Under Management: $180.9 billion vs analyst estimates of $183.6 billion (12.2% year-on-year growth, 1.5% miss)

- Revenue: $335.5 million vs analyst estimates of $323.5 million (13% year-on-year growth, 3.7% beat)

- Pre-tax Profit: $147.5 million (44% margin)

- Adjusted EPS: $1.26 vs analyst estimates of $1.09 (15.9% beat)

- Market Capitalization: $3.20 billion

Company Overview

Founded in 1994 with a focus on autonomous investment teams and a "high-value-added" approach, Artisan Partners (NYSE:APAM) is an investment management firm that offers actively managed equity and fixed income strategies to institutional and individual investors.

Artisan Partners operates through a distinctive business model that emphasizes investment autonomy. The firm structures itself around independent investment teams, each with its own unique investment process and philosophy. These teams manage a range of investment strategies across global equities, U.S. equities, emerging markets, and fixed income. This autonomous structure allows portfolio managers to pursue their investment approaches without corporate interference while benefiting from the firm's operational infrastructure.

The company serves a diverse client base that includes public and corporate pension plans, foundations, endowments, sovereign wealth funds, financial advisors, and individual investors. These clients turn to Artisan for specialized investment expertise that aims to deliver long-term returns that outperform market benchmarks. For example, a university endowment might allocate a portion of its assets to Artisan's Global Opportunities strategy to gain exposure to growth companies worldwide.

Artisan generates revenue primarily through management fees calculated as a percentage of assets under management (AUM). The fee structure typically varies by investment strategy, with specialized or higher-performing strategies commanding premium rates. The firm distributes its investment products through multiple channels, including directly to institutions, through financial intermediaries, and via separately managed accounts for high-net-worth individuals. Artisan maintains offices across the United States and in London, Dublin, Singapore, and Sydney, allowing it to serve clients globally and source investment opportunities in markets worldwide.

4. Asset Management

Asset management firms oversee investment portfolios for institutions and individuals. The industry benefits from the growing global wealth pool, retirement savings needs, and expansion into alternative investments (private equity, real estate, etc.). However, firms face significant pressure from the shift to lower-cost passive investment products, regulatory requirements for fee transparency, and increasing technology costs to stay competitive in portfolio management and client service.

Artisan Partners competes with other publicly traded asset managers such as T. Rowe Price (NASDAQ:TROW), BlackRock (NYSE:BLK), Franklin Resources (NYSE:BEN), and Invesco (NYSE:IVZ), as well as privately held firms like Fidelity Investments and Capital Group.

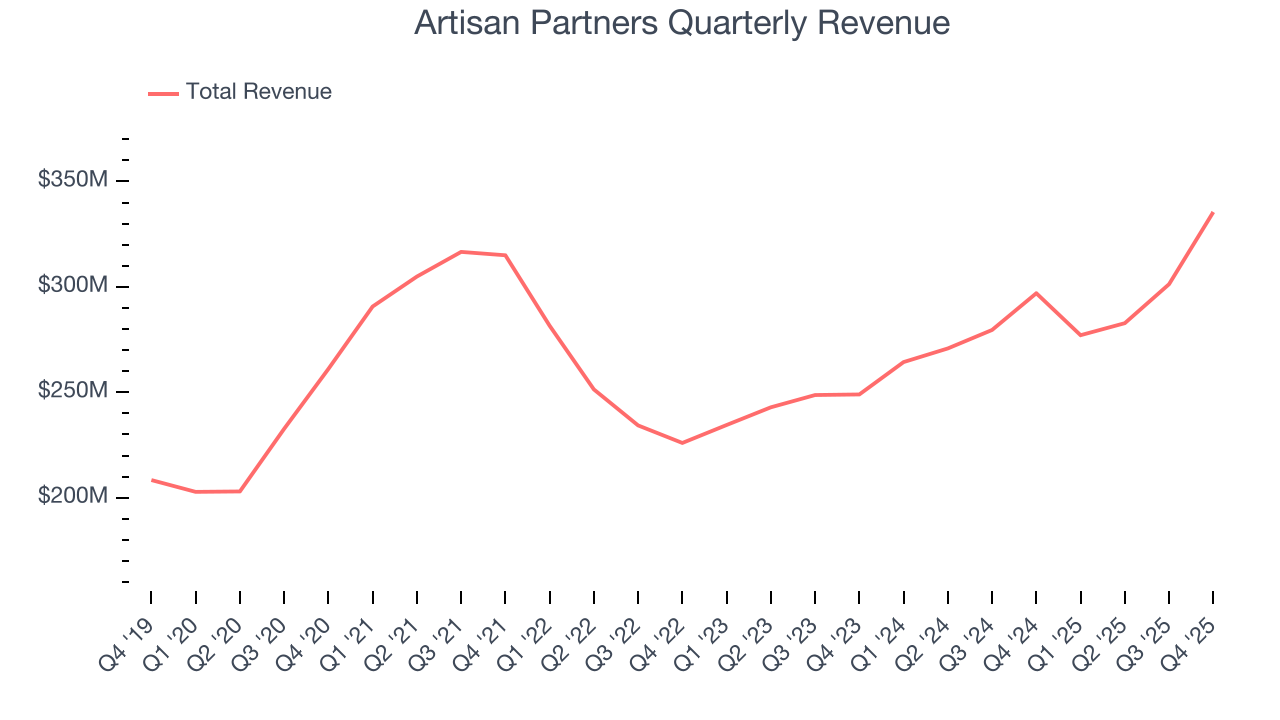

5. Revenue Growth

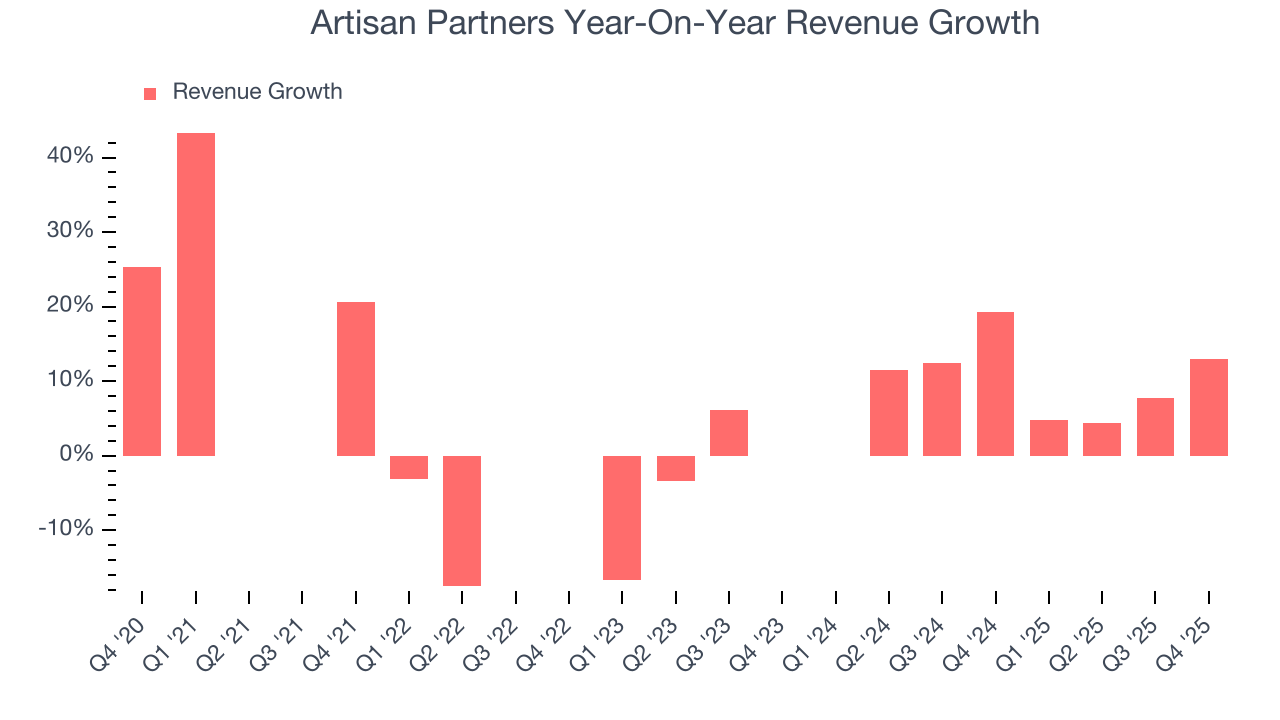

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Artisan Partners’s revenue grew at a tepid 5.9% compounded annual growth rate over the last five years. This was below our standard for the financials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Artisan Partners’s annualized revenue growth of 10.8% over the last two years is above its five-year trend, suggesting some bright spots.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Artisan Partners reported year-on-year revenue growth of 13%, and its $335.5 million of revenue exceeded Wall Street’s estimates by 3.7%.

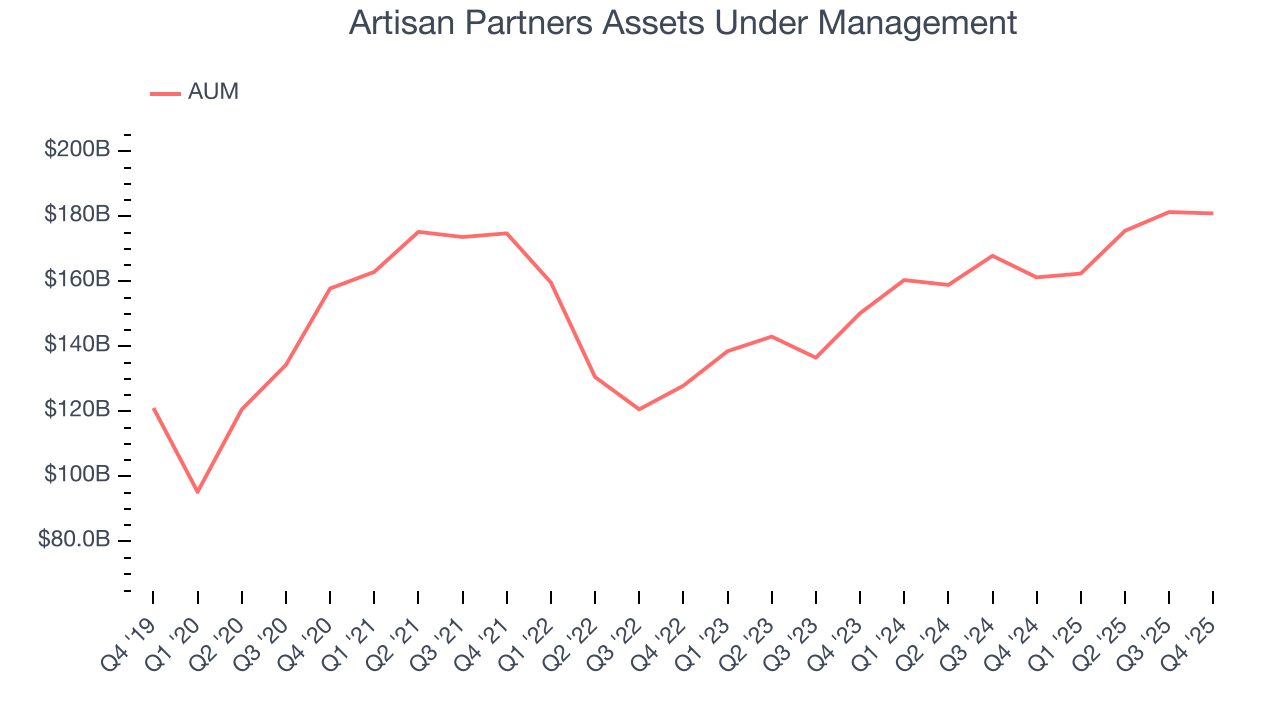

6. Assets Under Management (AUM)

Assets Under Management (AUM) represents the total value of investments that a financial institution manages for its clients. These assets generate steady income through management fees, creating predictable revenue streams that remain stable so long as clients remain invested with the firm.

Artisan Partners’s AUM has grown at an annual rate of 6.6% over the last five years, slightly worse than the broader financials industry but faster than its total revenue. When analyzing Artisan Partners’s AUM over the last two years, we can see that growth accelerated to 11% annually. This performance aligned with its total revenue.

In Q4, Artisan Partners’s AUM was $180.9 billion, falling 1.5% short of analysts’ expectations. This print was 12.2% higher than the same quarter last year.

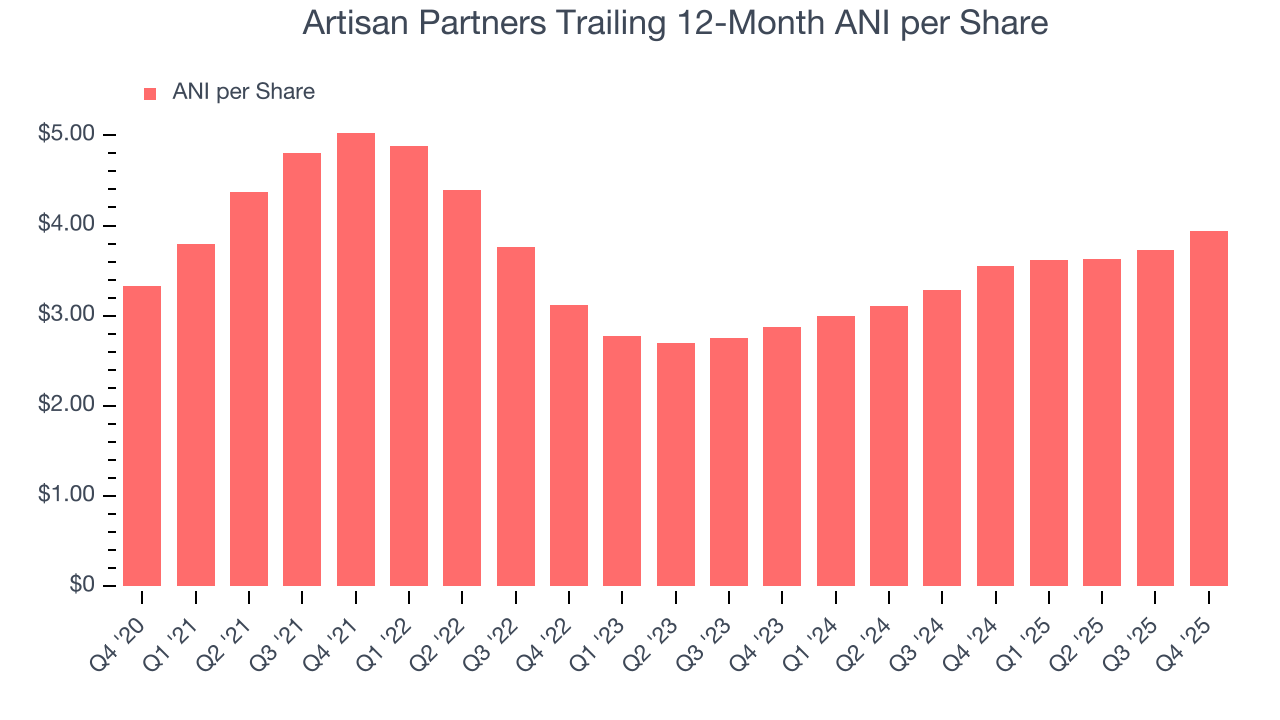

7. Adjusted Net Earnings per Share (ANI per Share)

When analyzing asset managers, we focus on ANI per share, which is essentially the same as the adjusted EPS calculations used throughout the broader market.

By excluding unrealized investment movements and non-recurring costs, ANI per share reveals the underlying profitability of the business. The per-share adjustment is crucial because it shows how earnings translate to individual shareholder ownership after accounting for share count changes.

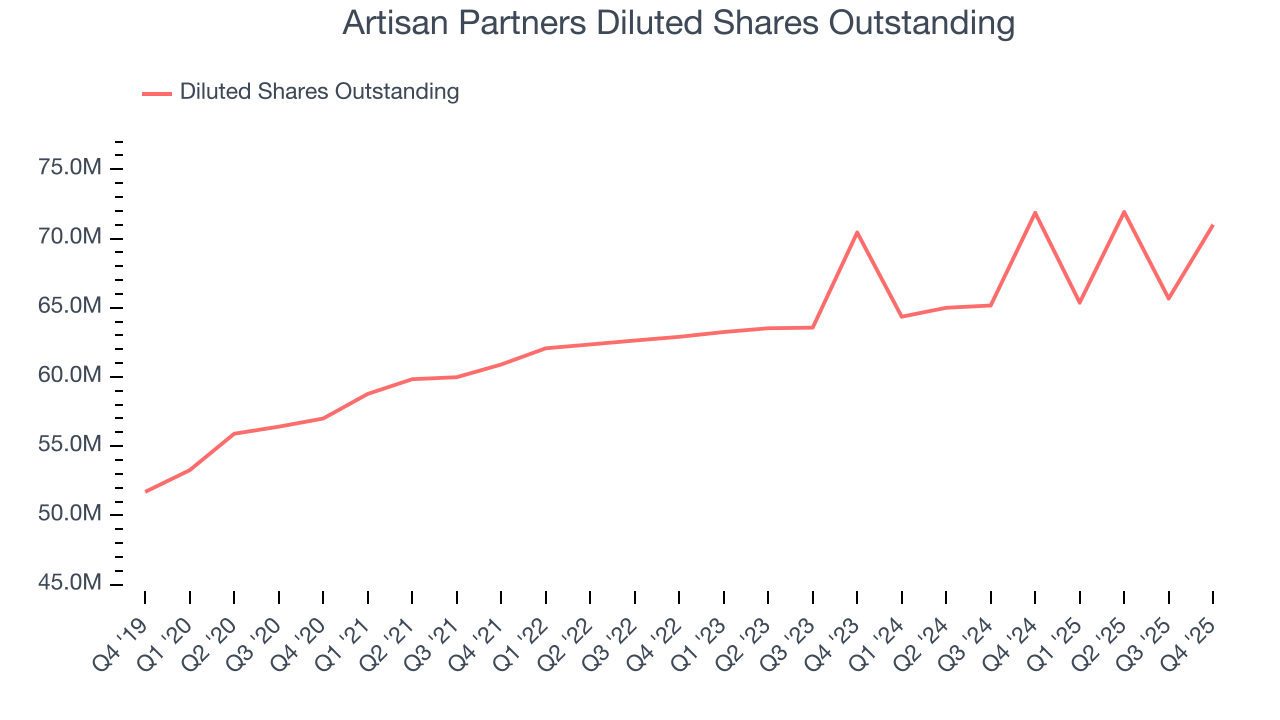

Over the last five years, Artisan Partners’s annual ANI per share growth of 3.4% was weak. It also diluted shareholders across this stretch, a headwind for its results.

On a two-year basis, Artisan Partners’s annualized ANI per share growth accelerated to 17%.

In Q4, Artisan Partners reported ANI per share of $1.26, up from $1.05 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results.

8. A Word on Book Value and ROE

You may wonder when we will analyze book value and return on equity (ROE) since Artisan Partners is a financials company. We pay less attention to these metrics for asset managers because they are not great measures of business quality.

Asset managers are fee-based, capital light firms that manage client capital rather than their own, so they are not balance sheet businesses. Additionally, book value fails to capture the value of brands, investment track records, and other intangibles, thus understating intrinsic value, while ROE can look artificially high due to the relatively smaller bases of equity capital needed to operate the business compared to banks and insurers.

9. Key Takeaways from Artisan Partners’s Q4 Results

It was good to see Artisan Partners beat analysts’ EPS expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its AUM slightly missed. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 3.9% to $46.26 immediately following the results.

10. Is Now The Time To Buy Artisan Partners?

Updated: March 6, 2026 at 11:50 PM EST

Before deciding whether to buy Artisan Partners or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Artisan Partners isn’t a terrible business, but it doesn’t pass our quality test. First off, its revenue growth was uninspiring over the last five years, and analysts don’t see anything changing over the next 12 months. On top of that, Artisan Partners’s weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders, and its AUM growth was mediocre over the last five years.

Artisan Partners’s P/E ratio based on the next 12 months is 9.3x. While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $42 on the company (compared to the current share price of $38.43).