ATI (ATI)

We see potential in ATI. Its rising free cash flow margin gives it more chips to play with.― StockStory Analyst Team

1. News

2. Summary

Why ATI Is Interesting

With its materials flying in nearly every commercial and military aircraft in service today, ATI (NYSE:ATI) produces highly specialized materials and components for aerospace, defense, medical, and energy applications using advanced metallurgy and manufacturing processes.

- Performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 80.9% outpaced its revenue gains

- A drawback is its push for growth has led to negative returns on capital, signaling value destruction

ATI has the potential to be a high-quality business. If you’ve been itching to buy the stock, the valuation seems reasonable.

Why Is Now The Time To Buy ATI?

ATI’s stock price of $121.87 implies a valuation ratio of 33.1x forward P/E. ATI’s valuation multiple is higher than that of many industrials peers, but we think this is appropriate when considering fundamentals.

It could be a good time to invest if you see something the market doesn’t.

3. ATI (ATI) Research Report: Q4 CY2025 Update

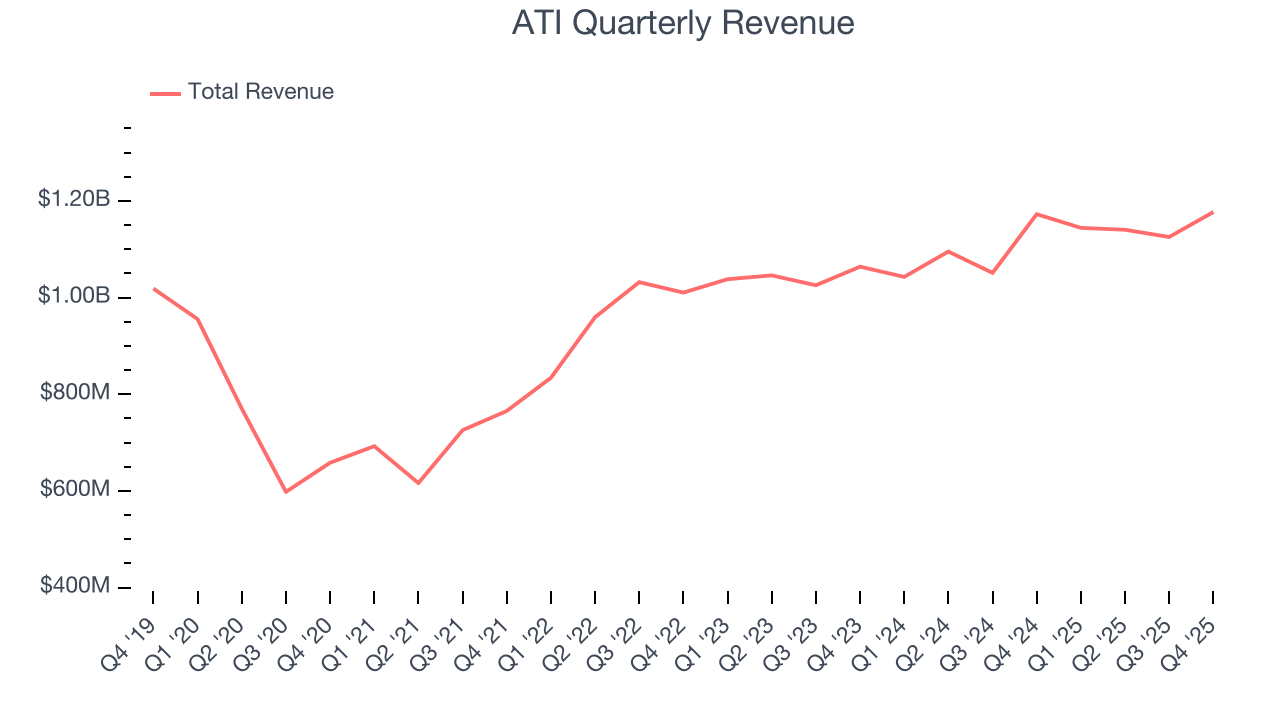

Specialty materials manufacturer ATI (NYSE:ATI) fell short of the markets revenue expectations in Q4 CY2025, with sales flat year on year at $1.18 billion. Its non-GAAP profit of $0.93 per share was 7.5% above analysts’ consensus estimates.

ATI (ATI) Q4 CY2025 Highlights:

- Revenue: $1.18 billion vs analyst estimates of $1.18 billion (flat year on year, 0.5% miss)

- Adjusted EPS: $0.93 vs analyst estimates of $0.87 (7.5% beat)

- Adjusted EBITDA: $231.9 million vs analyst estimates of $228.6 million (19.7% margin, 1.4% beat)

- Operating Margin: 14.5%, down from 17.8% in the same quarter last year

- Free Cash Flow Margin: 19%, down from 28.4% in the same quarter last year

- Market Capitalization: $16.54 billion

Company Overview

With its materials flying in nearly every commercial and military aircraft in service today, ATI (NYSE:ATI) produces highly specialized materials and components for aerospace, defense, medical, and energy applications using advanced metallurgy and manufacturing processes.

ATI's business is divided into two main segments: High Performance Materials & Components (HPMC) and Advanced Alloys & Solutions (AA&S). The HPMC segment, which generates about 86% of its revenue from aerospace and defense markets, creates sophisticated components for jet engines, airframes, and defense applications from nickel-based superalloys, titanium, and other specialty metals. These components must withstand extreme conditions like the high temperatures inside jet engines.

The AA&S segment produces flat products like plate, sheet, and strip materials used across multiple industries. While aerospace and defense account for approximately 60% of this segment's revenue, it also serves energy, medical, and electronics markets.

ATI's materials science expertise enables it to develop alloys with specific properties crucial for demanding applications. For example, its nickel-based superalloys are used in the hottest sections of jet engines where temperatures exceed 2,000°F, while its titanium components provide strength with lighter weight for aircraft structures. In medical applications, ATI's materials are used in MRI machines, replacement joints, and stents. The company maintains long-term agreements with major aerospace manufacturers, including Boeing, Airbus, GE Aerospace, and Rolls-Royce.

To address the critical titanium supply challenges facing the aerospace industry, ATI has been expanding its titanium melting capacity, with plans to increase it by 80% compared to 2022 levels by late 2025. The company is also investing in additive manufacturing (3D printing) capabilities to produce complex components that can't be made through traditional manufacturing methods.

4. Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

ATI's competitors include Berkshire Hathaway-owned Precision Castparts Corporation for specialty alloys and precision forgings, Howmet Aerospace (NYSE:HWM) for titanium alloys, Carpenter Technology Corporation (NYSE:CRS) for specialty alloys, and international competitors like VSMPO-AVISMA for titanium and Aubert & Duval for precision forgings.

5. Revenue Growth

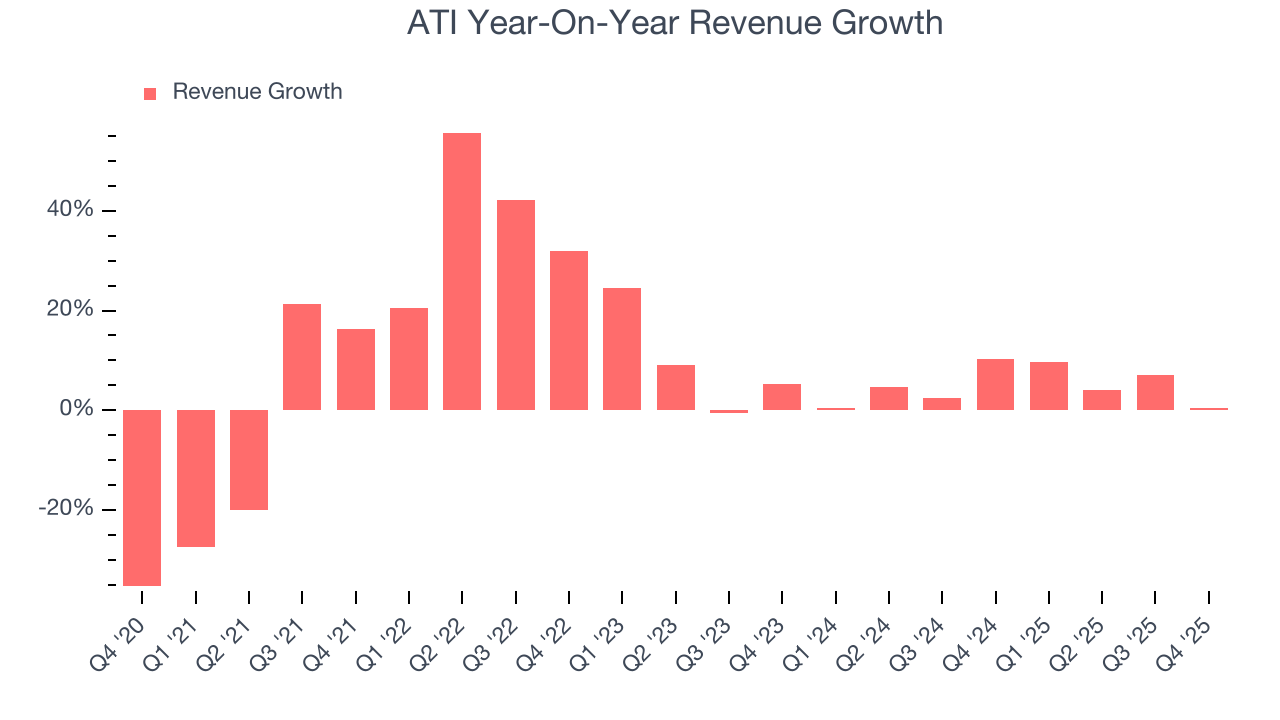

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, ATI grew its sales at a decent 9% compounded annual growth rate. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. ATI’s recent performance shows its demand has slowed as its annualized revenue growth of 4.8% over the last two years was below its five-year trend.

This quarter, ATI’s $1.18 billion of revenue was flat year on year, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8.7% over the next 12 months, an improvement versus the last two years. This projection is above average for the sector and suggests its newer products and services will catalyze better top-line performance.

6. Operating Margin

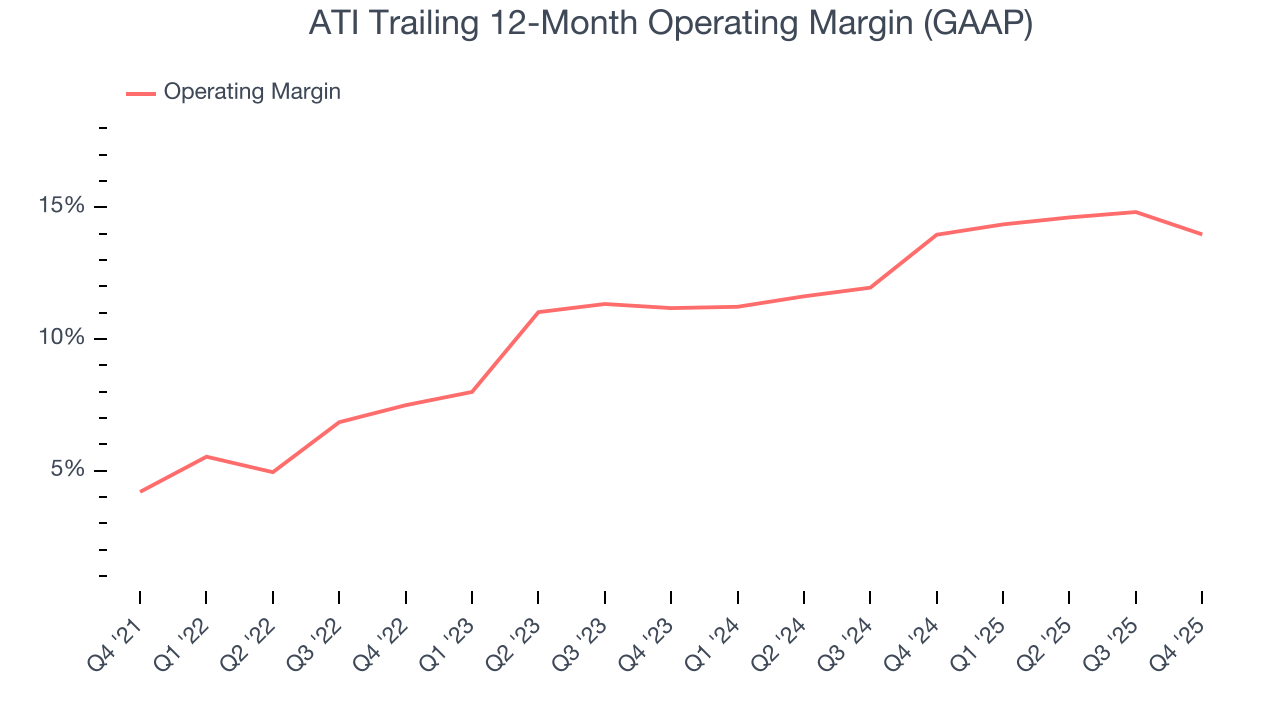

ATI has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 10.7%.

Analyzing the trend in its profitability, ATI’s operating margin rose by 9.8 percentage points over the last five years, as its sales growth gave it immense operating leverage.

In Q4, ATI generated an operating margin profit margin of 14.5%, down 3.3 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

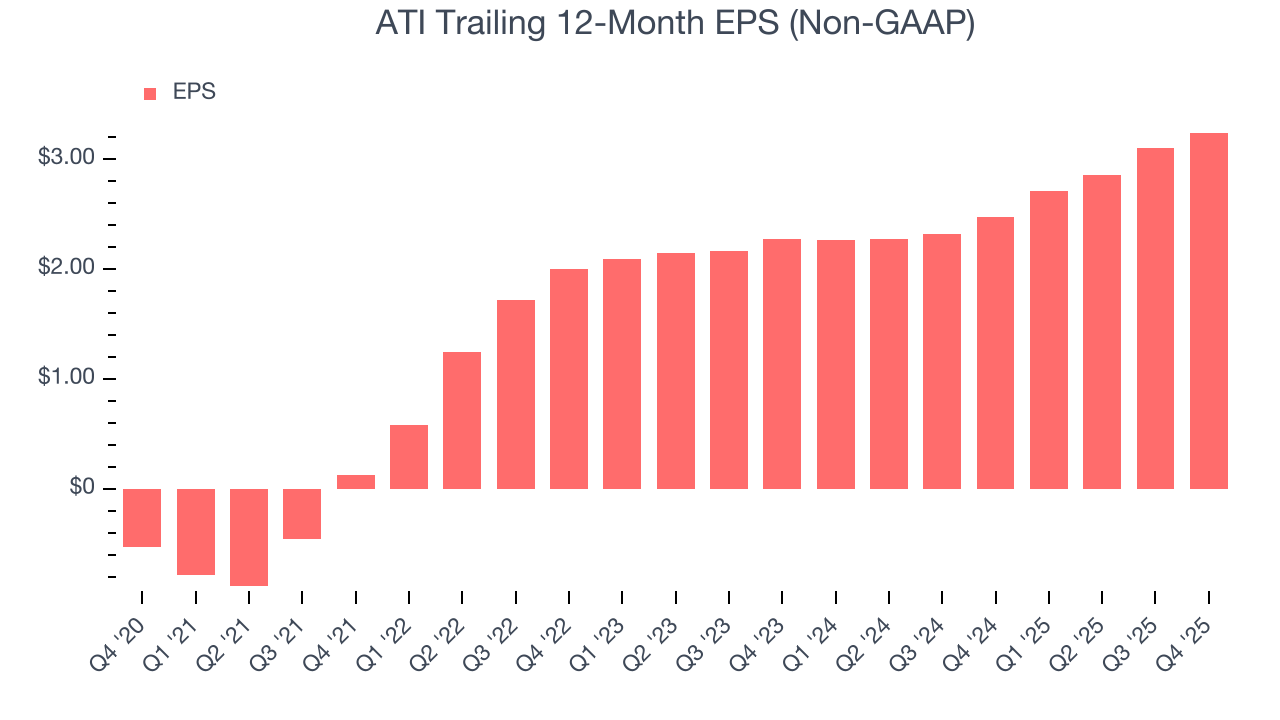

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

ATI’s full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it’s at an inflection point.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

ATI’s EPS grew at an astounding 19.5% compounded annual growth rate over the last two years, higher than its 4.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

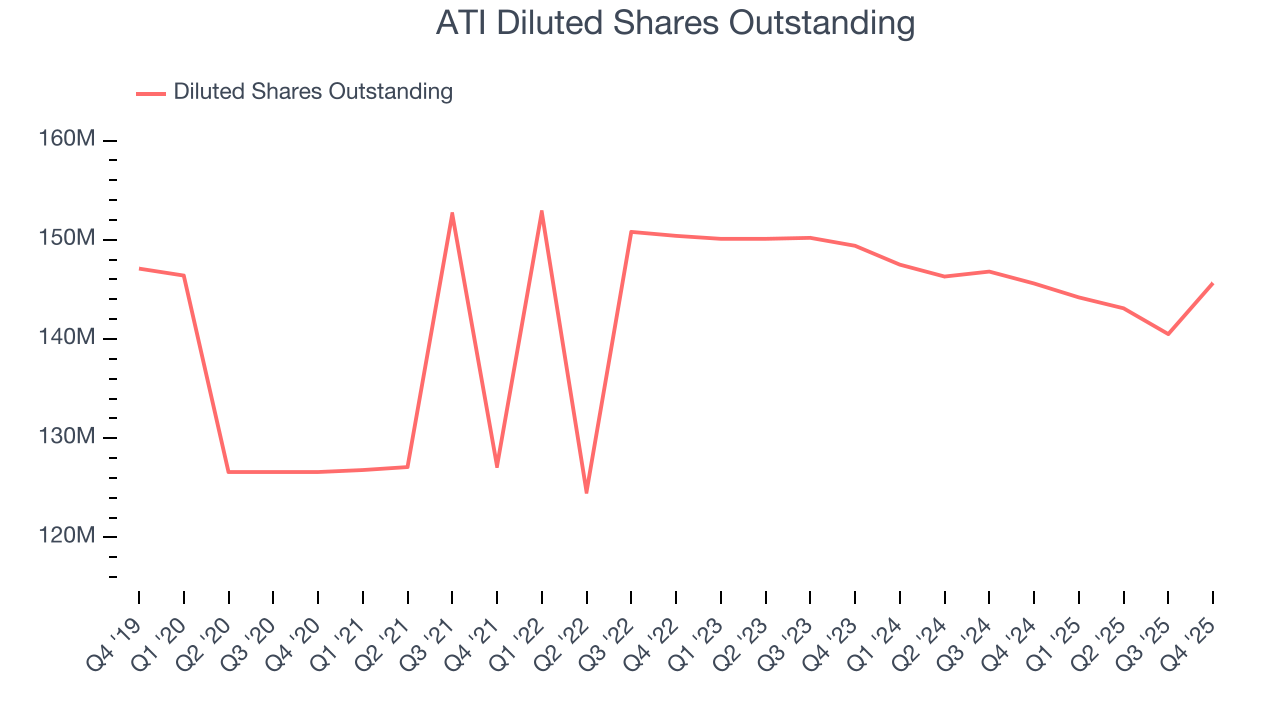

We can take a deeper look into ATI’s earnings to better understand the drivers of its performance. While we mentioned earlier that ATI’s operating margin declined this quarter, a two-year view shows its margin has expandedwhile its share count has shrunk 2.5%. Improving profitability and share buybacks are positive signs for shareholders as they juice EPS growth relative to revenue growth.

In Q4, ATI reported adjusted EPS of $0.93, up from $0.79 in the same quarter last year. This print beat analysts’ estimates by 7.5%. Over the next 12 months, Wall Street expects ATI’s full-year EPS of $3.24 to grow 19.3%.

8. Cash Is King

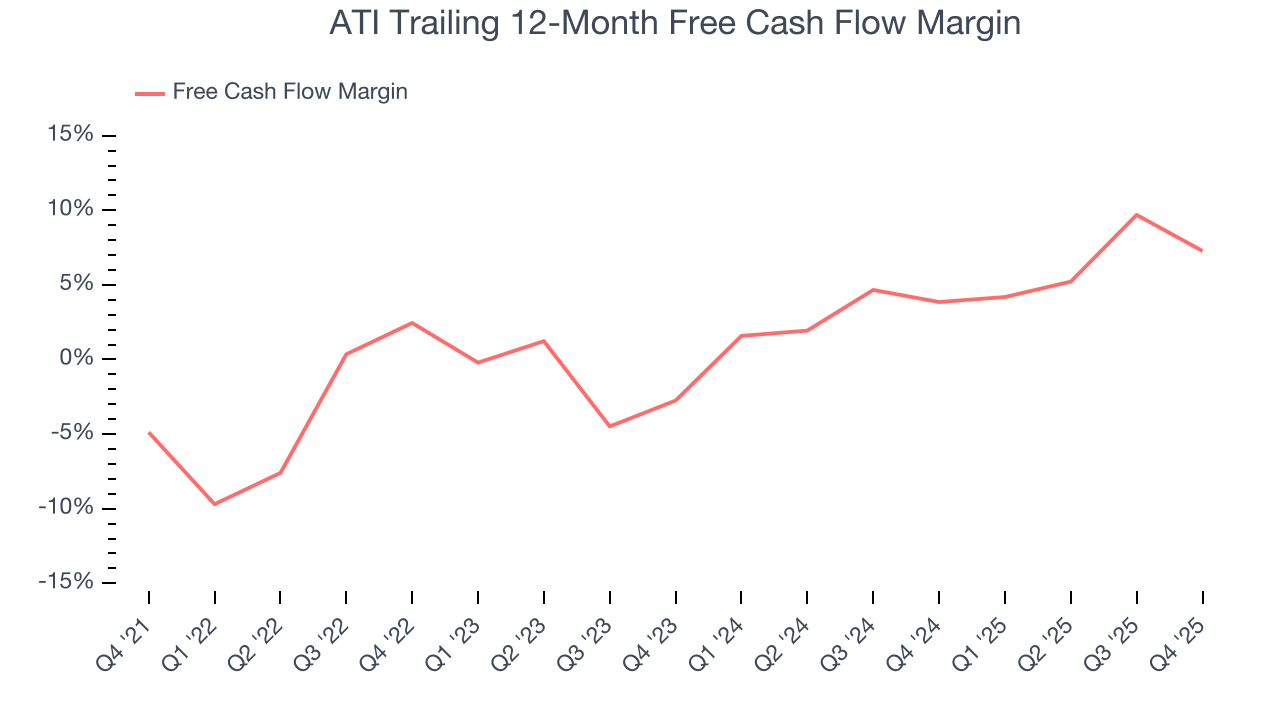

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

ATI has shown poor cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1.7%, lousy for an industrials business. The divergence from its good operating margin stems from its capital-intensive business model, which requires ATI to make large cash investments in working capital and capital expenditures.

Taking a step back, an encouraging sign is that ATI’s margin expanded by 12.1 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

ATI’s free cash flow clocked in at $223.1 million in Q4, equivalent to a 19% margin. The company’s cash profitability regressed as it was 9.5 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends trump temporary fluctuations.

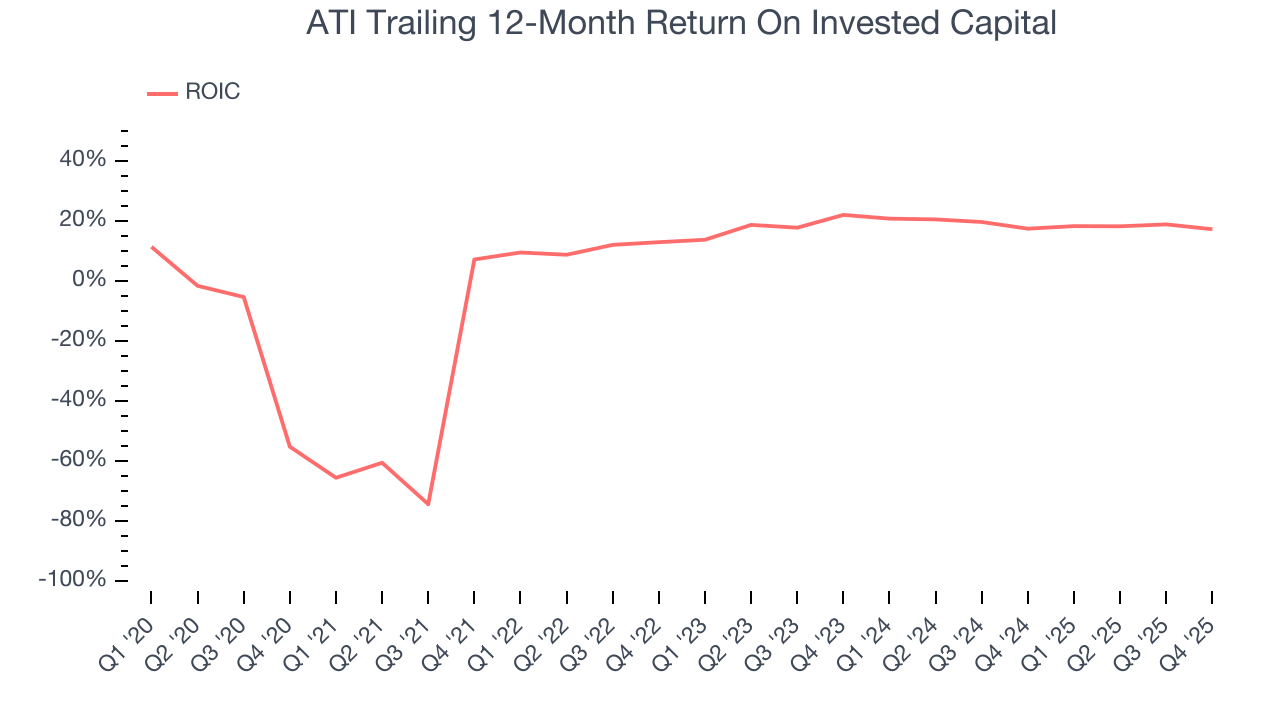

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

ATI’s five-year average ROIC was 15.4%, beating other industrials companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. ATI’s ROIC has increased over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

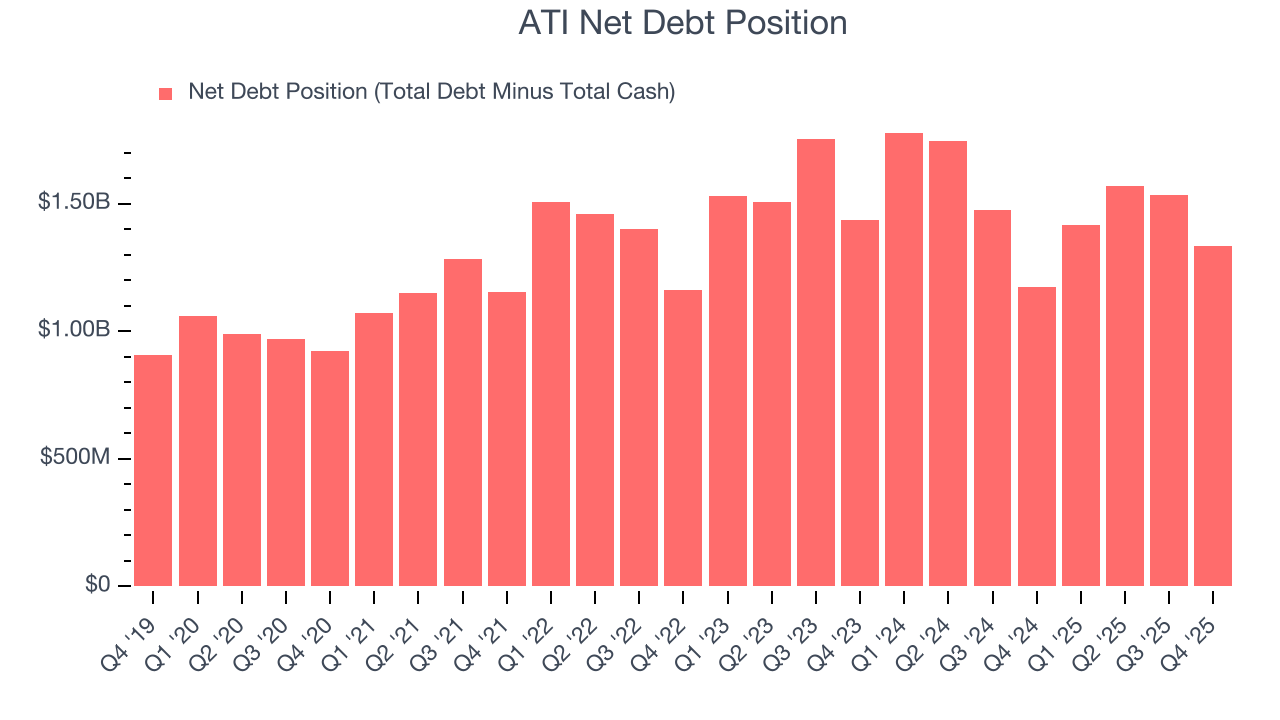

10. Balance Sheet Assessment

ATI reported $416.7 million of cash and $1.75 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $859.3 million of EBITDA over the last 12 months, we view ATI’s 1.6× net-debt-to-EBITDA ratio as safe. We also see its $50.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from ATI’s Q4 Results

It was good to see ATI beat analysts’ EPS expectations this quarter. We were also happy its EBITDA narrowly outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed. Zooming out, we think this was a mixed quarter. The stock traded up 5.1% to $128.02 immediately after reporting.

12. Is Now The Time To Buy ATI?

Updated: February 3, 2026 at 7:52 AM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in ATI.

First, the company’s revenue growth was good over the last five years, and analysts believe it can continue growing at these levels. And while its low free cash flow margins give it little breathing room, its rising cash profitability gives it more optionality. On top of that, ATI’s expanding operating margin shows the business has become more efficient.

ATI’s P/E ratio based on the next 12 months is 31.5x. Looking at the industrials space right now, ATI trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $133 on the company (compared to the current share price of $128.02), implying they see 3.9% upside in buying ATI in the short term.