BWX (BWXT)

We’d invest in BWX. Its revenue and EPS are projected to skyrocket next year, an optimistic sign for its share price.― StockStory Analyst Team

1. News

2. Summary

Why We Like BWX

Contributing components and materials to the famous Manhattan Project in the 1940s, BWX (NYSE:BWXT) is a manufacturer and service provider of nuclear components and fuel for government and commercial industries.

- Market share is on track to rise over the next 12 months as its 17.3% projected revenue growth implies demand will accelerate from its two-year trend

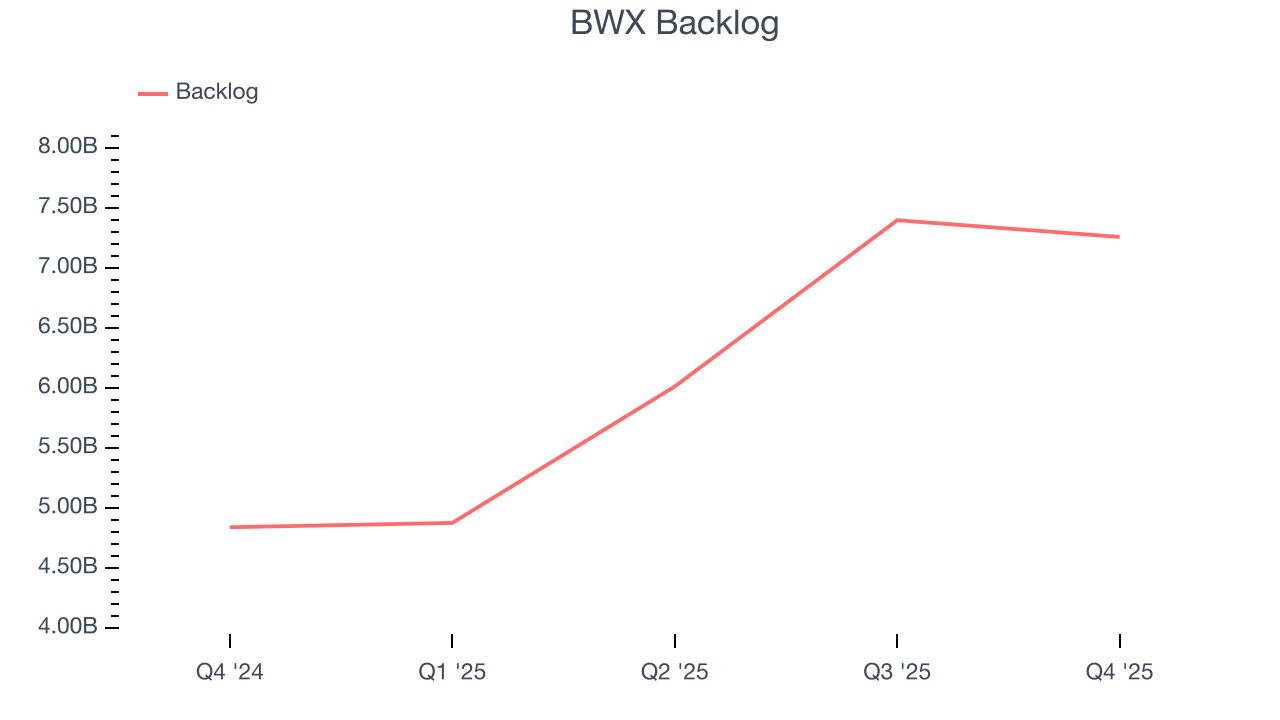

- Demand is greater than supply as the company’s 49.9% average backlog growth over the past two years shows it’s securing new contracts and accumulating more orders than it can fulfill

- Annual revenue growth of 13.2% over the past two years was outstanding, reflecting market share gains this cycle

BWX is a standout company. No coincidence the stock is up 221% over the last five years.

Is Now The Time To Buy BWX?

BWX is trading at $208.15 per share, or 45x forward P/E. There are high expectations given this pricey multiple; we can’t deny that.

Do you admire this business? If so, a small position seems prudent as the long-term outlook seems solid. Keep in mind that BWX’s lofty valuation could result in short-term volatility based on both macro and company-specific factors.

3. BWX (BWXT) Research Report: Q4 CY2025 Update

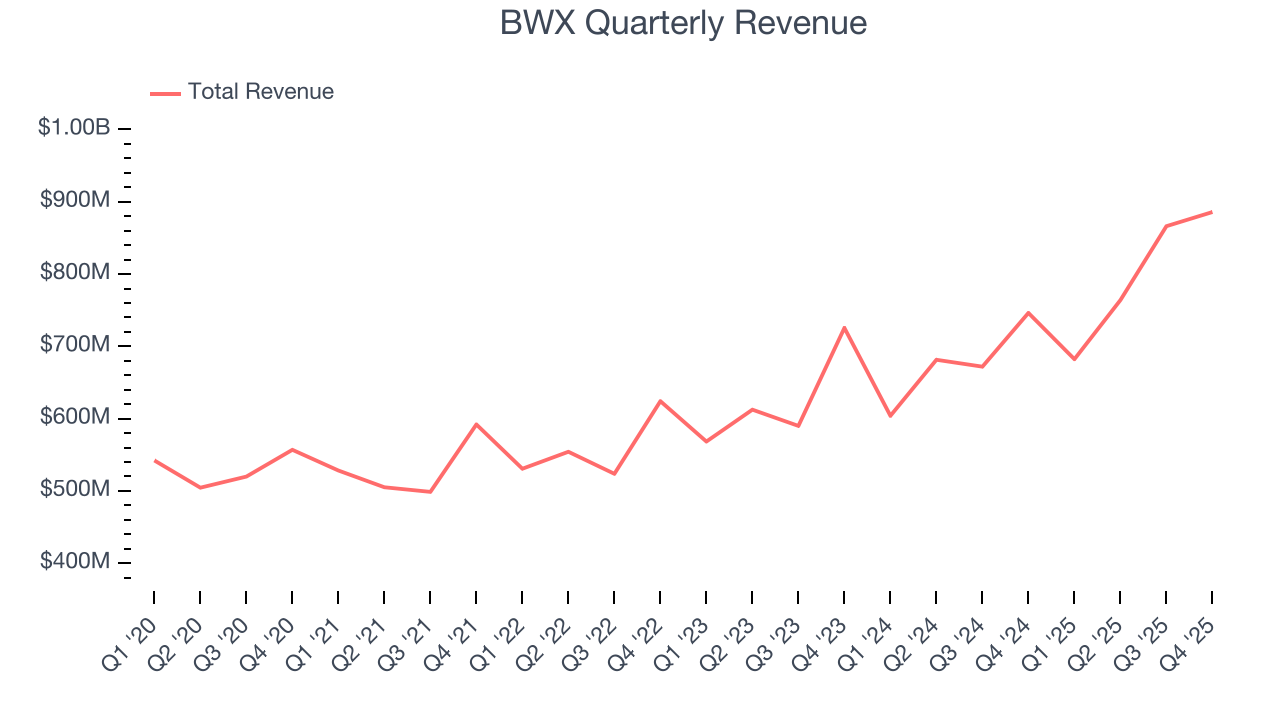

Aerospace and defense company BWX (NYSE:BWXT) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 18.7% year on year to $885.8 million. Its non-GAAP profit of $1.08 per share was 22.2% above analysts’ consensus estimates.

BWX (BWXT) Q4 CY2025 Highlights:

- Revenue: $885.8 million vs analyst estimates of $841 million (18.7% year-on-year growth, 5.3% beat)

- Adjusted EPS: $1.08 vs analyst estimates of $0.88 (22.2% beat)

- Adjusted EBITDA: $147.5 million vs analyst estimates of $145.8 million (16.7% margin, 1.1% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $4.63 at the midpoint, beating analyst estimates by 7.6%

- EBITDA guidance for the upcoming financial year 2026 is $652.5 million at the midpoint, in line with analyst expectations

- Operating Margin: 10.4%, down from 12.4% in the same quarter last year

- Free Cash Flow Margin: 6.4%, down from 30.1% in the same quarter last year

- Backlog: $7.26 billion at quarter end, up 49.9% year on year

- Market Capitalization: $18.87 billion

Company Overview

Contributing components and materials to the famous Manhattan Project in the 1940s, BWX (NYSE:BWXT) is a manufacturer and service provider of nuclear components and fuel for government and commercial industries.

BWX's primary production focus is on precision naval nuclear components, reactors, and nuclear fuel, as well as services like nuclear materials processing and disposal. The company also diversifies its portfolio by producing medical radioisotopes and radiopharmaceuticals.

BWX serves two types of customers: U.S. government agencies and commercial entities. Its government operations cater to the U.S. Department of Energy and Naval Nuclear Propulsion Program, which utilize the company's products and services such as Uranium fuel processing and maintenance of nuclear sites. On the other hand, commercially, BWX primarily sells auxiliary equipment such as reactor components to the nuclear industry, while radiopharmaceutical industries purchase products used in diagnostic imaging and radiotherapeutic treatments.

The company often secures its sales through contracts with government agencies and commercial entities, where contracts with government agencies are mostly long-term and fixed-price incentive fee contracts that provide the reimbursement of allowable costs incurred plus a fee. Contracts with commercial entities vary in scope and are often fixed-price contracts awarded through competitive bidding processes.

4. Defense Contractors

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

BWX’s peers and competitors include Lockheed Martin (NYSE:LMT) and Honeywell (NASDAQ:HON).

5. Revenue Growth

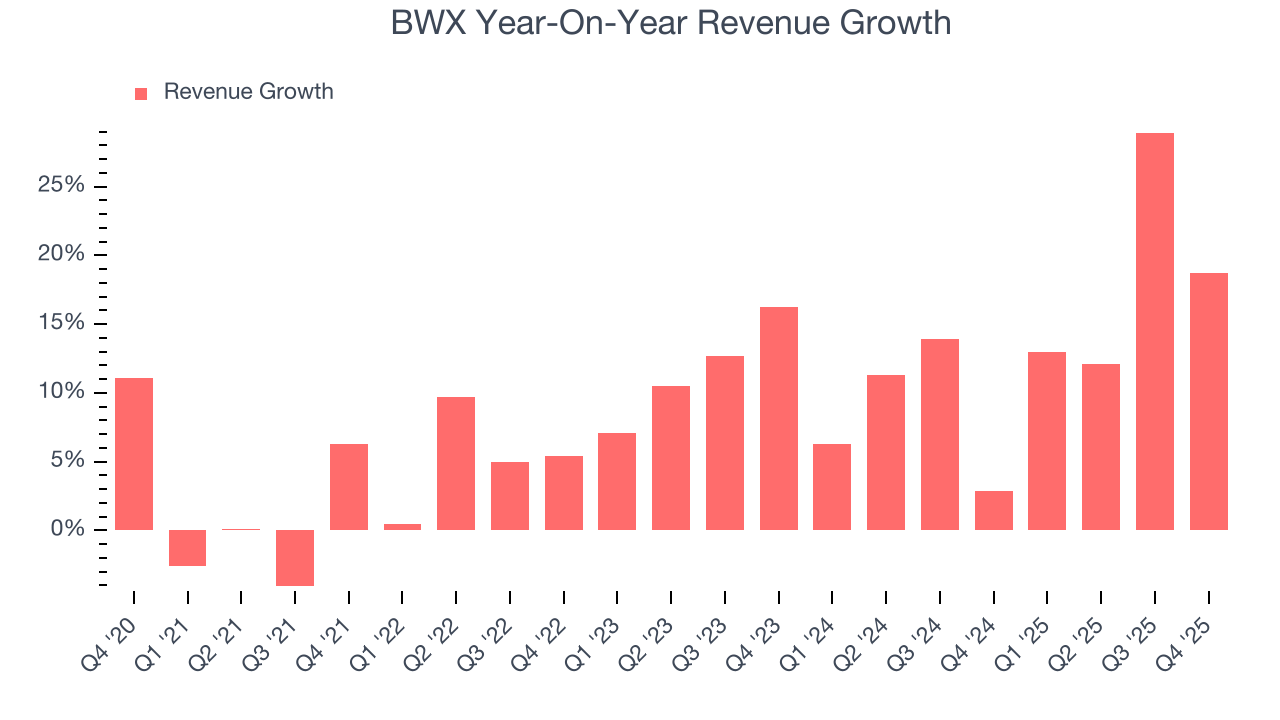

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, BWX’s sales grew at a decent 8.5% compounded annual growth rate over the last five years. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. BWX’s annualized revenue growth of 13.2% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

BWX also reports its backlog, or the value of its outstanding orders that have not yet been executed or delivered. BWX’s backlog reached $7.26 billion in the latest quarter and averaged 49.9% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for BWX’s products and services but raises concerns about capacity constraints.

This quarter, BWX reported year-on-year revenue growth of 18.7%, and its $885.8 million of revenue exceeded Wall Street’s estimates by 5.3%.

Looking ahead, sell-side analysts expect revenue to grow 14.5% over the next 12 months, similar to its two-year rate. This projection is commendable and suggests its newer products and services will catalyze better top-line performance.

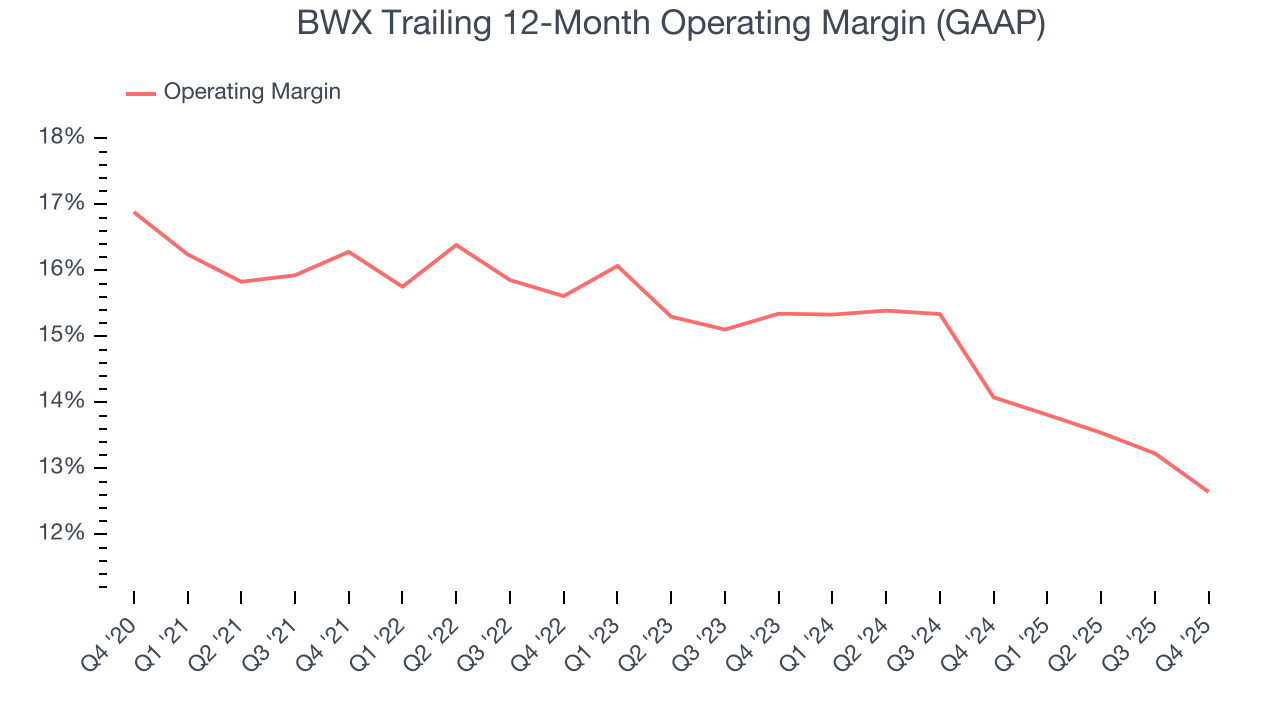

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

BWX has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 14.6%.

Analyzing the trend in its profitability, BWX’s operating margin decreased by 3.6 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

In Q4, BWX generated an operating margin profit margin of 10.4%, down 2 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

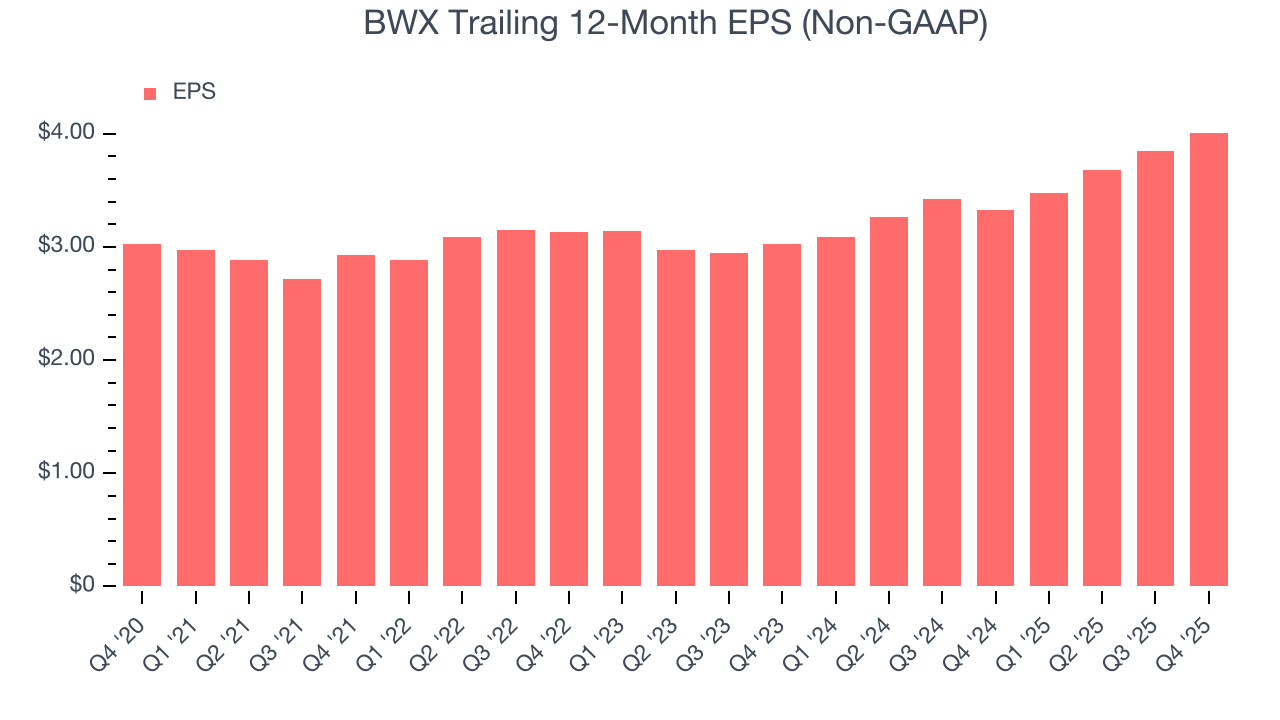

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

BWX’s EPS grew at an unimpressive 5.8% compounded annual growth rate over the last five years, lower than its 8.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to non-fundamental factors such as interest expenses and taxes.

We can take a deeper look into BWX’s earnings to better understand the drivers of its performance. As we mentioned earlier, BWX’s operating margin declined by 3.6 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For BWX, its two-year annual EPS growth of 15% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q4, BWX reported adjusted EPS of $1.08, up from $0.92 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects BWX’s full-year EPS of $4.01 to grow 6.3%.

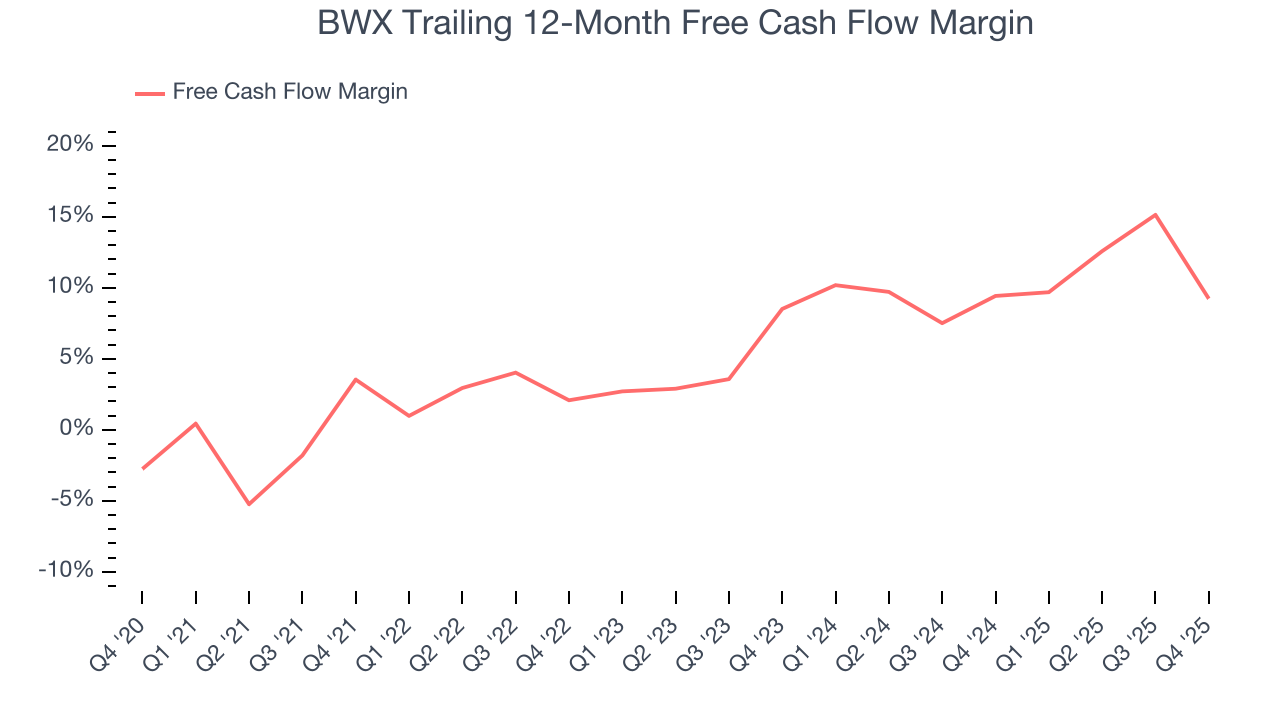

8. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

BWX has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.9% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that BWX’s margin expanded by 5.7 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

BWX’s free cash flow clocked in at $56.8 million in Q4, equivalent to a 6.4% margin. The company’s cash profitability regressed as it was 23.7 percentage points lower than in the same quarter last year, but we wouldn’t put too much weight on it because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing quarter-to-quarter swings. Long-term trends are more important.

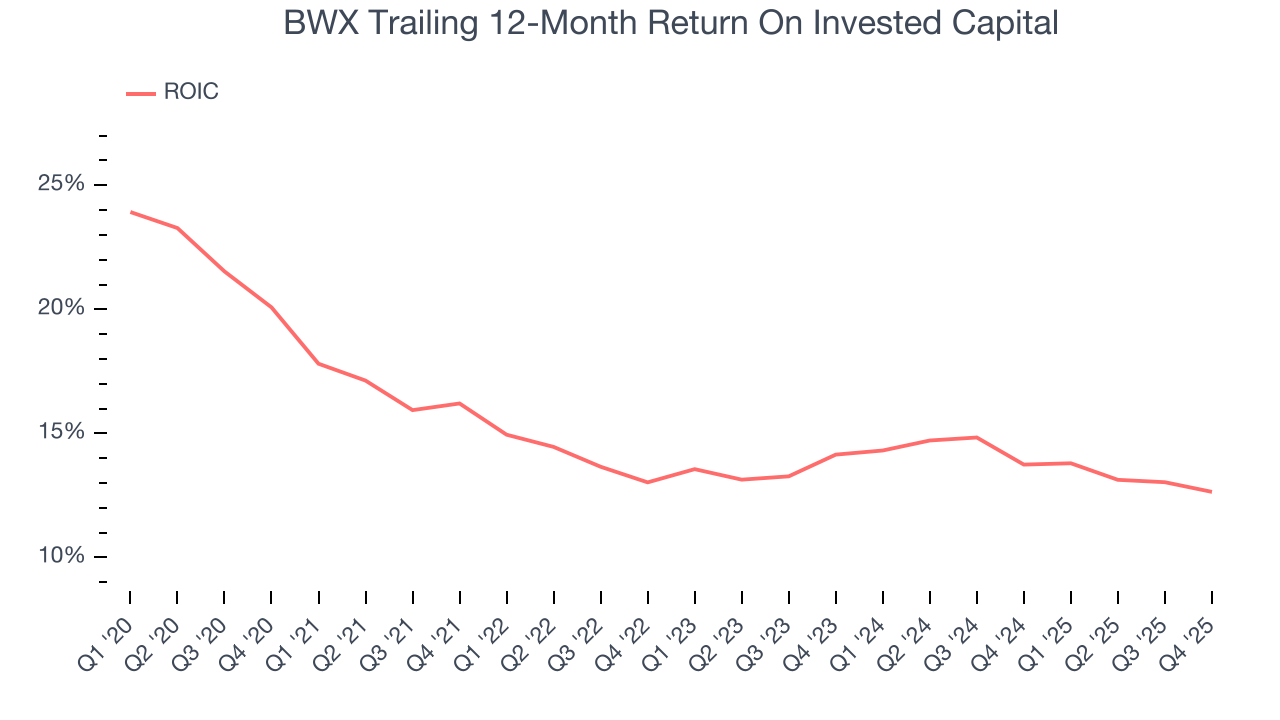

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

BWX’s five-year average ROIC was 14%, higher than most industrials businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, BWX’s ROIC averaged 1.4 percentage point decreases each year over the last few years. Only time will tell if its new bets can bear fruit and potentially reverse the trend.

10. Balance Sheet Assessment

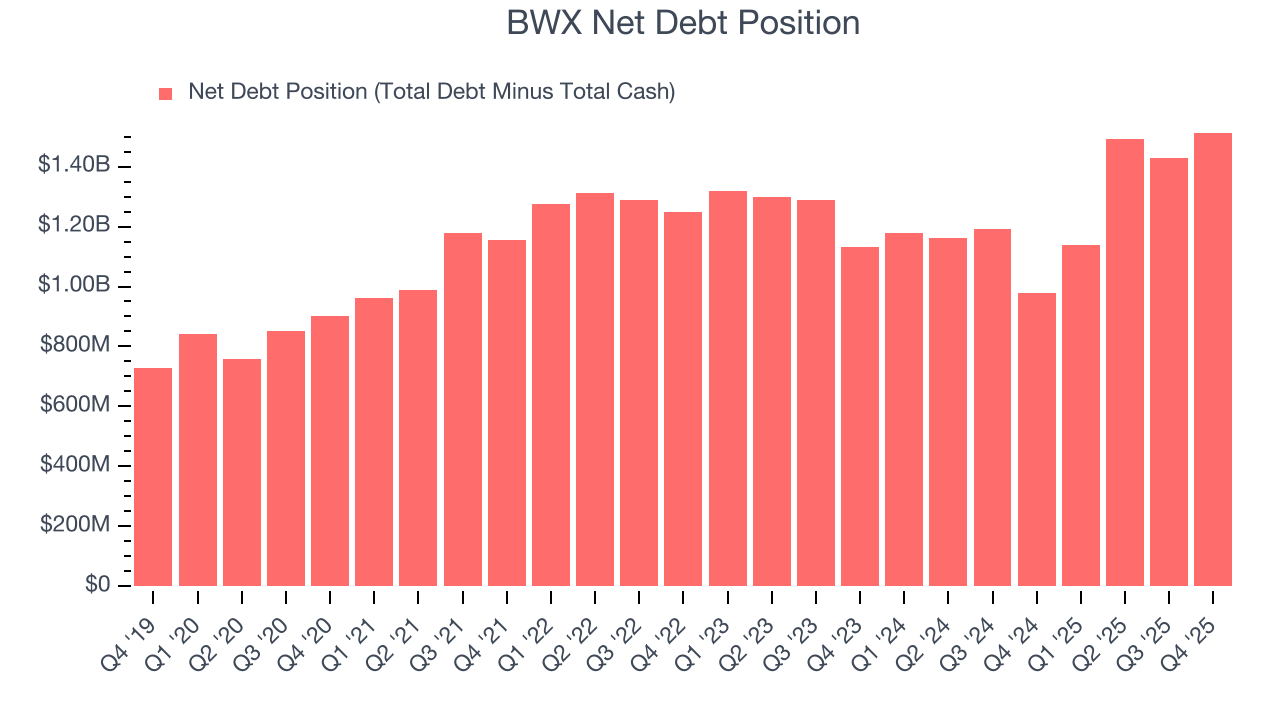

BWX reported $502.9 million of cash and $2.02 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $574.3 million of EBITDA over the last 12 months, we view BWX’s 2.6× net-debt-to-EBITDA ratio as safe. We also see its $22.62 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from BWX’s Q4 Results

We were impressed by how significantly BWX blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 5.2% to $208.89 immediately after reporting.

12. Is Now The Time To Buy BWX?

Updated: March 18, 2026 at 11:36 PM EDT

Before deciding whether to buy BWX or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

BWX is a high-quality business worth owning. For starters, its revenue growth was good over the last five years and is expected to accelerate over the next 12 months. And while its declining operating margin shows the business has become less efficient, its backlog growth has been marvelous. On top of that, BWX’s rising cash profitability gives it more optionality.

BWX’s P/E ratio based on the next 12 months is 45x. A lot of good news is certainly baked in given its premium multiple, but we’ll happily own BWX as its fundamentals really stand out. Investments like this should be held patiently for at least three to five years as they benefit from the power of long-term compounding, which more than makes up for any short-term price volatility that comes with high valuations.

Wall Street analysts have a consensus one-year price target of $232 on the company (compared to the current share price of $208.15).