Cadence Bank (CADE)

Cadence Bank doesn’t excite us. Its underwhelming returns on capital show it struggled to generate meaningful profits for shareholders.― StockStory Analyst Team

1. News

2. Summary

Why Cadence Bank Is Not Exciting

With roots dating back to 1885 and a strategic focus on middle-market commercial lending, Cadence Bancorporation (NYSE:CADE) is a bank holding company that provides commercial banking, retail banking, and wealth management services to middle-market businesses and individuals.

- Incremental sales over the last five years were less profitable as its 6.2% annual earnings per share growth lagged its revenue gains

- ROE of 8.9% reflects management’s challenges in identifying attractive investment opportunities

- On the bright side, its annual net interest income growth of 18.2% over the past five years was outstanding, reflecting market share gains this cycle

Cadence Bank’s quality is inadequate. We believe there are better opportunities elsewhere.

Why There Are Better Opportunities Than Cadence Bank

Cadence Bank is trading at $42.89 per share, or 1.3x forward P/B. The current valuation may be appropriate, but we’re still not buyers of the stock.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Cadence Bank (CADE) Research Report: Q4 CY2025 Update

Regional banking company Cadence Bank (NYSE:CADE) announced better-than-expected revenue in Q4 CY2025, with sales up 17.1% year on year to $528.4 million. Its non-GAAP profit of $0.85 per share was 6.4% above analysts’ consensus estimates.

Cadence Bank (CADE) Q4 CY2025 Highlights:

- Net Interest Income: $426.9 million vs analyst estimates of $429.3 million (17.1% year-on-year growth, 0.5% miss)

- Net Interest Margin: 3.6% vs analyst estimates of 3.5% (5.7 basis point beat)

- Revenue: $528.4 million vs analyst estimates of $524.7 million (17.1% year-on-year growth, 0.7% beat)

- Efficiency Ratio: 58.8% vs analyst estimates of 56.5% (235.3 basis point miss)

- Adjusted EPS: $0.85 vs analyst estimates of $0.80 (6.4% beat)

- Tangible Book Value per Share: $23.69 vs analyst estimates of $23.40 (10% year-on-year growth, 1.2% beat)

- Market Capitalization: $8.66 billion

Company Overview

With roots dating back to 1885 and a strategic focus on middle-market commercial lending, Cadence Bancorporation (NYSE:CADE) is a bank holding company that provides commercial banking, retail banking, and wealth management services to middle-market businesses and individuals.

Cadence operates primarily in Texas and the southeastern United States through a network of branches, ATMs, and digital banking platforms. The bank's commercial banking division targets businesses with annual revenues between $10 million and $500 million, offering customized lending solutions including lines of credit, acquisition financing, and commercial real estate loans.

For individual customers, Cadence provides traditional banking products such as checking and savings accounts, residential mortgages, and consumer loans. The bank enhances its revenue streams through several specialized services, including correspondent banking for other financial institutions, payroll processing through its Altera subsidiary, and merchant services.

Wealth management represents a significant component of Cadence's non-interest income. Through its Linscomb & Williams and Cadence Trust brands, the bank offers financial planning, retirement services, and investment management targeting affluent clients with investable assets ranging from $500,000 to $5 million. A business owner might utilize Cadence's commercial lending for expansion capital while simultaneously engaging their wealth management team for succession planning and personal investment management.

Cadence's business model balances interest income from its loan portfolio with fee-based revenue from treasury management, wealth services, and insurance products. The bank competes by leveraging relationship banking—assigning dedicated bankers who understand clients' industries and can coordinate comprehensive financial solutions across the bank's various divisions.

4. Regional Banks

Regional banks, financial institutions operating within specific geographic areas, serve as intermediaries between local depositors and borrowers. They benefit from rising interest rates that improve net interest margins (the difference between loan yields and deposit costs), digital transformation reducing operational expenses, and local economic growth driving loan demand. However, these banks face headwinds from fintech competition, deposit outflows to higher-yielding alternatives, credit deterioration (increasing loan defaults) during economic slowdowns, and regulatory compliance costs. Recent concerns about regional bank stability following high-profile failures and significant commercial real estate exposure present additional challenges.

Cadence Bank competes with regional banks like Regions Financial (NYSE:RF), Truist Financial (NYSE:TFC), and Hancock Whitney (NASDAQ:HWC), as well as larger national institutions including JPMorgan Chase (NYSE:JPM) and Bank of America (NYSE:BAC) in its southeastern and Texas markets.

5. Sales Growth

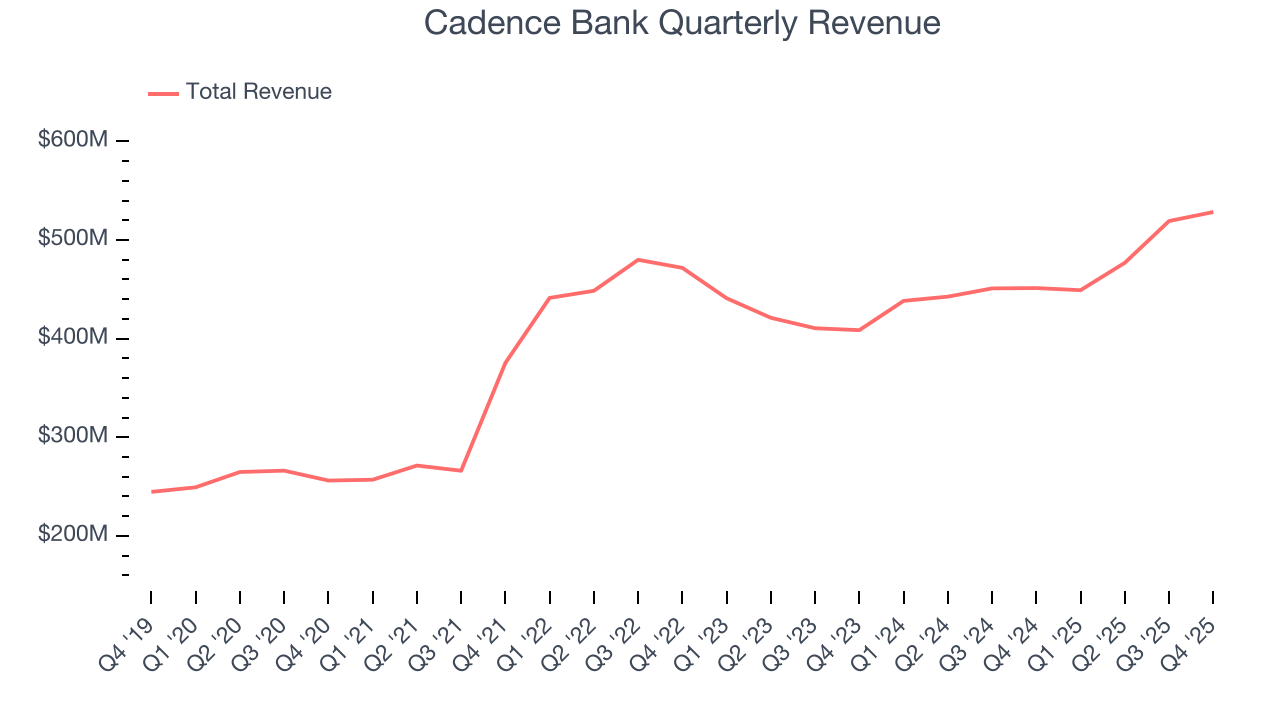

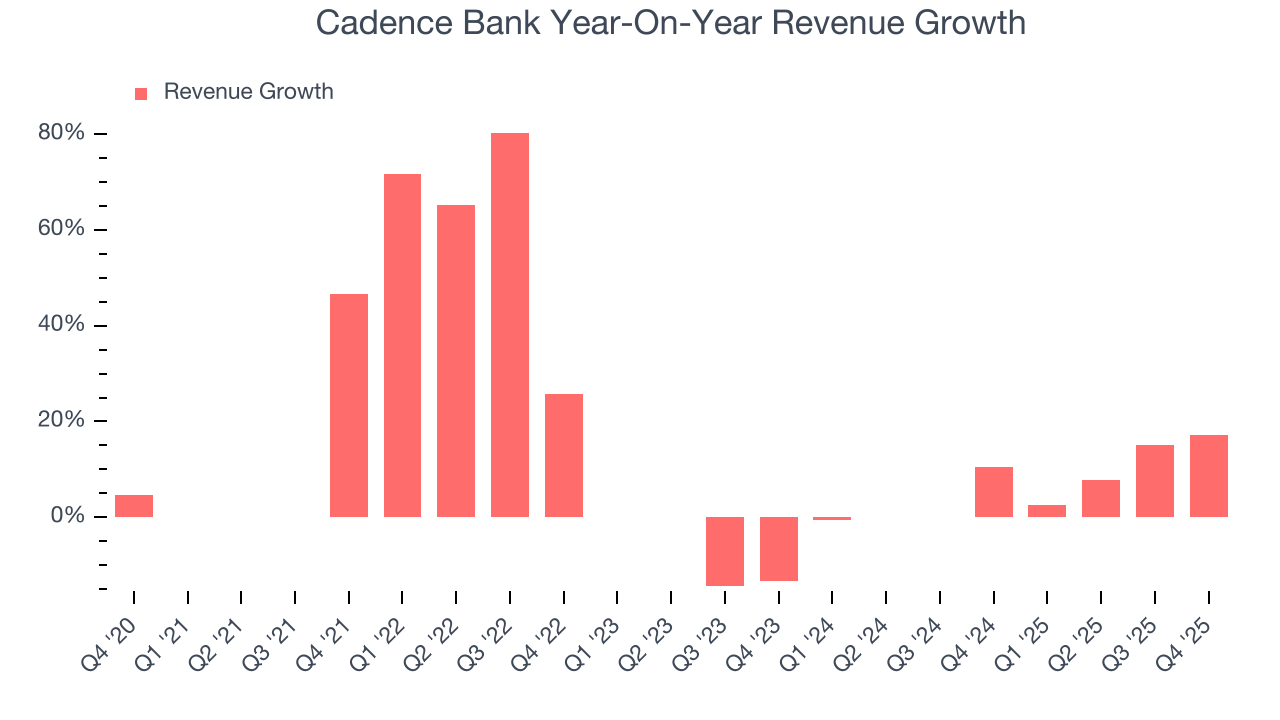

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees. Luckily, Cadence Bank’s revenue grew at a solid 13.7% compounded annual growth rate over the last five years. Its growth beat the average banking company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Cadence Bank’s recent performance shows its demand has slowed as its annualized revenue growth of 8.3% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Cadence Bank reported year-on-year revenue growth of 17.1%, and its $528.4 million of revenue exceeded Wall Street’s estimates by 0.7%.

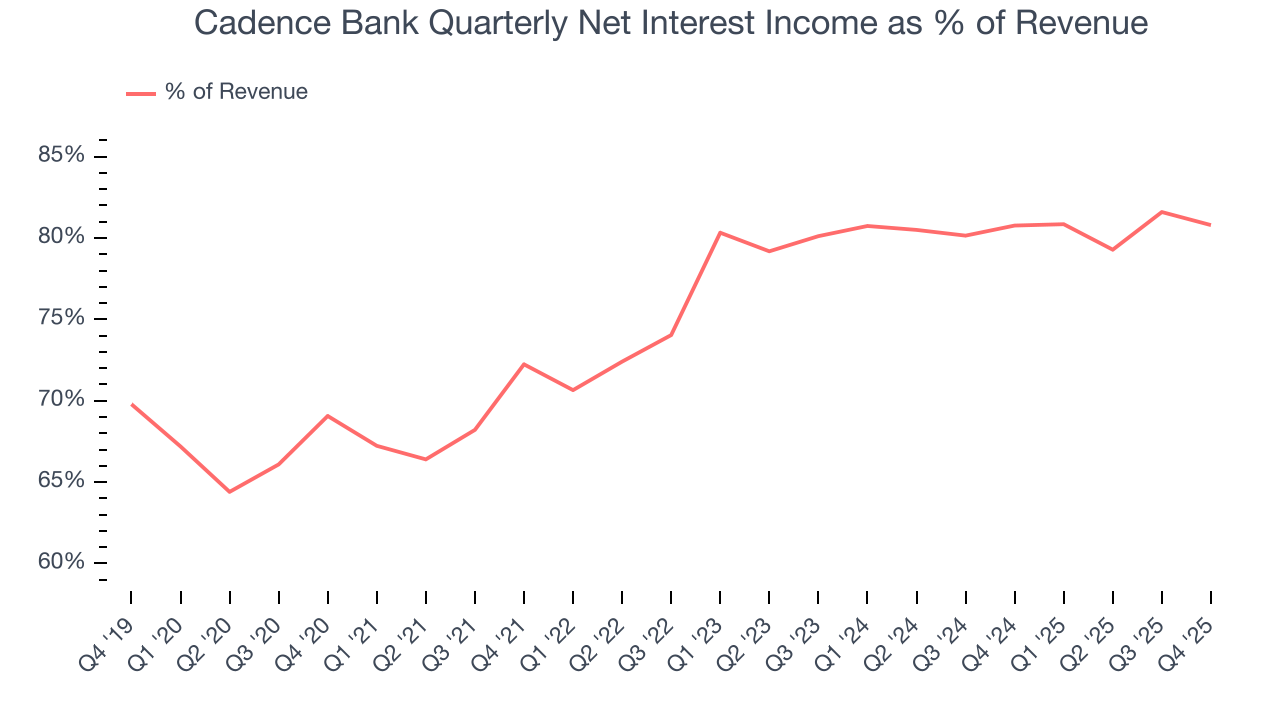

Net interest income made up 76.4% of the company’s total revenue during the last five years, meaning lending operations are Cadence Bank’s largest source of revenue.

Our experience and research show the market cares primarily about a bank’s net interest income growth as non-interest income is considered a lower-quality and non-recurring revenue source.

6. Earnings Per Share

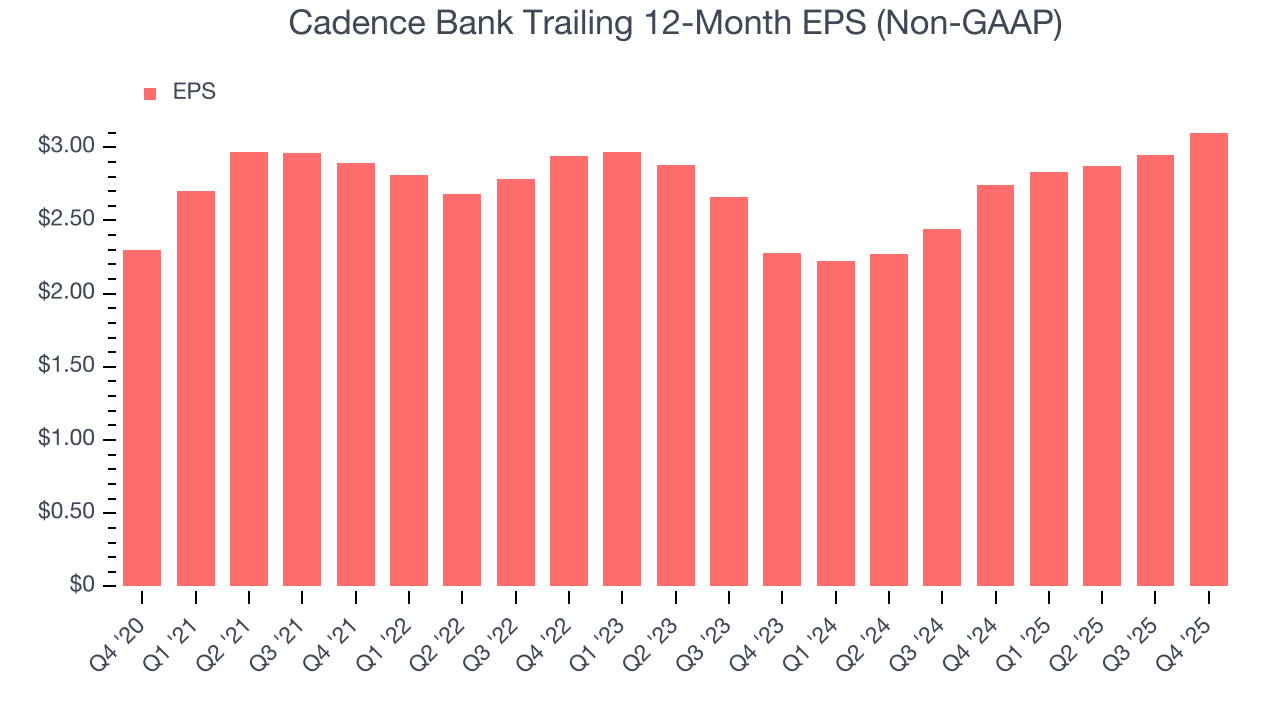

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Cadence Bank’s EPS grew at a weak 6.2% compounded annual growth rate over the last five years, lower than its 13.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Cadence Bank, its two-year annual EPS growth of 16.6% was higher than its five-year trend. This acceleration made it one of the faster-growing banking companies in recent history.

In Q4, Cadence Bank reported adjusted EPS of $0.85, up from $0.70 in the same quarter last year. This print beat analysts’ estimates by 6.4%. Over the next 12 months, Wall Street expects Cadence Bank’s full-year EPS of $3.10 to grow 11.3%.

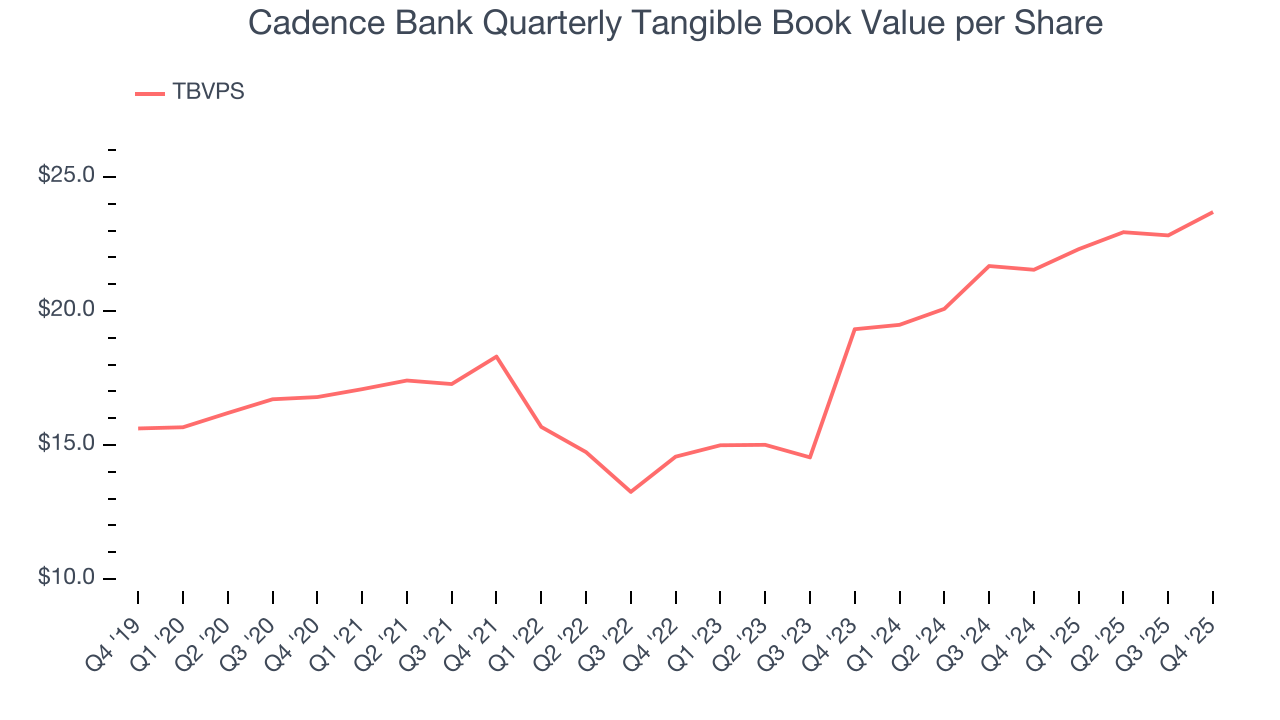

7. Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

Because of this, tangible book value per share (TBVPS) emerges as the critical performance benchmark. By excluding intangible assets with uncertain liquidation values, this metric captures real, liquid net worth per share. On the other hand, EPS is often distorted by mergers and flexible loan loss accounting. TBVPS provides clearer performance insights.

Cadence Bank’s TBVPS grew at an impressive 7.1% annual clip over the last five years. TBVPS growth has also accelerated recently, growing by 10.7% annually over the last two years from $19.32 to $23.69 per share.

Over the next 12 months, Consensus estimates call for Cadence Bank’s TBVPS to grow by 9.1% to $25.86, paltry growth rate.

8. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, Cadence Bank has averaged a Tier 1 capital ratio of 12%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

9. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Cadence Bank has averaged an ROE of 8.9%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

10. Key Takeaways from Cadence Bank’s Q4 Results

It was good to see Cadence Bank narrowly top analysts’ tangible book value per share expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its net interest income slightly missed and efficiency ratio also fell short of expectations. Zooming out, we think this was a mixed quarter. The market seemed to be hoping for more, and the stock traded down 3.9% to $44.63 immediately after reporting.

11. Is Now The Time To Buy Cadence Bank?

Updated: January 23, 2026 at 11:12 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Cadence Bank.

Cadence Bank has some positive attributes, but it isn’t one of our picks. First off, its revenue growth was solid over the last five years. And while Cadence Bank’s weak EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders, its expanding net interest margin shows its loan book is becoming more profitable.

Cadence Bank’s P/B ratio based on the next 12 months is 1.3x. This valuation multiple is fair, but we don’t have much faith in the company. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $43 on the company (compared to the current share price of $42.89).