Chewy (CHWY)

We’re skeptical of Chewy. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why We Think Chewy Will Underperform

Founded by Ryan Cohen, who later became known for his involvement in GameStop, Chewy (NYSE:CHWY) is an online retailer specializing in pet food, supplies, and healthcare services.

- Gross margin of 29.4% reflects its high servicing costs

- Estimated sales growth of 6.1% for the next 12 months implies demand will slow from its three-year trend

- A consolation is that its incremental sales significantly boosted profitability as its annual earnings per share growth of 212% over the last three years outstripped its revenue performance

Chewy doesn’t satisfy our quality benchmarks. There are more promising prospects in the market.

Why There Are Better Opportunities Than Chewy

Chewy’s stock price of $25.44 implies a valuation ratio of 12.3x forward EV/EBITDA. This multiple is quite expensive for the quality you get.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Chewy (CHWY) Research Report: Q3 CY2025 Update

E-commerce pet food and supplies retailer Chewy (NYSE:CHWY) reported revenue ahead of Wall Streets expectations in Q3 CY2025, with sales up 8.3% year on year to $3.12 billion. Its non-GAAP profit of $0.32 per share was 5.4% above analysts’ consensus estimates.

Chewy (CHWY) Q3 CY2025 Highlights:

- Revenue: $3.12 billion vs analyst estimates of $3.1 billion (8.3% year-on-year growth, 0.5% beat)

- Adjusted EPS: $0.32 vs analyst estimates of $0.30 (5.4% beat)

- Adjusted EBITDA: $180.9 million vs analyst estimates of $170 million (5.8% margin, 6.4% beat)

- Operating Margin: 2.1%, up from 0.9% in the same quarter last year

- Free Cash Flow Margin: 5.6%, up from 3.4% in the previous quarter

- Market Capitalization: $14.45 billion

Company Overview

Founded by Ryan Cohen, who later became known for his involvement in GameStop, Chewy (NYSE:CHWY) is an online retailer specializing in pet food, supplies, and healthcare services.

Chewy emerged in 2011 from a simple idea: to make pet shopping easier and more convenient. The founders recognized the need for an online platform dedicated to pet care, where pet owners could find everything from food to accessories under one virtual roof. Chewy was created to provide a one-stop-shop experience, simplifying the process of buying pet supplies and offering a wider variety than traditional brick-and-mortar stores.

Chewy offers an extensive range of pet products, including food, toys, pharmaceuticals, and grooming items. Its unique selling proposition lies in its vast product assortment, competitive pricing, and customer service. The company also provides prescription services and pet healthcare advice, catering to the complete needs of pet owners. Chewy's user-friendly website and mobile app enhance the shopping experience, making pet care accessible with just a few clicks.

The company generates revenue through the sale of pet products and services online. Chewy’s subscription-based model, Chewy Autoship, ensures a steady revenue stream by providing regular deliveries of pet essentials. This model appeals to busy pet owners looking for convenience and reliability.

4. Online Retail

Consumers ever rising demand for convenience, selection, and speed are secular engines underpinning ecommerce adoption. For years prior to Covid, ecommerce penetration as a percentage of overall retail would grow 1-2% annually, but in 2020 adoption accelerated by 5%, reaching 25%, as increased emphasis on convenience drove consumers to structurally buy more online. The surge in buying caused many online retailers to rapidly grow their logistics infrastructures, preparing them for further growth in the years ahead as consumer shopping habits continue to shift online.

Chewy competes with Amazon (NASDAQ:AMZN), Petco (NASDAQ:WOOF), BARK (NYSE:BARK), PetMed Express (NASDAQ:PETS), Walmart (NYSE:WMT), and Costco (NYSE:COST).

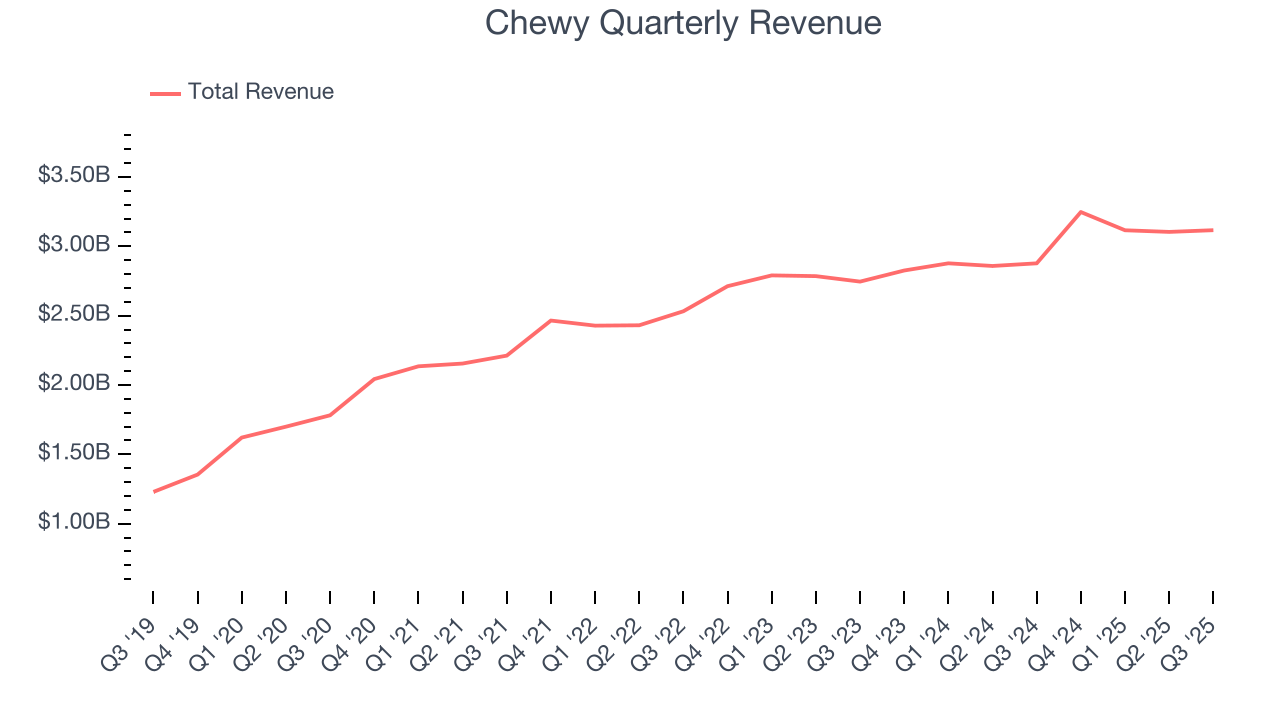

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Chewy’s sales grew at a mediocre 8.5% compounded annual growth rate over the last three years. This fell short of our benchmark for the consumer internet sector and is a poor baseline for our analysis.

This quarter, Chewy reported year-on-year revenue growth of 8.3%, and its $3.12 billion of revenue exceeded Wall Street’s estimates by 0.5%.

Looking ahead, sell-side analysts expect revenue to grow 5.9% over the next 12 months, a slight deceleration versus the last three years. This projection is underwhelming and indicates its products and services will face some demand challenges.

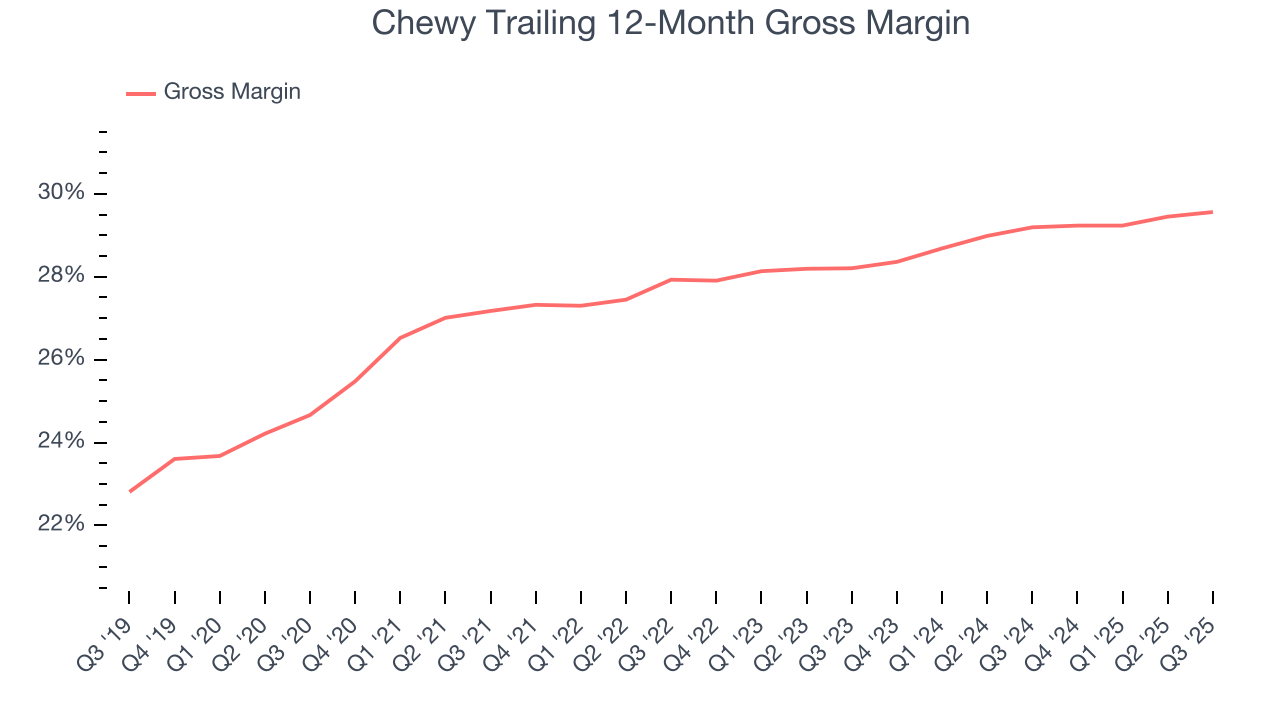

6. Gross Margin & Pricing Power

For online retail (separate from online marketplaces) businesses like Chewy, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include the cost of acquiring the products sold, shipping and fulfillment, customer service, and digital infrastructure.

Chewy’s unit economics are far below other consumer internet companies because it must carry inventories as an online retailer. This means it has relatively higher capital intensity than a pure software business like Meta or Airbnb and signals it operates in a competitive market. As you can see below, it averaged a 29.4% gross margin over the last two years. Said differently, Chewy had to pay a chunky $70.61 to its service providers for every $100 in revenue.

Chewy’s gross profit margin came in at 29.8% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

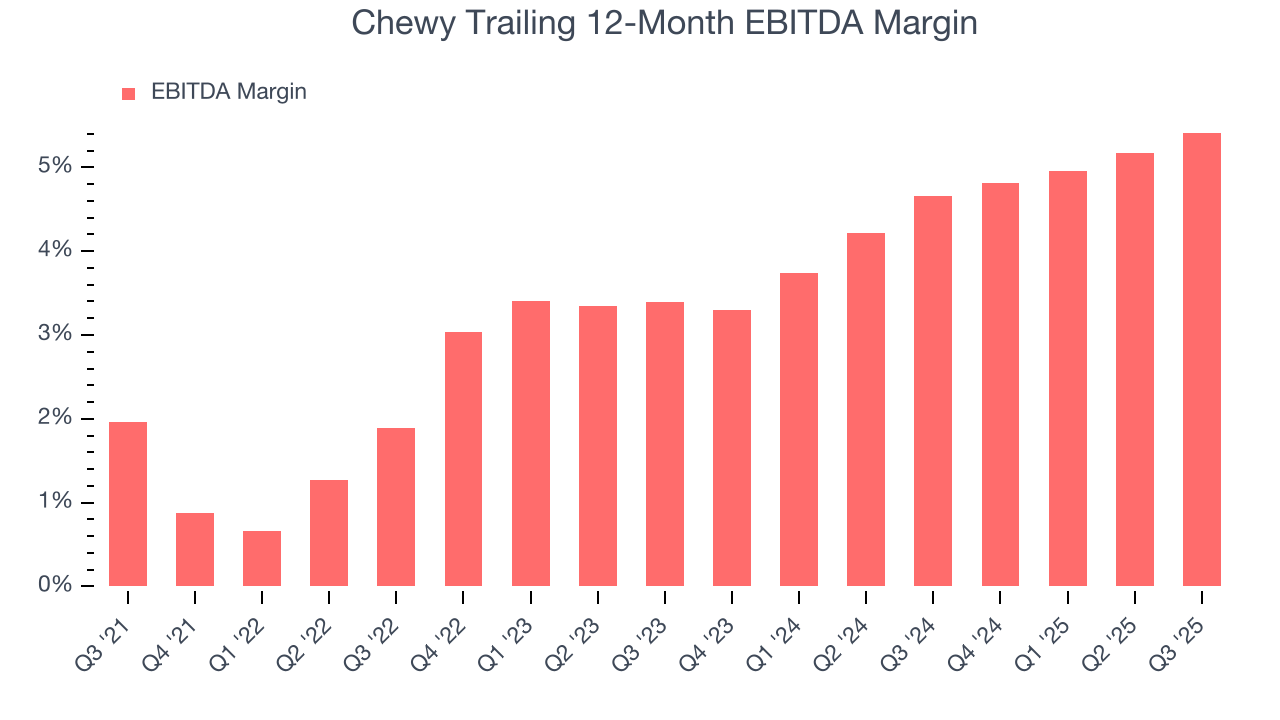

7. EBITDA

Investors regularly analyze operating income to understand a company’s profitability. Similarly, EBITDA is a common profitability metric for consumer internet companies because it excludes various one-time or non-cash expenses, offering a better perspective of the business’s profit potential.

Chewy has managed its cost base well over the last two years. It demonstrated solid profitability for a consumer internet business, producing an average EBITDA margin of 5.1%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Chewy’s EBITDA margin rose by 3.5 percentage points over the last few years, as its sales growth gave it operating leverage.

This quarter, Chewy generated an EBITDA margin profit margin of 5.8%, up 1 percentage points year on year. The increase was encouraging, and because its EBITDA margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

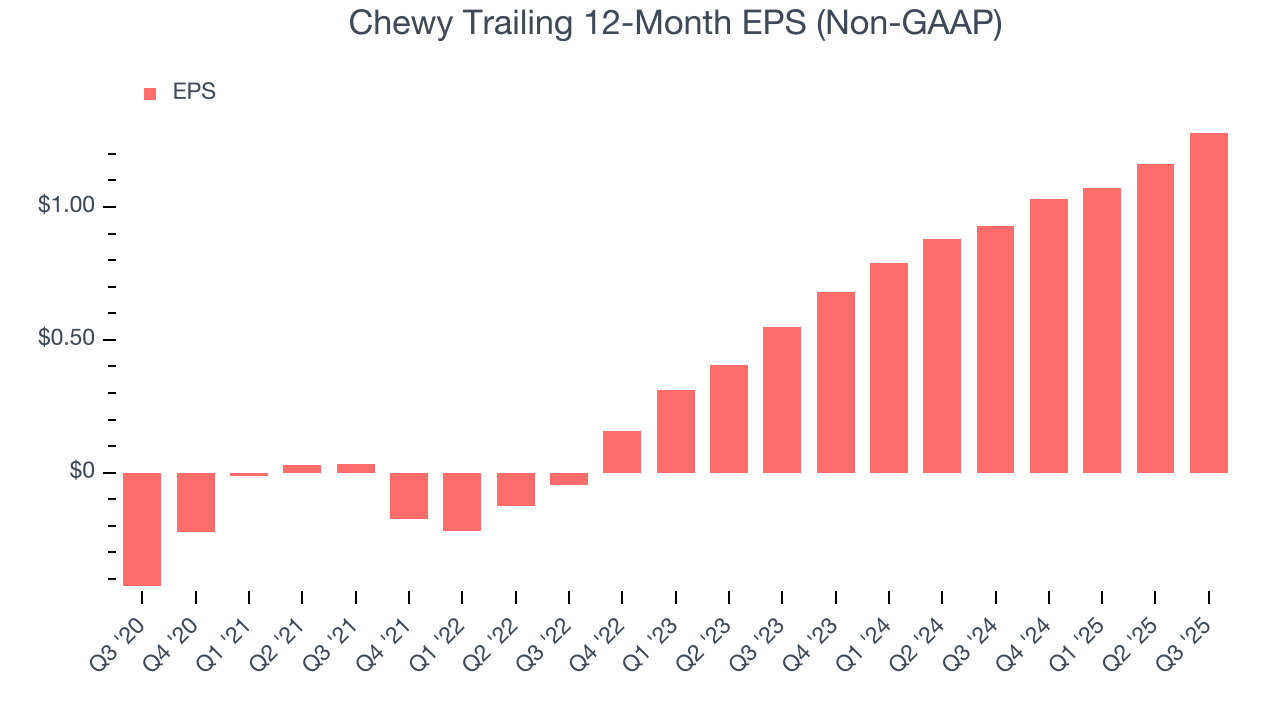

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

In Q3, Chewy reported adjusted EPS of $0.32, up from $0.20 in the same quarter last year. This print beat analysts’ estimates by 5.4%. Over the next 12 months, Wall Street expects Chewy’s full-year EPS of $1.28 to grow 12.1%.

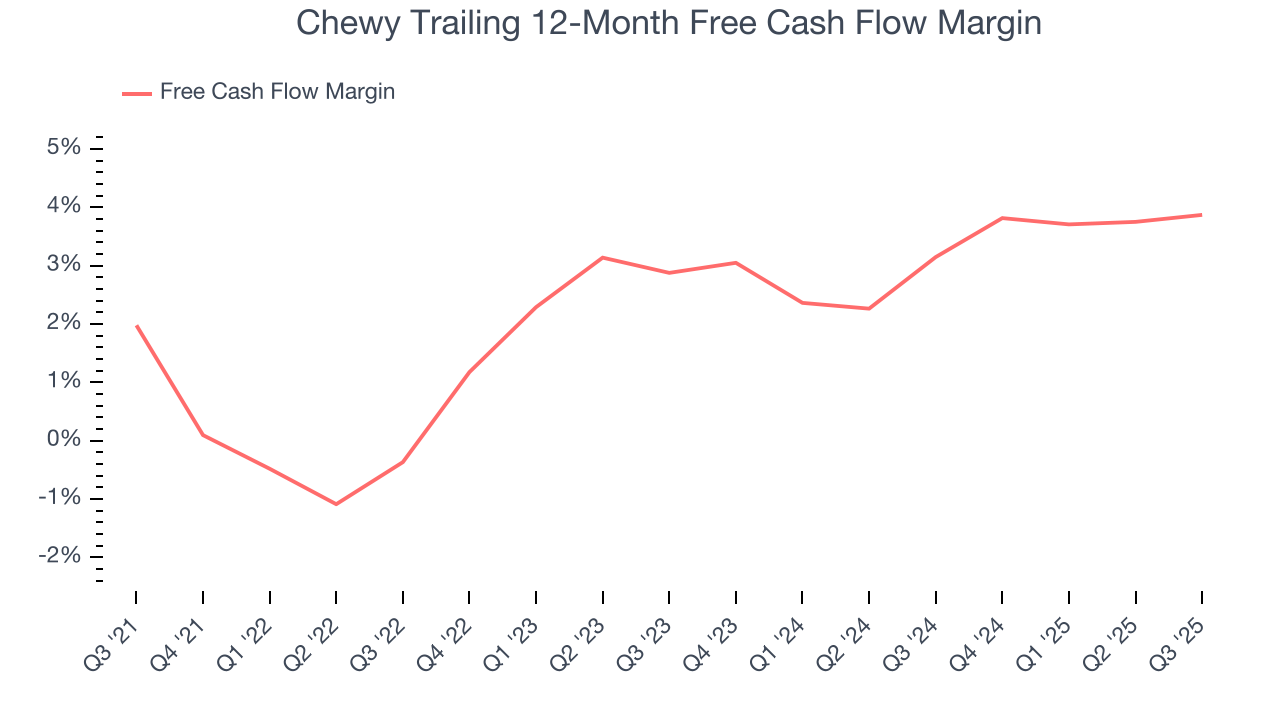

9. Cash Is King

Although EBITDA is undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Chewy has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.5%, subpar for a consumer internet business.

Taking a step back, an encouraging sign is that Chewy’s margin expanded by 4.2 percentage points over the last few years. We have no doubt shareholders would like to continue seeing its cash conversion rise as it gives the company more optionality.

Chewy’s free cash flow clocked in at $175.8 million in Q3, equivalent to a 5.6% margin. This cash profitability was in line with the comparable period last year and above its two-year average.

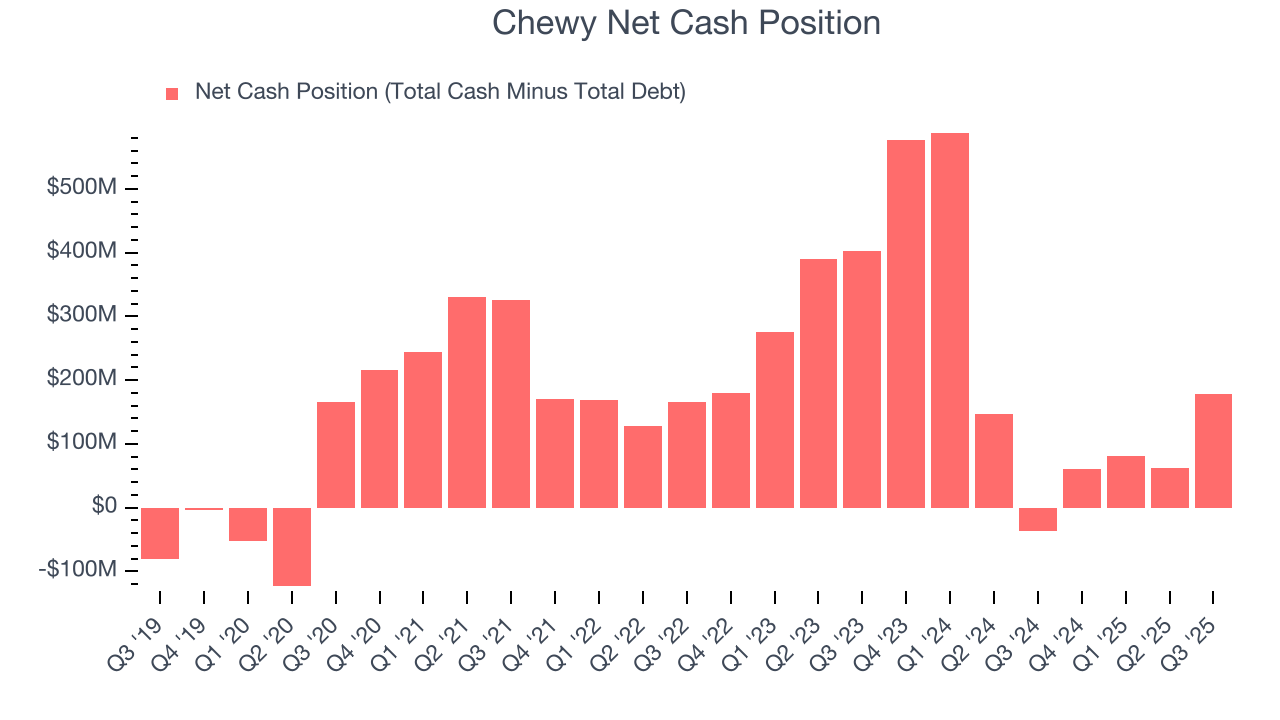

10. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Chewy is a profitable, well-capitalized company with $701.5 million of cash and $523 million of debt on its balance sheet. This $178.5 million net cash position gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Chewy’s Q3 Results

We enjoyed seeing Chewy beat analysts’ EBITDA expectations this quarter. Overall, we think this was a solid quarter with some key areas of upside. The stock traded up 2.8% to $35.82 immediately following the results.

12. Is Now The Time To Buy Chewy?

Updated: March 14, 2026 at 10:23 PM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Chewy, you should also grasp the company’s longer-term business quality and valuation.

Chewy isn’t a terrible business, but it isn’t one of our picks. First off, its revenue growth was mediocre over the last three years, and analysts expect its demand to deteriorate over the next 12 months. And while Chewy’s EPS growth over the last three years has been fantastic, its gross margins make it extremely difficult to reach positive operating profits compared to other consumer internet businesses.

Chewy’s EV/EBITDA ratio based on the next 12 months is 12.3x. This valuation tells us a lot of optimism is priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $43.82 on the company (compared to the current share price of $25.44).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.