Charles River Laboratories (CRL)

We aren’t fans of Charles River Laboratories. Its sales have underperformed and its low returns on capital show it has few growth opportunities.― StockStory Analyst Team

1. News

2. Summary

Why We Think Charles River Laboratories Will Underperform

Named after the Massachusetts river where it was founded in 1947, Charles River Laboratories (NYSE:CRL) provides non-clinical drug development services, research models, and manufacturing support to pharmaceutical and biotechnology companies.

- Organic revenue growth fell short of our benchmarks over the past two years and implies it may need to improve its products, pricing, or go-to-market strategy

- Demand will likely be weak over the next 12 months as Wall Street expects flat revenue

- On the bright side, its disciplined cost controls and effective management have materialized in a strong adjusted operating margin

Charles River Laboratories’s quality isn’t up to par. We’re looking for better stocks elsewhere.

Why There Are Better Opportunities Than Charles River Laboratories

At $153.66 per share, Charles River Laboratories trades at 13.6x forward P/E. Yes, this valuation multiple is lower than that of other healthcare peers, but we’ll remind you that you often get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Charles River Laboratories (CRL) Research Report: Q4 CY2025 Update

Lab services company Charles River Laboratories (NYSE:CRL) beat Wall Street’s revenue expectations in Q4 CY2025, but sales were flat year on year at $994.2 million. Its non-GAAP profit of $2.39 per share was 1.9% above analysts’ consensus estimates.

Charles River Laboratories (CRL) Q4 CY2025 Highlights:

- Revenue: $994.2 million vs analyst estimates of $980.9 million (flat year on year, 1.4% beat)

- Adjusted EPS: $2.39 vs analyst estimates of $2.35 (1.9% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $10.95 at the midpoint, beating analyst estimates by 0.6%

- Operating Margin: -28.5%, down from -16.7% in the same quarter last year

- Free Cash Flow Margin: 8.9%, similar to the same quarter last year

- Organic Revenue fell 2.6% year on year (beat)

- Market Capitalization: $7.80 billion

Company Overview

Named after the Massachusetts river where it was founded in 1947, Charles River Laboratories (NYSE:CRL) provides non-clinical drug development services, research models, and manufacturing support to pharmaceutical and biotechnology companies.

Charles River operates through three main segments that support different stages of drug development. The Research Models and Services segment supplies laboratory animals (primarily rodents) that are essential for early-stage drug testing, along with related services like colony management and health monitoring. These purpose-bred research models serve as foundational tools for discovering new molecules and testing drug safety before human trials.

The Discovery and Safety Assessment segment, which generates the majority of the company's revenue, offers comprehensive services spanning from early drug discovery to regulatory-required safety testing. Scientists at Charles River can identify and validate drug targets, optimize potential drug candidates, and conduct toxicology studies to determine if compounds are safe enough for human trials. This segment allows pharmaceutical companies to outsource complex scientific work rather than maintaining these capabilities in-house.

The Manufacturing Solutions segment helps ensure the quality and safety of biopharmaceutical products. Its Microbial Solutions business provides testing systems to detect contamination in pharmaceutical manufacturing, including the industry-standard endotoxin testing products derived from horseshoe crab blood. The Biologics Solutions business offers analytical testing for biologic drugs and contract development and manufacturing services for cell and gene therapies.

A typical client might engage Charles River to help identify a promising drug candidate, test it in appropriate research models, conduct required safety assessments, and support manufacturing quality control—essentially outsourcing much of the non-clinical development process to a specialized partner. The company generates revenue through service fees and product sales to pharmaceutical companies, biotechnology firms, academic institutions, and government agencies worldwide.

Charles River has expanded its capabilities through strategic acquisitions, particularly in high-growth areas like cell and gene therapy. The company maintains facilities across North America, Europe, and Asia, positioning itself near major biopharmaceutical hubs to serve clients globally.

4. Drug Development Inputs & Services

Companies specializing in drug development inputs and services play a crucial role in the pharmaceutical and biotechnology value chain. Essential support for drug discovery, preclinical testing, and manufacturing means stable demand, as pharmaceutical companies often outsource non-core functions with medium to long-term contracts. However, the business model faces high capital requirements, customer concentration, and vulnerability to shifts in biopharma R&D budgets or regulatory frameworks. Looking ahead, the industry will likely enjoy tailwinds such as increasing investment in biologics, cell and gene therapies, and advancements in precision medicine, which drive demand for sophisticated tools and services. There is a growing trend of outsourcing in drug development for nimbleness and cost efficiency, which benefits the industry. On the flip side, potential headwinds include pricing pressures as efforts to contain healthcare costs are always top of mind. An evolving regulatory backdrop could also slow innovation or client activity.

Charles River's competitors include other preclinical contract research organizations like Labcorp Drug Development (NYSE: LH), IQVIA (NYSE: IQV), and Thermo Fisher Scientific's (NYSE: TMO) contract research services. In the cell and gene therapy CDMO space, it competes with Catalent (NYSE: CTLT) and Lonza Group (SWX: LONN).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $4.02 billion in revenue over the past 12 months, Charles River Laboratories has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

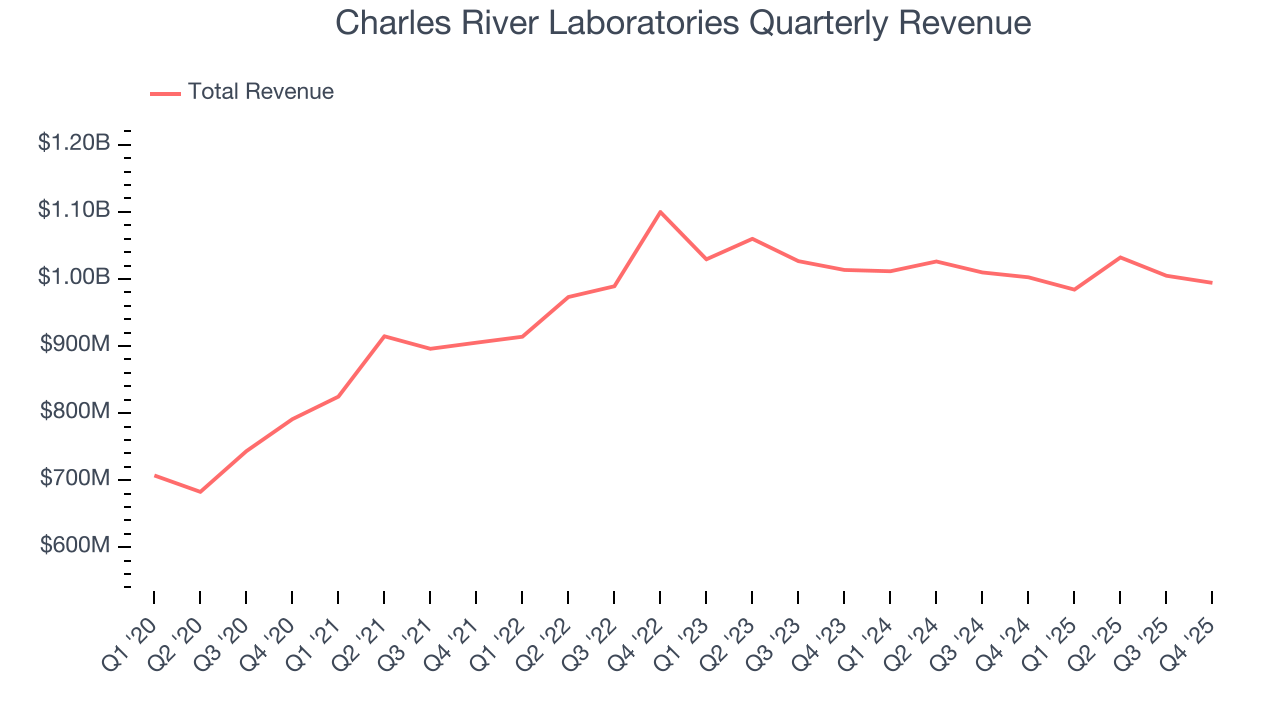

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Regrettably, Charles River Laboratories’s sales grew at a mediocre 6.5% compounded annual growth rate over the last five years. This was below our standard for the healthcare sector and is a tough starting point for our analysis.

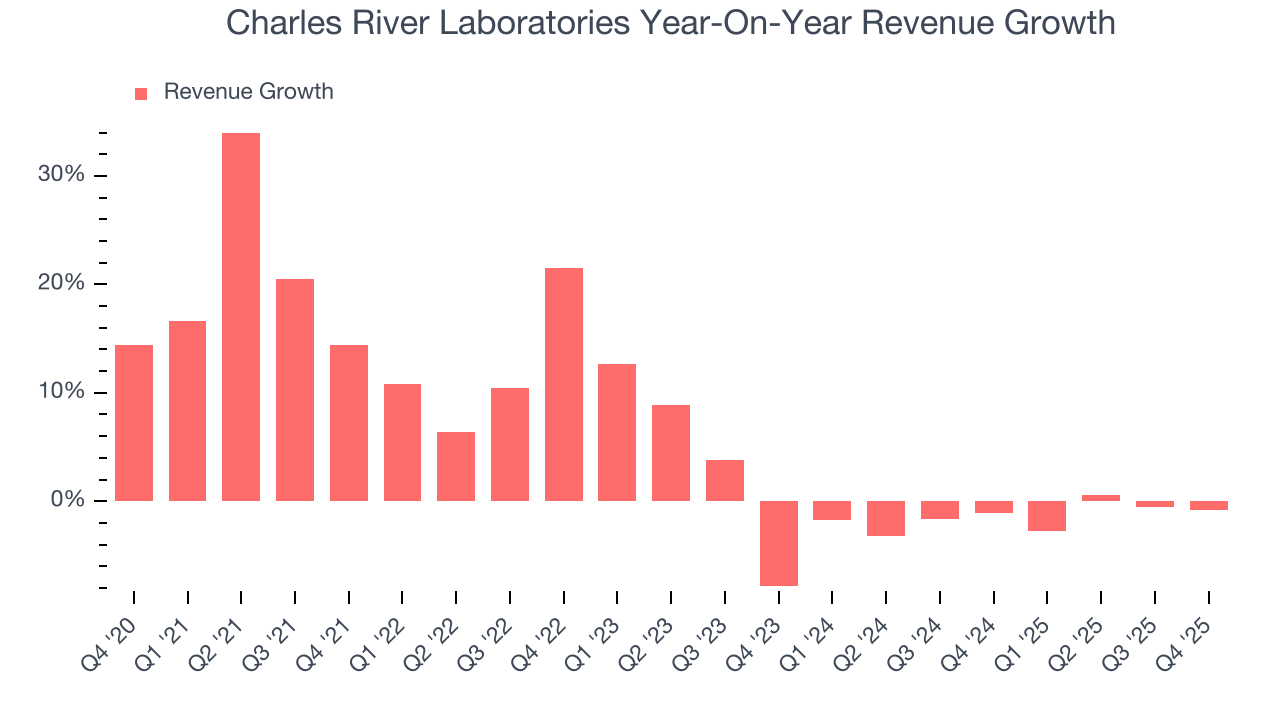

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Charles River Laboratories’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.4% annually.

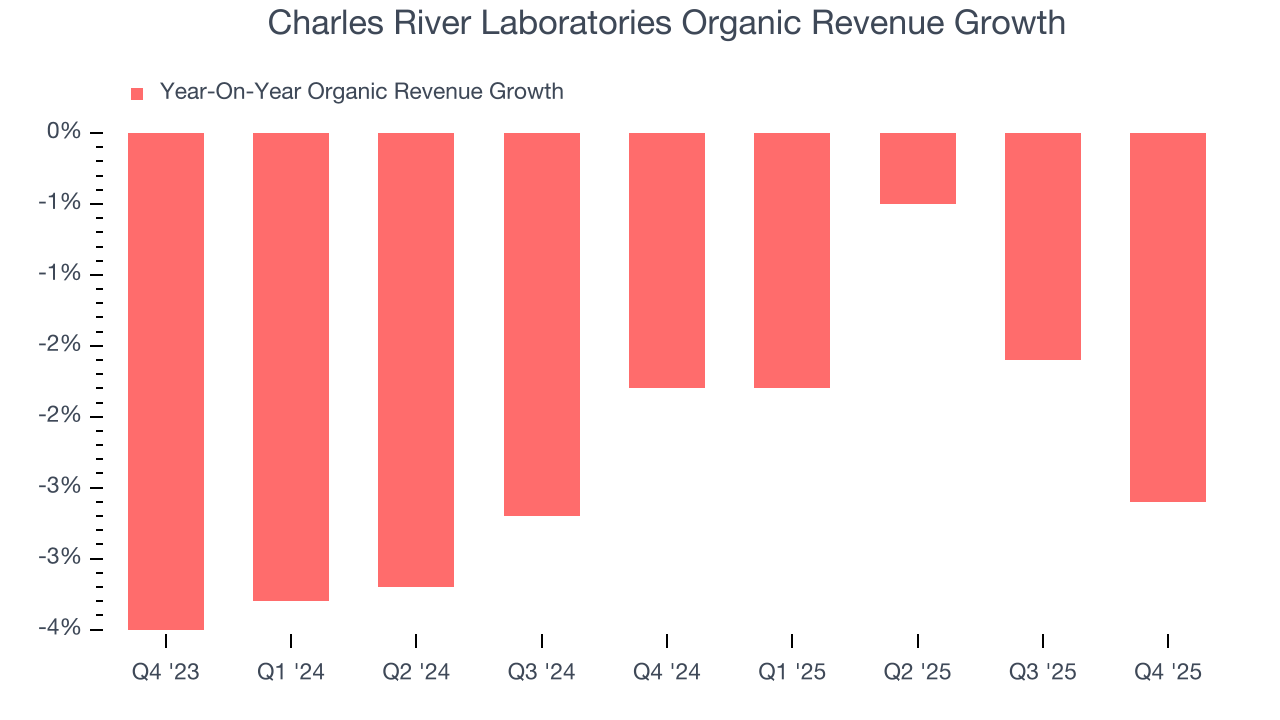

Charles River Laboratories also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Charles River Laboratories’s organic revenue averaged 2.2% year-on-year declines. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Charles River Laboratories’s $994.2 million of revenue was flat year on year but beat Wall Street’s estimates by 1.4%.

Looking ahead, sell-side analysts expect revenue to grow 1.5% over the next 12 months. While this projection suggests its newer products and services will fuel better top-line performance, it is still below the sector average.

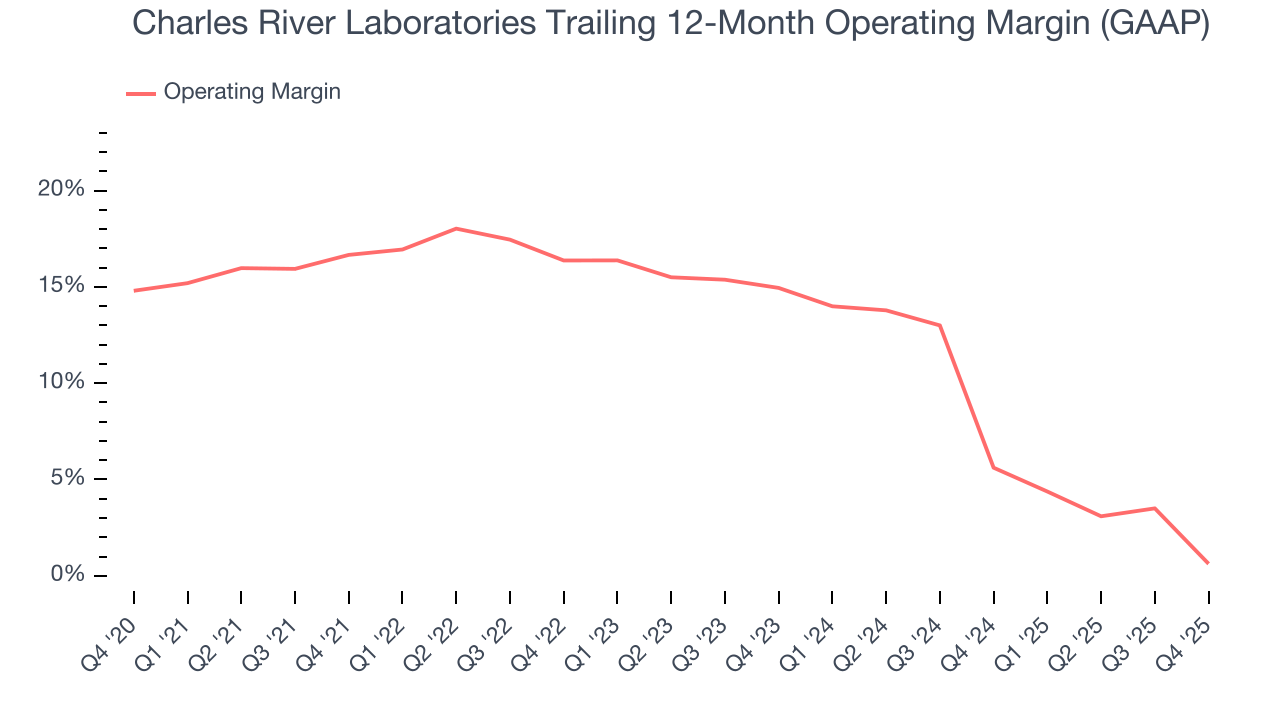

7. Operating Margin

Charles River Laboratories has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 10.7%, higher than the broader healthcare sector.

Looking at the trend in its profitability, Charles River Laboratories’s operating margin decreased by 16 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 14.3 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Charles River Laboratories generated an operating margin profit margin of negative 28.5%, down 11.8 percentage points year on year. This contraction shows it was less efficient because its expenses increased relative to its revenue.

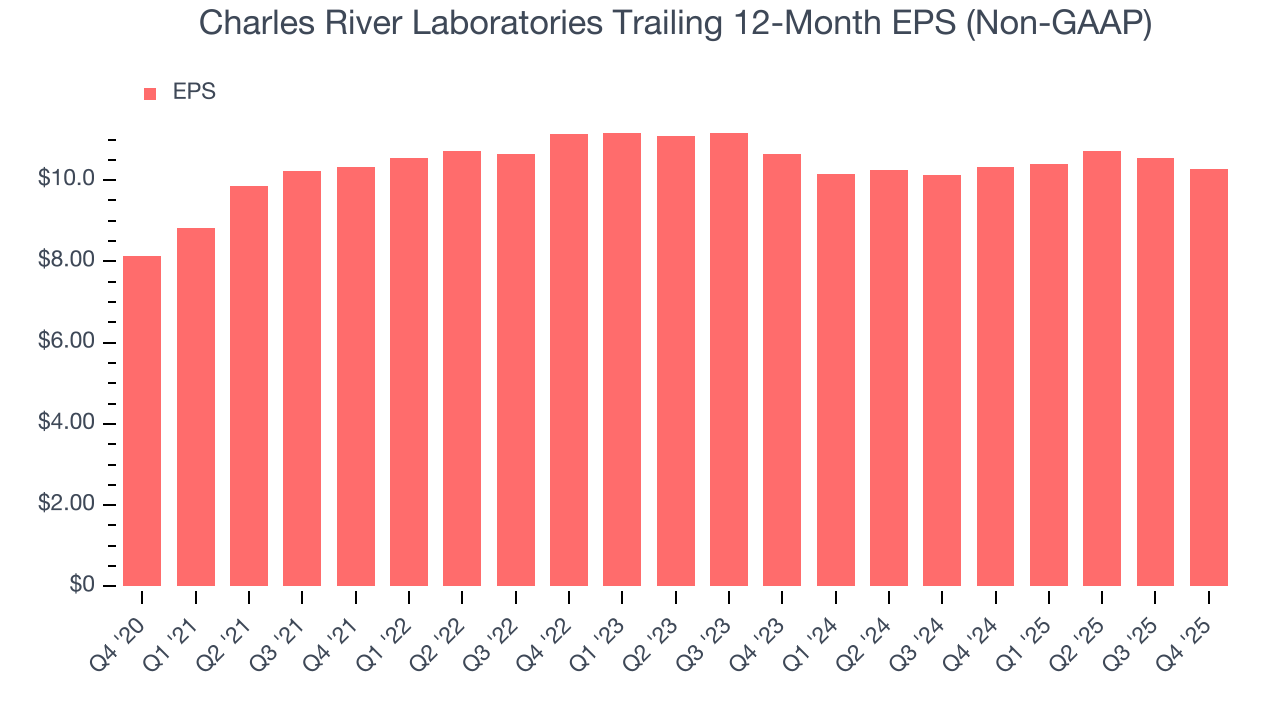

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Charles River Laboratories’s unimpressive 4.8% annual EPS growth over the last five years aligns with its revenue performance. This tells us it maintained its per-share profitability as it expanded.

In Q4, Charles River Laboratories reported adjusted EPS of $2.39, down from $2.66 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 1.9%. Over the next 12 months, Wall Street expects Charles River Laboratories’s full-year EPS of $10.28 to grow 6%.

9. Cash Is King

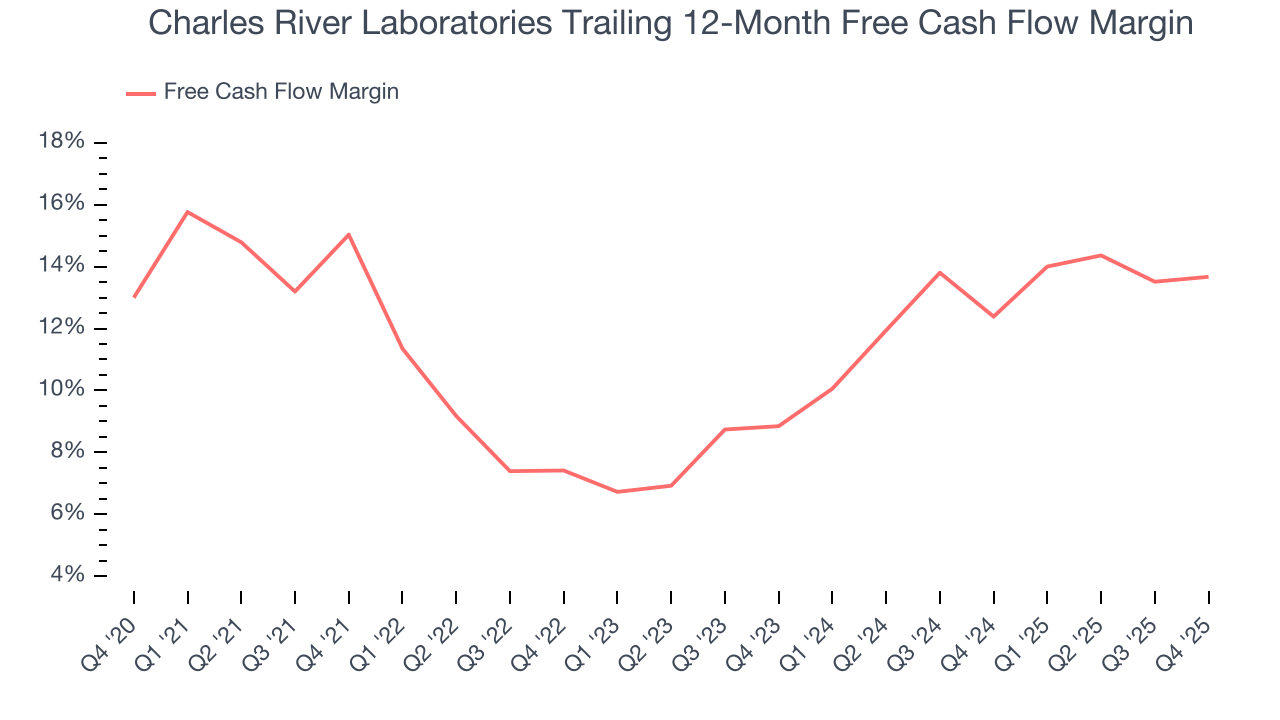

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Charles River Laboratories has shown impressive cash profitability, giving it the option to reinvest or return capital to investors. The company’s free cash flow margin averaged 11.4% over the last five years, better than the broader healthcare sector.

Taking a step back, we can see that Charles River Laboratories’s margin dropped by 1.4 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Charles River Laboratories’s free cash flow clocked in at $88.95 million in Q4, equivalent to a 8.9% margin. This cash profitability was in line with the comparable period last year but below its five-year average. In a silo, this isn’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

10. Return on Invested Capital (ROIC)

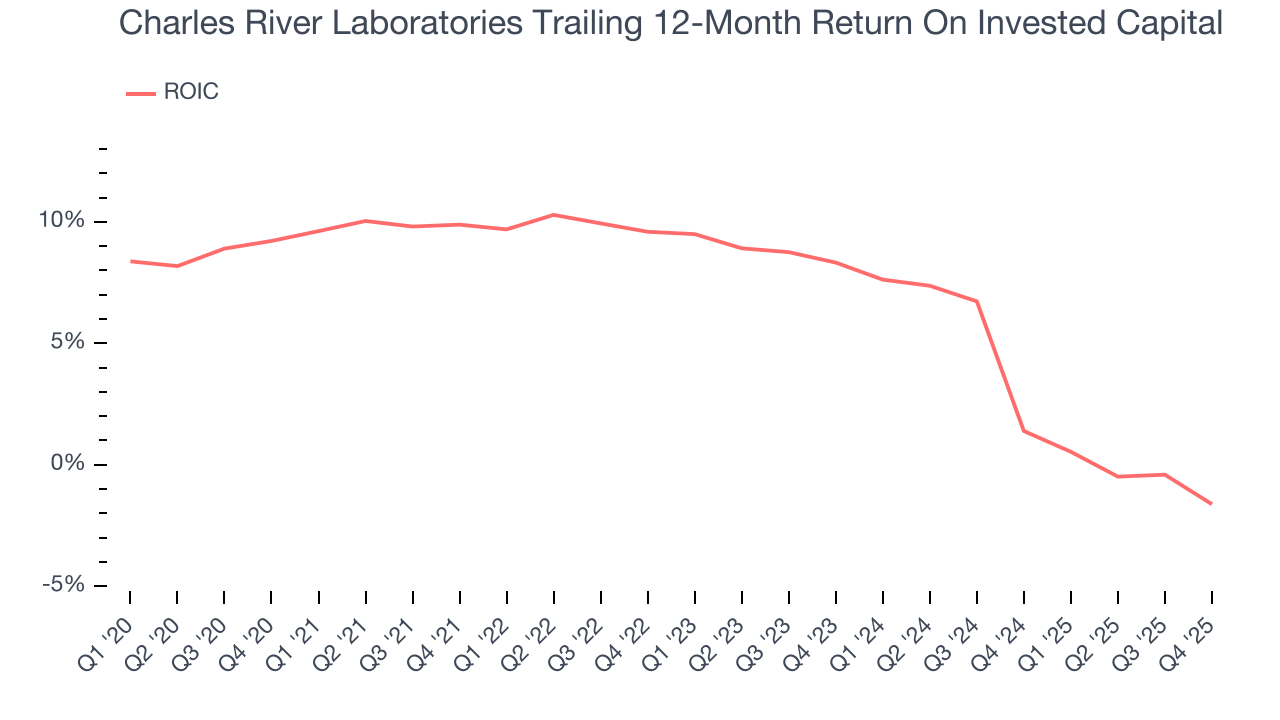

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Charles River Laboratories historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.5%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Charles River Laboratories’s ROIC has decreased over the last few years. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

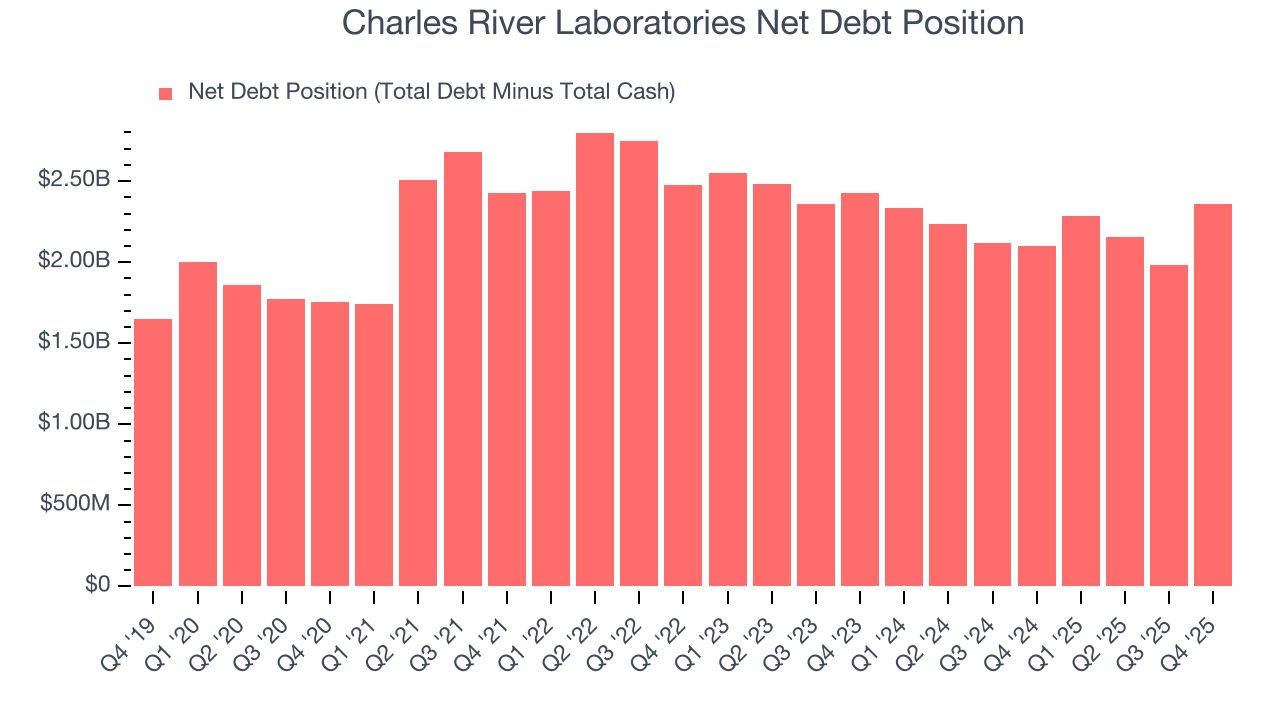

Charles River Laboratories reported $213.8 million of cash and $2.57 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $559.1 million of EBITDA over the last 12 months, we view Charles River Laboratories’s 4.2× net-debt-to-EBITDA ratio as safe. We also see its $56.57 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Charles River Laboratories’s Q4 Results

It was good to see Charles River Laboratories narrowly top analysts’ revenue and EPS expectations this quarter. We were also happy its organic revenue narrowly outperformed Wall Street’s estimates. Looking ahead, EPS guidance was again slightly ahead of expectations. Overall, this print had some key positives. The stock remained flat at $158.00 immediately following the results.

13. Is Now The Time To Buy Charles River Laboratories?

Updated: March 18, 2026 at 12:22 AM EDT

When considering an investment in Charles River Laboratories, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Charles River Laboratories isn’t a terrible business, but it isn’t one of our picks. For starters, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. While its sturdy operating margins show it has disciplined cost controls, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its organic revenue declined.

Charles River Laboratories’s P/E ratio based on the next 12 months is 13.6x. Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $197.47 on the company (compared to the current share price of $153.66).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.