Curtiss-Wright (CW)

We see solid potential in Curtiss-Wright. It not only produces robust profits but also has improved its margins, showing its quality is rising.― StockStory Analyst Team

1. News

2. Summary

Why We Like Curtiss-Wright

Formed from a merger of 12 companies, Curtiss-Wright (NYSE:CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

- Earnings growth has massively outpaced its peers over the last two years as its EPS has compounded at 18% annually

- Excellent operating margin highlights the strength of its business model, and its operating leverage amplified its profits over the last five years

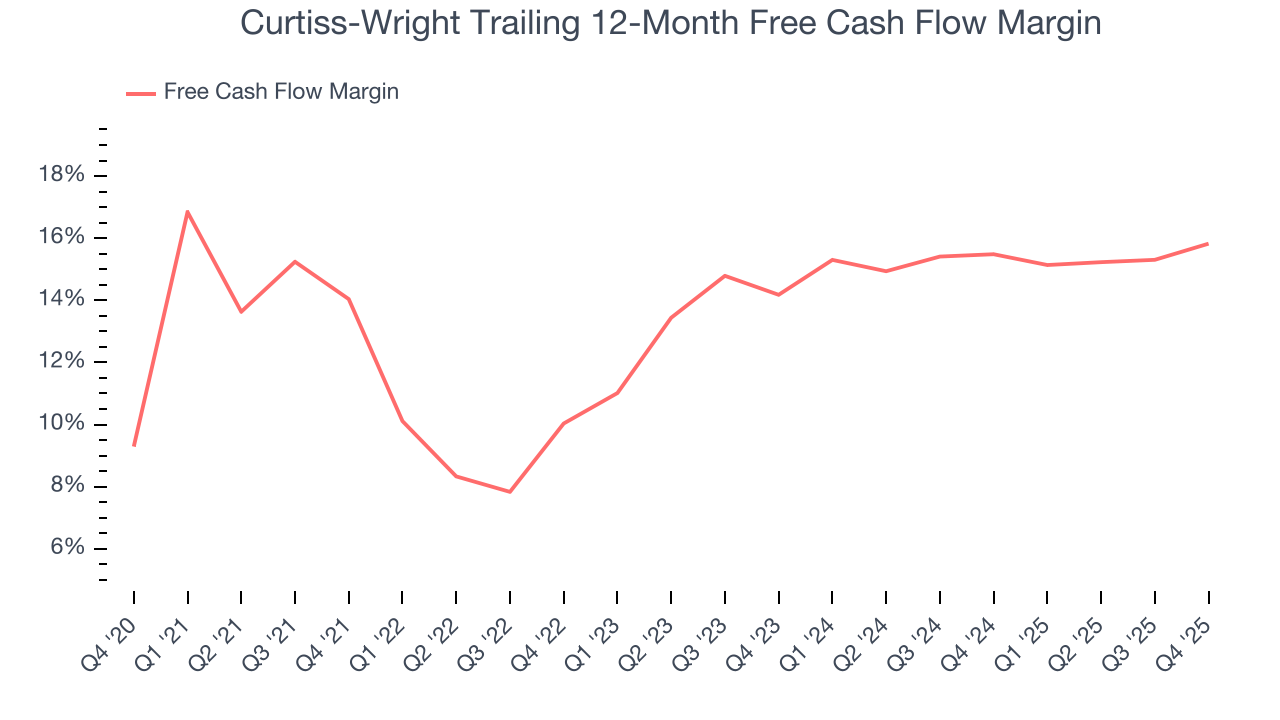

- Strong free cash flow margin of 13.9% gives it the option to reinvest, repurchase shares, or pay dividends

We see a bright future for Curtiss-Wright. No coincidence the stock is up 458% over the last five years.

Is Now The Time To Buy Curtiss-Wright?

At $645.97 per share, Curtiss-Wright trades at 46.8x forward P/E. There’s no arguing the market has lofty expectations given its premium multiple.

Are you a fan of the company and its story? If so, we suggest a small position as the long-term outlook seems promising. Keep in mind that Curtiss-Wright’s lofty valuation could result in short-term volatility based on both macro and company-specific factors.

3. Curtiss-Wright (CW) Research Report: Q4 CY2025 Update

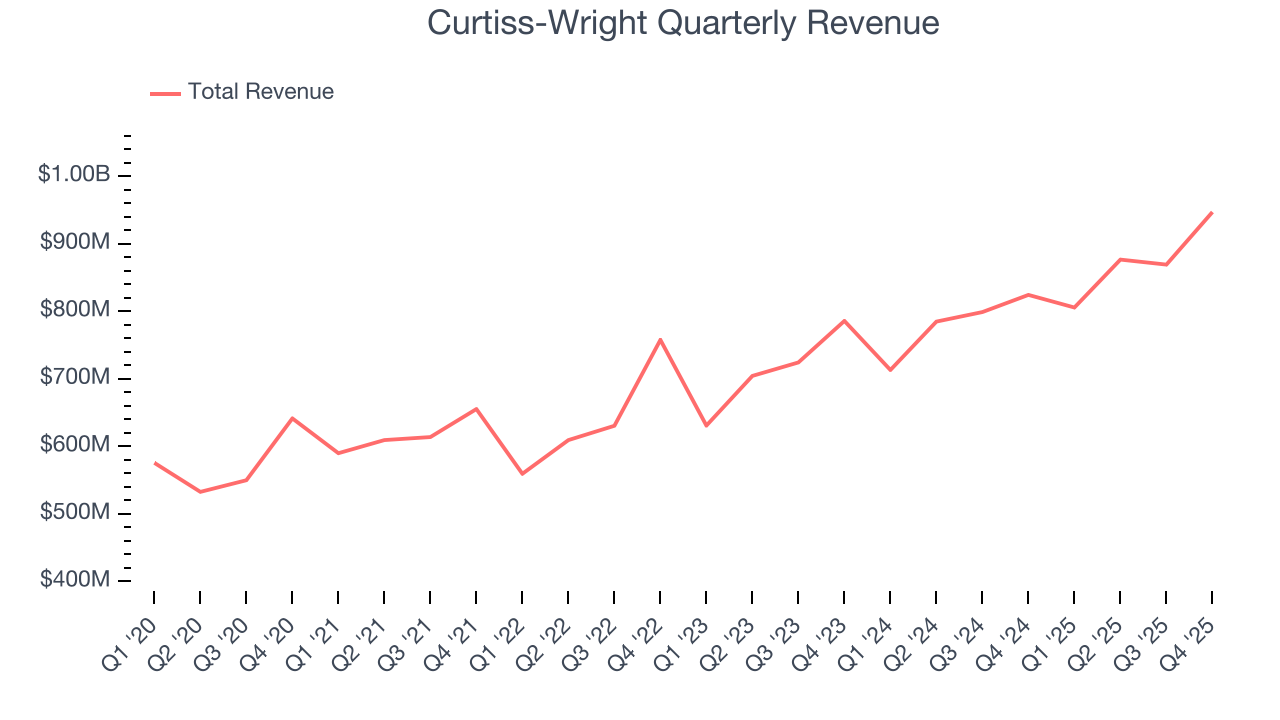

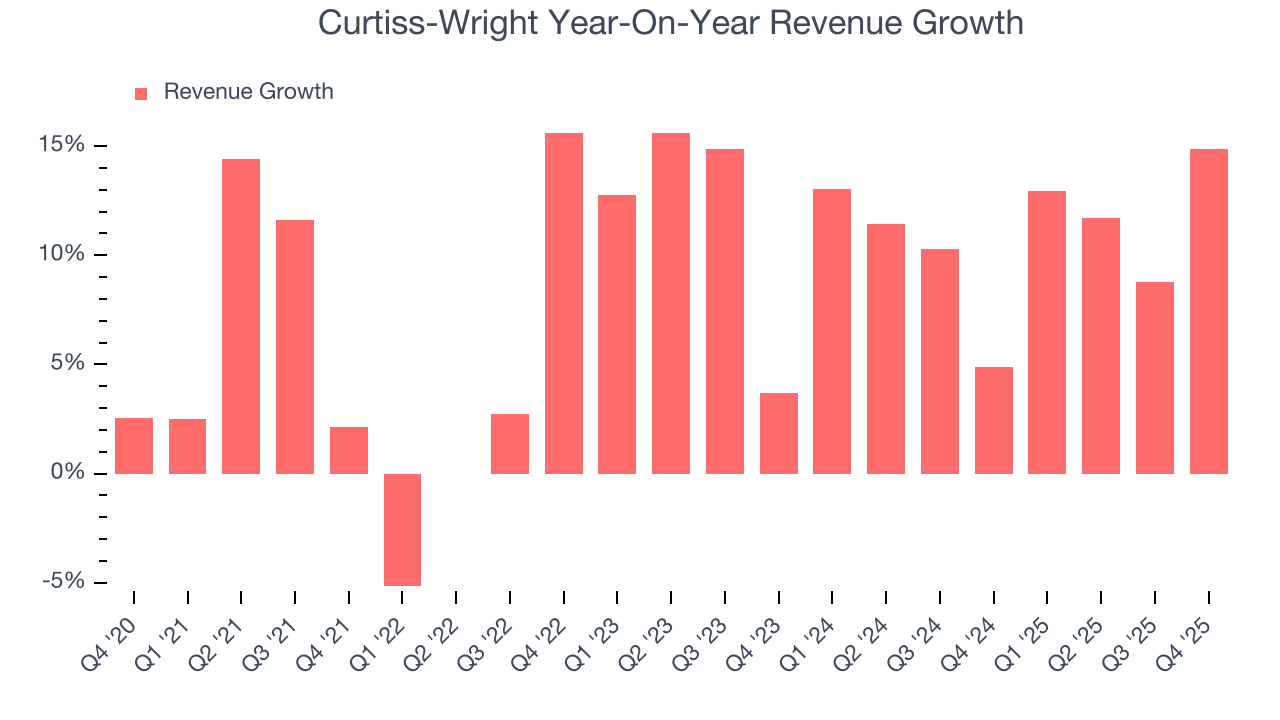

Aerospace and defense company Curtiss-Wright (NYSE:CW) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 14.9% year on year to $947 million. The company’s full-year revenue guidance of $3.74 billion at the midpoint came in 1.2% above analysts’ estimates. Its non-GAAP profit of $3.79 per share was 2.8% above analysts’ consensus estimates.

Curtiss-Wright (CW) Q4 CY2025 Highlights:

- Revenue: $947 million vs analyst estimates of $890.4 million (14.9% year-on-year growth, 6.4% beat)

- Adjusted EPS: $3.79 vs analyst estimates of $3.69 (2.8% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $14.93 at the midpoint, beating analyst estimates by 2.1%

- Operating Margin: 19.2%, in line with the same quarter last year

- Free Cash Flow Margin: 33.3%, similar to the same quarter last year

- Market Capitalization: $23.8 billion

Company Overview

Formed from a merger of 12 companies, Curtiss-Wright (NYSE:CW) provides a range of products and services to the aerospace, industrial, electronic, and maritime industries.

Curtiss-Wright was formed in 1929 through the merger of companies founded by Glenn Curtiss, the father of naval aviation, and the Wright brothers, who are credited with building the world’s first successful airplane. It initially focused on aircraft manufacturing and has since diversified into various products including electronic systems and flow control technologies.

Today, Curtiss-Wright offers specialized products and services across the aerospace, defense, and power industries. The company produces everything from power management electronics and aircraft sensors to advanced surface treatments that improve the durability of metal parts. Specifically, in defense, Curtiss-Wright provides vital technologies such as embedded computing systems, flight testing instruments, and communication solutions while in the naval and energy sectors it supplies equipment like naval propulsion systems and coolant pumps for nuclear reactors.

Curtiss-Wright primarily goes to market through a global network of direct sales forces and independent representatives. Revenue is largely generated from the sale of engineered components, systems, and services, and a significant portion comes from long-term contracts with government and defense entities as well as commercial agreements within the power generation and naval sectors.

In addition to outright sales, Curtiss-Wright benefits from aftermarket revenue sources such as maintenance, repair, and overhaul services, and the supply of replacement parts. These services are crucial for ensuring the operational continuity and efficiency of customer equipment, thus creating a consistent demand and revenue stream.

The financial performance of Curtiss-Wright is closely linked to governmental defense spending, the health of the aerospace industry, and the global demand for energy, particularly nuclear power. These factors directly affect the company’s sales volumes and the development of new projects within its key market segments.

4. Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Curtiss-Wright’s peers and competitors include Lockheed Martin (NYSE:LMT), General Electrics (NYSE:GE), and Honeywell International (NASDAQ:HON)

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Thankfully, Curtiss-Wright’s 8.8% annualized revenue growth over the last five years was decent. Its growth was slightly above the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Curtiss-Wright’s annualized revenue growth of 10.9% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

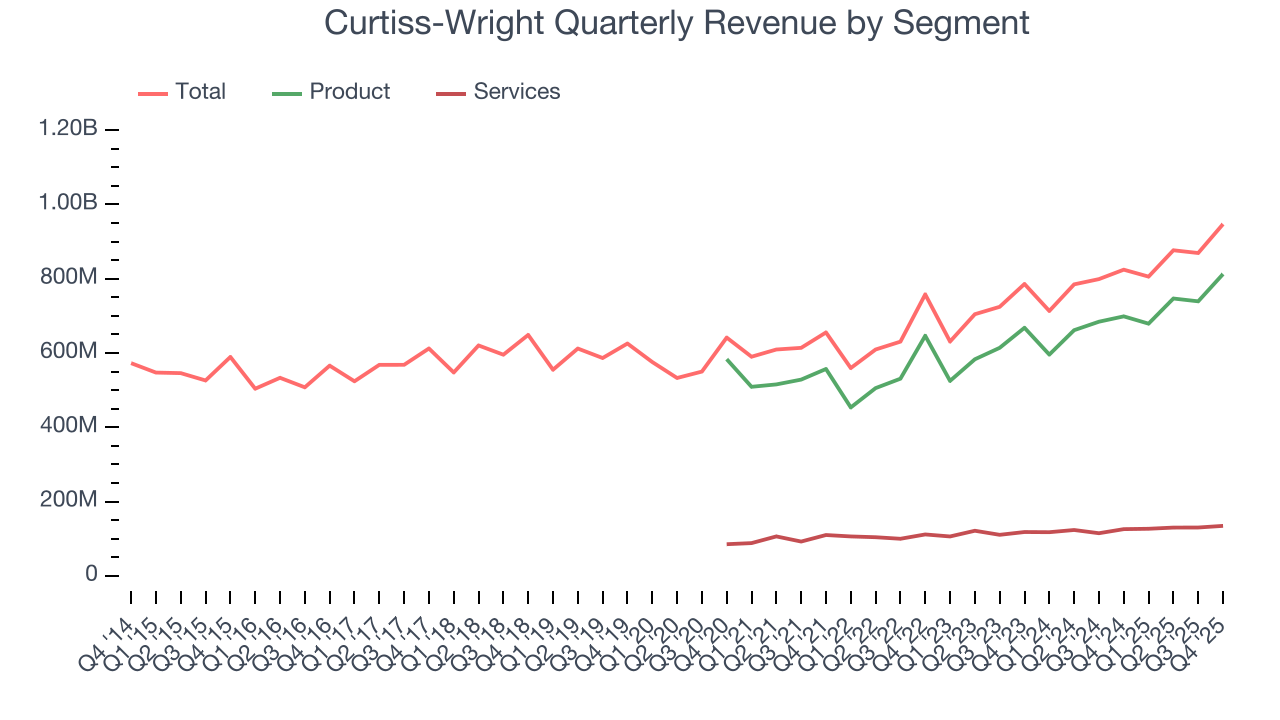

We can dig further into the company’s revenue dynamics by analyzing its most important segments, Product and Services, which are 85.8% and 14.2% of revenue. Over the last two years, Curtiss-Wright’s Product revenue (aerospace & defense technology) averaged 11.8% year-on-year growth while its Services revenue (testing, maintenance, consulting) averaged 7.1% growth.

This quarter, Curtiss-Wright reported year-on-year revenue growth of 14.9%, and its $947 million of revenue exceeded Wall Street’s estimates by 6.4%.

Looking ahead, sell-side analysts expect revenue to grow 5.7% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and indicates its products and services will see some demand headwinds. At least the company is tracking well in other measures of financial health.

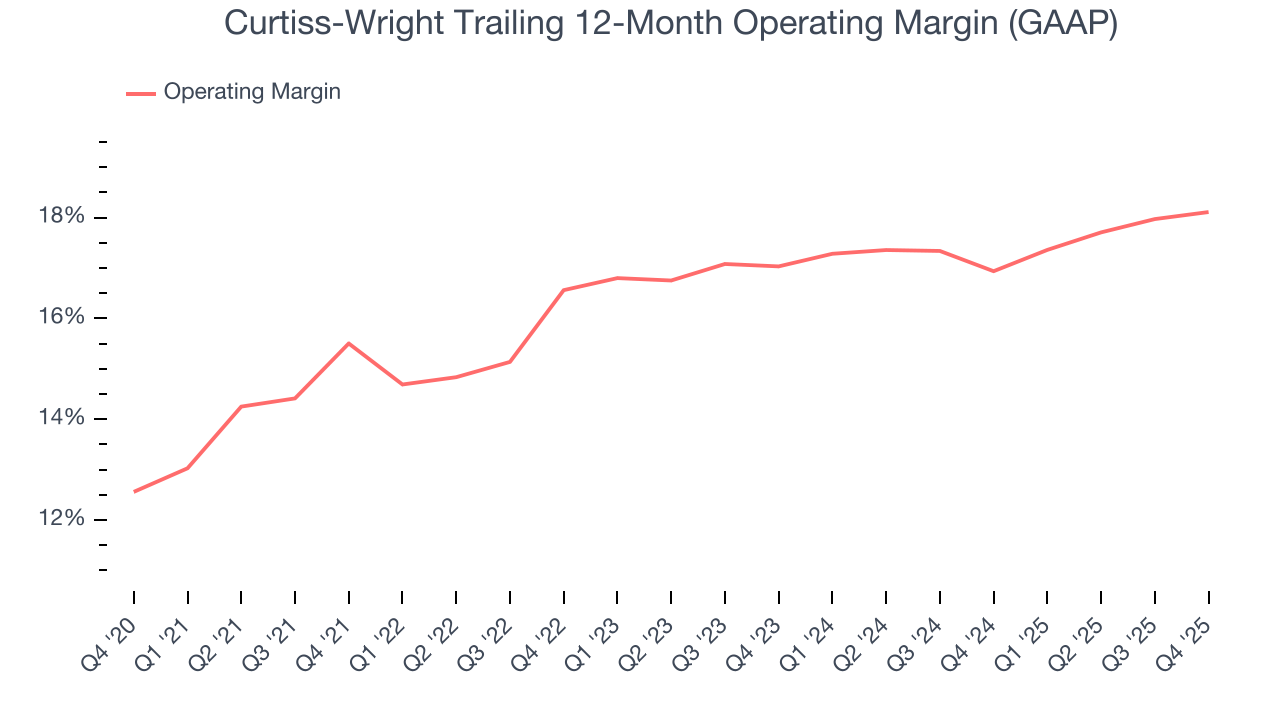

6. Operating Margin

Curtiss-Wright has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.9%.

Looking at the trend in its profitability, Curtiss-Wright’s operating margin rose by 2.6 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q4, Curtiss-Wright generated an operating margin profit margin of 19.2%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

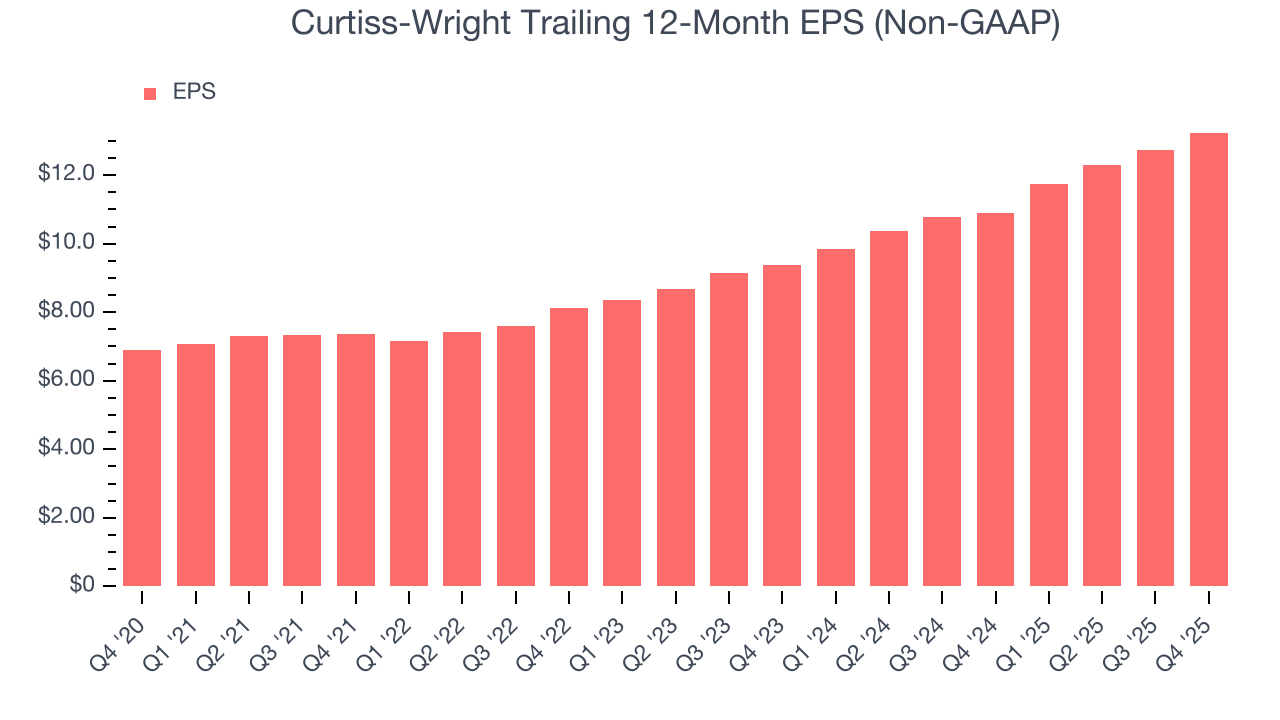

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Curtiss-Wright’s EPS grew at a remarkable 14% compounded annual growth rate over the last five years, higher than its 8.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

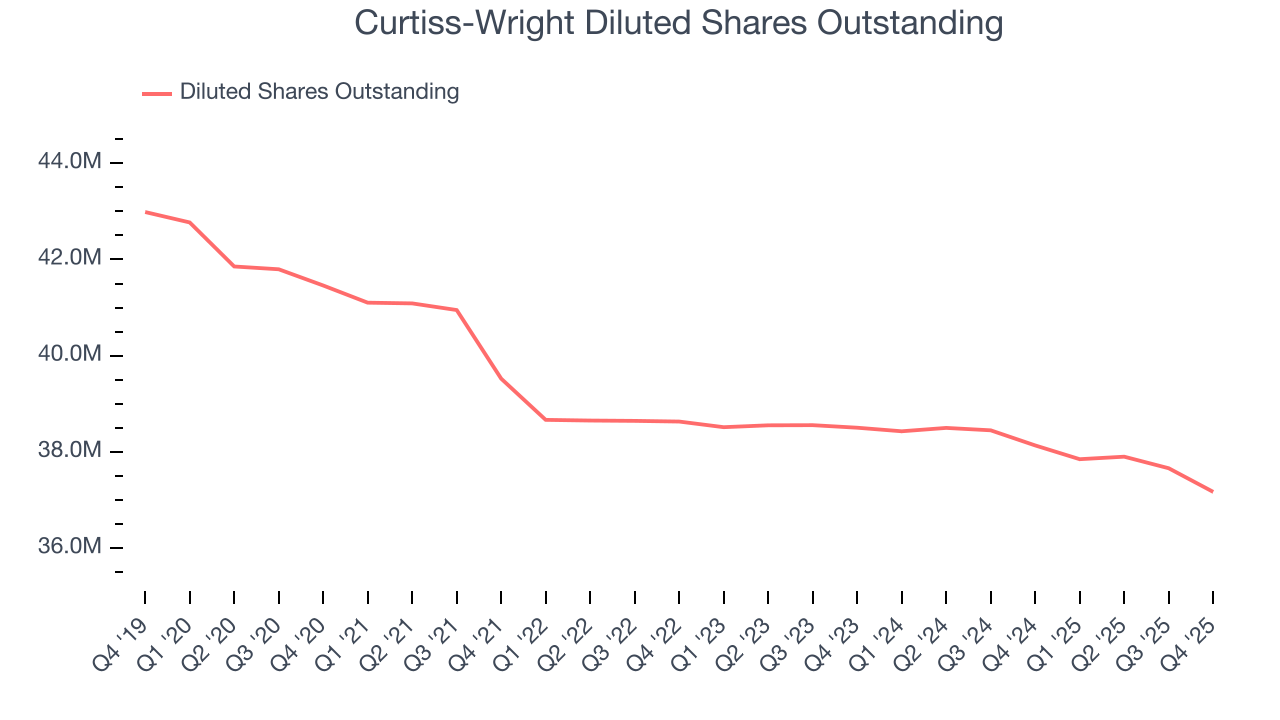

Diving into the nuances of Curtiss-Wright’s earnings can give us a better understanding of its performance. As we mentioned earlier, Curtiss-Wright’s operating margin was flat this quarter but expanded by 2.6 percentage points over the last five years. On top of that, its share count shrank by 10.3%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Curtiss-Wright, its two-year annual EPS growth of 18.8% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Curtiss-Wright reported adjusted EPS of $3.79, up from $3.27 in the same quarter last year. This print beat analysts’ estimates by 2.8%. Over the next 12 months, Wall Street expects Curtiss-Wright’s full-year EPS of $13.24 to grow 9.7%.

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Curtiss-Wright has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 14.1% over the last five years.

Taking a step back, we can see that Curtiss-Wright’s margin expanded by 1.8 percentage points during that time. This is encouraging because it gives the company more optionality.

Curtiss-Wright’s free cash flow clocked in at $315 million in Q4, equivalent to a 33.3% margin. This cash profitability was in line with the comparable period last year and above its five-year average.

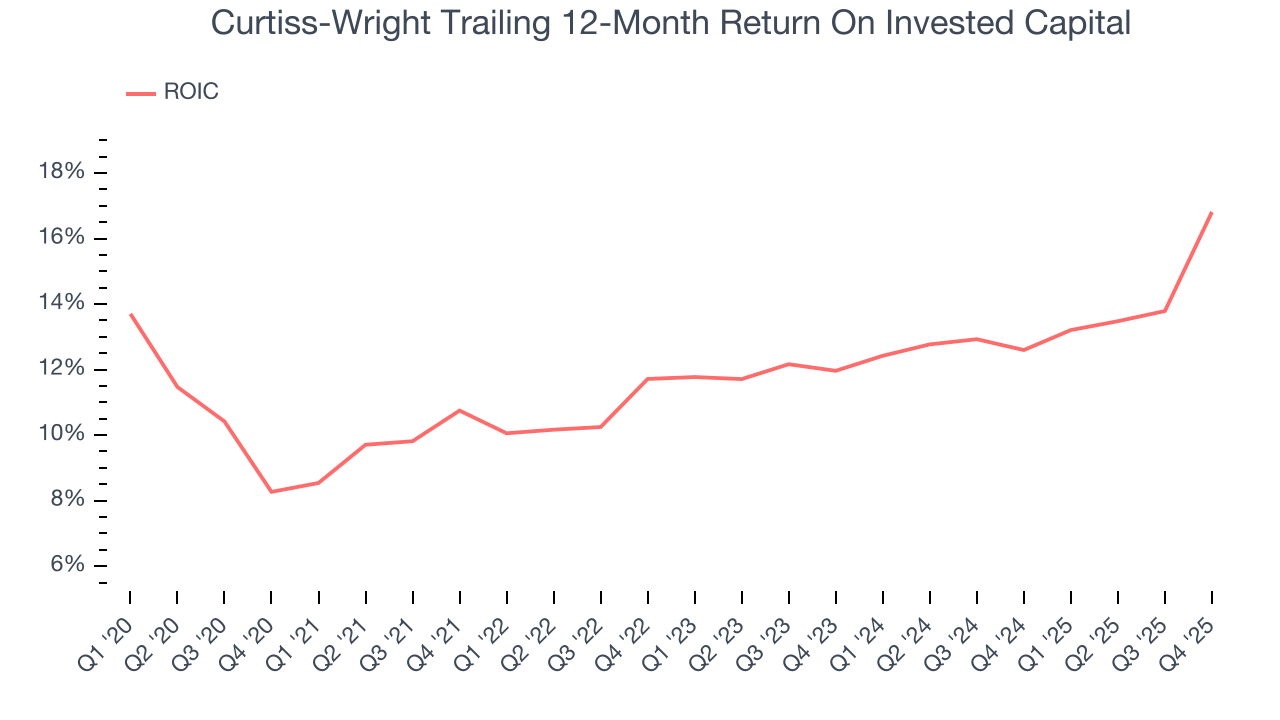

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Curtiss-Wright’s five-year average ROIC was 12.8%, higher than most industrials businesses. This illustrates its management team’s ability to invest in profitable growth opportunities and generate value for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Curtiss-Wright’s ROIC increased by 3.5 percentage points annually each year over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

10. Key Takeaways from Curtiss-Wright’s Q4 Results

We were impressed by how significantly Curtiss-Wright blew past analysts’ revenue expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 3.1% to $654.50 immediately after reporting.

11. Is Now The Time To Buy Curtiss-Wright?

Updated: February 11, 2026 at 4:47 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Curtiss-Wright is an amazing business ranking highly on our list. First of all, the company’s revenue growth was good over the last five years. On top of that, its impressive operating margins show it has a highly efficient business model, and its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits.

Curtiss-Wright’s P/E ratio based on the next 12 months is 43.7x. A lot of good news is certainly baked in given its premium multiple, but we’ll happily own Curtiss-Wright as its fundamentals really stand out. It’s often wise to hold investments like this for at least three to five years, as the power of long-term compounding negates short-term price swings that can accompany high valuations.

Wall Street analysts have a consensus one-year price target of $638.14 on the company (compared to the current share price of $654.50).