Danaher (DHR)

We’re skeptical of Danaher. Its weak sales growth and declining returns on capital show its demand and profits are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Danaher Will Underperform

Born from a real estate investment trust that transformed into a manufacturing powerhouse, Danaher (NYSE:DHR) is a global science and technology company that provides specialized equipment, software, and services for biotechnology, life sciences, and diagnostics.

- Annual sales growth of 2% over the last five years lagged behind its healthcare peers as its large revenue base made it difficult to generate incremental demand

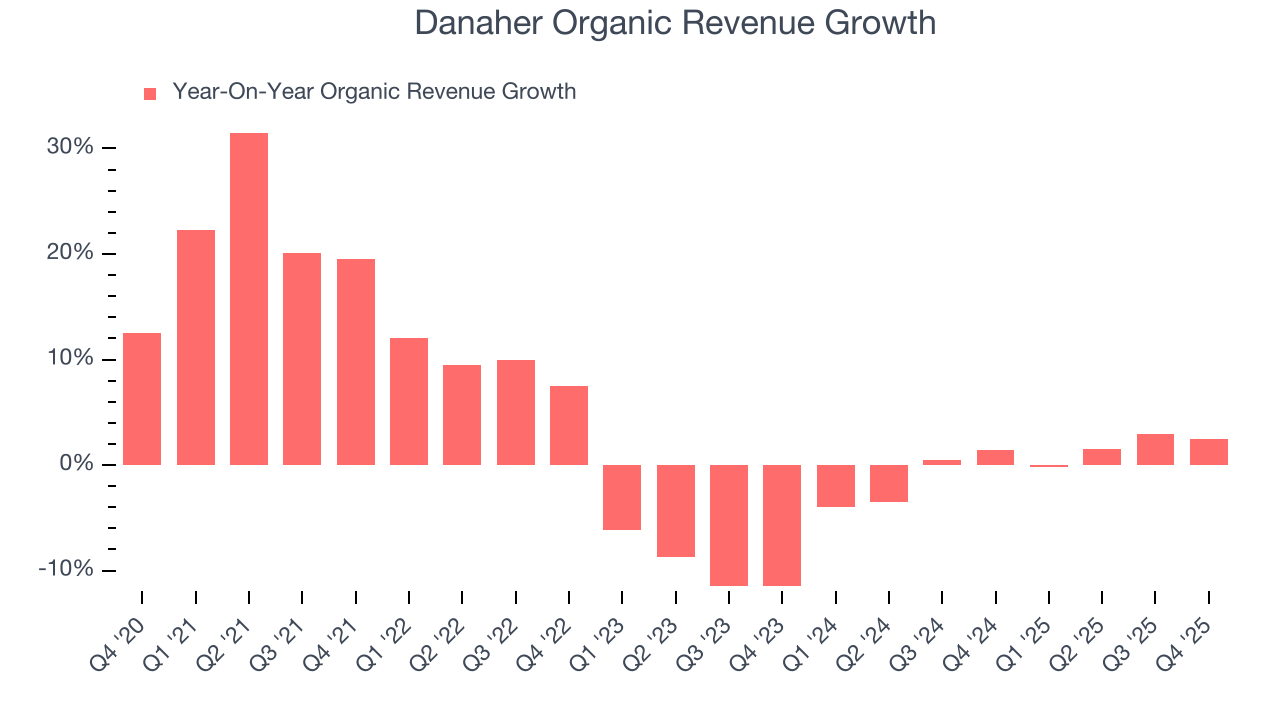

- Core business is underperforming as its organic revenue has disappointed over the past two years, suggesting it might need acquisitions to stimulate growth

- A positive is that its excellent adjusted operating margin highlights the strength of its business model

Danaher falls short of our quality standards. We see more attractive opportunities in the market.

Why There Are Better Opportunities Than Danaher

At $190.29 per share, Danaher trades at 22.8x forward P/E. Not only is Danaher’s multiple richer than most healthcare peers, but it’s also expensive for its revenue characteristics.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Danaher (DHR) Research Report: Q4 CY2025 Update

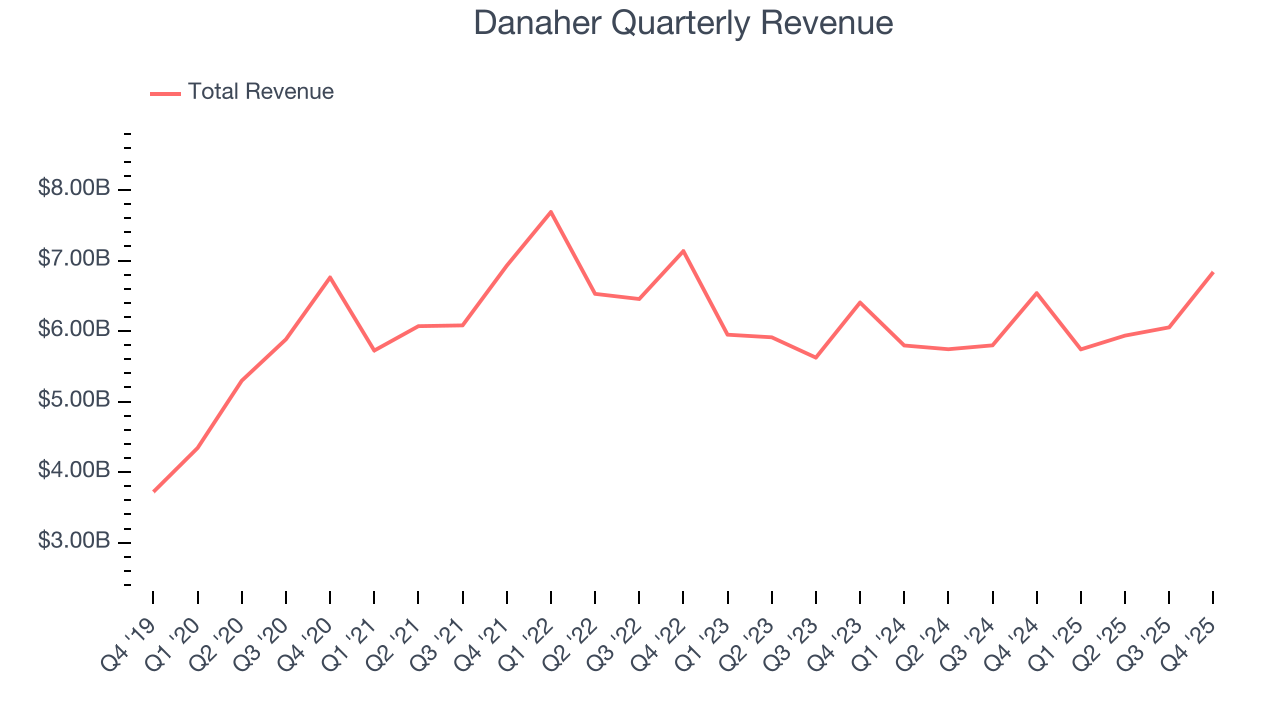

Diversified science and technology company Danaher (NYSE:DHR) met Wall Streets revenue expectations in Q4 CY2025, with sales up 4.6% year on year to $6.84 billion. Its non-GAAP profit of $2.23 per share was 1.8% above analysts’ consensus estimates.

Danaher (DHR) Q4 CY2025 Highlights:

- Revenue: $6.84 billion vs analyst estimates of $6.81 billion (4.6% year-on-year growth, in line)

- Adjusted EPS: $2.23 vs analyst estimates of $2.19 (1.8% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $8.43 at the midpoint, in line with analyst estimates

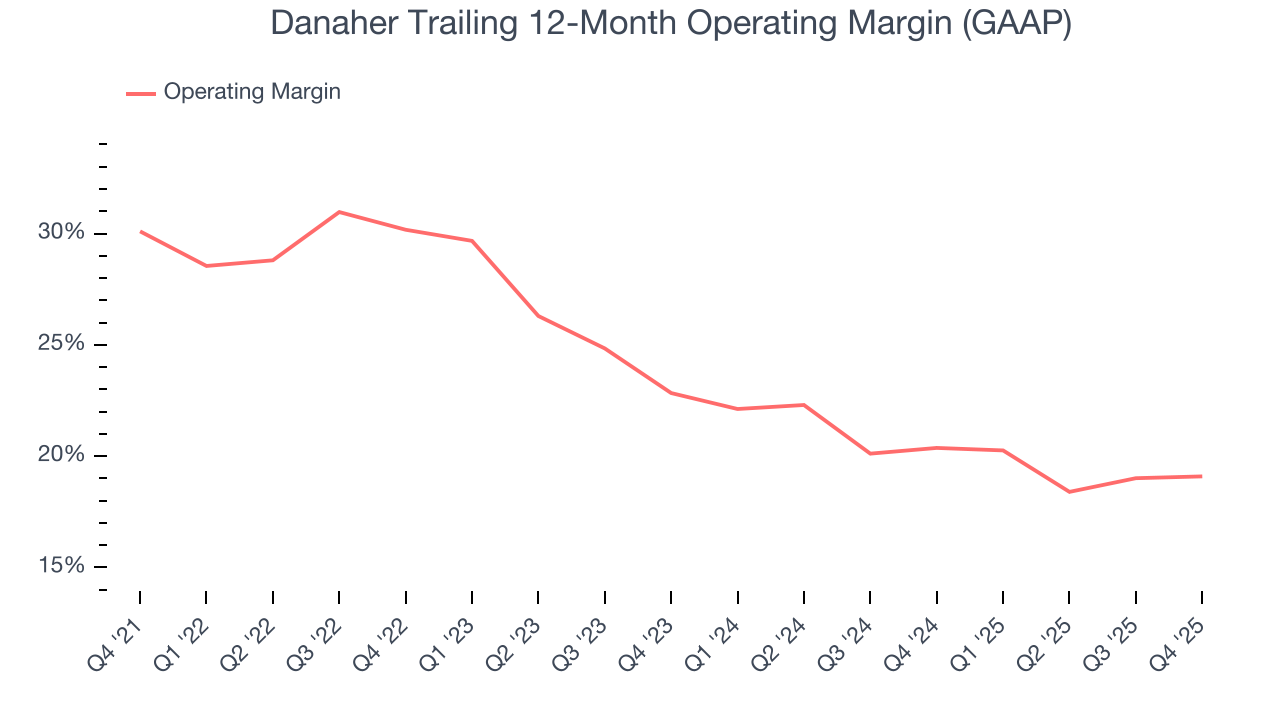

- Operating Margin: 22%, in line with the same quarter last year

- Free Cash Flow Margin: 25.5%, up from 23% in the same quarter last year

- Organic Revenue rose 2.5% year on year (beat)

- Market Capitalization: $166.5 billion

Company Overview

Born from a real estate investment trust that transformed into a manufacturing powerhouse, Danaher (NYSE:DHR) is a global science and technology company that provides specialized equipment, software, and services for biotechnology, life sciences, and diagnostics.

Danaher operates through three main segments: Biotechnology, Life Sciences, and Diagnostics. Each segment serves distinct but interconnected markets within healthcare and scientific research.

In its Biotechnology segment, Danaher provides technologies that help pharmaceutical companies develop and manufacture biological medicines. These range from traditional therapies like vaccines and insulin to cutting-edge treatments such as cell and gene therapies. For example, a biotech company might use Danaher's filtration systems and bioreactors to produce monoclonal antibodies for cancer treatment, while relying on its quality control instruments to ensure product purity.

The Life Sciences segment offers tools that researchers use to study the building blocks of life—DNA, RNA, proteins, and cells. These instruments help scientists understand disease mechanisms and identify potential treatments. A university researcher investigating Alzheimer's disease might use Danaher's mass spectrometers to analyze brain proteins, microscopes to examine tissue samples, and genomic tools to study genetic factors.

In Diagnostics, Danaher provides systems that healthcare providers use to diagnose diseases and guide treatment decisions. These include blood analyzers that detect markers of heart disease, molecular diagnostic platforms that identify infectious pathogens, and pathology systems that help detect cancer. A hospital laboratory might run hundreds of patient blood samples daily through Danaher's chemistry analyzers to measure cholesterol levels, kidney function, and other critical health indicators.

Danaher generates revenue primarily through an initial equipment sale followed by ongoing purchases of high-margin consumables, software, and services. This razor/razor blade business model creates recurring revenue streams as customers continually need reagents, test kits, and maintenance services to keep their systems running.

The company employs a management philosophy called the Danaher Business System, which emphasizes continuous improvement, lean manufacturing principles, and strategic acquisition integration. With operations in more than 50 countries, Danaher serves customers worldwide, though North America represents its largest market at approximately 42% of sales.

4. Research Tools & Consumables

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

Danaher competes with several major life sciences and medical technology companies including Thermo Fisher Scientific (NYSE:TMO), Abbott Laboratories (NYSE:ABT), Siemens Healthineers (ETR:SHL), Roche (SWX:ROG), and Becton Dickinson (NYSE:BDX). In specific segments, it also faces competition from specialized players like Illumina (NASDAQ:ILMN) in genomics and Bio-Rad Laboratories (NYSE:BIO) in life sciences research.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $24.57 billion in revenue over the past 12 months, Danaher sports economies of scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

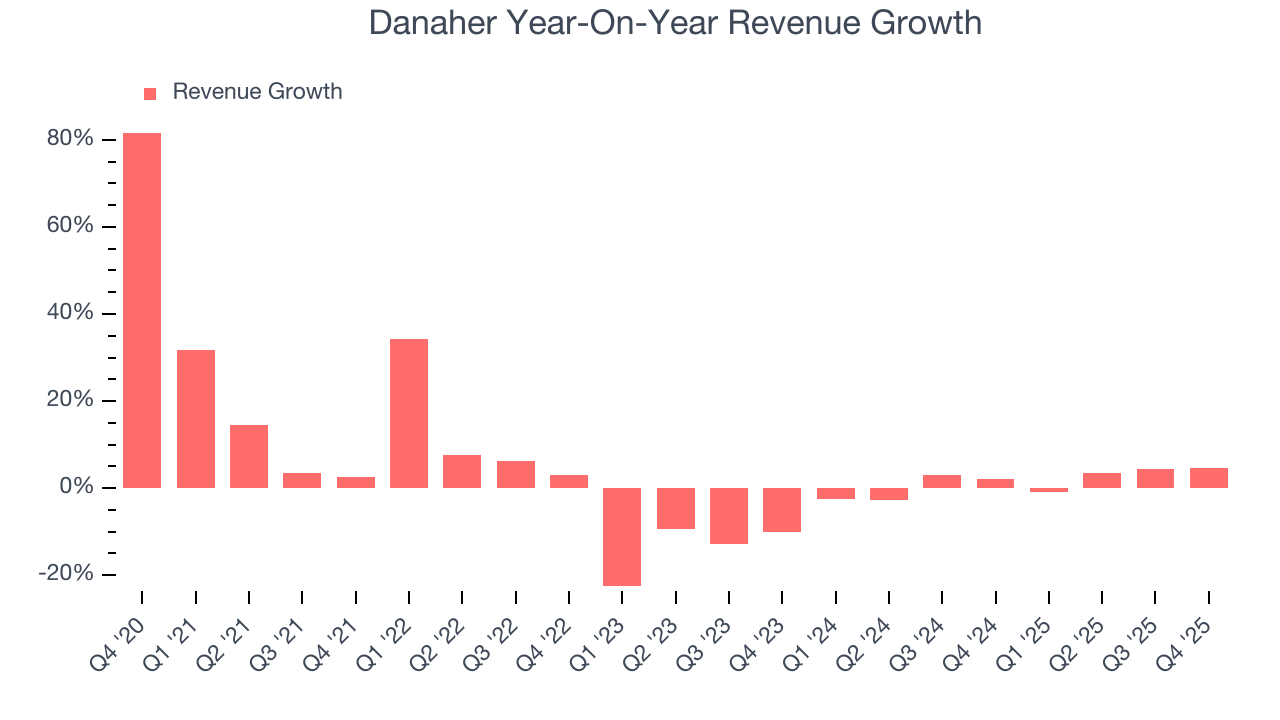

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Danaher’s sales grew at a tepid 2% compounded annual growth rate over the last five years. This was below our standards and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Danaher’s annualized revenue growth of 1.4% over the last two years aligns with its five-year trend, suggesting its demand was consistently weak.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Danaher’s organic revenue was flat. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Danaher grew its revenue by 4.6% year on year, and its $6.84 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 3.8% over the next 12 months. Although this projection suggests its newer products and services will fuel better top-line performance, it is still below average for the sector.

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Danaher has been an efficient company over the last five years. It was one of the more profitable businesses in the healthcare sector, boasting an average operating margin of 24.7%.

Analyzing the trend in its profitability, Danaher’s operating margin decreased by 11 percentage points over the last five years. The company’s two-year trajectory also shows it failed to get its profitability back to the peak as its margin fell by 3.7 percentage points. This performance was poor no matter how you look at it - it shows its expenses were rising and it couldn’t pass those costs onto its customers.

In Q4, Danaher generated an operating margin profit margin of 22%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

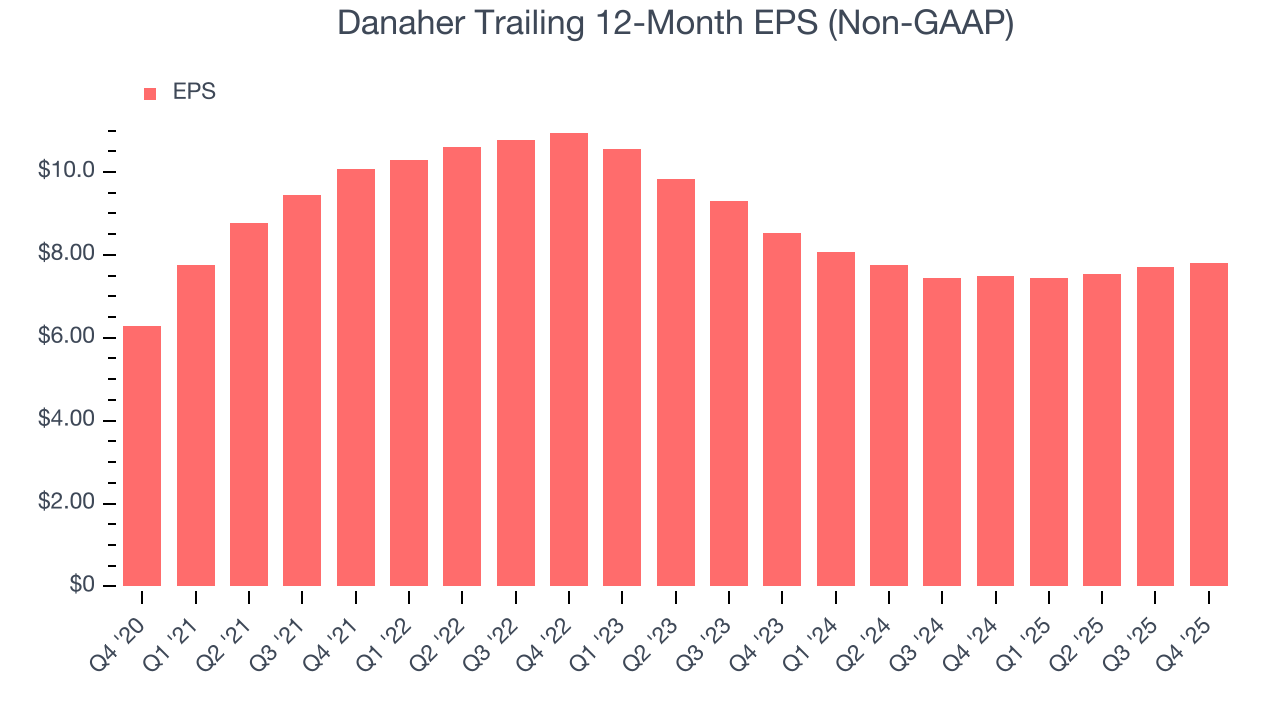

Danaher’s EPS grew at an unimpressive 4.4% compounded annual growth rate over the last five years. This performance was better than its flat revenue but doesn’t tell us much about its business quality because its operating margin didn’t improve.

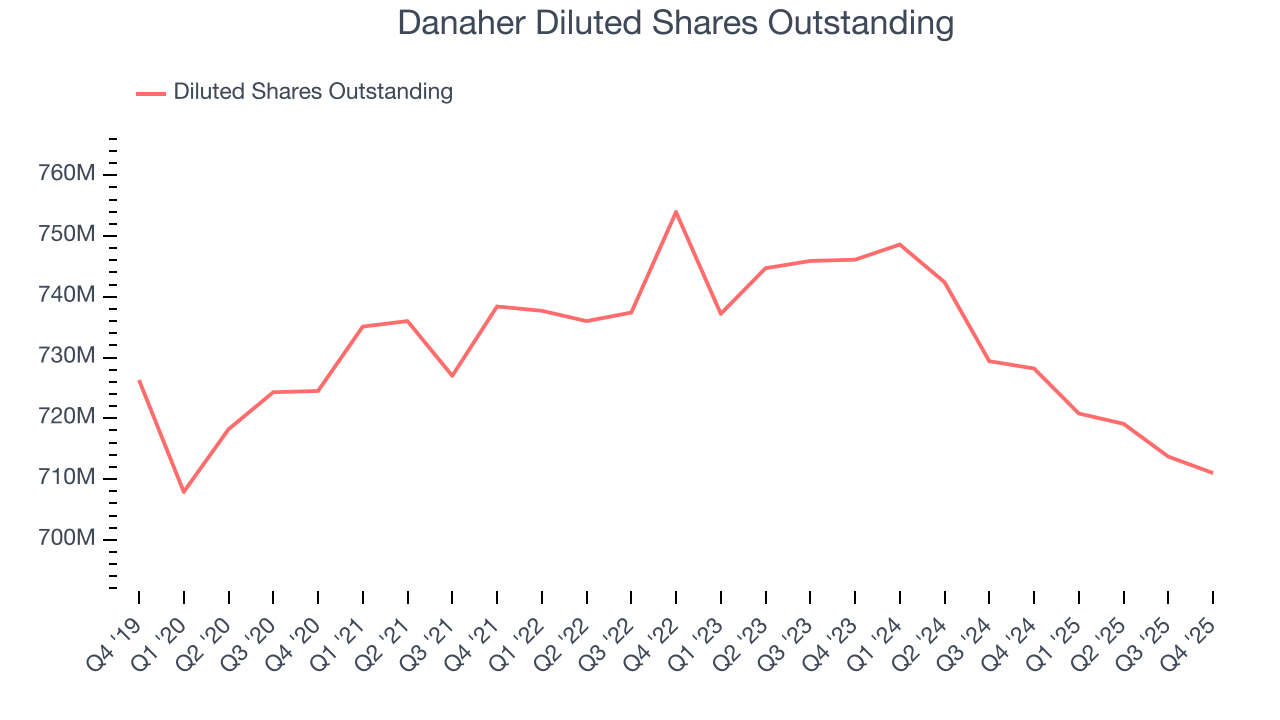

We can take a deeper look into Danaher’s earnings to better understand the drivers of its performance. A five-year view shows that Danaher has repurchased its stock, shrinking its share count by 1.9%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Danaher reported adjusted EPS of $2.23, up from $2.14 in the same quarter last year. This print beat analysts’ estimates by 1.8%. Over the next 12 months, Wall Street expects Danaher’s full-year EPS of $7.80 to grow 8.1%.

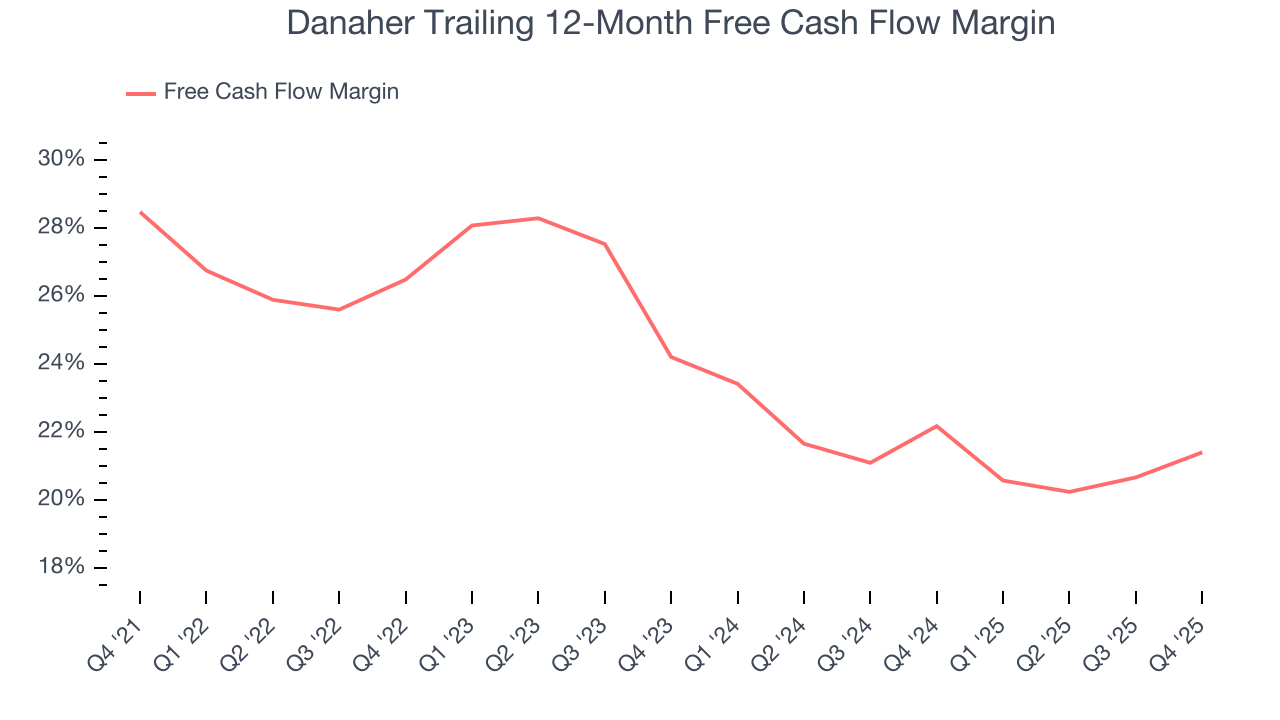

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Danaher has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 24.6% over the last five years, quite impressive for a healthcare business.

Taking a step back, we can see that Danaher’s margin dropped by 7.1 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Danaher’s free cash flow clocked in at $1.75 billion in Q4, equivalent to a 25.5% margin. This result was good as its margin was 2.5 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

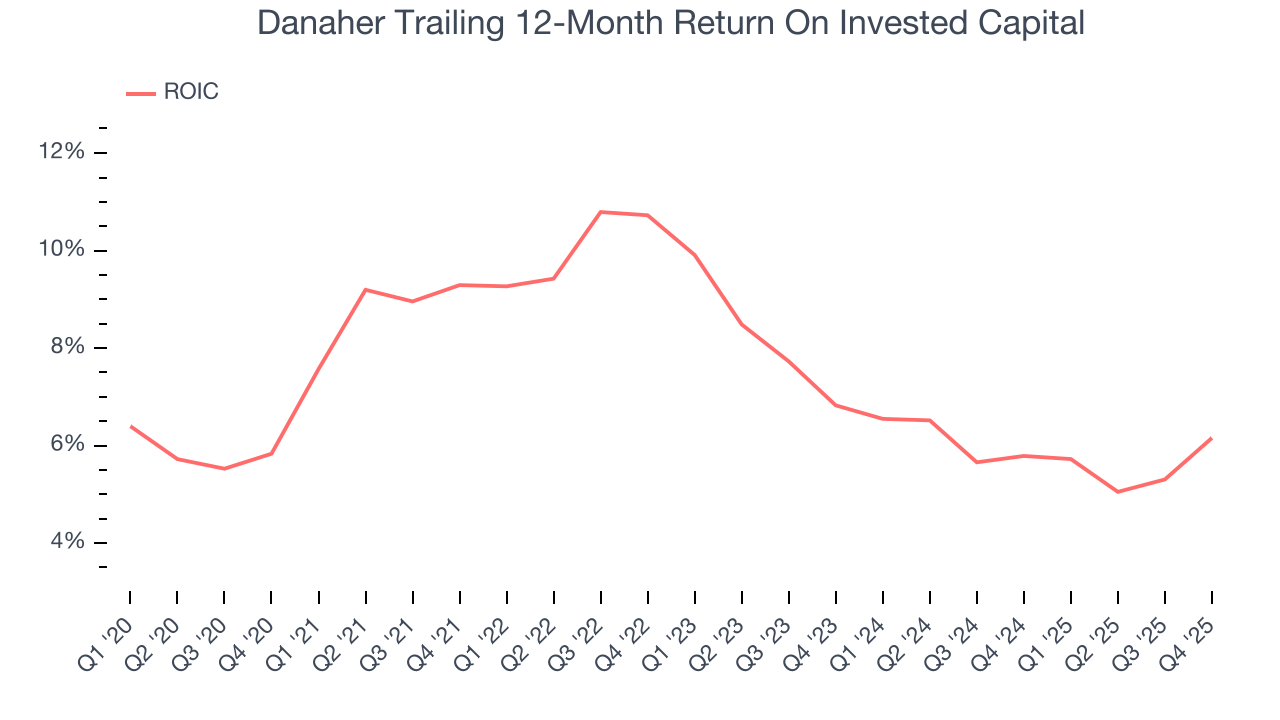

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Danaher’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 7.8%, slightly better than typical healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Danaher’s ROIC averaged 4 percentage point decreases each year. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

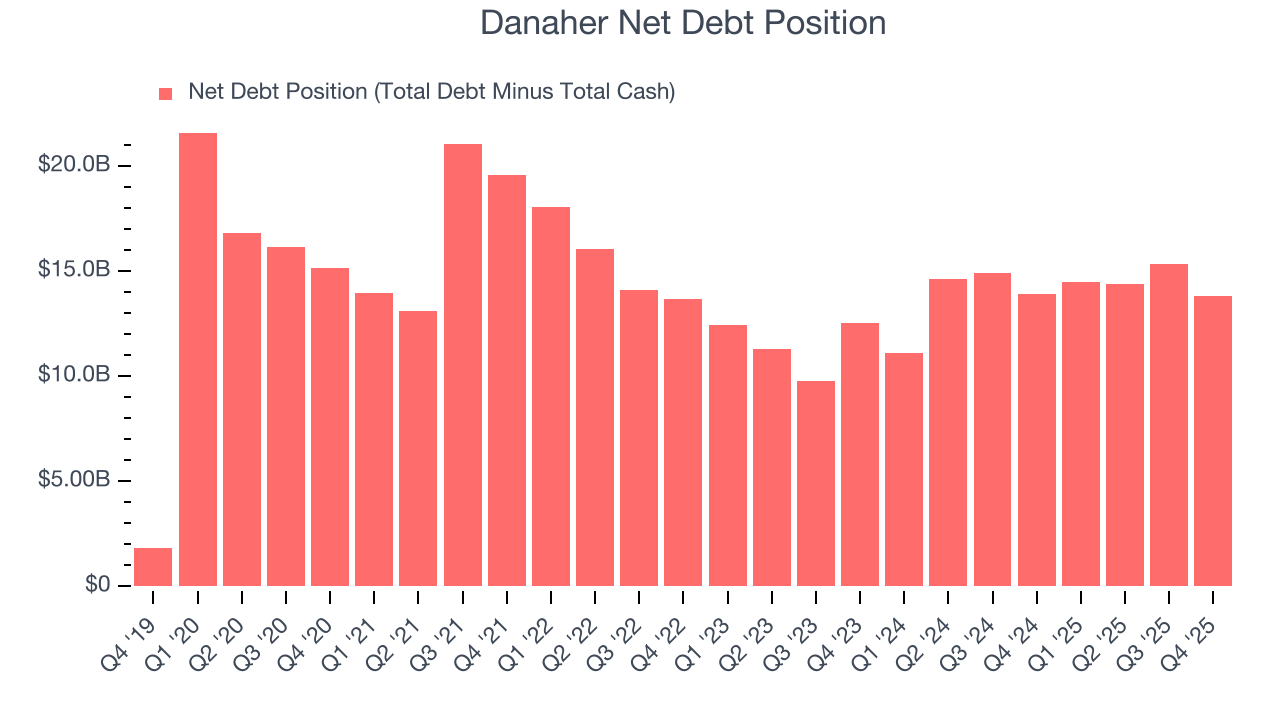

11. Balance Sheet Assessment

Danaher reported $4.62 billion of cash and $18.42 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $7.69 billion of EBITDA over the last 12 months, we view Danaher’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $151 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Danaher’s Q4 Results

Danaher roughly met analysts’ organic revenue expectations this quarter, leading to in line revenue. EPS beat slightly. Zooming out, we think this was a fine quarter without too many surprises good or bad. The stock remained flat at $238 immediately following the results.

13. Is Now The Time To Buy Danaher?

Updated: March 19, 2026 at 11:54 PM EDT

Before making an investment decision, investors should account for Danaher’s business fundamentals and valuation in addition to what happened in the latest quarter.

Danaher isn’t a terrible business, but it doesn’t pass our quality test. For starters, its revenue growth was uninspiring over the last five years. While its impressive operating margins show it has a highly efficient business model, the downside is its declining adjusted operating margin shows the business has become less efficient. On top of that, its cash profitability fell over the last five years.

Danaher’s P/E ratio based on the next 12 months is 22.8x. Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $264.91 on the company (compared to the current share price of $190.29).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.