Edgewell Personal Care (EPC)

Edgewell Personal Care faces an uphill battle. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Edgewell Personal Care Will Underperform

Boasting brands such as Banana Boat, Schick, and Skintimate, Edgewell Personal Care (NYSE:EPC) sells personal care products in the skin and sun care, shave, and feminine care categories.

- Products aren't resonating with the market as its revenue declined by 3.3% annually over the last three years

- Organic revenue growth fell short of our benchmarks over the past two years and implies it may need to improve its products, pricing, or go-to-market strategy

- High net-debt-to-EBITDA ratio of 6× could force the company to raise capital at unfavorable terms if market conditions deteriorate

Edgewell Personal Care doesn’t meet our quality standards. Better stocks can be found in the market.

Why There Are Better Opportunities Than Edgewell Personal Care

At $19.76 per share, Edgewell Personal Care trades at 8.7x forward P/E. This sure is a cheap multiple, but you get what you pay for.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Edgewell Personal Care (EPC) Research Report: Q4 CY2025 Update

Personal care company Edgewell Personal Care (NYSE:EPC) reported earnings in Q4 CY2025. Consolidated Net Sales (Inclusive of the Feminine Care Business) were $486.8 million, ahead of expectations. Its non-GAAP profit of $0.03 per share was significantly above analysts’ consensus estimates.

Correction note:

The previous version of this report estimated quarterly sales at $422.8 million. This version has been updated to reflect the Consolidated Net Sales (Inclusive of the Feminine Care Business) of $486.8 million.

The data used in the report besides Revenue, non GAAP EPS and non GAAP EBITDA are GAAP (continuing operations and exclude Femcare).

Edgewell Personal Care (EPC) Q4 CY2025 Highlights:

- Consolidated Net Sales (Inclusive of the Feminine Care Business):$486.8 million

- Adjusted EPS: $0.03 vs analyst estimates of -$0.16 (significant beat)

- Management lowered its full-year Adjusted EPS guidance to $1.90 at the midpoint, a 19.1% decrease

- EBITDA guidance for the full year is $255 million at the midpoint, below analyst estimates of $301.8 million

- Market Capitalization: $969.3 million

Company Overview

Boasting brands such as Banana Boat, Schick, and Skintimate, Edgewell Personal Care (NYSE:EPC) sells personal care products in the skin and sun care, shave, and feminine care categories.

The company was founded in 2015 as a result of a spin-off from Energizer Holdings. While Edgewell is relatively new, its portfolio is comprised of several legacy brands, some of which date back over a century.

Edgewell goes to market through three product segments: sun and skin care, shave, and feminine care. Sun and skin care focus on sunscreens, lotions, and tanning products under brands such as Hawaiian Tropic. Shave products feature razor systems and disposable blades for men and women under brands such as Edge and Shave Guard. Feminine care offers tampons and related offerings under the Playtex and o.b. Brands.

The product portfolio is broad, so the Edgewell Personal Care customer is also broad. However, these customers generally are seeking high-quality personal care products at a reasonable price. Brands matter because they are signals of reliability, so this is another area where Edgewell wins.

Edgewell products enjoy broad distribution. Most supermarkets, drugstores and pharmacies, big-box retailers, and convenience stores carry one or more of the company’s brands. Because many of these brands are leaders in their categories, they also enjoy advantaged shelf placement as well.

4. Personal Care

While personal care products products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Competitors in the personal care market include Proctor & Gamble (NYSE:PG), Unilever (LSE:ULVR), and Kimberly-Clark (NYSE:KMB).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

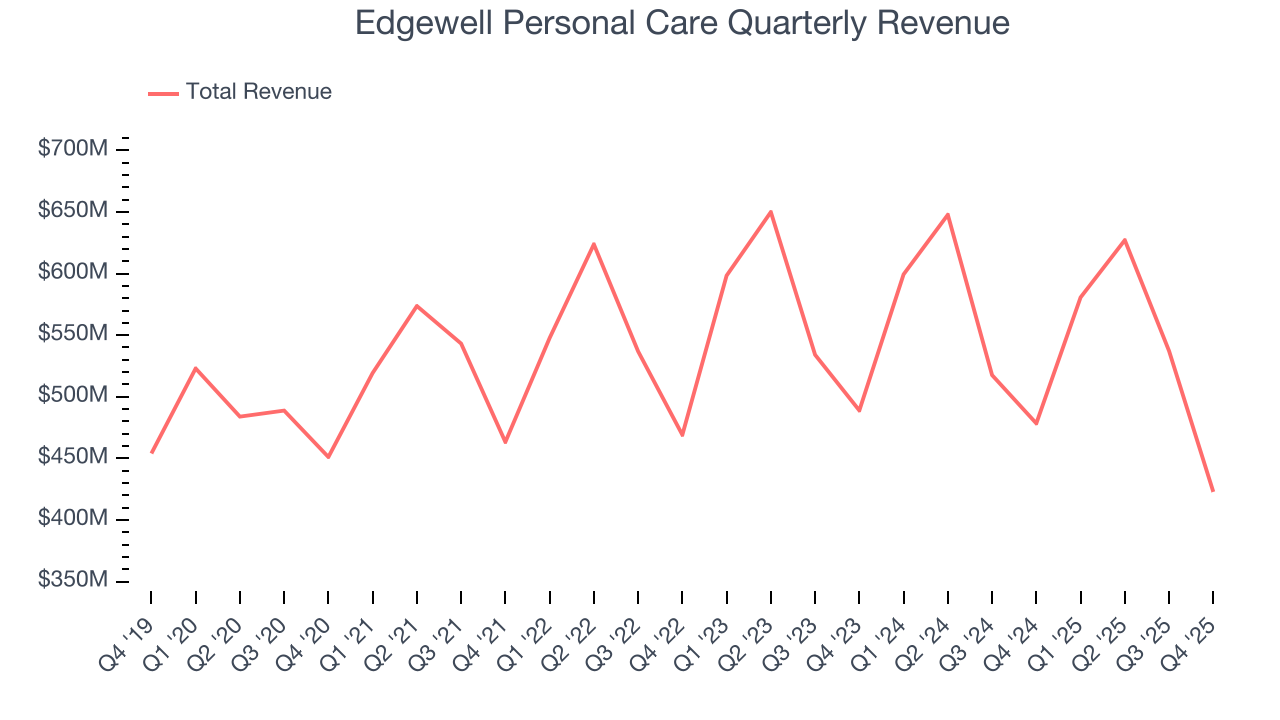

With $2.17 billion in revenue over the past 12 months, Edgewell Personal Care is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Edgewell Personal Care struggled to increase demand as its $2.17 billion of sales for the trailing 12 months was close to its revenue three years ago. This shows demand was soft, a poor baseline for our analysis.

Sales Consolidated Net Sales (Inclusive of the Feminine Care Business) were $486.8 million, ahead of expectations.

Looking ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months. Although this projection indicates its newer products will fuel better top-line performance, it is still below average for the sector.

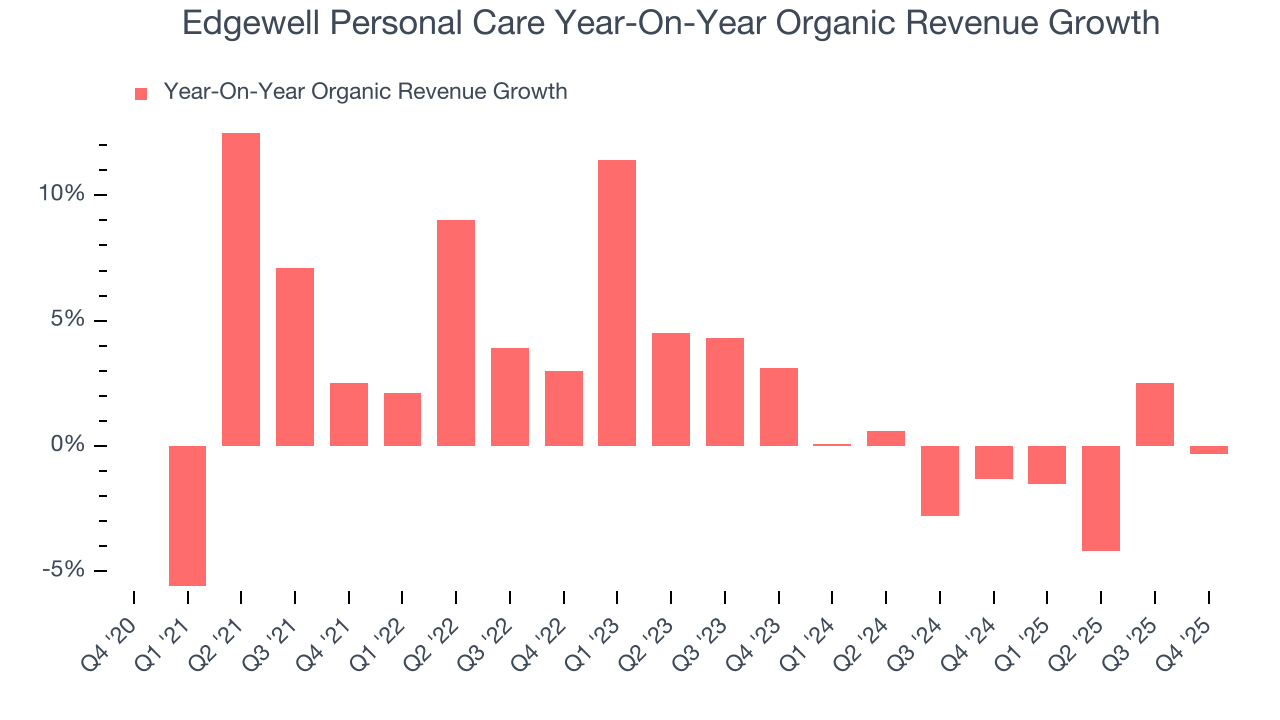

6. Organic Revenue Growth

When analyzing revenue growth, we care most about organic revenue growth. This metric captures a business’s performance excluding one-time events such as mergers, acquisitions, and divestitures as well as foreign currency fluctuations.

The demand for Edgewell Personal Care’s products has barely risen over the last eight quarters. On average, the company’s organic sales have been flat.

In the latest quarter, Edgewell Personal Care’s year on year organic sales were flat. This performance was more or less in line with its historical levels.

7. Gross Margin & Pricing Power

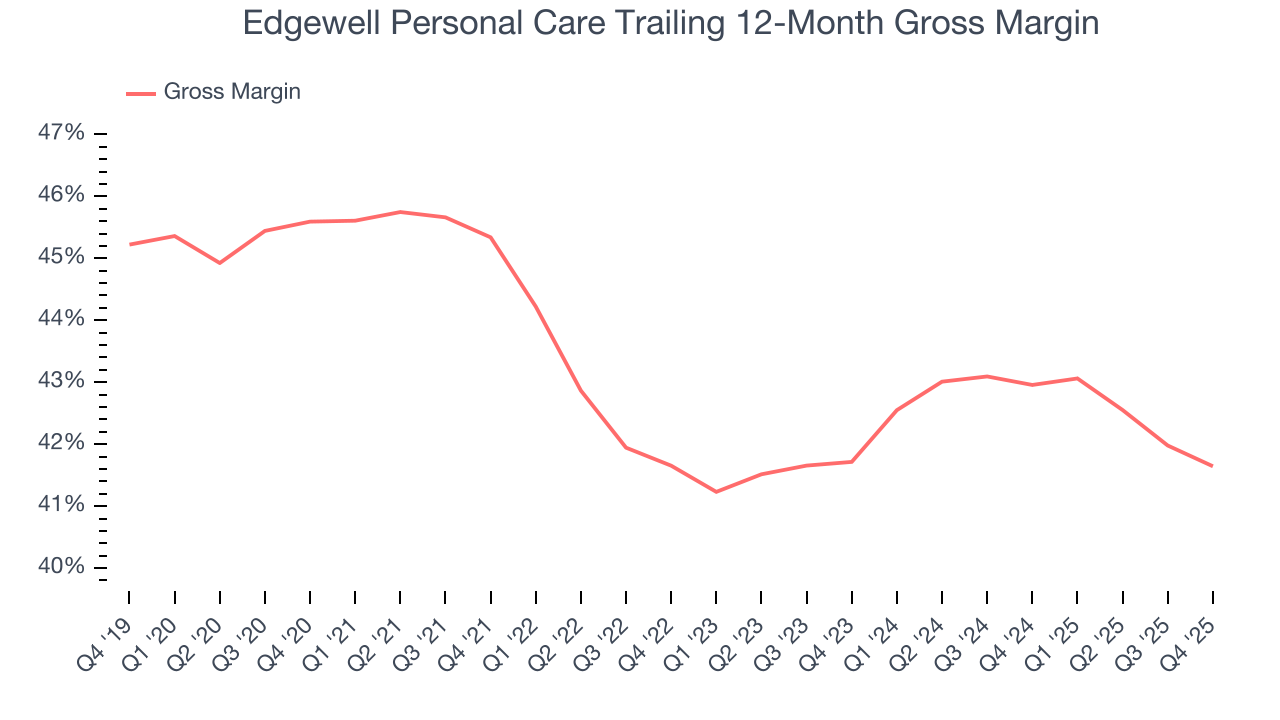

Edgewell Personal Care has great unit economics for a consumer staples company, giving it ample room to invest in areas such as marketing and talent to grow its brand. As you can see below, it averaged an excellent 42.3% gross margin over the last two years. That means for every $100 in revenue, only $57.69 went towards paying for raw materials, production of goods, transportation, and distribution.

This quarter, Edgewell Personal Care’s gross profit margin was 38.1%, down 2 percentage points year on year. Edgewell Personal Care’s full-year margin has also been trending down over the past 12 months, decreasing by 1.3 percentage points. If this move continues, it could suggest a more competitive environment with some pressure to lower prices and higher input costs (such as raw materials and manufacturing expenses).

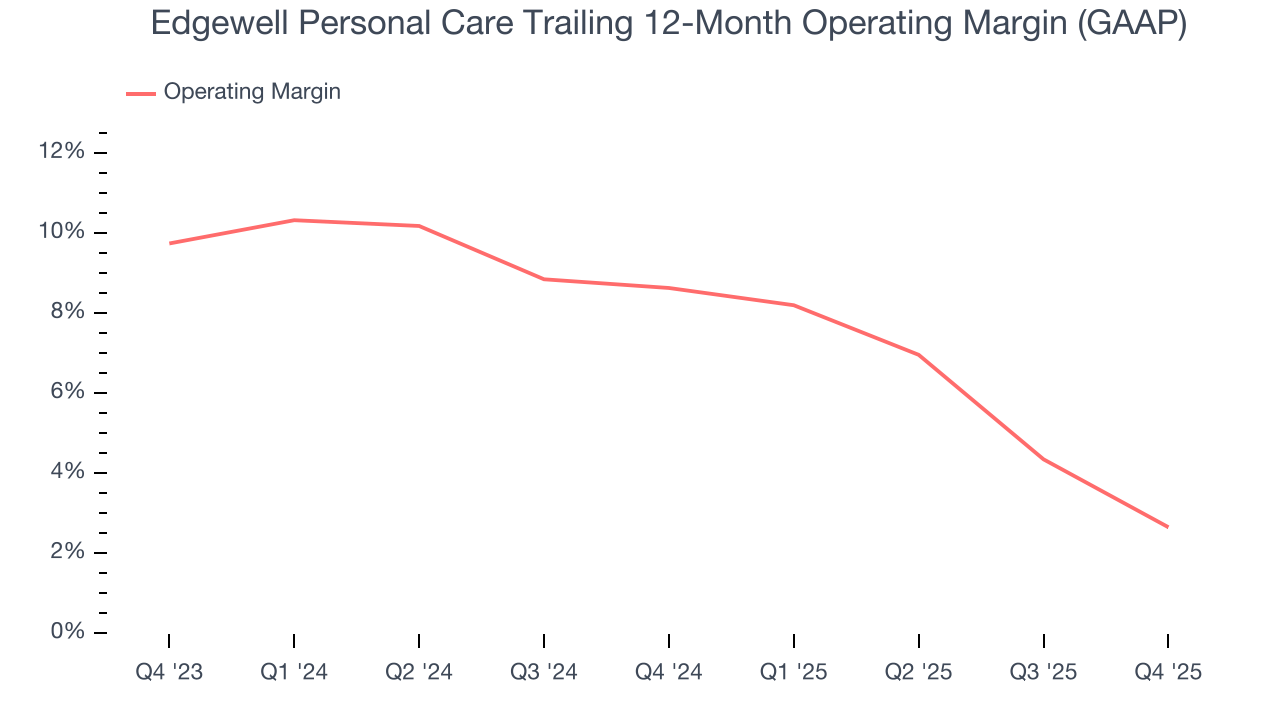

8. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Edgewell Personal Care was profitable over the last two years but held back by its large cost base. Its average operating margin of 5.7% was weak for a consumer staples business. This result is surprising given its high gross margin as a starting point.

Looking at the trend in its profitability, Edgewell Personal Care’s operating margin decreased by 6 percentage points over the last year. Edgewell Personal Care’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Edgewell Personal Care generated an operating margin profit margin of negative 4.5%, down 8.7 percentage points year on year. Since Edgewell Personal Care’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, and administrative overhead increased.

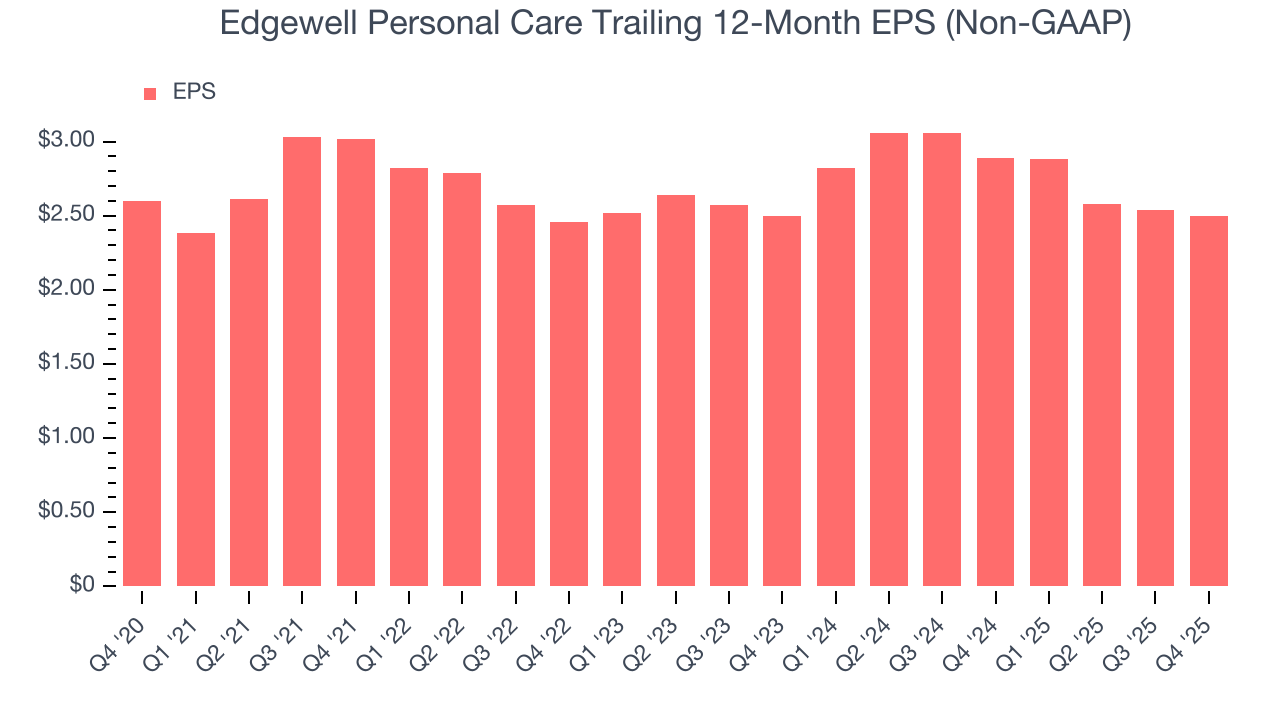

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Edgewell Personal Care’s EPS was flat over the last three years, just like its revenue. This performance was underwhelming across the board.

In Q4, Edgewell Personal Care reported adjusted EPS of $0.03, down from $0.07 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Edgewell Personal Care’s full-year EPS of $2.50 to shrink by 5.1%.

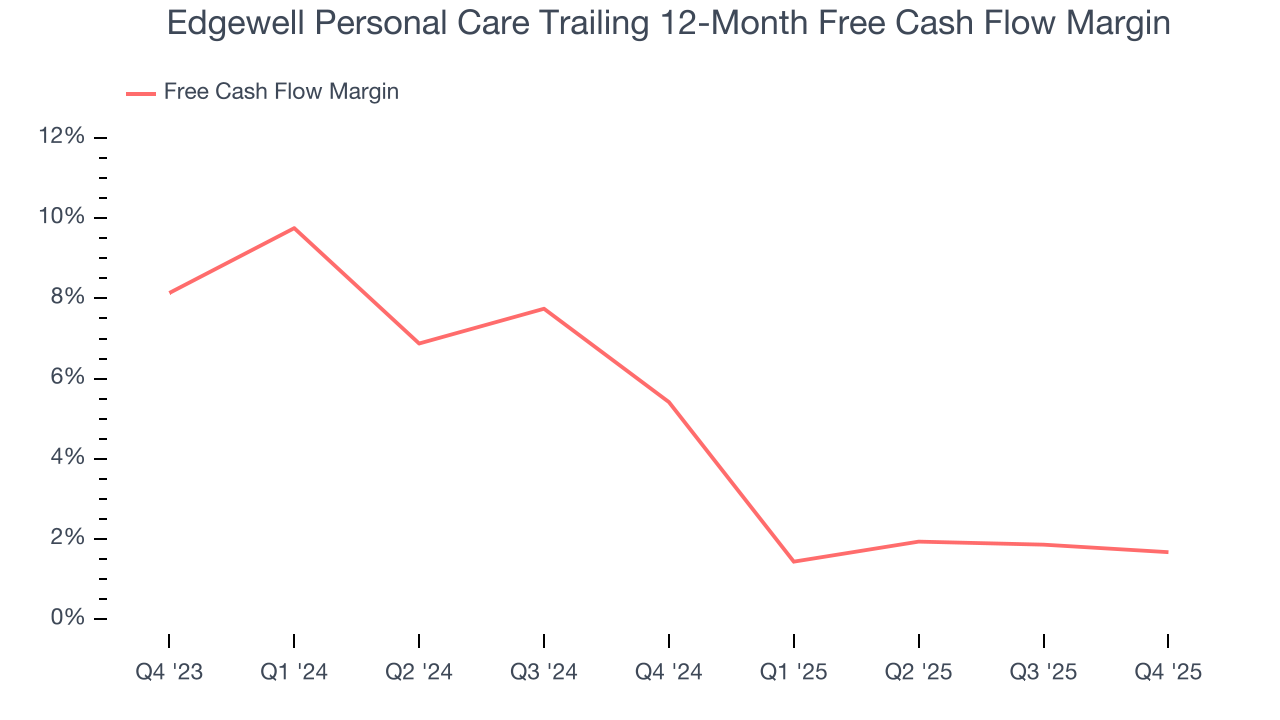

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Edgewell Personal Care has shown mediocre cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 3.6%, subpar for a consumer staples business.

Taking a step back, we can see that Edgewell Personal Care’s margin dropped by 3.7 percentage points over the last year. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s in the middle of an investment cycle.

Edgewell Personal Care burned through $137.5 million of cash in Q4, equivalent to a negative 32.5% margin. The company’s cash burn was similar to its $132.4 million of lost cash in the same quarter last year. These numbers deviate from its longer-term margin, indicating it is a seasonal business that must build up inventory during certain quarters.

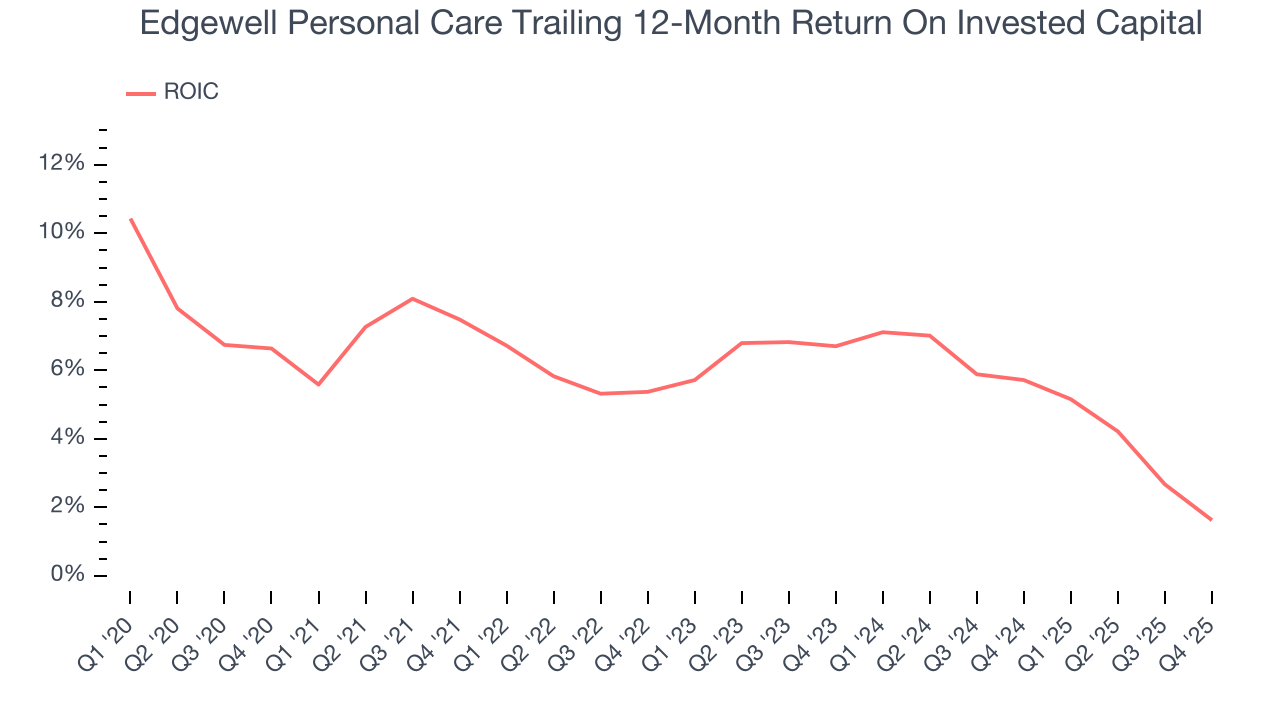

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Edgewell Personal Care historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 5.4%, somewhat low compared to the best consumer staples companies that consistently pump out 20%+.

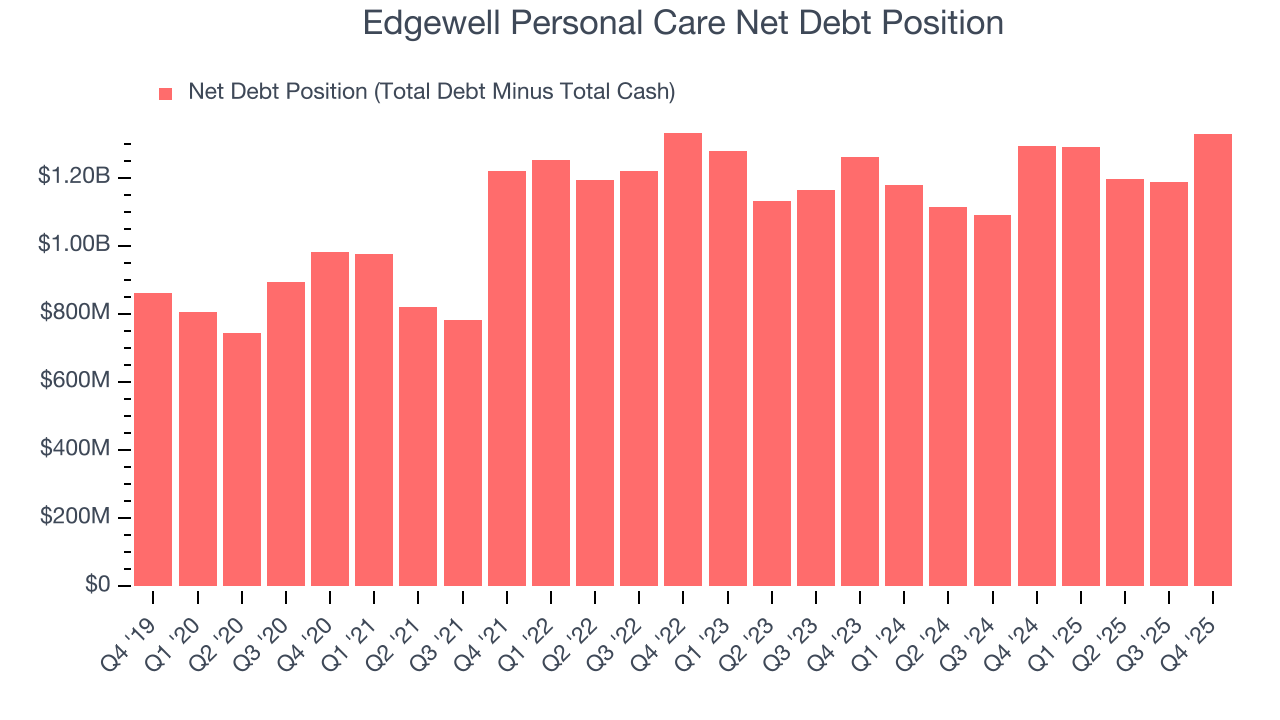

12. Balance Sheet Assessment

Edgewell Personal Care reported $223.3 million of cash and $1.55 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $284.2 million of EBITDA over the last 12 months, we view Edgewell Personal Care’s 4.7× net-debt-to-EBITDA ratio as safe. We also see its $54.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Edgewell Personal Care’s Q4 Results

It was good to see Edgewell Personal Care beat analysts’ EPS expectations this quarter. Overall, this was a mixed quarter. The stock traded up 2.8% to $21.34 immediately following the results.

14. Is Now The Time To Buy Edgewell Personal Care?

Updated: March 16, 2026 at 10:54 PM EDT

Before deciding whether to buy Edgewell Personal Care or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

Edgewell Personal Care falls short of our quality standards. To begin with, its revenue has declined over the last three years. While its gross margins indicate a healthy starting point for the overall profitability of the business, the downside is its declining operating margin shows the business has become less efficient. On top of that, its projected EPS for the next year is lacking.

Edgewell Personal Care’s P/E ratio based on the next 12 months is 9.2x. While this valuation is optically cheap, the potential downside is huge given its shaky fundamentals. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $24.33 on the company (compared to the current share price of $20.23).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.