Evolent Health (EVH)

We’re cautious of Evolent Health. Not only has its sales growth been weak but also its negative returns on capital show it destroyed value.― StockStory Analyst Team

1. News

2. Summary

Why We Think Evolent Health Will Underperform

Founded in 2011 to transform how healthcare is delivered to patients with complex needs, Evolent Health (NYSE:EVH) provides specialty care management services and technology solutions that help health plans and providers deliver better care for patients with complex conditions.

- Push for growth has led to negative returns on capital, signaling value destruction, and its shrinking returns suggest its past profit sources are losing steam

- Smaller revenue base of $1.88 billion means it hasn’t achieved the economies of scale that some industry juggernauts enjoy

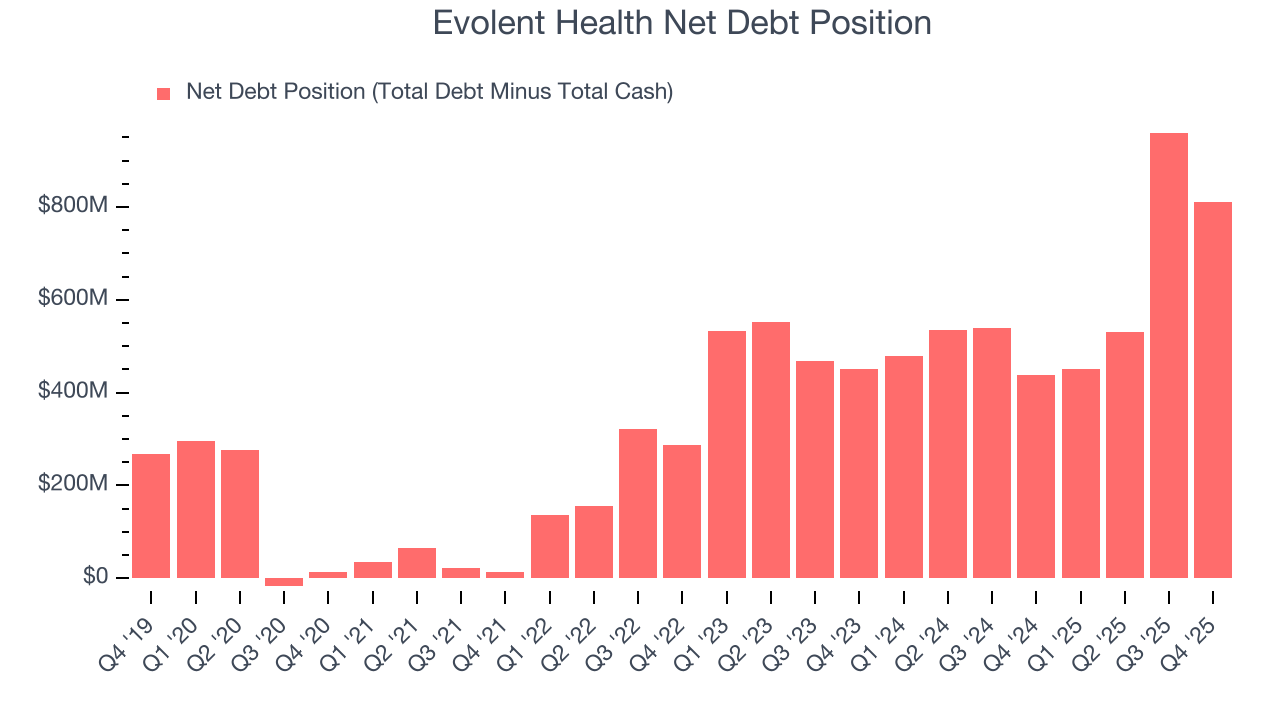

- High net-debt-to-EBITDA ratio of 6× could force the company to raise capital at unfavorable terms if market conditions deteriorate

Evolent Health’s quality is inadequate. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Evolent Health

At $2.54 per share, Evolent Health trades at 15.2x forward P/E. This multiple is lower than most healthcare companies, but for good reason.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Evolent Health (EVH) Research Report: Q4 CY2025 Update

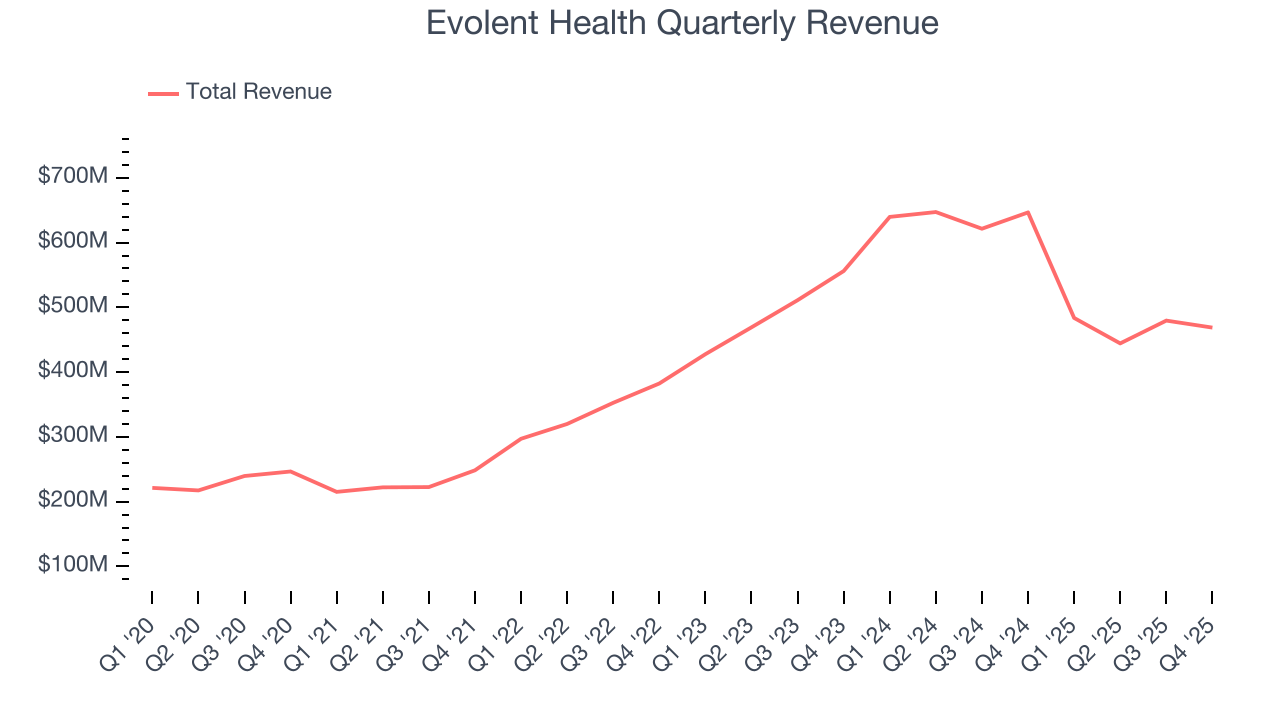

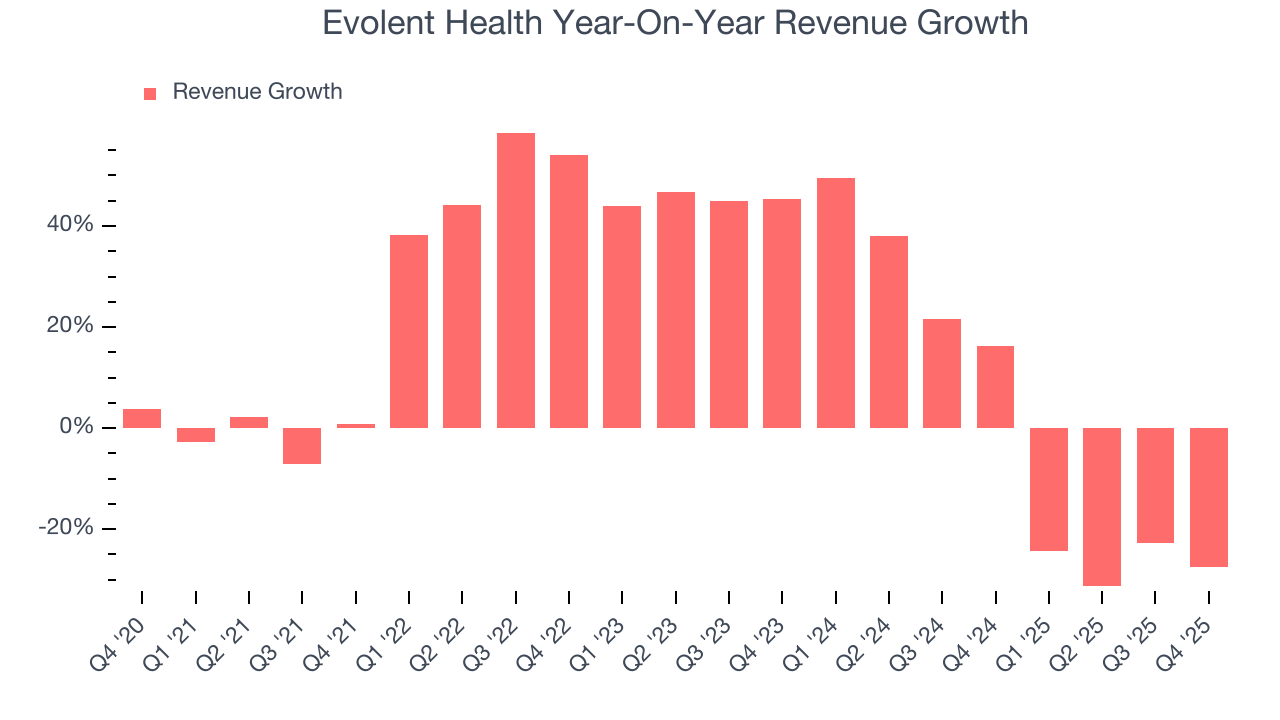

Healthcare solutions company Evolent Health (NYSE:EVH) met Wall Street’s revenue expectations in Q4 CY2025, but sales fell by 27.5% year on year to $468.7 million. The company’s full-year revenue guidance of $2.5 billion at the midpoint came in 4.9% above analysts’ estimates. Its non-GAAP profit of $0.08 per share was 62.7% above analysts’ consensus estimates.

Evolent Health (EVH) Q4 CY2025 Highlights:

- Revenue: $468.7 million vs analyst estimates of $469 million (27.5% year-on-year decline, in line)

- Adjusted EPS: $0.08 vs analyst estimates of $0.05 (62.7% beat)

- Adjusted EBITDA: $37.79 million vs analyst estimates of $35.71 million (8.1% margin, 5.8% beat)

- EBITDA guidance for the upcoming financial year 2026 is $125 million at the midpoint, below analyst estimates of $151.6 million

- Operating Margin: -87.1%, down from -2.9% in the same quarter last year

- Free Cash Flow was $41.04 million, up from -$32.38 million in the same quarter last year

- Sales Volumes rose 6% year on year (4.2% in the same quarter last year)

- Market Capitalization: $309.1 million

Company Overview

Founded in 2011 to transform how healthcare is delivered to patients with complex needs, Evolent Health (NYSE:EVH) provides specialty care management services and technology solutions that help health plans and providers deliver better care for patients with complex conditions.

Evolent Health focuses on three core areas: specialty care management, total cost of care management, and administrative services. The company's specialty care management services target high-cost, complex conditions like cancer, cardiovascular disease, and musculoskeletal disorders. These services include building networks of high-performing providers, designing evidence-based clinical pathways, and deploying proprietary technology to guide treatment decisions.

For specialty care management, Evolent uses its CarePro platform to provide clinical decision support and ensure providers adhere to best-practice treatment protocols. This approach aims to improve patient outcomes while reducing unnecessary costs for health plans and risk-bearing entities.

The company's total cost of care management solution helps healthcare providers succeed under value-based contracts, where they assume financial responsibility for patient populations. Evolent identifies high-risk patients and coordinates targeted interventions through primary care physicians to prevent costly complications or hospitalizations.

On the administrative side, Evolent offers its Identifi platform, which aggregates and analyzes healthcare data to manage care workflows and engage patients. The platform provides services like health plan administration, pharmacy benefit management, risk management, and analytics.

A health plan might engage Evolent to manage its cancer patients by implementing evidence-based treatment protocols, connecting patients with high-performing oncologists, and using technology to track outcomes. This approach can reduce unnecessary treatments while ensuring patients receive appropriate care.

Evolent generates revenue through service contracts with health plans, provider organizations, and other risk-bearing entities. The company has expanded its capabilities through strategic acquisitions, including New Century Health (oncology and cardiovascular care), IPG (musculoskeletal management), and NIA (radiology and genetics management).

4. Healthcare Technology for Providers

The healthcare technology sector provides software and data analytics to help hospitals and clinics streamline operations and improve patient outcomes, often through value-based care models. Future growth is expected as providers prioritize digital transformation to manage rising costs and patient demands. Tailwinds include the adoption of AI-driven tools and government incentives for digitization. There challenges as well, including long sales cycles and slow adoption by providers, who may be resistance to change. Tightening hospital budgets and cybersecurity threats are additional risks that could slow adoption.

Evolent Health competes with other healthcare management and technology companies such as Optum (part of UnitedHealth Group, NYSE:UNH), Signify Health (acquired by CVS Health, NYSE:CVS), and Evernorth (part of Cigna Group, NYSE:CI), as well as specialized care management firms like Magellan Health and AIM Specialty Health.

5. Revenue Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With just $1.88 billion in revenue over the past 12 months, Evolent Health is a small company in an industry where scale matters. This makes it difficult to build trust with customers because healthcare is heavily regulated, complex, and resource-intensive.

6. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Evolent Health grew its sales at a solid 15.2% compounded annual growth rate. Its growth beat the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Evolent Health’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 2.3% over the last two years.

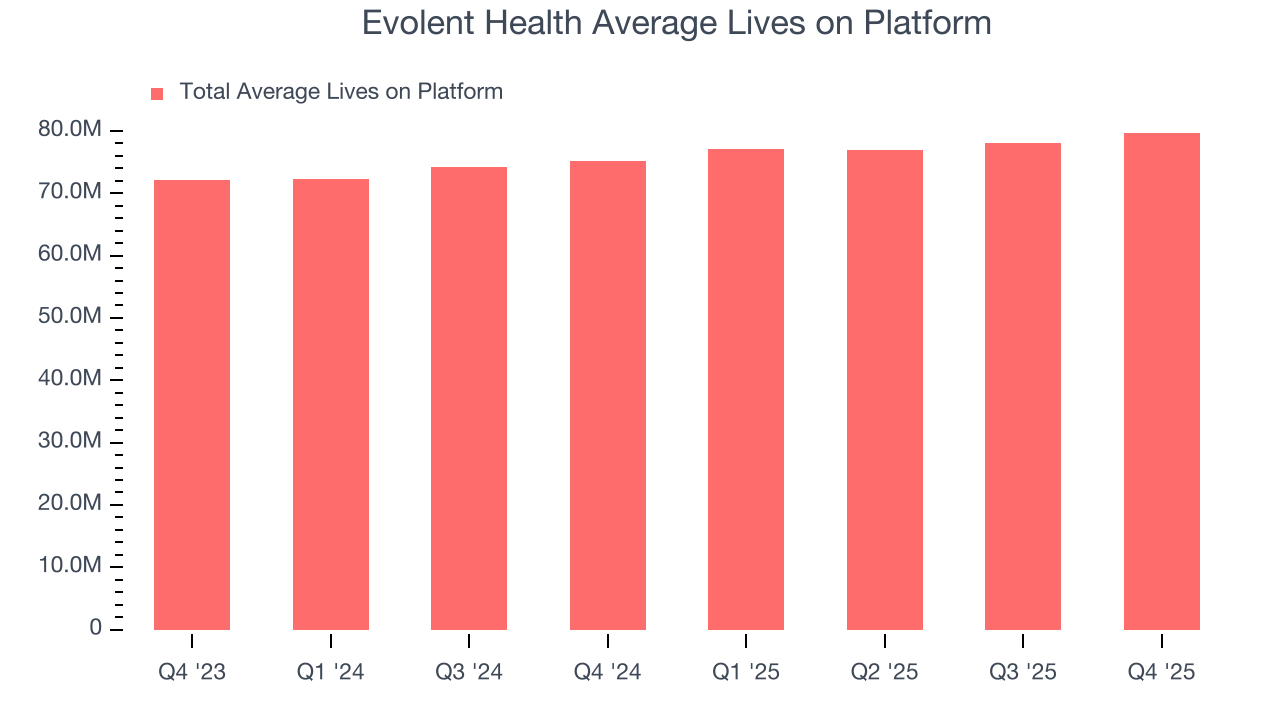

We can dig further into the company’s revenue dynamics by analyzing its number of average lives on platform, which reached 79.68 million in the latest quarter. Over the last two years, Evolent Health’s average lives on platform averaged 5.5% year-on-year growth. Because this number is better than its revenue growth, we can see the company’s average selling price decreased.

This quarter, Evolent Health reported a rather uninspiring 27.5% year-on-year revenue decline to $468.7 million of revenue, in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 27.8% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and implies its newer products and services will fuel better top-line performance.

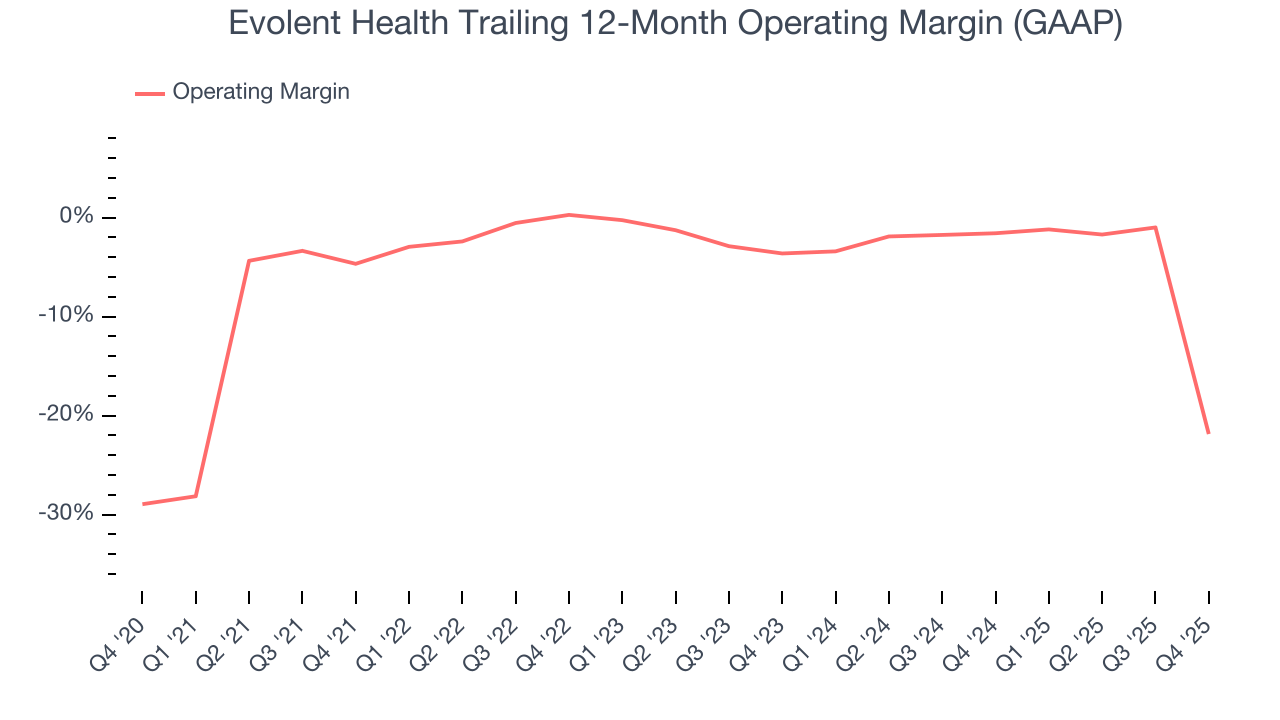

7. Operating Margin

Evolent Health’s high expenses have contributed to an average operating margin of negative 6.5% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

Analyzing the trend in its profitability, Evolent Health’s operating margin decreased by 17.2 percentage points over the last five years. This performance was caused by more recent speed bumps as the company’s margin fell by 18.2 percentage points on a two-year basis. We’re disappointed in these results because it shows its expenses were rising and it couldn’t pass those costs onto its customers.

This quarter, Evolent Health generated a negative 87.1% operating margin.

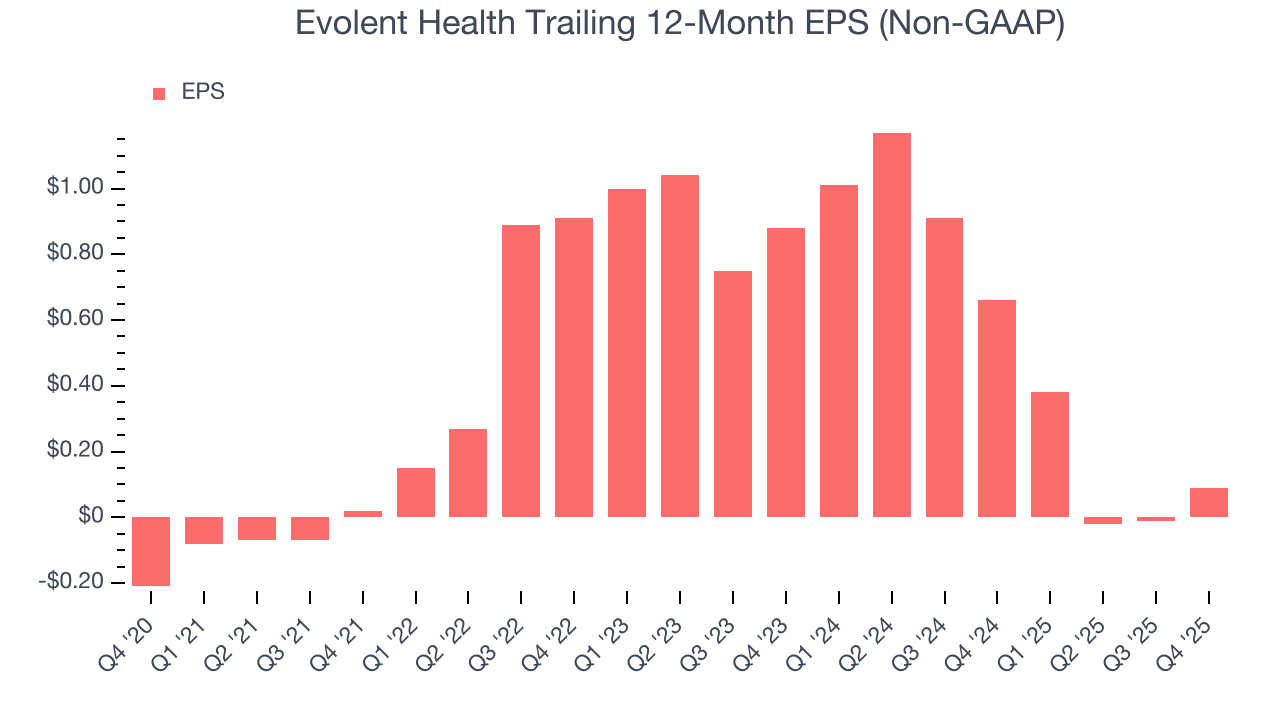

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Evolent Health’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q4, Evolent Health reported adjusted EPS of $0.08, up from negative $0.02 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Evolent Health’s full-year EPS of $0.09 to grow 173%.

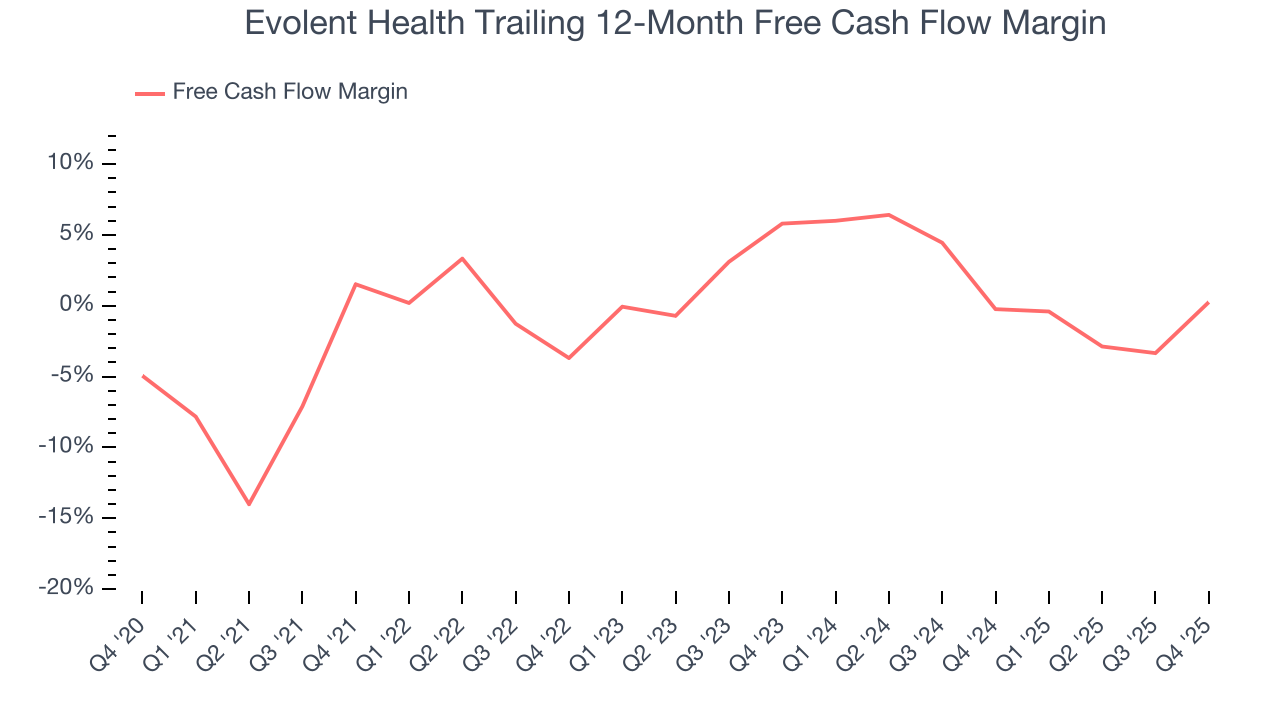

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Evolent Health broke even from a free cash flow perspective over the last five years, giving the company limited opportunities to return capital to shareholders.

Taking a step back, we can see that Evolent Health’s margin dropped by 1.3 percentage points during that time. Almost any movement in the wrong direction is undesirable because of its already low cash conversion. If the trend continues, it could signal it’s in the middle of an investment cycle.

Evolent Health’s free cash flow clocked in at $41.04 million in Q4, equivalent to a 8.8% margin. Its cash flow turned positive after being negative in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

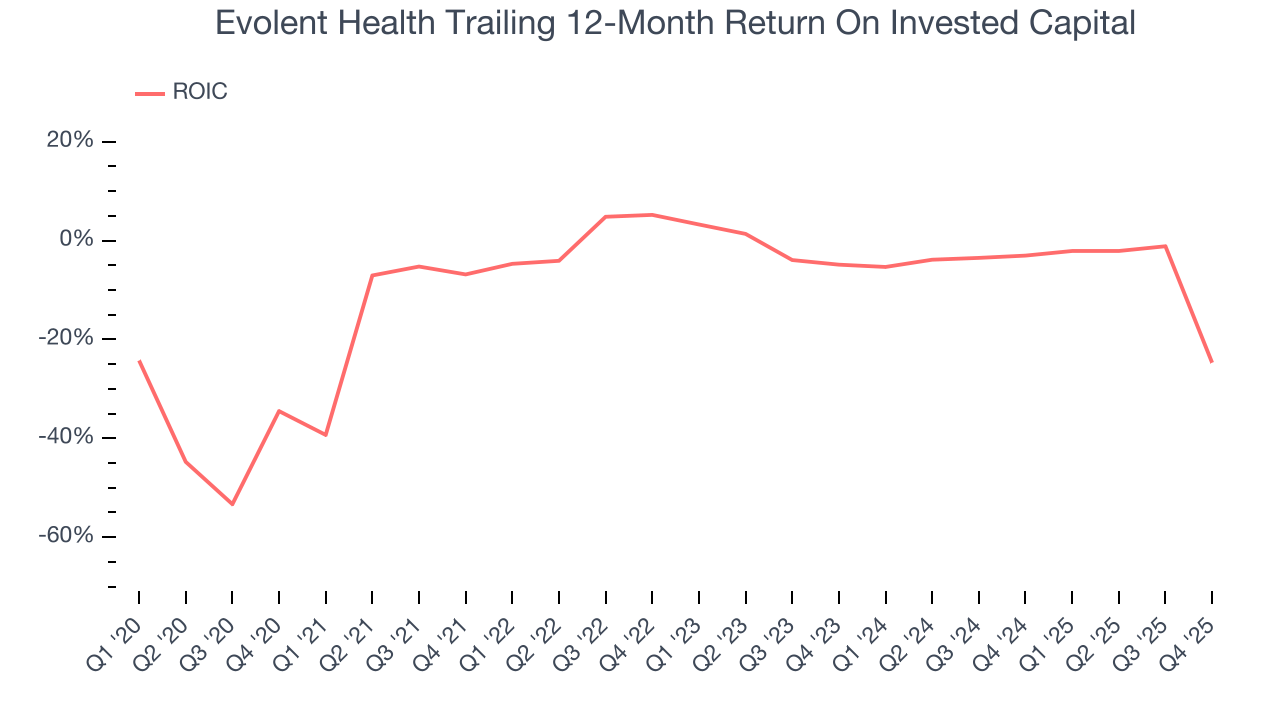

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Evolent Health’s five-year average ROIC was negative 6.8%, meaning management lost money while trying to expand the business. Its returns were among the worst in the healthcare sector.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Evolent Health’s ROIC has unfortunately decreased significantly. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Evolent Health’s $989.7 million of debt exceeds the $178 million of cash on its balance sheet. Furthermore, its 5× net-debt-to-EBITDA ratio (based on its EBITDA of $151.2 million over the last 12 months) shows the company is overleveraged.

At this level of debt, incremental borrowing becomes increasingly expensive and credit agencies could downgrade the company’s rating if profitability falls. Evolent Health could also be backed into a corner if the market turns unexpectedly – a situation we seek to avoid as investors in high-quality companies.

We hope Evolent Health can improve its balance sheet and remain cautious until it increases its profitability or pays down its debt.

12. Key Takeaways from Evolent Health’s Q4 Results

It was good to see Evolent Health beat analysts’ EPS expectations this quarter. We were also glad its full-year revenue guidance trumped Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed. Overall, we think this was a mixed quarter. The stock remained flat at $2.53 immediately after reporting.

13. Is Now The Time To Buy Evolent Health?

Updated: March 24, 2026 at 12:03 AM EDT

Are you wondering whether to buy Evolent Health or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Evolent Health isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was solid over the last five years and is expected to accelerate over the next 12 months, its relatively low ROIC suggests management has struggled to find compelling investment opportunities. And while the company’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders, the downside is its diminishing returns show management's prior bets haven't worked out.

Evolent Health’s P/E ratio based on the next 12 months is 15.2x. Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are more exciting stocks to buy at the moment.

Wall Street analysts have a consensus one-year price target of $5.18 on the company (compared to the current share price of $2.54).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.