FactSet (FDS)

FactSet doesn’t impress us. It’s recently struggled to grow its revenue, a worrying sign for investors seeking high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why FactSet Is Not Exciting

Founded in 1978 when financial data was still primarily delivered through paper reports, FactSet (NYSE:FDS) provides financial data, analytics, and technology solutions that investment professionals use to research, analyze, and manage their portfolios.

- Earnings per share lagged its peers over the last five years as they only grew by 8.9% annually

- A bright spot is that its industry-leading 32.1% return on equity demonstrates management’s skill in finding high-return investments

FactSet’s quality is insufficient. You should search for better opportunities.

Why There Are Better Opportunities Than FactSet

At $211 per share, FactSet trades at 11.7x forward P/E. Yes, this valuation multiple is lower than that of other financials peers, but we’ll remind you that you often get what you pay for.

It’s better to pay up for high-quality businesses with higher long-term earnings potential rather than to buy lower-quality stocks because they appear cheap. These challenged businesses often don’t re-rate, a phenomenon known as a “value trap”.

3. FactSet (FDS) Research Report: Q4 CY2025 Update

Financial data provider FactSet (NYSE:FDS) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 6.9% year on year to $607.6 million. The company expects the full year’s revenue to be around $2.44 billion, close to analysts’ estimates. Its non-GAAP profit of $4.51 per share was 3.5% above analysts’ consensus estimates.

FactSet (FDS) Q4 CY2025 Highlights:

- Revenue: $607.6 million vs analyst estimates of $600 million (6.9% year-on-year growth, 1.3% beat)

- Pre-tax Profit: $190.1 million (31.3% margin)

- Adjusted EPS: $4.51 vs analyst estimates of $4.36 (3.5% beat)

- The company reconfirmed its revenue guidance for the full year of $2.44 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $17.25 at the midpoint

- Market Capitalization: $11.08 billion

Company Overview

Founded in 1978 when financial data was still primarily delivered through paper reports, FactSet (NYSE:FDS) provides financial data, analytics, and technology solutions that investment professionals use to research, analyze, and manage their portfolios.

FactSet operates through a subscription-based model, delivering its services via workstations, data feeds, APIs, and cloud-based solutions. The company's platform integrates vast amounts of market data with sophisticated analytical tools, enabling clients to conduct investment research, construct portfolios, measure performance, manage risk, and generate reports.

The company serves a diverse client base that includes institutional asset managers, investment bankers, wealth managers, hedge funds, private equity firms, and corporate users. For instance, a portfolio manager at an asset management firm might use FactSet to screen for investment opportunities based on specific criteria, analyze a company's financial performance against its peers, and monitor portfolio risk exposures—all within a single platform.

FactSet organizes its business into three geographic segments: Americas (accounting for about two-thirds of revenue), EMEA (Europe, Middle East, and Africa), and Asia Pacific. Its offerings are tailored to different firm types, including Institutional Buyside (serving asset managers and hedge funds), Dealmakers (serving investment bankers and corporate users), Wealth (serving financial advisors), and Partnerships and CUSIP Global Services (providing security identifiers and data solutions).

Beyond its core data and analytics, FactSet differentiates itself through managed services that function as extensions of clients' internal teams. The company continues to expand its capabilities through investments in artificial intelligence, which powers features like automated portfolio commentary generation and natural language data queries.

4. Financial Exchanges & Data

Financial exchanges and data providers operate trading platforms and sell market information. They enjoy relatively stable revenue from trading fees and subscriptions, increasing demand for data analytics, and expansion opportunities in emerging markets. Challenges include regulatory oversight of market structure, competition from alternative trading venues, and substantial technology investments needed to maintain low-latency trading infrastructure and data security.

FactSet's primary competitors include Bloomberg L.P., S&P Global Market Intelligence, and London Stock Exchange Group's Data & Analytics division. Other competitors in the financial data and analytics space include BlackRock's Aladdin platform, MSCI Inc., and Morningstar Inc.

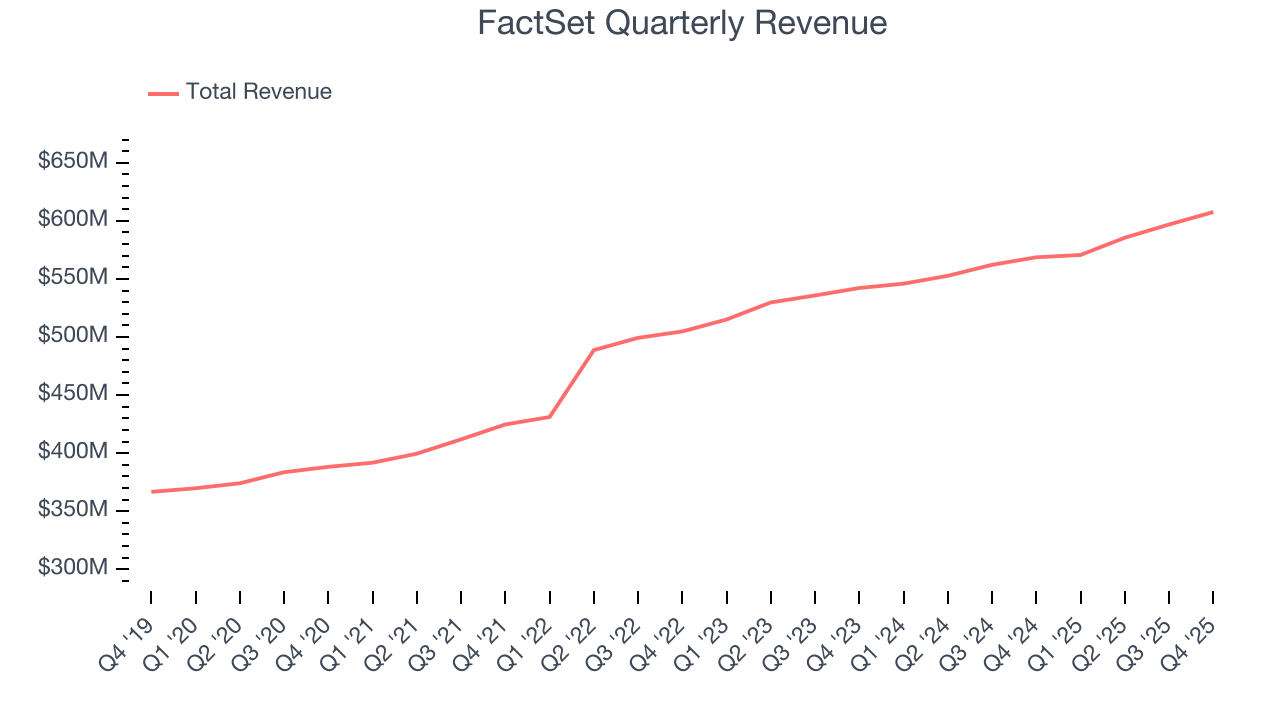

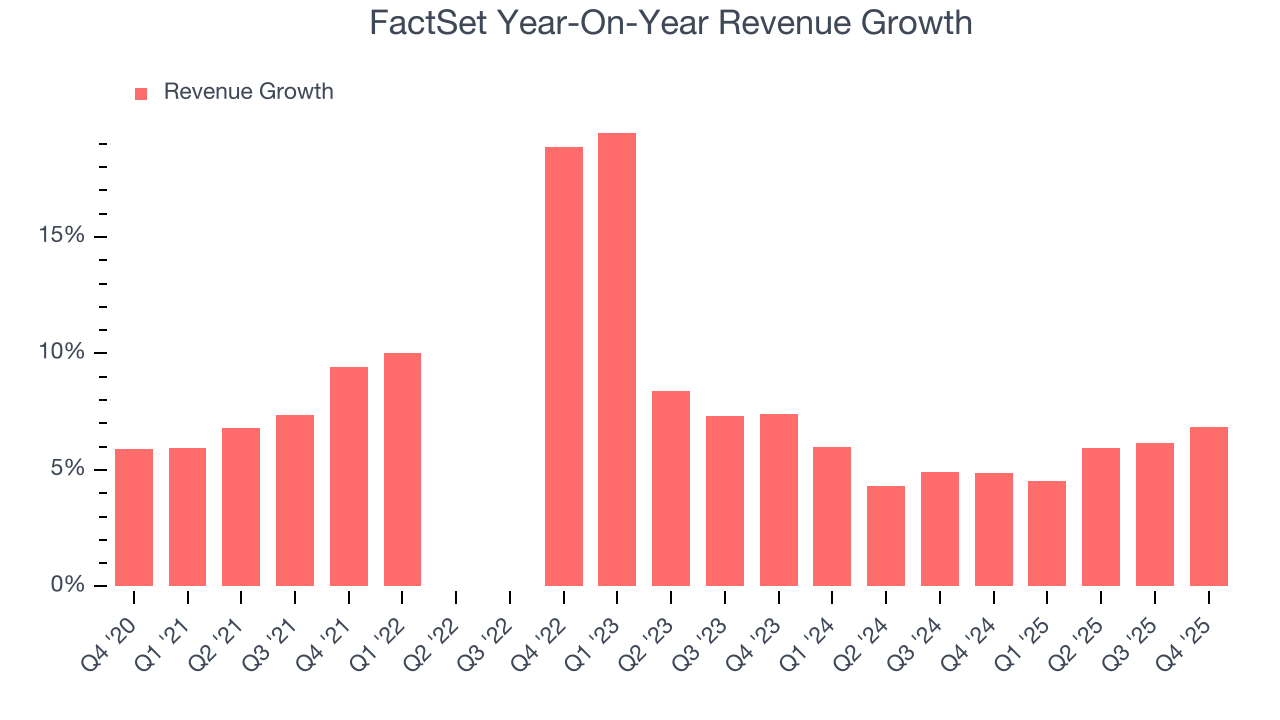

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, FactSet’s revenue grew at a decent 9.3% compounded annual growth rate over the last five years. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. FactSet’s recent performance shows its demand has slowed as its annualized revenue growth of 5.5% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, FactSet reported year-on-year revenue growth of 6.9%, and its $607.6 million of revenue exceeded Wall Street’s estimates by 1.3%.

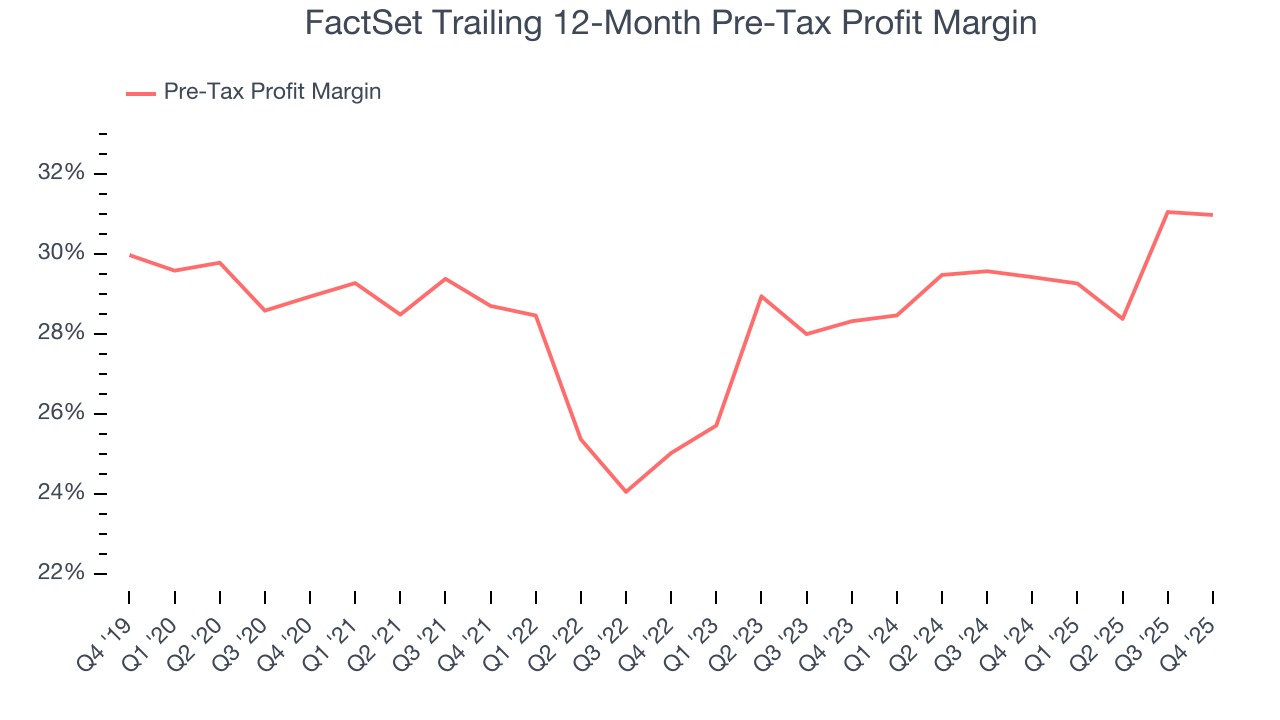

6. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Financial Exchanges & Data companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Financials companies manage interest-bearing assets and liabilities, making the interest income and expenses included in pre-tax profit essential to their profit calculation. Taxes, being external factors beyond management control, are appropriately excluded from this alternative margin measure.

Over the last five years, FactSet’s pre-tax profit margin has fallen by 2 percentage points, going from 28.7% to 31%. It has also expanded by 2.7 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

In Q4, FactSet’s pre-tax profit margin was 31.3%. This result was in line with the same quarter last year.

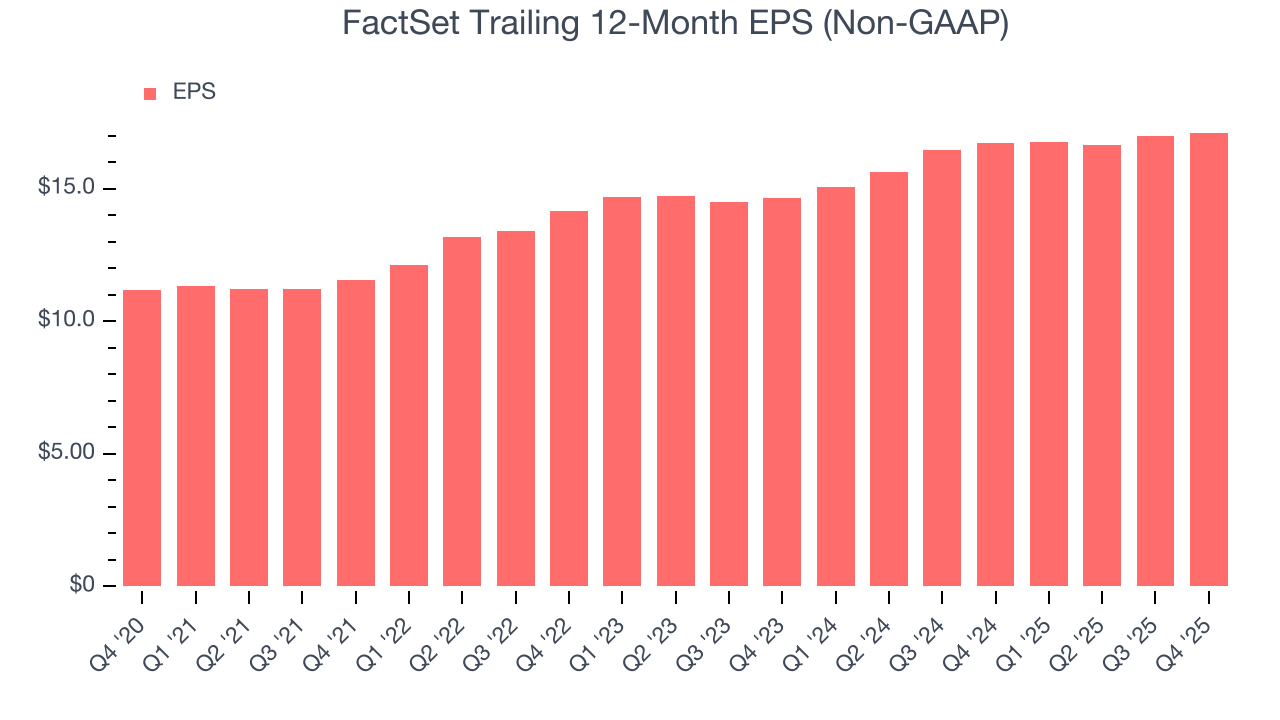

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

FactSet’s unimpressive 8.9% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Although it wasn’t great, FactSet’s two-year annual EPS growth of 8.1% topped its 5.5% two-year revenue growth.

Diving into the nuances of FactSet’s earnings can give us a better understanding of its performance. While we mentioned earlier that FactSet’s pre-tax profit margin was flat this quarter, a two-year view shows its margin has expandedwhile its share count has shrunk 2.7%. Improving profitability and share buybacks are positive signs for shareholders as they juice EPS growth relative to revenue growth.

In Q4, FactSet reported adjusted EPS of $4.51, up from $4.37 in the same quarter last year. This print beat analysts’ estimates by 3.5%. Over the next 12 months, Wall Street expects FactSet’s full-year EPS of $17.11 to grow 3.6%.

8. Return on Equity

Return on equity, or ROE, tells us how much profit a company generates for each dollar of shareholder equity, a key funding source for banks. Over a long period, banks with high ROE tend to compound shareholder wealth faster through retained earnings, buybacks, and dividends.

Over the last five years, FactSet has averaged an ROE of 32.3%, exceptional for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This is a bright spot for FactSet.

9. Balance Sheet Assessment

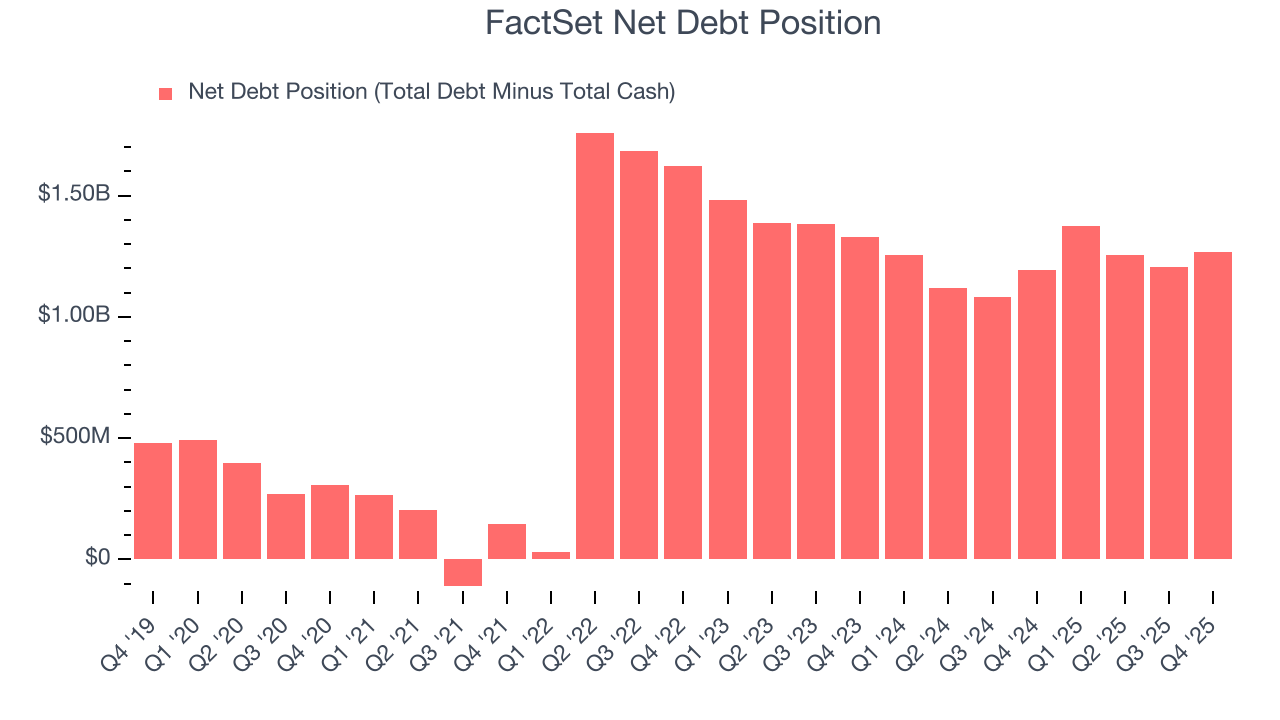

FactSet reported $292.7 million of cash and $1.56 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $954 million of EBITDA over the last 12 months, we view FactSet’s 1.3× net-debt-to-EBITDA ratio as safe. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

10. Key Takeaways from FactSet’s Q4 Results

We enjoyed seeing FactSet beat analysts’ EBITDA expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance slightly missed. Zooming out, we think this was a mixed quarter. The stock remained flat at $297.75 immediately following the results.

11. Is Now The Time To Buy FactSet?

Updated: March 22, 2026 at 12:52 AM EDT

Before making an investment decision, investors should account for FactSet’s business fundamentals and valuation in addition to what happened in the latest quarter.

There are some bright spots in FactSet’s fundamentals, but its business quality ultimately falls short. First off, its revenue growth was good over the last five years. And while FactSet’s unimpressive EPS growth over the last five years shows it’s failed to produce meaningful profits for shareholders, its stellar ROE suggests it has been a well-run company historically.

FactSet’s P/E ratio based on the next 12 months is 11.7x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $296.71 on the company (compared to the current share price of $211).