F&G Annuities & Life (FG)

F&G Annuities & Life is a special business. Its revenue and EPS are projected to skyrocket next year, an optimistic sign for its share price.― StockStory Analyst Team

1. News

2. Summary

Why We Like F&G Annuities & Life

Founded in 1959 and serving approximately 677,000 policyholders who rely on its financial protection products, F&G Annuities & Life (NYSE:FG) provides fixed annuities, life insurance, and pension risk transfer solutions to retail and institutional clients.

- Annual revenue growth of 61.4% over the past five years was outstanding, reflecting market share gains this cycle

- Impressive 37.7% annual book value per share growth over the last two years indicates it’s building equity value this cycle

- Strong 92% annualized net premiums earned expansion over the last five years shows it’s capturing market share this cycle

F&G Annuities & Life is a market leader. The price looks reasonable when considering its quality, and we think now is a favorable time to invest.

Why Is Now The Time To Buy F&G Annuities & Life?

F&G Annuities & Life’s stock price of $33.37 implies a valuation ratio of 0.9x forward P/B. The valuation multiple is below many companies in the insurance sector. We therefore think the stock is a good deal for the fundamentals.

Entry price matters much less than business quality when investing for the long term, but hey, it certainly doesn’t hurt to get in at an attractive price.

3. F&G Annuities & Life (FG) Research Report: Q3 CY2025 Update

Insurance solutions provider F&G Annuities & Life (NYSE:FG) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 16.5% year on year to $1.69 billion. Its non-GAAP profit of $1.22 per share was 25.4% above analysts’ consensus estimates.

F&G Annuities & Life (FG) Q3 CY2025 Highlights:

Company Overview

Founded in 1959 and serving approximately 677,000 policyholders who rely on its financial protection products, F&G Annuities & Life (NYSE:FG) provides fixed annuities, life insurance, and pension risk transfer solutions to retail and institutional clients.

F&G specializes in retirement and protection products, with fixed indexed annuities (FIAs) forming the core of its retail business. These products allow customers to participate in market gains through indices like the S&P 500 while protecting their principal from market downturns. The company also offers multi-year guarantee annuities (MYGAs) that provide guaranteed interest rates over specified periods, and recently expanded into registered index-linked annuities (RILAs) that offer higher return potential with some downside risk.

For institutional clients, F&G provides pension risk transfer solutions where it assumes responsibility for pension obligations from corporate plan sponsors, converting them into guaranteed income streams for retirees. The company also issues funding agreements to generate spread-based income without mortality risk.

F&G distributes its retail products through three main channels: independent agents (via approximately 280 independent marketing organizations representing nearly 102,000 agents), banks, and broker-dealers (through about 21 institutions representing approximately 10,000 financial advisers). This multi-channel approach allows F&G to reach diverse customer segments seeking retirement security.

The company generates revenue primarily through spread-based earnings—investing policyholder premiums in fixed income securities while paying out guaranteed rates or index-linked returns to policyholders. F&G manages risk through strategic reinsurance arrangements with various partners, allowing it to optimize capital efficiency and manage reserve requirements.

F&G leverages its strategic partnership with Blackstone, which provides investment management expertise to enhance portfolio yields while maintaining appropriate risk levels across varying market cycles.

4. Life Insurance

Life insurance companies collect premiums from policyholders in exchange for providing a future death benefit or retirement income stream. Interest rates matter for the sector (and make it cyclical), with higher rates allowing insurers to reinvest their fixed-income portfolios at more attractive yields and vice versa. Additionally, favorable demographic shifts, such as an aging population, are driving strong demand for retirement products while AI and data analytics offer significant opportunities to improve underwriting accuracy and operational efficiency. Conversely, the industry faces headwinds from persistent competition from agile insurtechs that threaten traditional distribution models.

F&G Annuities & Life competes with major insurance providers in the annuity and life insurance markets, including Athene (owned by Apollo Global Management), American Equity Investment Life, Global Atlantic (owned by KKR), Lincoln Financial Group (NYSE:LNC), and Prudential Financial (NYSE:PRU).

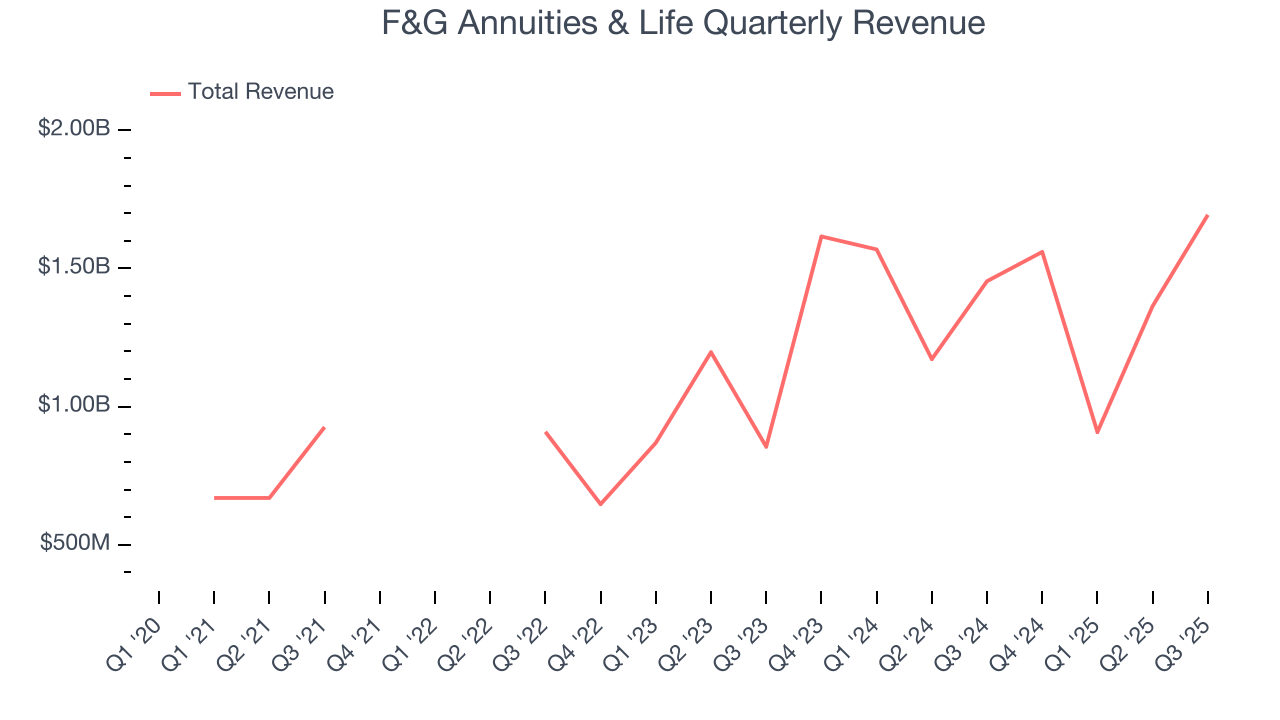

5. Revenue Growth

Insurance companies earn revenue from three primary sources: 1) The core insurance business itself, often called underwriting and represented in the income statement as premiums 2) Income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities 3) Fees from various sources such as policy administration, annuities, or other value-added services. Thankfully, F&G Annuities & Life’s 15% annualized revenue growth over the last four years was incredible. Its growth surpassed the average insurance company and shows its offerings resonate with customers, a great starting point for our analysis.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. F&G Annuities & Life’s annualized revenue growth of 24.4% over the last two years is above its four-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, F&G Annuities & Life reported year-on-year revenue growth of 16.5%, and its $1.69 billion of revenue exceeded Wall Street’s estimates by 20.8%.

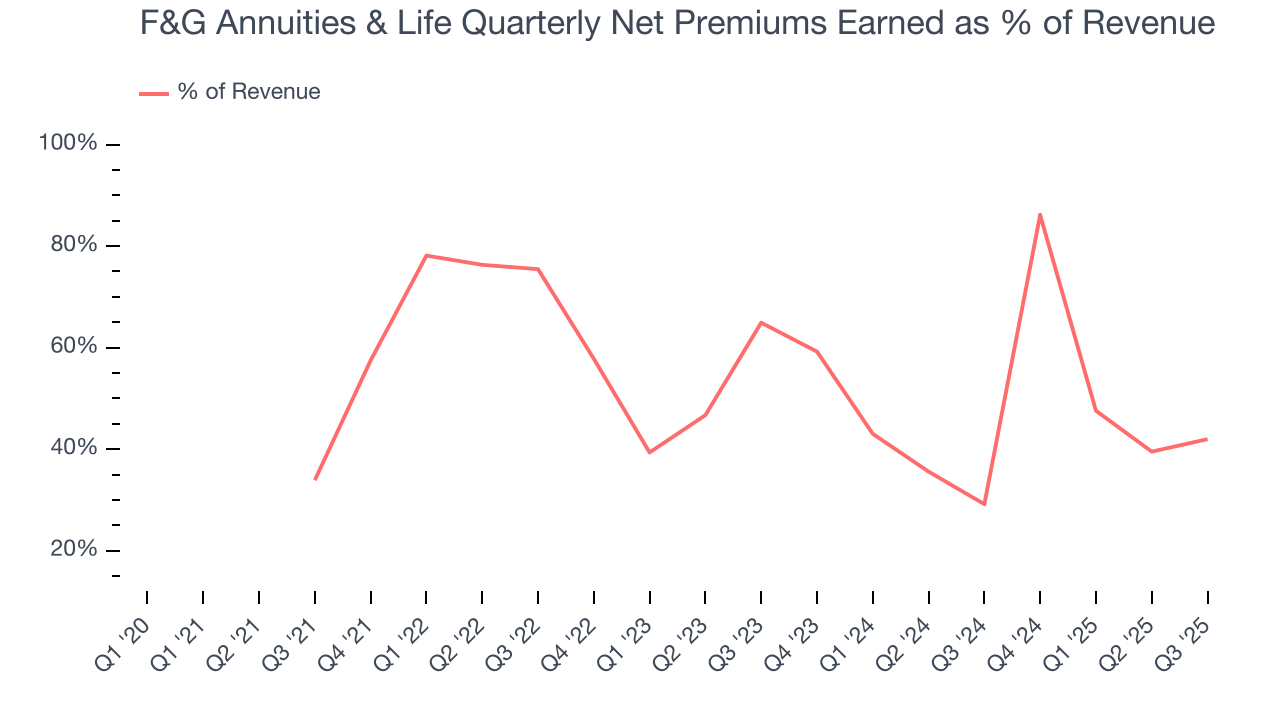

Net premiums earned made up 48.8% of the company’s total revenue during the last five years, meaning F&G Annuities & Life’s growth drivers strike a balance between insurance and non-insurance activities.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Net premiums earned commands greater market attention due to its reliability and consistency, whereas investment and fee income are often seen as more volatile revenue streams that fluctuate with market conditions.

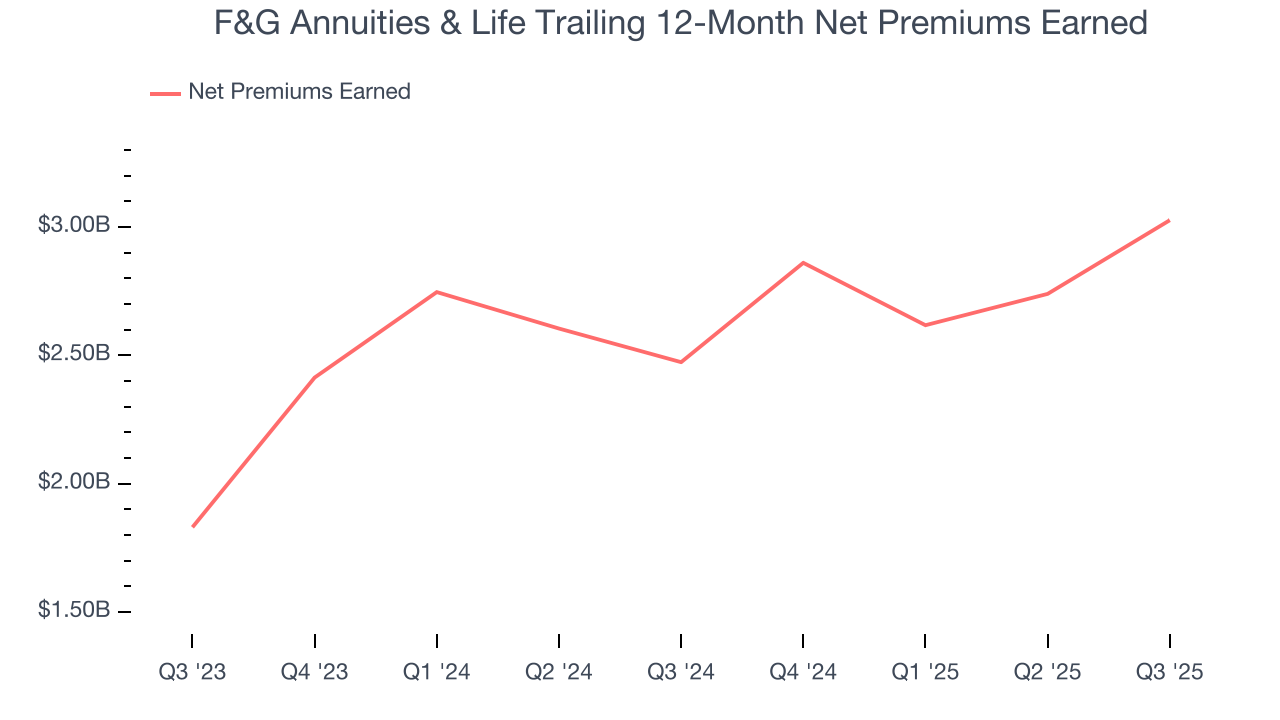

6. Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

- Gross premiums - what’s ceded to reinsurers as a risk mitigation and transfer strategy

F&G Annuities & Life’s net premiums earned has grown at a 41.3% annualized rate over the last four years, much better than the broader insurance industry and faster than its total revenue.

When analyzing F&G Annuities & Life’s net premiums earned over the last two years, we can see that growth decelerated to 28.6% annually. Since two-year net premiums earned grew faster than total revenue over this period, it's implied that other line items such as investment income grew at a slower rate. While these additional streams certainly contribute to the bottom line, their impact can vary. Some firms have shown greater success and long-term consistency in investing their float compared to peers. However, sharp fluctuations in the fixed income and equity markets can significantly affect short-term performance.

F&G Annuities & Life produced $711 million of net premiums earned in Q3, up a hearty 67.7% year on year and topping Wall Street Consensus estimates by 6%.

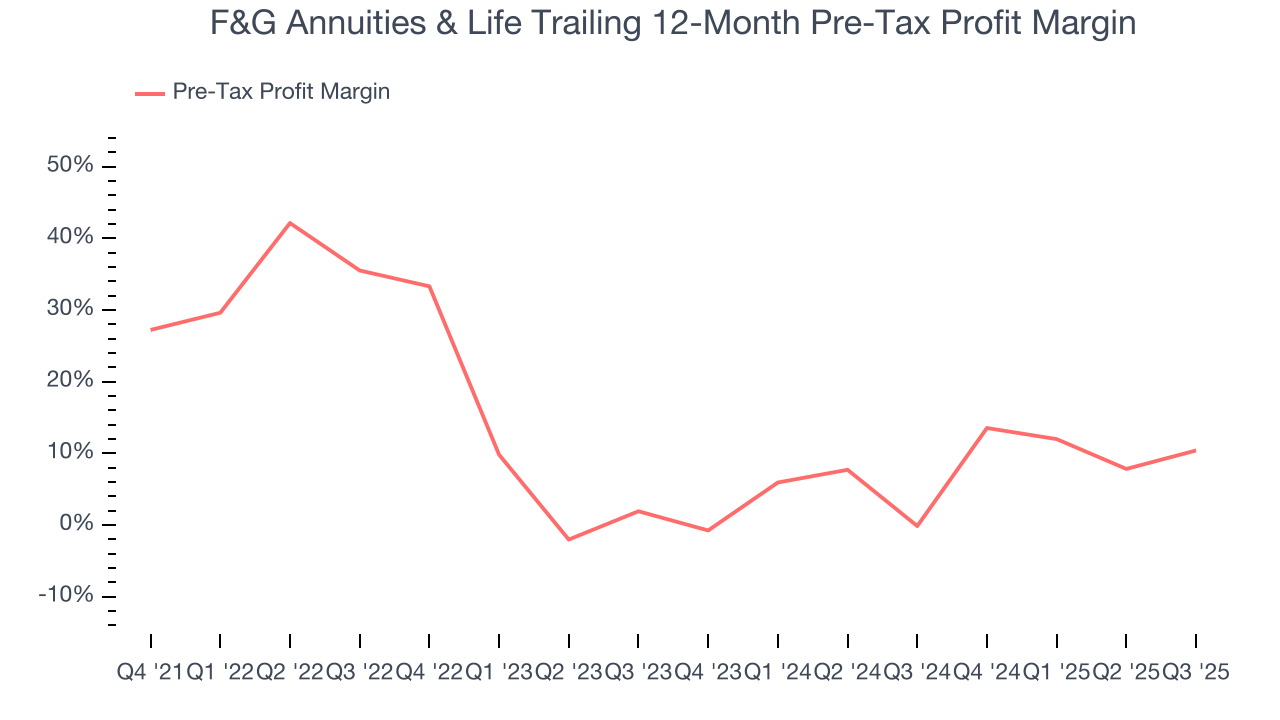

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Insurance companies are balance sheet businesses, where assets and liabilities define the economics. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not. This is pre-tax profit by definition.

Over the last two years, F&G Annuities & Life’s pre-tax profit margin has fallen by 8.5 percentage points, going from 1.9% to 10.4%. Said differently, the company’s expenses have grown at a slower rate than revenue, which typically signals prudent management.

F&G Annuities & Life’s pre-tax profit margin came in at 7.7% this quarter. This result was 9.8 percentage points better than the same quarter last year.

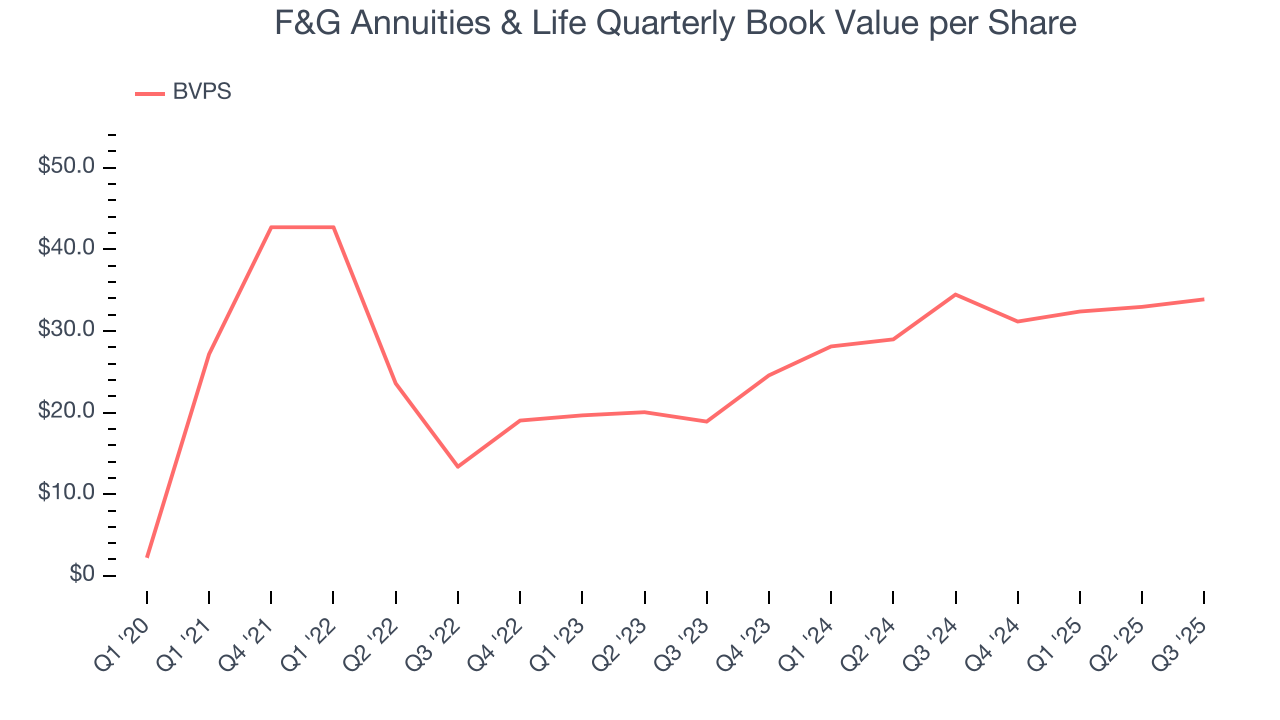

8. Book Value Per Share (BVPS)

Insurers are balance sheet businesses, collecting premiums upfront and paying out claims over time. Premiums collected but not yet paid out, often referred to as the float, are invested and create an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality. While other (and more commonly known) per-share metrics like EPS can sometimes be lumpy due to reserve releases or one-time items and can be managed or skewed while still following accounting rules, BVPS reflects long-term capital growth and is harder to manipulate.

Fortunately for investors, F&G Annuities & Life’s BVPS grew at an incredible 33.9% annual clip over the last two years.

Over the next 12 months, Consensus estimates call for F&G Annuities & Life’s BVPS to grow by 48.4% to $46.03, elite growth rate.

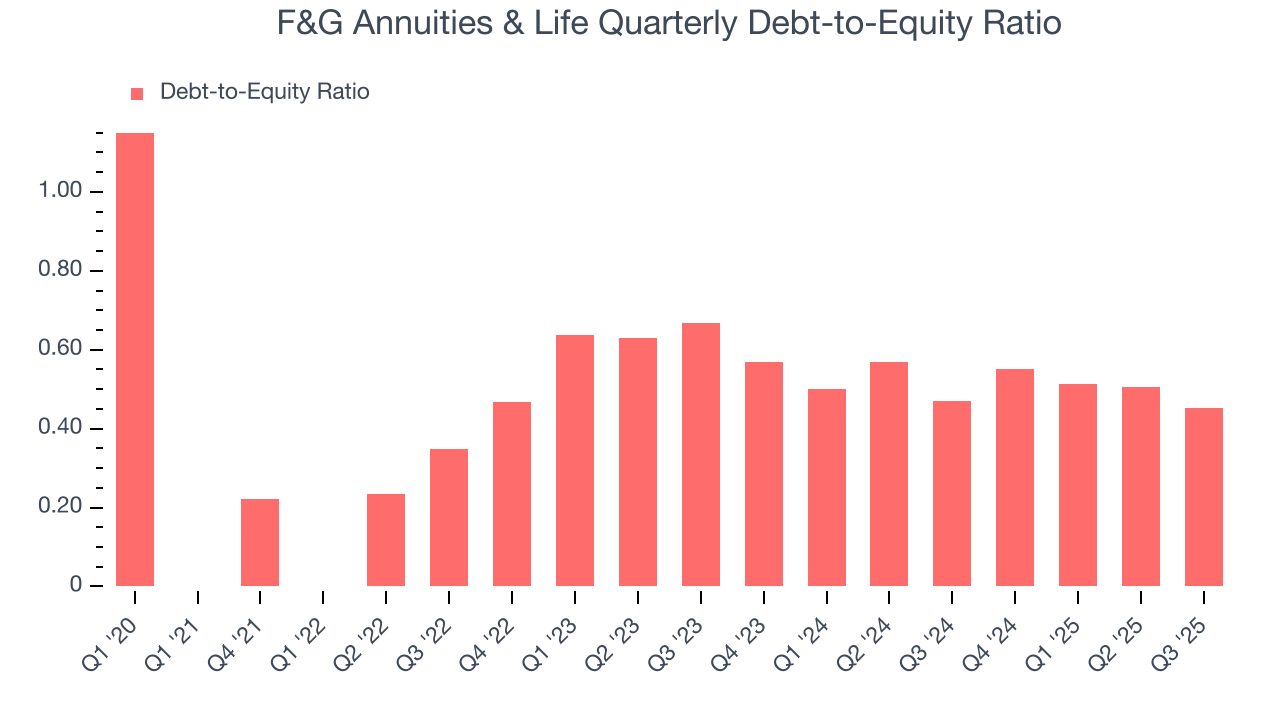

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

F&G Annuities & Life currently has $2.24 billion of debt and $4.94 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.5×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

10. Key Takeaways from F&G Annuities & Life’s Q3 Results

It was good to see F&G Annuities & Life beat analysts’ EPS expectations this quarter. We were also excited its net premiums earned outperformed Wall Street’s estimates by a wide margin. On the other hand, its book value per share missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $29.87 immediately following the results.

11. Is Now The Time To Buy F&G Annuities & Life?

Updated: December 3, 2025 at 11:32 PM EST

When considering an investment in F&G Annuities & Life, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

F&G Annuities & Life is an amazing business ranking highly on our list. First of all, the company’s revenue growth was exceptional over the last five years. And while its weak EPS growth over the last two years shows it’s failed to produce meaningful profits for shareholders, its net premiums earned growth was exceptional over the last five years. Additionally, F&G Annuities & Life’s projected EPS for the next year implies the company will start generating shareholder value.

F&G Annuities & Life’s P/B ratio based on the next 12 months is 0.9x. Looking across the spectrum of insurance businesses, F&G Annuities & Life’s fundamentals clearly illustrate it’s a special business. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $34 on the company (compared to the current share price of $33.37).