Fidelis Insurance (FIHL)

We’re wary of Fidelis Insurance. Its decelerating revenue growth and even worse EPS performance give us little confidence it can beat the market.― StockStory Analyst Team

1. News

2. Summary

Why Fidelis Insurance Is Not Exciting

Founded in Bermuda in 2014 and designed to adapt nimbly to evolving market conditions, Fidelis Insurance (NYSE:FIHL) is a global specialty insurance and reinsurance company focused on creating value through strategic capital allocation, expert risk selection and a network of long-term underwriting partnerships.

- Estimated sales growth of 4.5% for the next 12 months implies demand will slow from its two-year trend

- A positive is that its annual revenue growth of 24.4% over the past three years was outstanding, reflecting market share gains this cycle

Fidelis Insurance’s quality is not up to our standards. There are more profitable opportunities elsewhere.

Why There Are Better Opportunities Than Fidelis Insurance

Fidelis Insurance is trading at $18.84 per share, or 0.6x forward P/B. This sure is a cheap multiple, but you get what you pay for.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Fidelis Insurance (FIHL) Research Report: Q4 CY2025 Update

Specialty insurance provider Fidelis Insurance (NYSE:FIHL) missed Wall Street’s revenue expectations in Q4 CY2025, with sales falling 10.8% year on year to $600.9 million. Its non-GAAP profit of $1.09 per share was 1.3% above analysts’ consensus estimates.

Fidelis Insurance (FIHL) Q4 CY2025 Highlights:

- Net Premiums Earned: $552.9 million vs analyst estimates of $621.3 million (12.9% year-on-year decline, 11% miss)

- Revenue: $600.9 million vs analyst estimates of $706.8 million (10.8% year-on-year decline, 15% miss)

- Combined Ratio: 80.6% vs analyst estimates of 84.5% (390 basis point beat)

- Adjusted EPS: $1.09 vs analyst estimates of $1.08 (1.3% beat)

- Book Value per Share: $24.61 vs analyst estimates of $24.51 (12.3% year-on-year growth, in line)

- Market Capitalization: $2.07 billion

Company Overview

Founded in Bermuda in 2014 and designed to adapt nimbly to evolving market conditions, Fidelis Insurance (NYSE:FIHL) is a global specialty insurance and reinsurance company focused on creating value through strategic capital allocation, expert risk selection and a network of long-term underwriting partnerships.

Fidelis operates through three distinct business segments that serve different market needs. The Specialty segment offers traditional insurance lines including Aviation and Aerospace, Energy, Marine, and Property, targeting areas where market dislocations create pricing opportunities. The Bespoke segment focuses on highly tailored solutions like Credit and Political Risk coverage, where clients often seek regulatory capital relief rather than traditional insurance protection. The Reinsurance segment primarily handles residential property catastrophe coverage with a strong North American focus.

The company employs sophisticated risk modeling and analytics, particularly for natural catastrophe exposures where it has developed its own climate change impact assessments to supplement third-party models. This analytical approach allows Fidelis to carefully manage aggregate exposures and shift its business mix as market conditions change.

Fidelis distributes its products primarily through insurance brokers and intermediaries, with Marsh & McLennan and Aon being significant distribution partners. This broker-driven approach provides efficient access to global markets without requiring an extensive proprietary distribution network.

The company maintains a conservative investment approach, primarily holding high-quality, short-duration fixed income securities like U.S. Treasuries, government bonds, and investment-grade corporate debt. Fidelis operates globally with its principal subsidiaries located in Bermuda, the United Kingdom, and Ireland, each regulated by their respective financial authorities.

4. Reinsurance

This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. The primary headwind remains the immense and concentrated exposure to large-scale catastrophe losses, as the growing impact of climate change challenges traditional risk models and creates significant earnings volatility. Additionally, they face the risk of adverse prior-year reserve development, where claims prove more costly than anticipated, while the eventual influx of new capital from alternative sources threatens to soften the market and compress future returns.

Fidelis Insurance competes with other specialty insurers and reinsurers including Arch Capital Group (NASDAQ:ACGL), Axis Capital Holdings (NYSE:AXS), RenaissanceRe Holdings (NYSE:RNR), and Hiscox (LON:HSX).

5. Revenue Growth

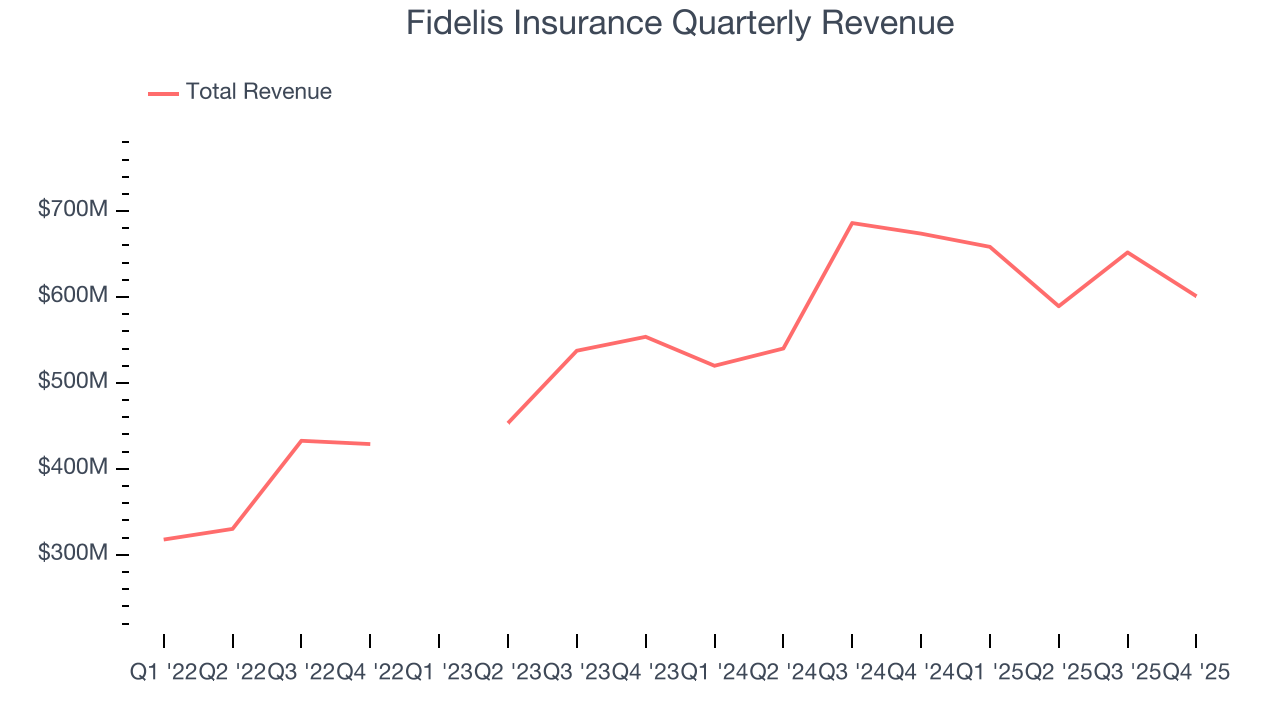

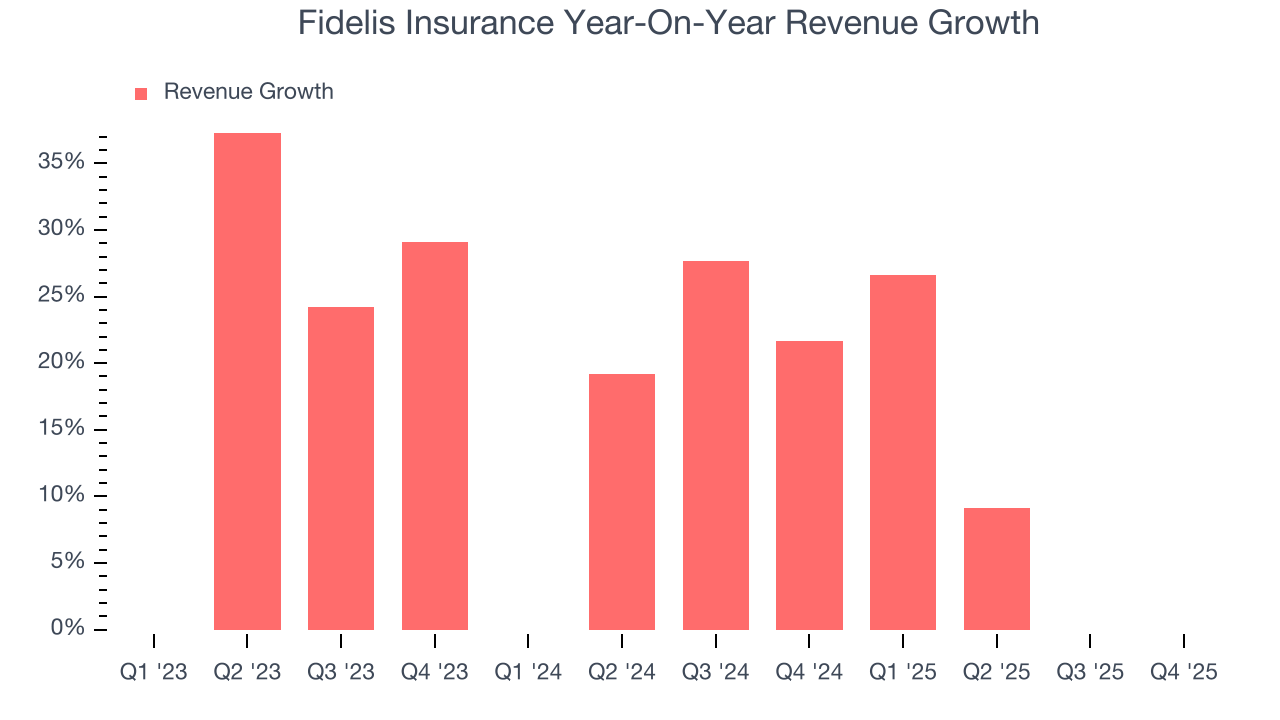

Insurance companies generate revenue three ways. The first is the core insurance business itself, represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected but not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from policy administration, annuities, and other value-added services. Thankfully, Fidelis Insurance’s 24.4% annualized revenue growth over the last three years was incredible. Its growth beat the average insurance company and shows its offerings resonate with customers, a helpful starting point for our analysis.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Fidelis Insurance’s annualized revenue growth of 9.2% over the last two years is below its three-year trend, but we still think the results suggest healthy demand.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Fidelis Insurance missed Wall Street’s estimates and reported a rather uninspiring 10.8% year-on-year revenue decline, generating $600.9 million of revenue.

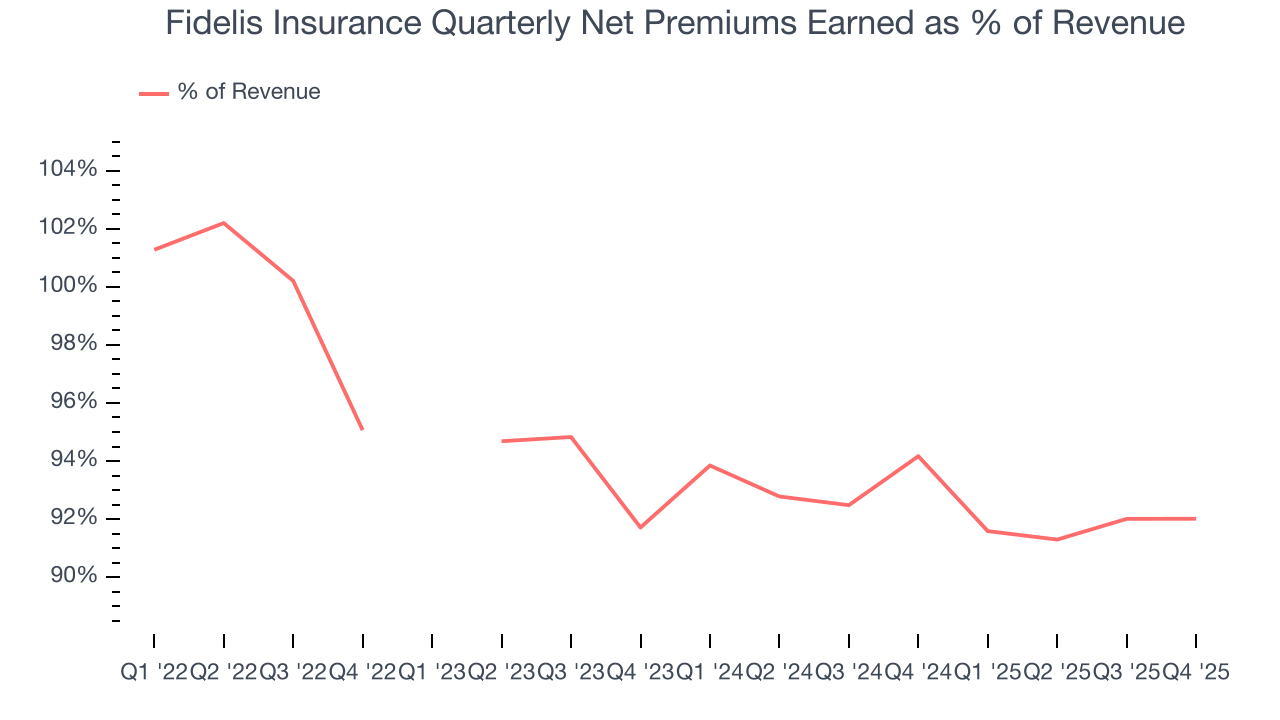

Net premiums earned made up 78.6% of the company’s total revenue during the last four years, meaning insurance operations are Fidelis Insurance’s largest source of revenue.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

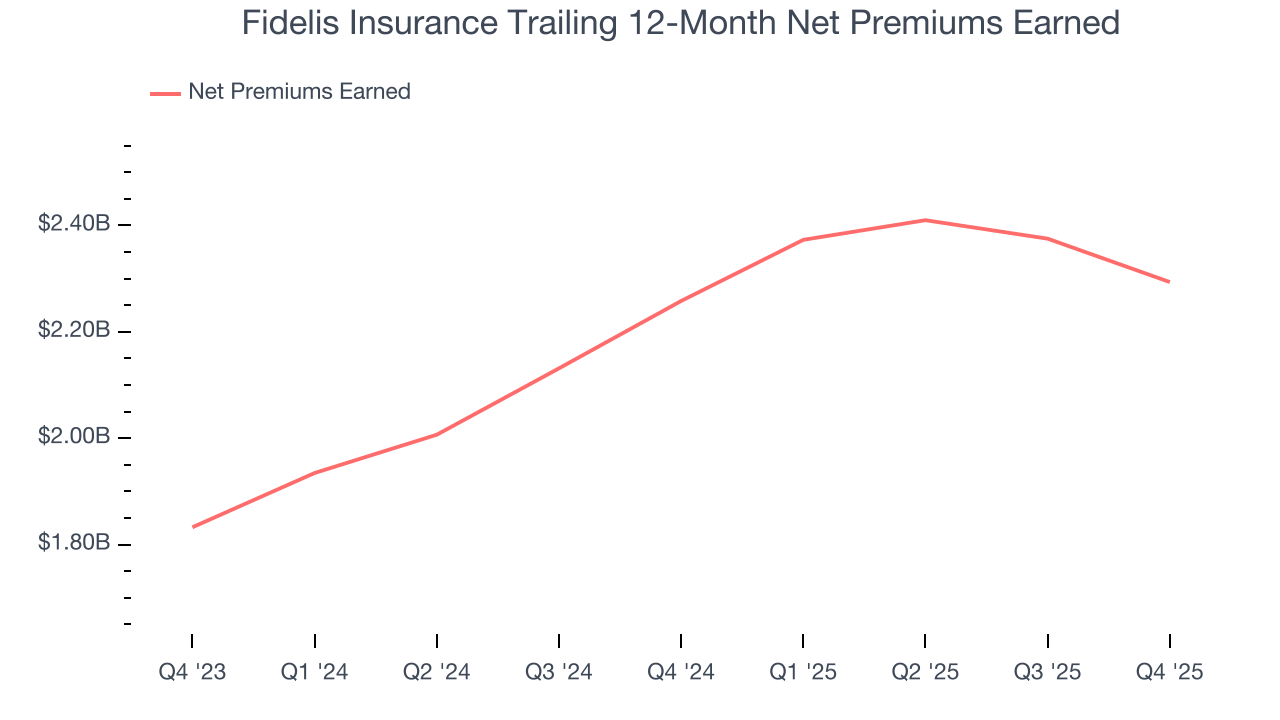

6. Net Premiums Earned

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

- Gross premiums - what’s ceded to reinsurers as a risk mitigation and transfer strategy

Fidelis Insurance’s net premiums earned has grown at a 20.1% annualized rate over the last three years, much better than the broader insurance industry but slower than its total revenue.

When analyzing Fidelis Insurance’s net premiums earned over the last two years, we can see that growth decelerated to 11.9% annually. Since two-year net premiums earned grew faster than total revenue over this period, it's implied that other line items such as investment income grew at a slower rate. These additional streams do play a key role in the bottom line, but their impact can vary. While some firms have excelled in consistently investing their float, sudden shifts in the fixed income and equity markets can heavily sway short-term performance.

This quarter, Fidelis Insurance’s net premiums earned was $552.9 million, down 12.9% year on year and short of Wall Street Consensus estimates.

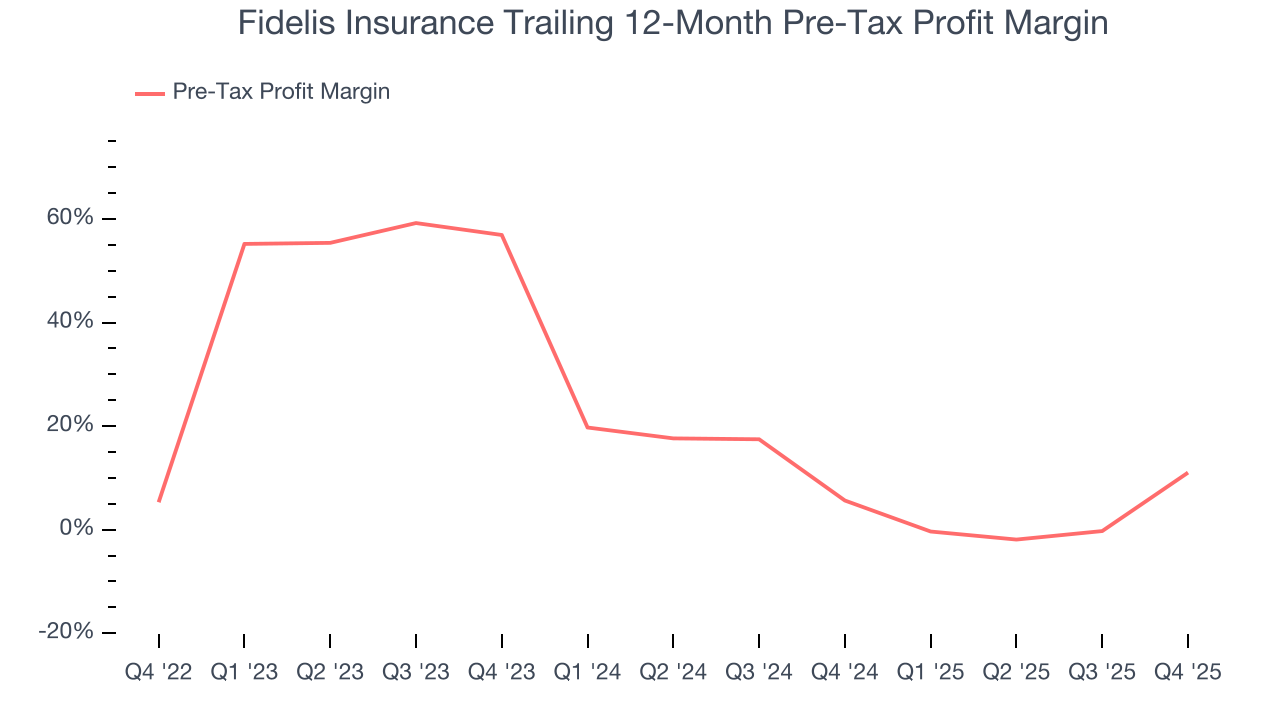

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Insurance companies are balance sheet businesses, where assets and liabilities define the economics. Interest income and expense should therefore be factored into the definition of profit but taxes - which are largely out of a company’s control - should not. This is pre-tax profit by definition.

Over the last two years, Fidelis Insurance’s pre-tax profit margin has risen by 45.9 percentage points, going from 56.9% to 11%. Said differently, the company’s expenses have increased at a faster rate than revenue, which usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

Fidelis Insurance’s pre-tax profit margin came in at 23.8% this quarter. This result was 44.5 percentage points better than the same quarter last year.

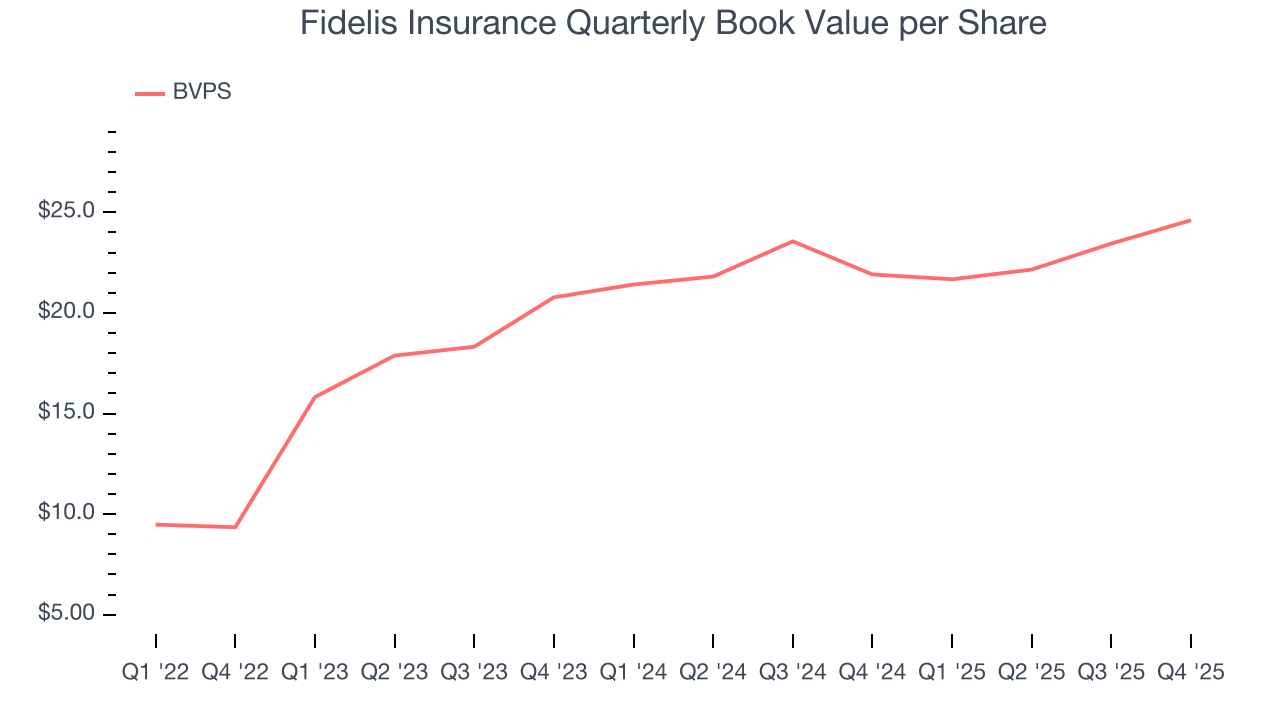

8. Book Value Per Share (BVPS)

Insurance companies are balance sheet businesses, collecting premiums upfront and paying out claims over time. The float – premiums collected but not yet paid out – are invested, creating an asset base supported by a liability structure. Book value captures this dynamic by measuring:

- Assets (investment portfolio, cash, reinsurance recoverables) - liabilities (claim reserves, debt, future policy benefits)

BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

To the detriment of investors, Fidelis Insurance’s BVPS grew at a tepid 8.8% annual clip over the last two years.

Over the next 12 months, Consensus estimates call for Fidelis Insurance’s BVPS to grow by 30% to $24.51, elite growth rate.

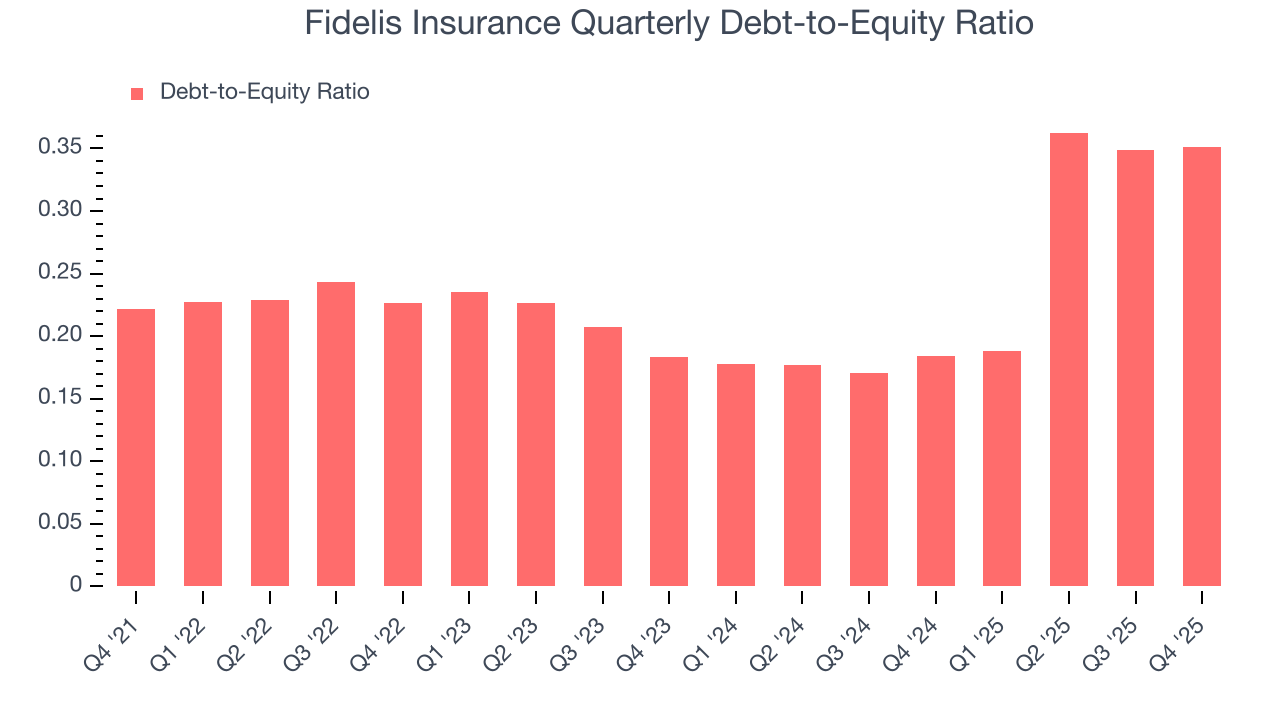

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Fidelis Insurance currently has $843.2 million of debt and $2.4 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.3×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

10. Key Takeaways from Fidelis Insurance’s Q4 Results

We struggled to find many positives in these results. Its revenue missed and its net premiums earned fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $20.10 immediately after reporting.

11. Is Now The Time To Buy Fidelis Insurance?

Updated: March 23, 2026 at 1:14 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Fidelis Insurance, you should also grasp the company’s longer-term business quality and valuation.

Fidelis Insurance isn’t a terrible business, but it isn’t one of our picks. Although its revenue growth was exceptional over the last three years, it’s expected to deteriorate over the next 12 months and its declining EPS over the last two years makes it a less attractive asset to the public markets. And while the company’s net premiums earned growth was exceptional over the last three years, the downside is its declining pre-tax profit margin shows the business has become less efficient.

Fidelis Insurance’s P/B ratio based on the next 12 months is 0.6x. While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $22 on the company (compared to the current share price of $18.84).

Although the price target is bullish, readers should exercise caution because analysts tend to be overly optimistic. The firms they work for, often big banks, have relationships with companies that extend into fundraising, M&A advisory, and other rewarding business lines. As a result, they typically hesitate to say bad things for fear they will lose out. We at StockStory do not suffer from such conflicts of interest, so we’ll always tell it like it is.