Globus Medical (GMED)

Globus Medical piques our interest. Its blend of high growth and outstanding profitability makes for a nice return algorithm.― StockStory Analyst Team

1. News

2. Summary

Why Globus Medical Is Interesting

With operations spanning 64 countries and a portfolio of over 10 new products launched in 2023 alone, Globus Medical (NYSE:GMED) develops and sells implantable devices, surgical instruments, and technology solutions for spine, orthopedic, and neurosurgical procedures.

- Impressive 30.1% annual revenue growth over the last five years indicates it’s winning market share this cycle

- Earnings growth has massively outpaced its peers over the last five years as its EPS has compounded at 22.8% annually

- A drawback is its below-average returns on capital indicate management struggled to find compelling investment opportunities, and its decreasing returns suggest its historical profit centers are aging

Globus Medical is close to becoming a high-quality business. If you like the stock, the price seems fair.

Why Is Now The Time To Buy Globus Medical?

Globus Medical’s stock price of $84.80 implies a valuation ratio of 18.9x forward P/E. Scanning the healthcare landscape, we think the price is reasonable for the revenue growth you get.

This could be a good time to invest if you think there are underappreciated aspects of the business.

3. Globus Medical (GMED) Research Report: Q4 CY2025 Update

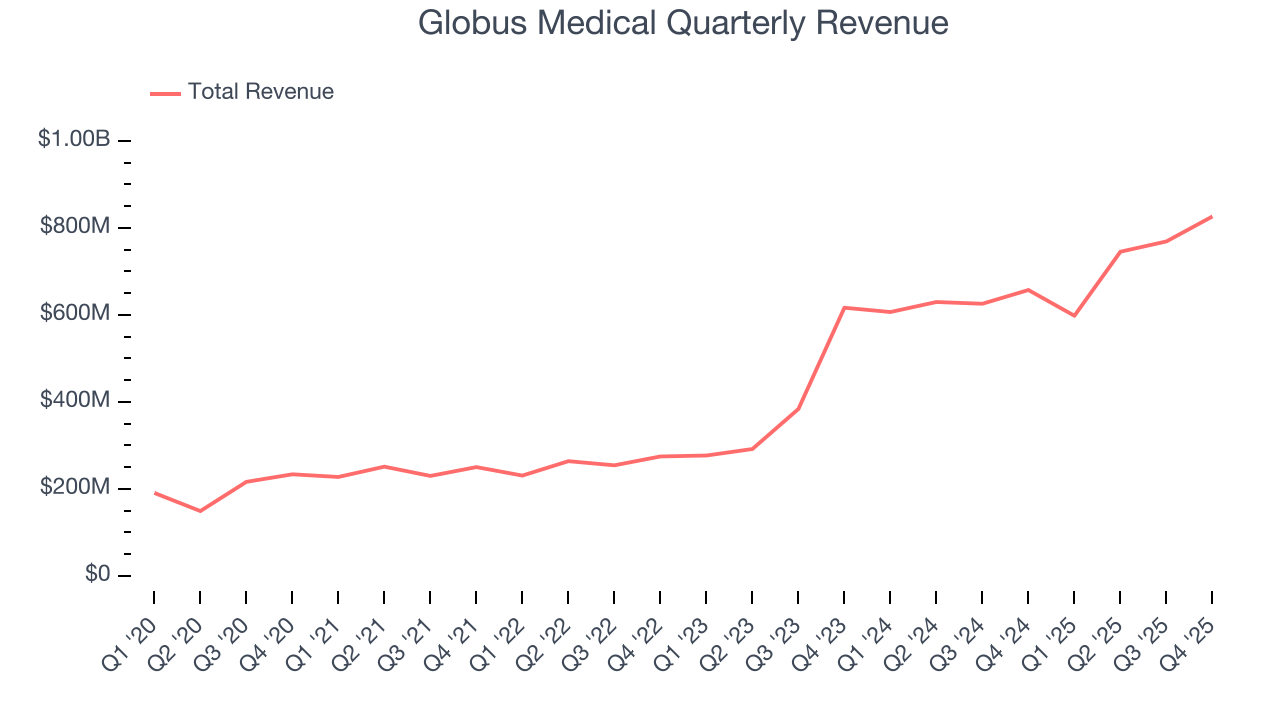

Medical device company Globus Medical (NYSE:GMED) announced better-than-expected revenue in Q4 CY2025, with sales up 25.7% year on year to $826.4 million. The company’s full-year revenue guidance of $3.2 billion at the midpoint came in 1.2% above analysts’ estimates. Its non-GAAP profit of $1.28 per share was 11% above analysts’ consensus estimates.

Globus Medical (GMED) Q4 CY2025 Highlights:

- Revenue: $826.4 million vs analyst estimates of $800.8 million (25.7% year-on-year growth, 3.2% beat)

- Adjusted EPS: $1.28 vs analyst estimates of $1.15 (11% beat)

- Adjusted EBITDA: $280.5 million vs analyst estimates of $267.2 million (33.9% margin, 5% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $4.45 at the midpoint, beating analyst estimates by 4.8%

- Operating Margin: 20.5%, up from 9.2% in the same quarter last year

- Free Cash Flow Margin: 24.5%, down from 29.4% in the same quarter last year

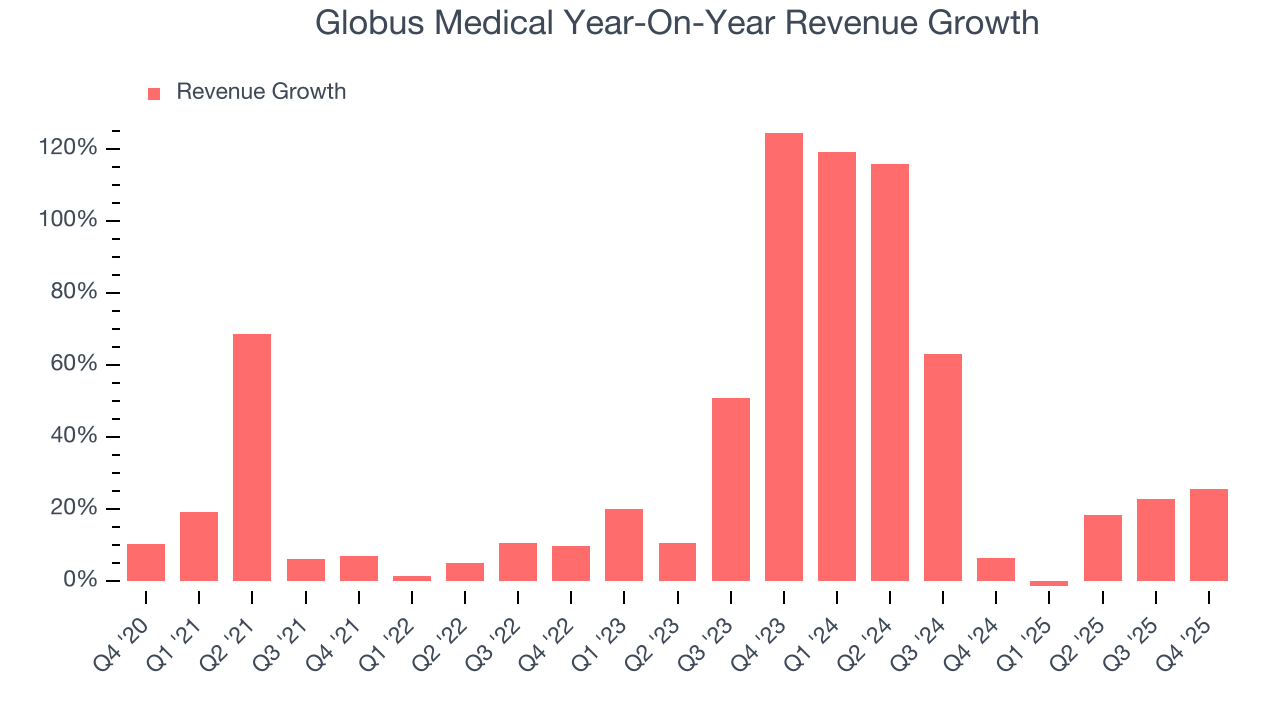

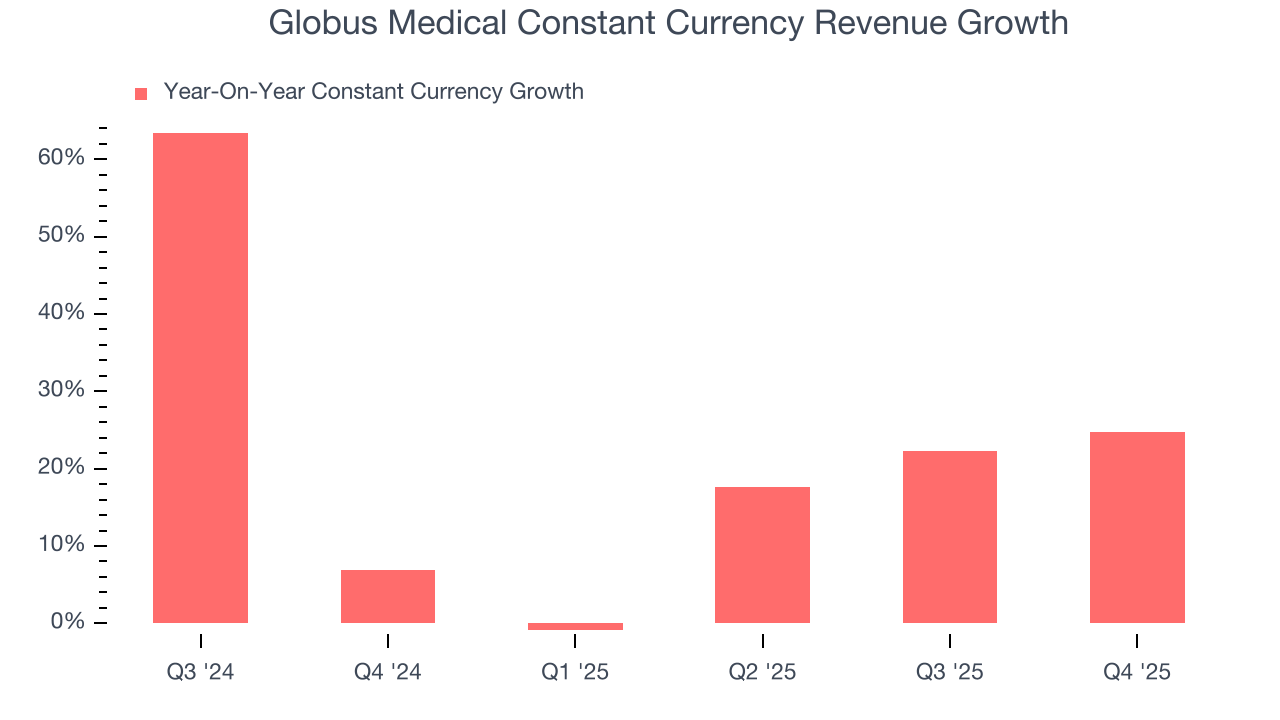

- Constant Currency Revenue rose 24.7% year on year (6.9% in the same quarter last year)

- Market Capitalization: $12.5 billion

Company Overview

With operations spanning 64 countries and a portfolio of over 10 new products launched in 2023 alone, Globus Medical (NYSE:GMED) develops and sells implantable devices, surgical instruments, and technology solutions for spine, orthopedic, and neurosurgical procedures.

Globus Medical's business is organized into two main categories: Musculoskeletal Solutions and Enabling Technologies. The Musculoskeletal Solutions segment comprises implantable devices, biologics, surgical instruments, and neuromonitoring services used in spinal, orthopedic, and neurosurgical procedures. These products address conditions ranging from degenerative disorders to deformities, tumors, and traumatic injuries.

The company's spine products include traditional fusion implants like pedicle screw systems and plating systems, as well as innovative expandable solutions that can be customized during surgery. For orthopedic trauma, Globus offers solutions for fracture patterns in upper and lower extremities, including plates, screws, nails, and external fixation devices. The company also provides hip and knee replacement implants for degenerative conditions.

A distinctive offering is Globus Medical's neuromonitoring service, which uses proprietary software to provide real-time feedback about nerve proximity during surgery. This technology translates complex neurophysiological data into simple information that helps surgeons navigate safely around nerves.

The Enabling Technologies category features advanced imaging, navigation, and robotics systems designed to enhance surgical precision. The ExcelsiusGPS platform, a robotic guidance and navigation system, supports minimally invasive procedures with applications for screw and interbody spacer placement. The company also offers Surgimap, a surgical planning software platform with predictive algorithms, and Excelsius3D, an imaging platform that provides three imaging modalities and can be integrated with the robotic navigation system.

Globus Medical sells its products primarily through an exclusive global sales force, with representatives often present in operating rooms during surgeries. The company invests significantly in surgeon education and training programs to demonstrate the benefits of its products and procedures, offering courses globally through both in-person and virtual formats.

In 2023, Globus Medical acquired NuVasive, a spine technology company, expanding its global reach and enhancing its product offerings. While the United States remains the primary market for Globus Medical's products, international sales accounted for approximately 18.4% of total sales in 2023.

4. Medical Devices & Supplies - Specialty

The medical devices industry operates a business model that balances steady demand with significant investments in innovation and regulatory compliance. The industry benefits from recurring revenue streams tied to consumables, maintenance services, and incremental upgrades to the latest technologies, although specialty devices are more niche. The capital-intensive nature of product development, coupled with lengthy regulatory pathways and the need for clinical validation, can weigh on profitability and timelines. In addition, there are constant pricing pressures from healthcare systems and insurers maximizing cost efficiency. Over the next several years, one tailwind is demographic–aging populations means rising chronic disease rates that drive greater demand for medical interventions and monitoring solutions. Advances in digital health, such as remote patient monitoring and smart devices, are also expected to unlock new demand by shortening upgrade cycles. On the other hand, the industry faces headwinds from pricing and reimbursement pressures as healthcare providers increasingly adopt value-based care models. Additionally, the integration of cybersecurity for connected devices adds further risk and complexity for device manufacturers.

Globus Medical's main competitors include Alphatec Holdings, Orthofix, Integra LifeSciences, and ZimVie, as well as larger medical device companies that operate in the musculoskeletal space such as Medtronic, Stryker, and Johnson & Johnson's DePuy Synthes.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $2.94 billion in revenue over the past 12 months, Globus Medical has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Globus Medical’s sales grew at an incredible 30.1% compounded annual growth rate over the last five years. Its growth beat the average healthcare company and shows its offerings resonate with customers, a helpful starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Globus Medical’s annualized revenue growth of 36.9% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

We can dig further into the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 22.3% year-on-year growth. Because this number is lower than its normal revenue growth, we can see that foreign exchange rates have boosted Globus Medical’s performance.

This quarter, Globus Medical reported robust year-on-year revenue growth of 25.7%, and its $826.4 million of revenue topped Wall Street estimates by 3.2%.

Looking ahead, sell-side analysts expect revenue to grow 7.6% over the next 12 months, a deceleration versus the last two years. Still, this projection is above average for the sector and suggests the market sees some success for its newer products and services.

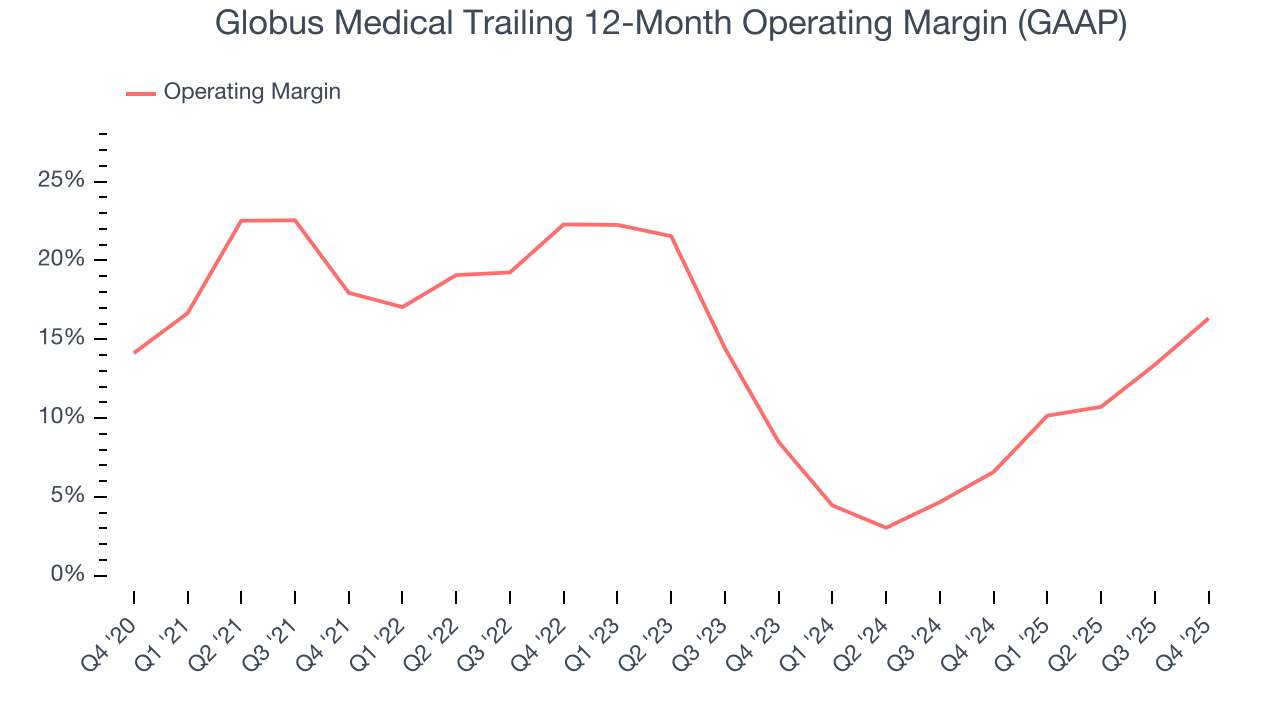

7. Operating Margin

Globus Medical has done a decent job managing its cost base over the last five years. The company has produced an average operating margin of 13.1%, higher than the broader healthcare sector.

Looking at the trend in its profitability, Globus Medical’s operating margin decreased by 1.6 percentage points over the last five years, but it rose by 7.8 percentage points on a two-year basis. We like Globus Medical and hope it can right the ship.

In Q4, Globus Medical generated an operating margin profit margin of 20.5%, up 11.3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

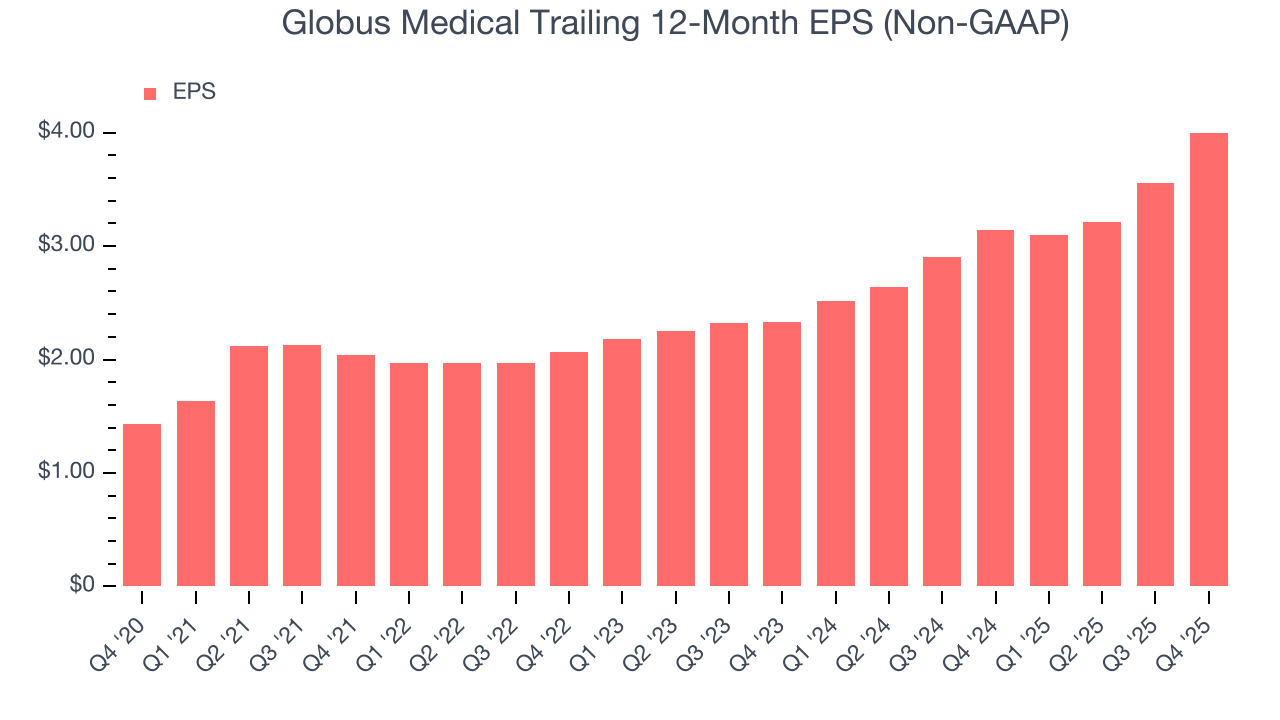

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Globus Medical’s EPS grew at an astounding 22.8% compounded annual growth rate over the last five years. However, this performance was lower than its 30.1% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

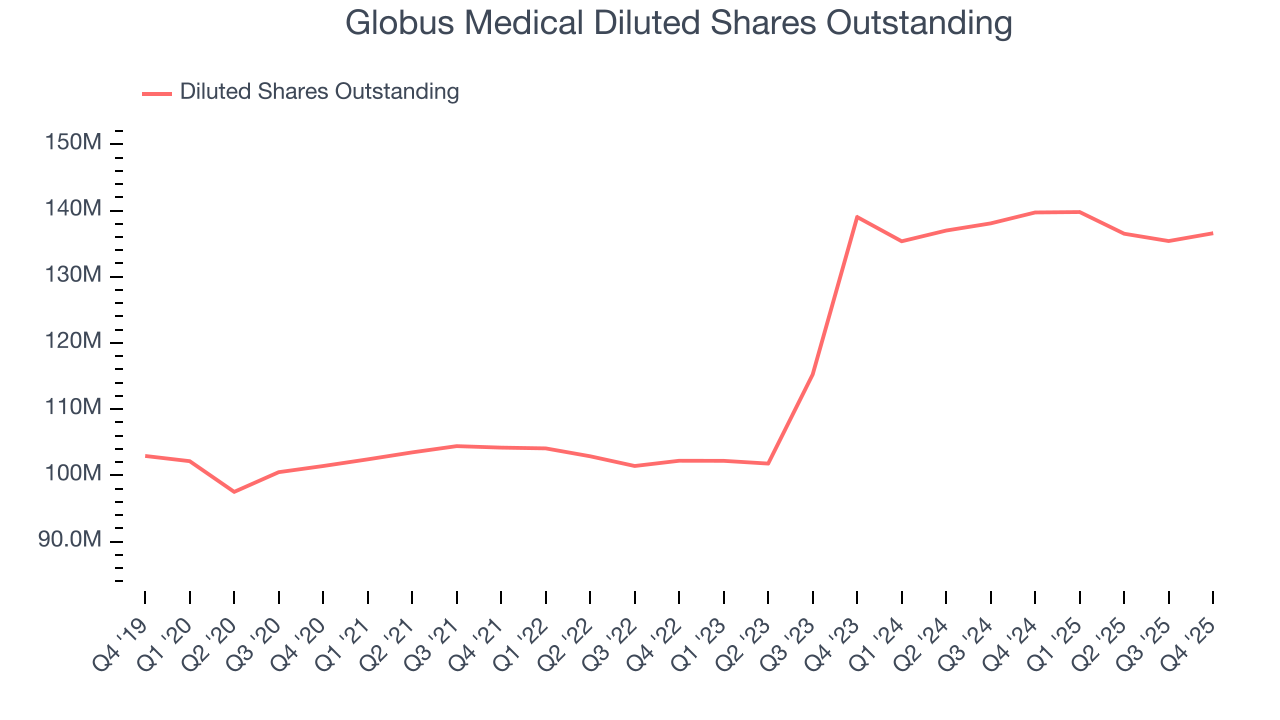

We can take a deeper look into Globus Medical’s earnings to better understand the drivers of its performance. As we mentioned earlier, Globus Medical’s operating margin expanded this quarter but declined by 1.6 percentage points over the last five years. Its share count also grew by 34.7%, meaning the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q4, Globus Medical reported adjusted EPS of $1.28, up from $0.84 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Globus Medical’s full-year EPS of $4 to grow 4.3%.

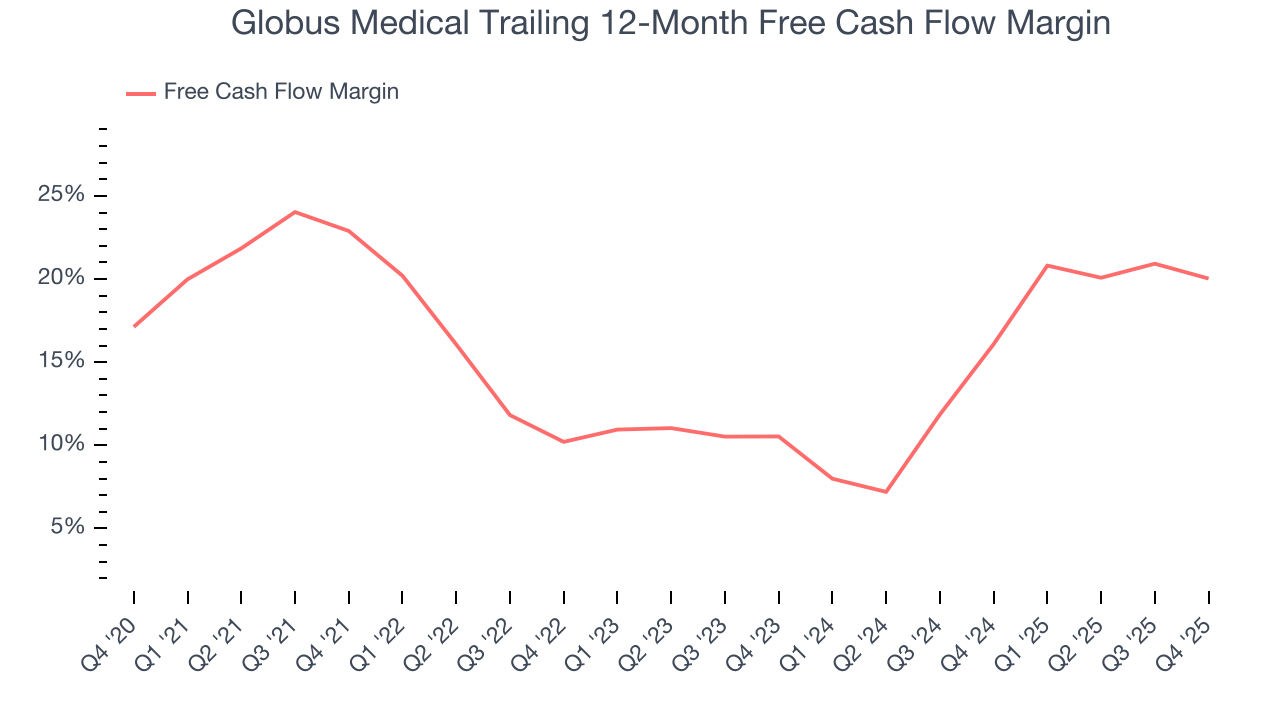

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Globus Medical has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 16.5% over the last five years, quite impressive for a healthcare business.

Taking a step back, we can see that Globus Medical’s margin dropped by 2.9 percentage points during that time. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity. We’ll give the company the benefit of the doubt for now as its overall financial profile is still healthy.

Globus Medical’s free cash flow clocked in at $202.4 million in Q4, equivalent to a 24.5% margin. The company’s cash profitability regressed as it was 4.9 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because investment needs can be seasonal, leading to short-term swings. Long-term trends are more important.

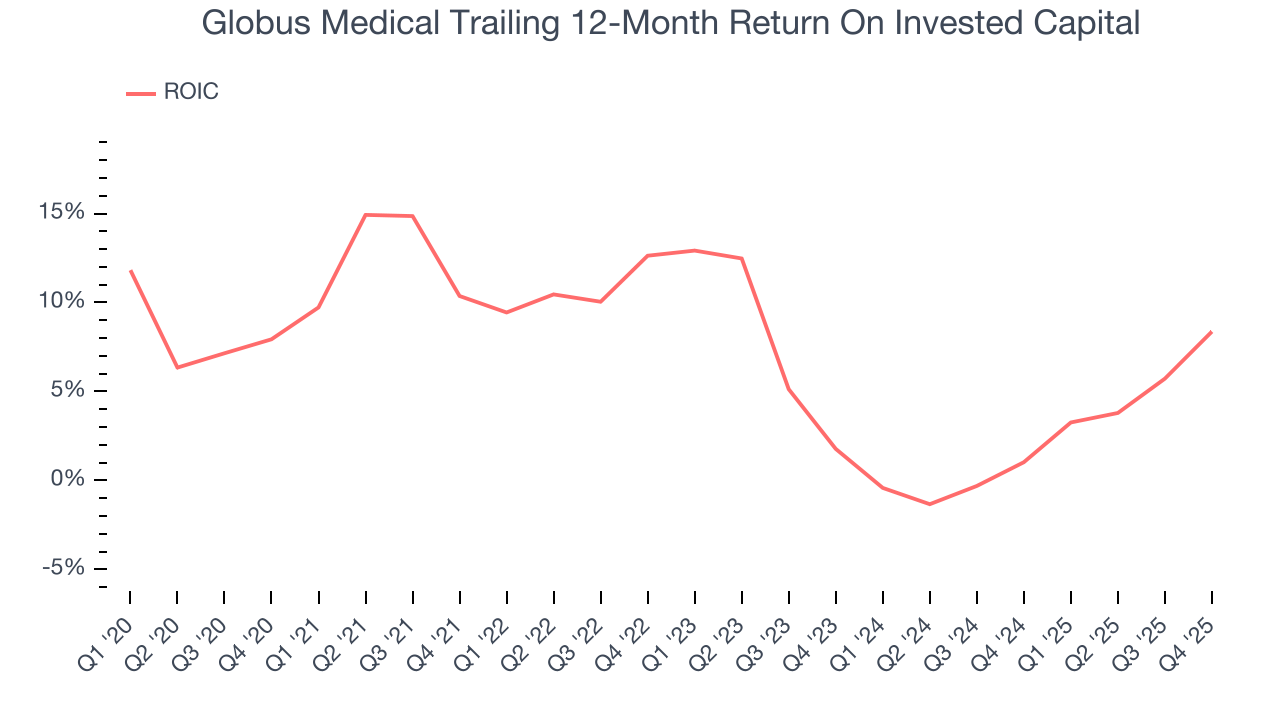

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Globus Medical has shown solid fundamentals lately, it historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 6.8%, somewhat low compared to the best healthcare companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Globus Medical’s ROIC has decreased over the last few years. If its returns keep falling, it could suggest its profitable growth opportunities are drying up. We’ll keep a close eye.

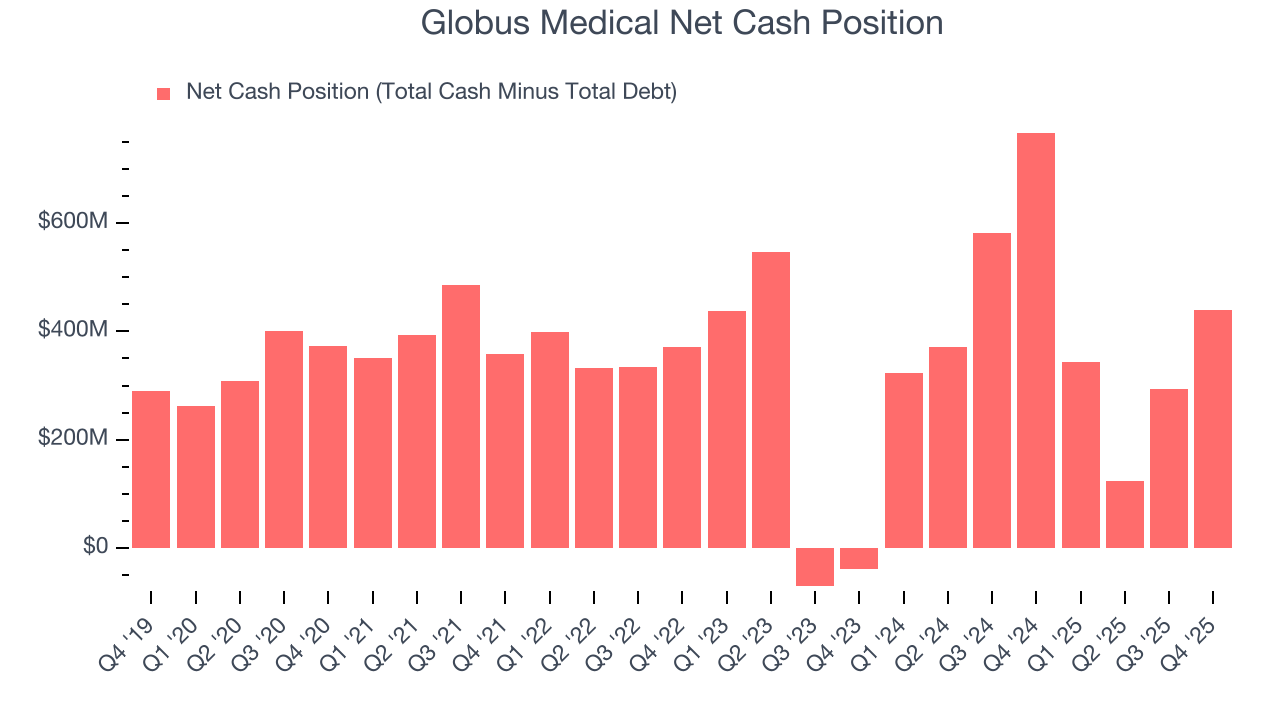

11. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Globus Medical is a profitable, well-capitalized company with $557.2 million of cash and $118.7 million of debt on its balance sheet. This $438.6 million net cash position is 3.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Globus Medical’s Q4 Results

We enjoyed seeing Globus Medical beat analysts’ full-year EPS guidance expectations this quarter. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 1.9% to $93.65 immediately following the results.

13. Is Now The Time To Buy Globus Medical?

Updated: March 14, 2026 at 11:56 PM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Globus Medical.

We think Globus Medical is a good business. To kick things off, its revenue growth was exceptional over the last five years. And while its diminishing returns show management's recent bets still have yet to bear fruit, its constant currency growth has been marvelous. On top of that, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Globus Medical’s P/E ratio based on the next 12 months is 18.9x. Looking at the healthcare space right now, Globus Medical trades at a compelling valuation. If you believe in the company and its growth potential, now is an opportune time to buy shares.

Wall Street analysts have a consensus one-year price target of $109.31 on the company (compared to the current share price of $84.80), implying they see 28.9% upside in buying Globus Medical in the short term.