Hamilton Insurance Group (HG)

Hamilton Insurance Group doesn’t impress us. Its sales and EPS are expected to be weak over the next year, which doesn’t bode well for its share price.― StockStory Analyst Team

1. News

2. Summary

Why Hamilton Insurance Group Is Not Exciting

Founded in 2013 and operating through three distinct underwriting platforms across four countries, Hamilton Insurance Group (NYSE:HG) operates global specialty insurance and reinsurance platforms across Lloyd's, Ireland, Bermuda, and the United States.

- Sales are projected to tank by 1.2% over the next 12 months as demand evaporates

- A consolation is that its market share has increased this cycle as its 27% annual revenue growth over the last three years was exceptional

Hamilton Insurance Group falls short of our expectations. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Hamilton Insurance Group

At $29.46 per share, Hamilton Insurance Group trades at 0.9x forward P/B. This multiple is lower than most insurance companies, but for good reason.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Hamilton Insurance Group (HG) Research Report: Q4 CY2025 Update

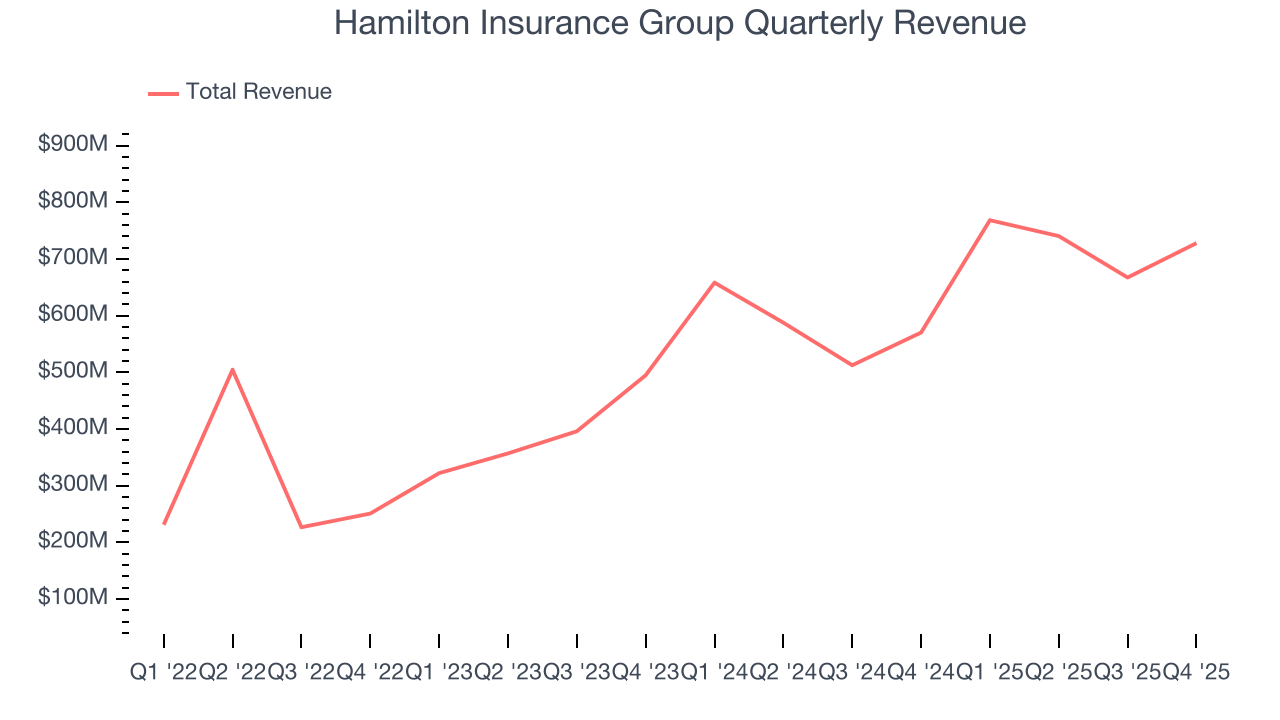

Specialty insurance company Hamilton Insurance Group (NYSE:HG) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 27.7% year on year to $728.3 million. Its non-GAAP profit of $1.65 per share was 56.4% above analysts’ consensus estimates.

Hamilton Insurance Group (HG) Q4 CY2025 Highlights:

- Net Premiums Earned: $576.7 million (19.7% year-on-year growth)

- Revenue: $728.3 million vs analyst estimates of $645.2 million (27.7% year-on-year growth, 12.9% beat)

- Combined Ratio: 87% vs analyst estimates of 86.8% (20 basis point miss)

- Adjusted EPS: $1.65 vs analyst estimates of $1.05 (56.4% beat)

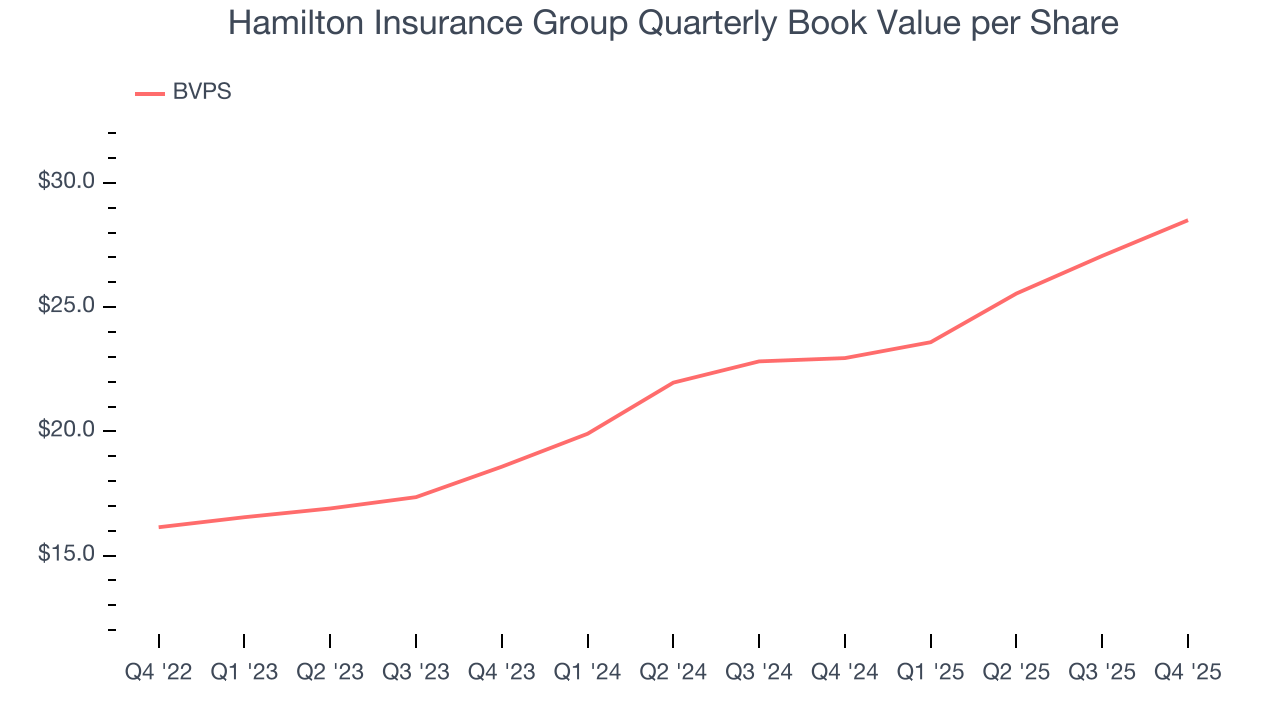

- Book Value per Share: $28.50 (24.2% year-on-year growth)

- Market Capitalization: $3 billion

Company Overview

Founded in 2013 and operating through three distinct underwriting platforms across four countries, Hamilton Insurance Group (NYSE:HG) operates global specialty insurance and reinsurance platforms across Lloyd's, Ireland, Bermuda, and the United States.

Hamilton structures its business into two main segments: International and Bermuda. The International segment includes Hamilton Global Specialty, which focuses on medium to large commercial accounts through Lloyd's Syndicate 4000 and its Irish subsidiary, and Hamilton Select, which serves the U.S. Excess & Surplus market for small to mid-sized hard-to-place risks. The Bermuda segment operates through Hamilton Re, writing property, casualty, and specialty reinsurance globally while also offering high excess insurance products primarily to large U.S. commercial clients.

The company's diverse product portfolio spans property coverage (including natural disaster protection), casualty lines (such as financial and professional liability, cyber, and excess casualty), and specialty insurance (covering risks like political violence, fine art, kidnap and ransom, and space satellites). For example, a multinational corporation might use Hamilton's directors and officers liability coverage to protect its leadership from lawsuits, while an energy company might purchase its upstream energy insurance to cover offshore drilling operations.

Hamilton generates revenue by collecting premiums for the risks it underwrites, with distribution primarily through insurance brokers, managing general agents, and wholesale channels. The company employs a disciplined underwriting approach, strategically using reinsurance to protect its capital and reduce exposure to large loss events. This balanced approach to risk management allows Hamilton to operate across multiple geographies and insurance markets while maintaining financial stability.

4. Reinsurance

This is a cyclical industry, and the sector benefits when there is 'hard market', characterized by strong premium rate increases that outpace loss and cost inflation, resulting in robust underwriting margins. The opposite is true in a 'soft market'. Interest rates also matter, as they determine the yields earned on fixed-income portfolios. The primary headwind remains the immense and concentrated exposure to large-scale catastrophe losses, as the growing impact of climate change challenges traditional risk models and creates significant earnings volatility. Additionally, they face the risk of adverse prior-year reserve development, where claims prove more costly than anticipated, while the eventual influx of new capital from alternative sources threatens to soften the market and compress future returns.

Hamilton Insurance Group competes with established specialty insurers and reinsurers including Arch Capital Group Ltd., AXIS Capital Holdings Limited, Beazley plc, Hiscox Ltd, Lancashire Holdings Limited, Markel Corporation, and RenaissanceRe Holdings Ltd., as well as various Lloyd's syndicates that operate in the specialty insurance market.

5. Revenue Growth

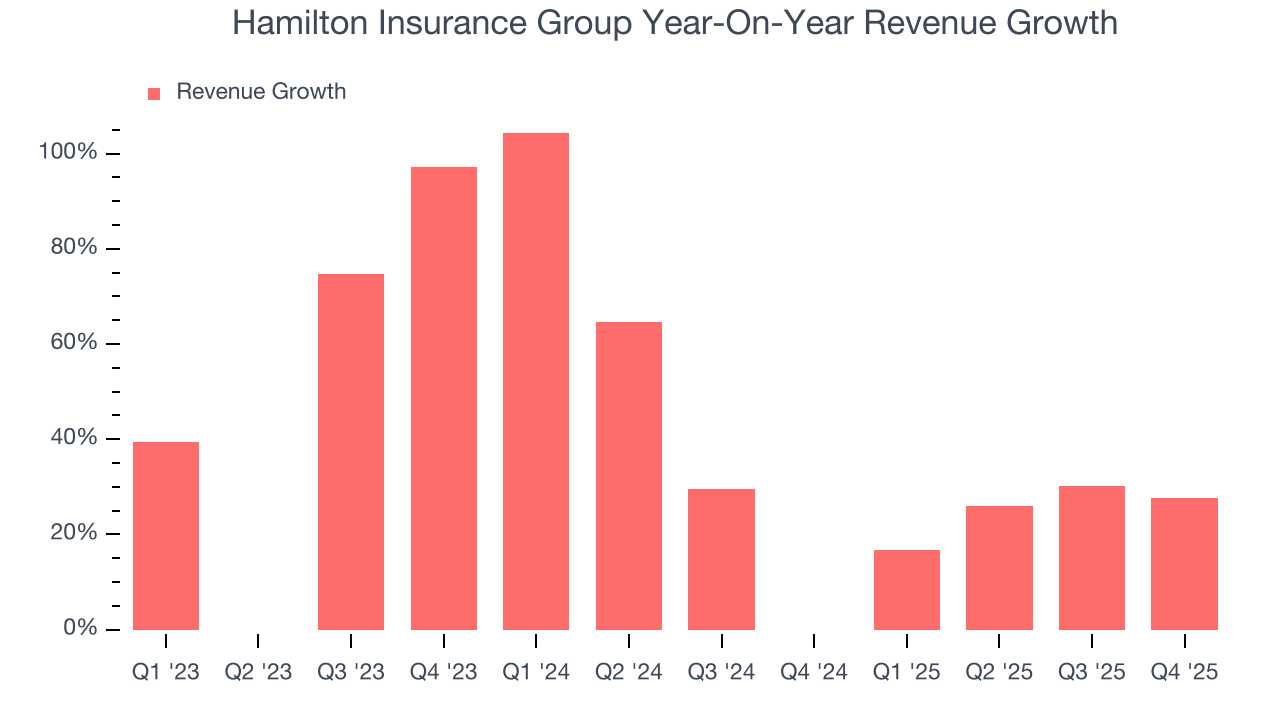

Insurers earn revenue three ways. The core insurance business itself, often called underwriting and represented in the income statement as premiums earned, is one way. Investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities is the second way. Fees from various sources such as policy administration, annuities, or other value-added services is the third. Luckily, Hamilton Insurance Group’s revenue grew at an incredible 27% compounded annual growth rate over the last three years. Its growth beat the average insurance company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Hamilton Insurance Group’s annualized revenue growth of 36% over the last two years is above its three-year trend, suggesting its demand was strong and recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Hamilton Insurance Group reported robust year-on-year revenue growth of 27.7%, and its $728.3 million of revenue topped Wall Street estimates by 12.9%.

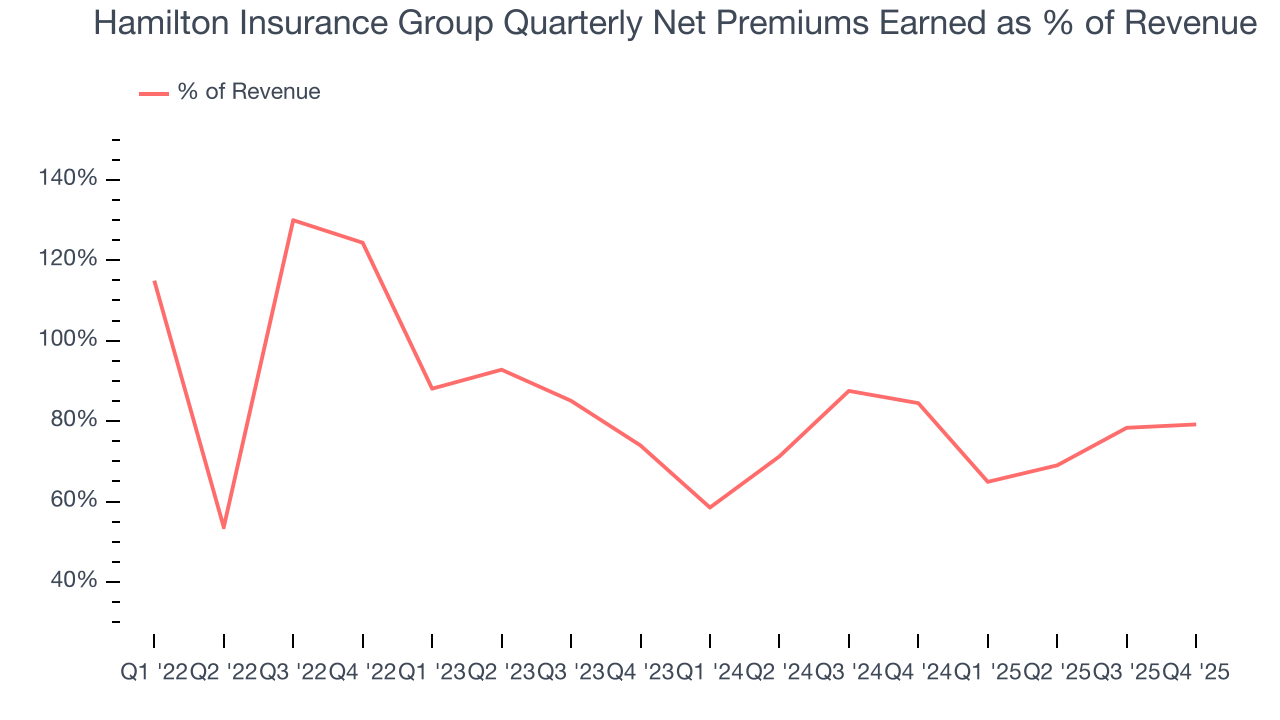

Net premiums earned made up 78.6% of the company’s total revenue during the last four years, meaning insurance operations are Hamilton Insurance Group’s largest source of revenue.

Markets consistently prioritize net premiums earned growth over investment and fee income, recognizing its superior quality as a core indicator of the company’s underwriting success and market penetration.

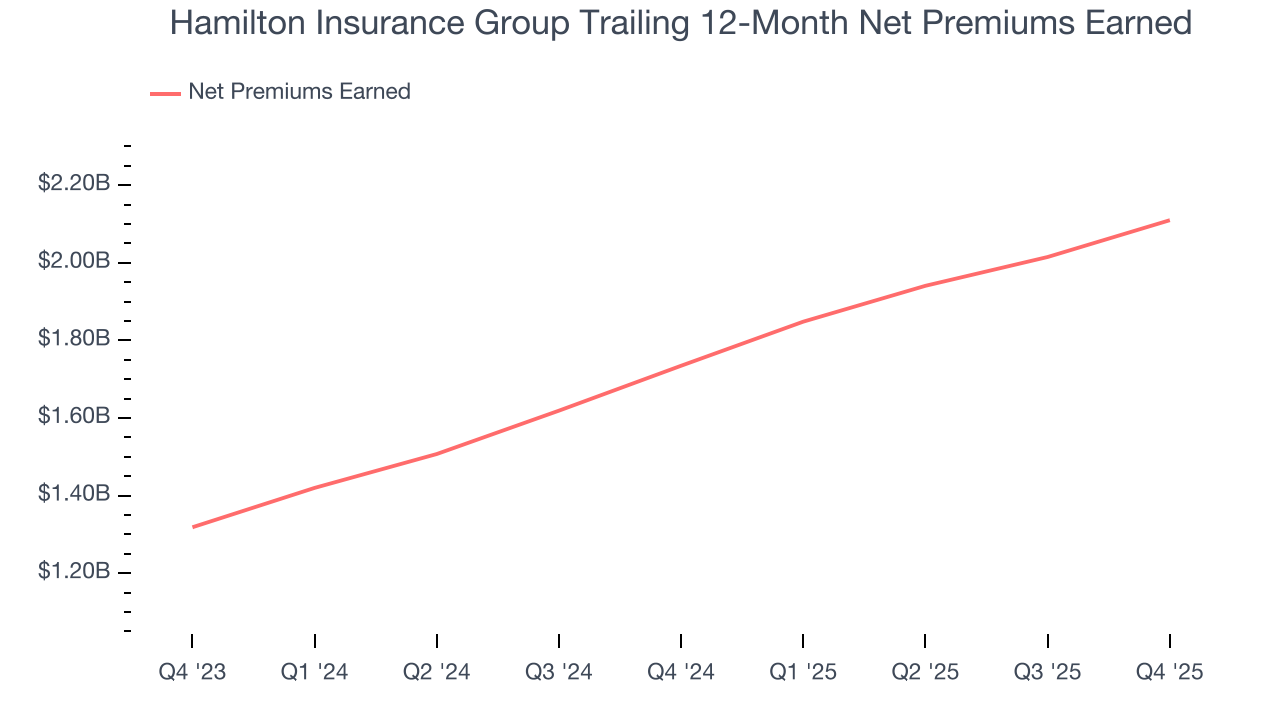

6. Net Premiums Earned

Net premiums earned are net of what’s paid to reinsurers (insurance for insurance companies), which are used by insurers to protect themselves from large losses.

Hamilton Insurance Group’s net premiums earned has grown at a 23.5% annualized rate over the last three years, much better than the broader insurance industry but slower than its total revenue.

When analyzing Hamilton Insurance Group’s net premiums earned over the last two years, we can see that growth accelerated to 26.5% annually. Since two-year net premiums earned grew slower than total revenue over this period, it’s implied that other line items such as investment income grew at a faster rate. These extra revenue streams are important to the bottom line, yet their performance can be inconsistent. Some firms have been more successful and consistent in managing their float, but sharp fluctuations in the fixed income and equity markets can dramatically affect short-term results.

Hamilton Insurance Group’s net premiums earned came in at $576.7 million this quarter, up a hearty 19.7% year on year.

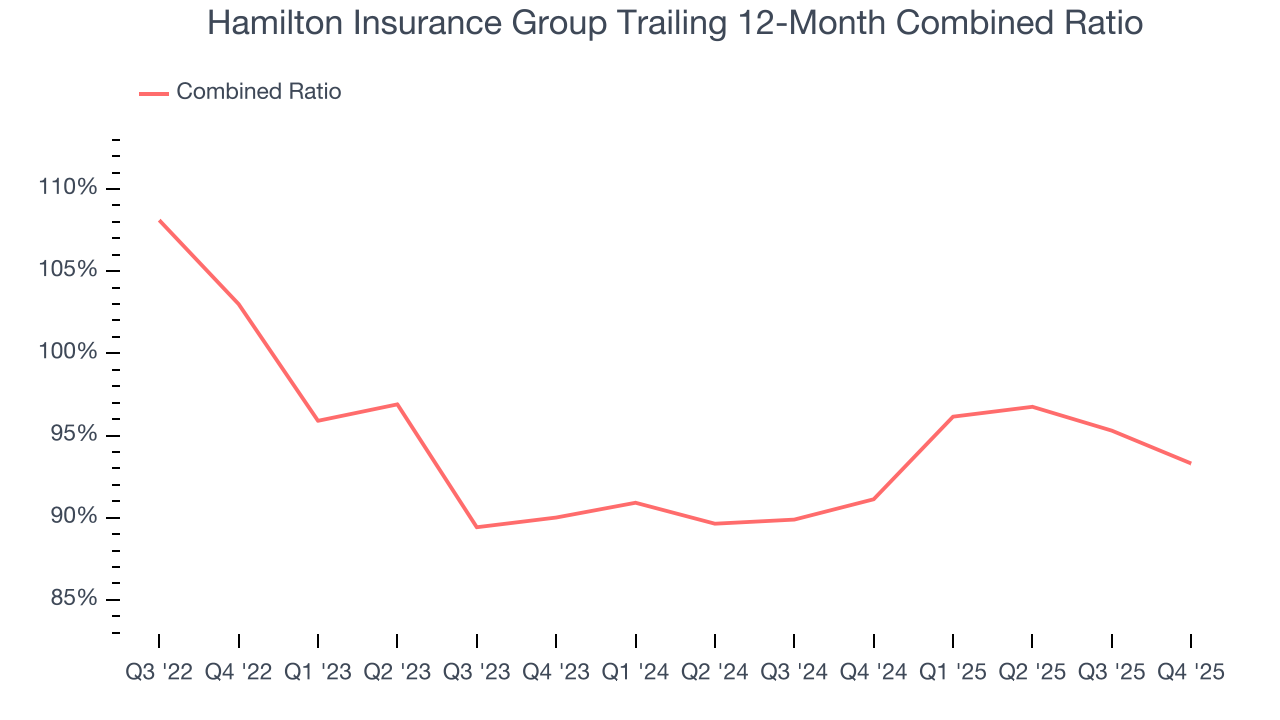

7. Combined Ratio

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For insurance companies, we look at the combined ratio rather than the operating expenses and margins that define sectors such as consumer, tech, and industrials.

The combined ratio is:

- The costs of underwriting (salaries, commissions, overhead) + what an insurer pays out in claims, all divided by net premiums earned

If a company boasts a combined ratio under 100%, it is underwriting profitably. If above 100%, it is losing money on its core operations of selling insurance policies.

Given the calculation, a lower expense ratio is better. Over the last two years, Hamilton Insurance Group’s combined ratio has increased by 3.3 percentage points, going from 90% to 93.3%. Said differently, the company’s expenses have increased at a faster rate than revenue, which usually raises questions unless the company is in high-growth mode and reinvesting its profits into attractive ventures.

In Q4, Hamilton Insurance Group’s combined ratio was 87%, close to analysts’ expectations. This result was 8 percentage points better than the same quarter last year.

8. Book Value Per Share (BVPS)

Insurers are balance sheet businesses, collecting premiums upfront and paying out claims over time. Premiums collected but not yet paid out, often referred to as the float, are invested and create an asset base supported by a liability structure. Book value per share (BVPS) captures this dynamic by measuring these assets (investment portfolio, cash, reinsurance recoverables) less liabilities (claim reserves, debt, future policy benefits). BVPS is essentially the residual value for shareholders.

We therefore consider BVPS very important to track for insurers and a metric that sheds light on business quality because it reflects long-term capital growth and is harder to manipulate than more commonly-used metrics like EPS.

To investors’ benefit, Hamilton Insurance Group’s BVPS grew at an exceptional 23.9% annual clip over the last two years.

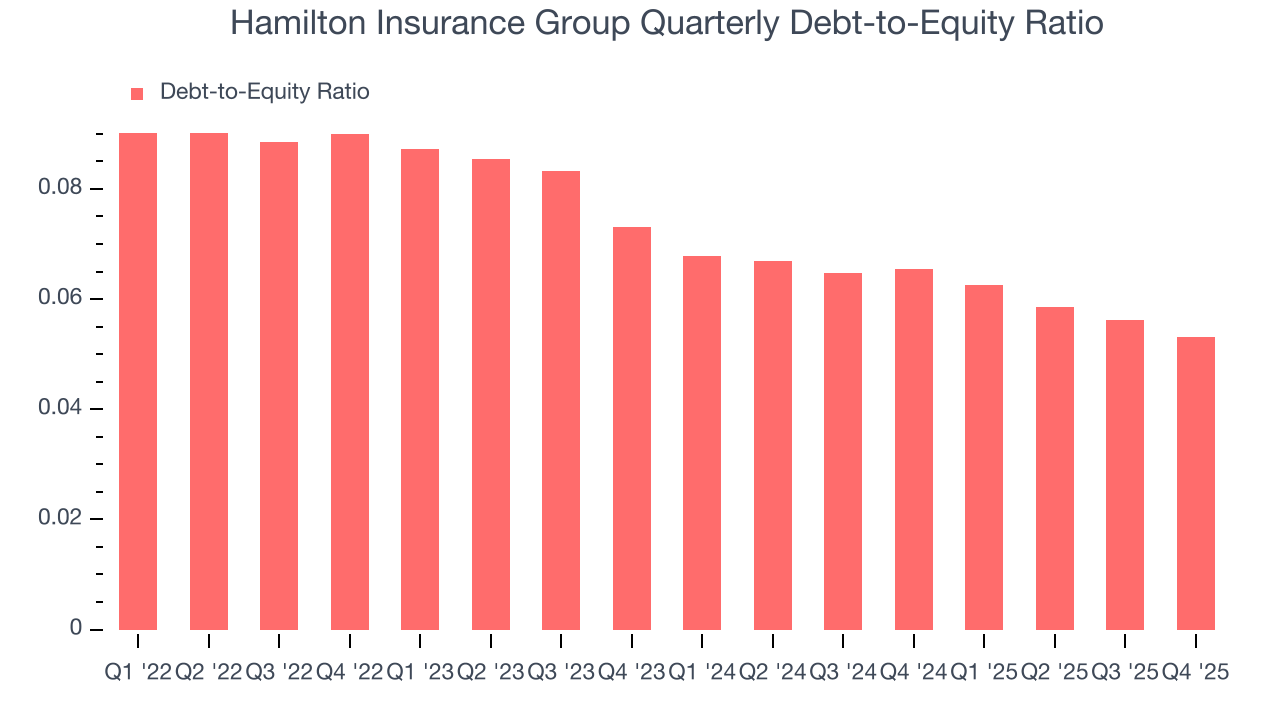

9. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Hamilton Insurance Group currently has $149.7 million of debt and $2.82 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.1×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 1.0× for an insurance business. Anything below 0.5× is a bonus.

10. Key Takeaways from Hamilton Insurance Group’s Q4 Results

It was good to see Hamilton Insurance Group beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a solid print. The stock traded up 6.2% to $31.15 immediately after reporting.

11. Is Now The Time To Buy Hamilton Insurance Group?

Updated: March 25, 2026 at 12:32 AM EDT

Are you wondering whether to buy Hamilton Insurance Group or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Hamilton Insurance Group doesn’t top our investment wishlist, but we understand that it’s not a bad business. First off, its revenue growth was exceptional over the last three years. And while Hamilton Insurance Group’s projected EPS for the next year is lacking, its net premiums earned growth was exceptional over the last three years.

Hamilton Insurance Group’s P/B ratio based on the next 12 months is 0.9x. While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $32.86 on the company (compared to the current share price of $29.46).