Howmet (HWM)

Howmet is an amazing business. It generates heaps of cash that are reinvested into the business, creating a virtuous cycle of returns.― StockStory Analyst Team

1. News

2. Summary

Why We Like Howmet

Inventing the first forged aluminum truck wheel, Howmet (NYSE:HWM) specializes in lightweight metals engineering and manufacturing multi-material components used in vehicles.

- Performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 21.6% outpaced its revenue gains

- Excellent operating margin highlights the strength of its business model, and its operating leverage amplified its profits over the last five years

- Robust free cash flow profile gives it the flexibility to invest in growth initiatives or return capital to shareholders, and its rising cash conversion increases its margin of safety

We’re optimistic about Howmet. No coincidence the stock is up 730% over the last five years.

Is Now The Time To Buy Howmet?

Howmet is trading at $207.85 per share, or 49.7x forward P/E. The pricey valuation means expectations are high for this company over the near to medium term.

Are you a fan of the company and believe in the bull case? If so, you can own a smaller position, as high-quality companies tend to outperform the market over a long-term period regardless of entry price.

3. Howmet (HWM) Research Report: Q3 CY2025 Update

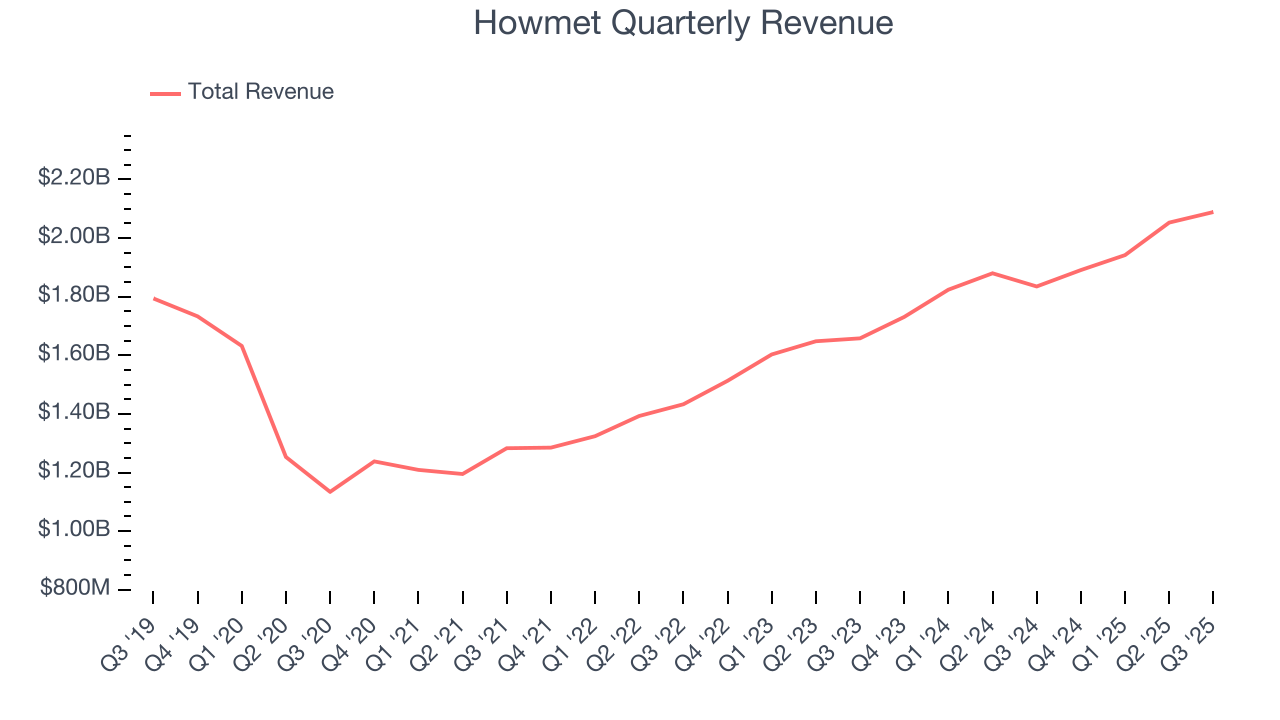

Aerospace and defense company Howmet (NYSE:HWM) reported Q3 CY2025 results exceeding the market’s revenue expectations, with sales up 13.8% year on year to $2.09 billion. The company expects next quarter’s revenue to be around $2.1 billion, close to analysts’ estimates. Its non-GAAP profit of $0.95 per share was 4.5% above analysts’ consensus estimates.

Howmet (HWM) Q3 CY2025 Highlights:

- Revenue: $2.09 billion vs analyst estimates of $2.04 billion (13.8% year-on-year growth, 2.3% beat)

- Adjusted EPS: $0.95 vs analyst estimates of $0.91 (4.5% beat)

- Adjusted EBITDA: $614 million vs analyst estimates of $588.6 million (29.4% margin, 4.3% beat)

- Revenue Guidance for Q4 CY2025 is $2.1 billion at the midpoint, roughly in line with what analysts were expecting

- Management raised its full-year Adjusted EPS guidance to $3.67 at the midpoint, a 1.9% increase

- EBITDA guidance for the full year is $2.38 billion at the midpoint, above analyst estimates of $2.34 billion

- Operating Margin: 25.9%, up from 22.9% in the same quarter last year

- Free Cash Flow Margin: 20.2%, up from 8.8% in the same quarter last year

- Market Capitalization: $82.03 billion

Company Overview

Inventing the first forged aluminum truck wheel, Howmet (NYSE:HWM) specializes in lightweight metals engineering and manufacturing multi-material components used in vehicles.

Howmet Aerospace originated in 1920, focusing initially on metal fabrication before transitioning to components for jet engines and gas turbines. The company grew through acquisitions and strategic expansions, enhancing its technological and production capabilities. In 2000, Howmet merged with Alcoa, joining its engineered products and solutions segment, which significantly boosted its resources for precision engineering. The company became part of Arconic after Alcoa split into two entities in 2016. In 2020, Arconic further divided into Howmet Aerospace and Arconic Corporation, allowing each entity to specialize on its core operations. Today, Howmet Aerospace stands as a provider of advanced engineered solutions for the aerospace and transportation industries, known for its critical role in developing technologies essential for modern aircraft and industrial applications.

Howmet Aerospace offers a comprehensive range of high-performance components and engineered products tailored primarily for the aerospace and commercial transportation industries. The product lineup includes everything from precision-engineered jet engine components utilized in both commercial and defense aviation, to aerospace fastening systems that enhance aircraft efficiency and safety. Additionally, Howmet is known for its pioneering forged aluminum wheels, which significantly reduce weight and fuel consumption in commercial vehicles. Further, Howmet provides advanced airfoils and coatings capable of withstanding extreme temperatures, along with structural parts crafted from titanium and nickel superalloys for the aerospace sector.

Howmet Aerospace generates revenue through the sale of its engineered products. The company's largest revenue source is from the aerospace sector, complemented by revenue from the commercial transportation industry. Revenue is also derived from contracts with the U.S. government as well as foreign government agencies. Additionally, Howmet offers aftermarket services, including repair and maintenance for aerospace products, contributing to recurring revenue streams. The company also extends its market reach to industrial sectors such as gas turbines, oil and gas, providing a diverse income base. These revenue streams are supported by long-term contracts and partnerships with key industry players, providing some visibility into future earnings.

4. Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Howmet’s competitors include Boeing (NYSE:BA), Lockheed Martin (NYSE:LMT), and TransDigm (NYSE:TDG)

5. Revenue Growth

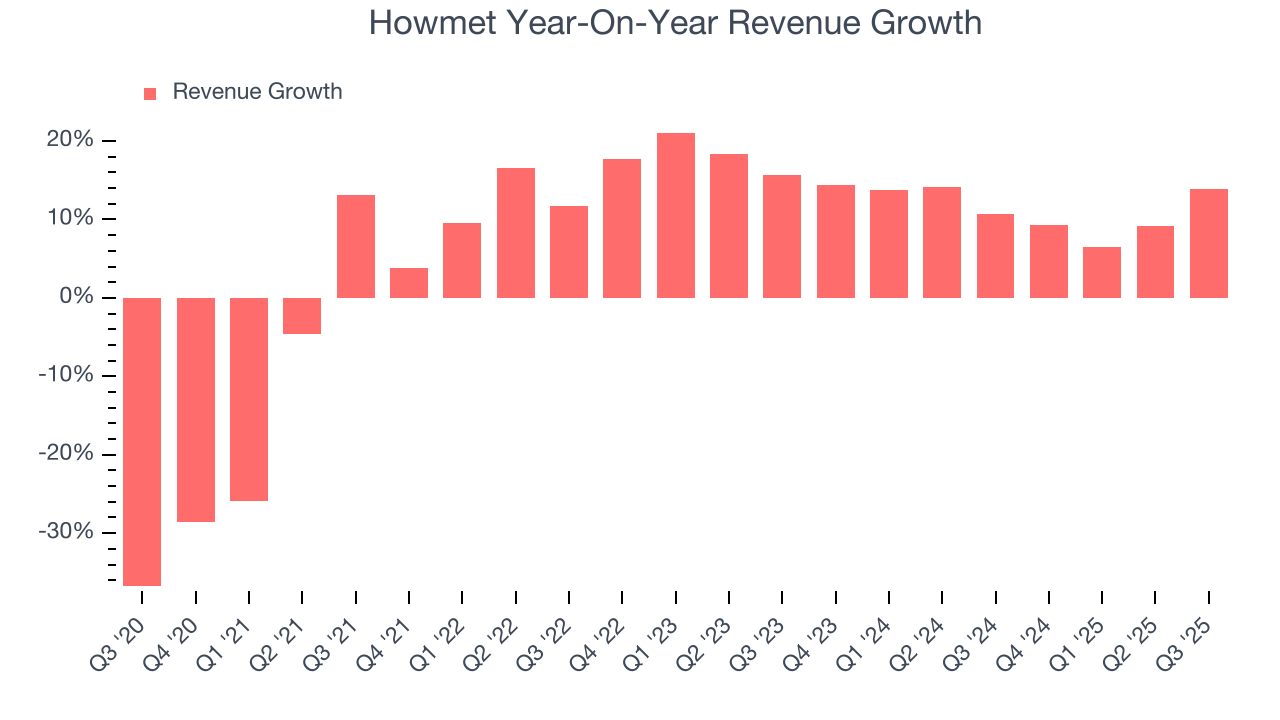

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Howmet’s 6.8% annualized revenue growth over the last five years was mediocre. This wasn’t a great result compared to the rest of the industrials sector, but there are still things to like about Howmet.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Howmet’s annualized revenue growth of 11.4% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

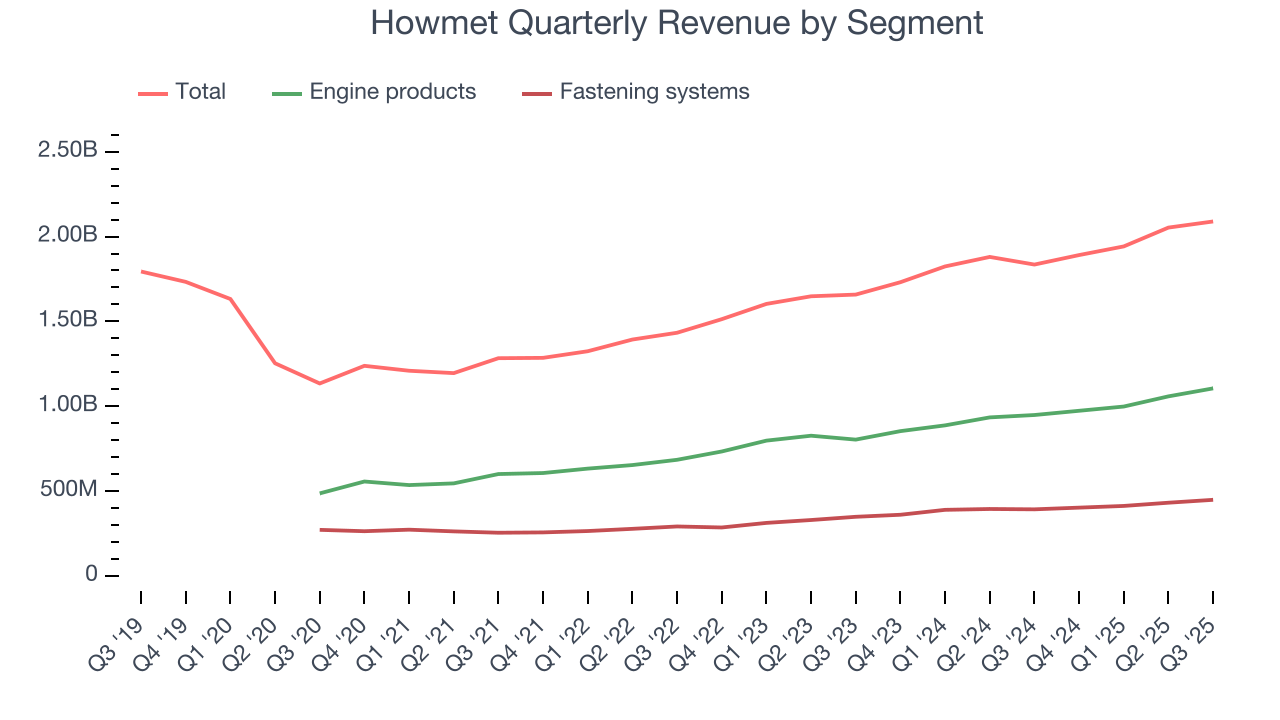

We can better understand the company’s revenue dynamics by analyzing its most important segments, Engine products and Fastening systems, which are 52.9% and 21.4% of revenue. Over the last two years, Howmet’s Engine products revenue (aircraft engines, industrial turbines) averaged 14.4% year-on-year growth while its Fastening systems revenue (connector products and tools) averaged 15.6% growth.

This quarter, Howmet reported year-on-year revenue growth of 13.8%, and its $2.09 billion of revenue exceeded Wall Street’s estimates by 2.3%. Company management is currently guiding for a 11.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.8% over the next 12 months, a slight deceleration versus the last two years. Still, this projection is admirable and indicates the market is forecasting success for its products and services.

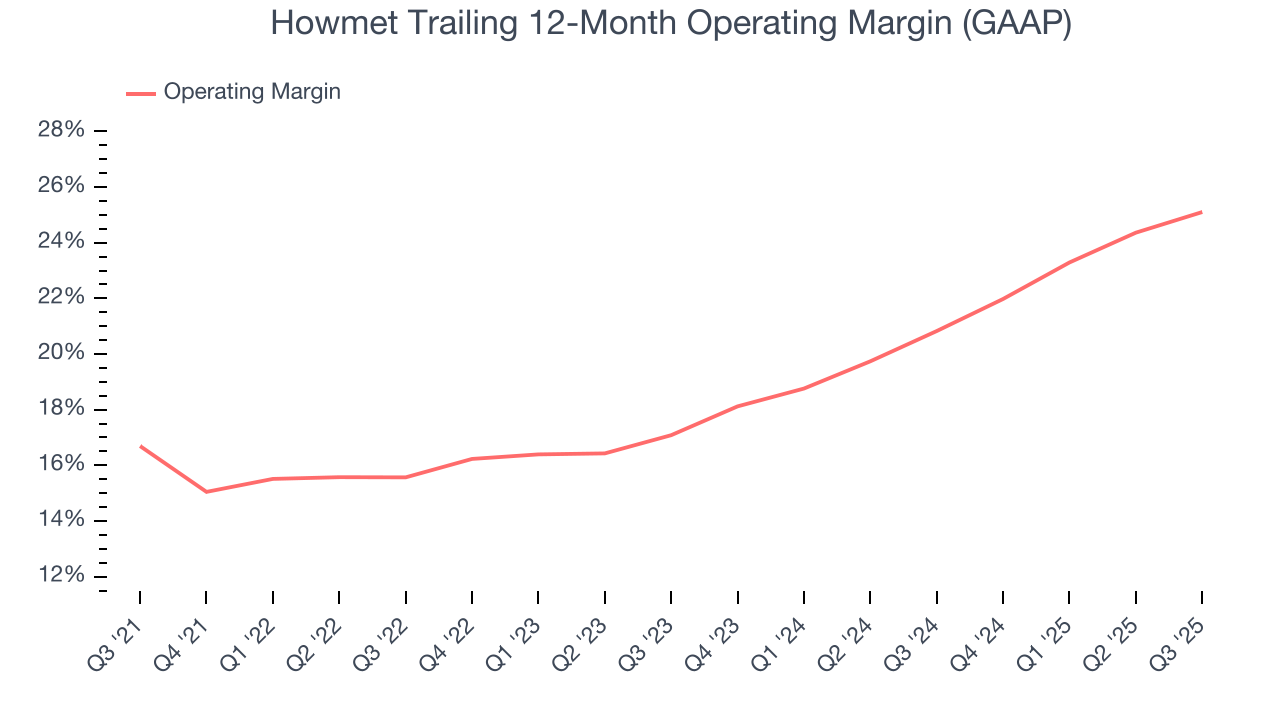

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Howmet has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 19.6%.

Analyzing the trend in its profitability, Howmet’s operating margin rose by 8.4 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q3, Howmet generated an operating margin profit margin of 25.9%, up 3 percentage points year on year. This increase was a welcome development and shows it was more efficient.

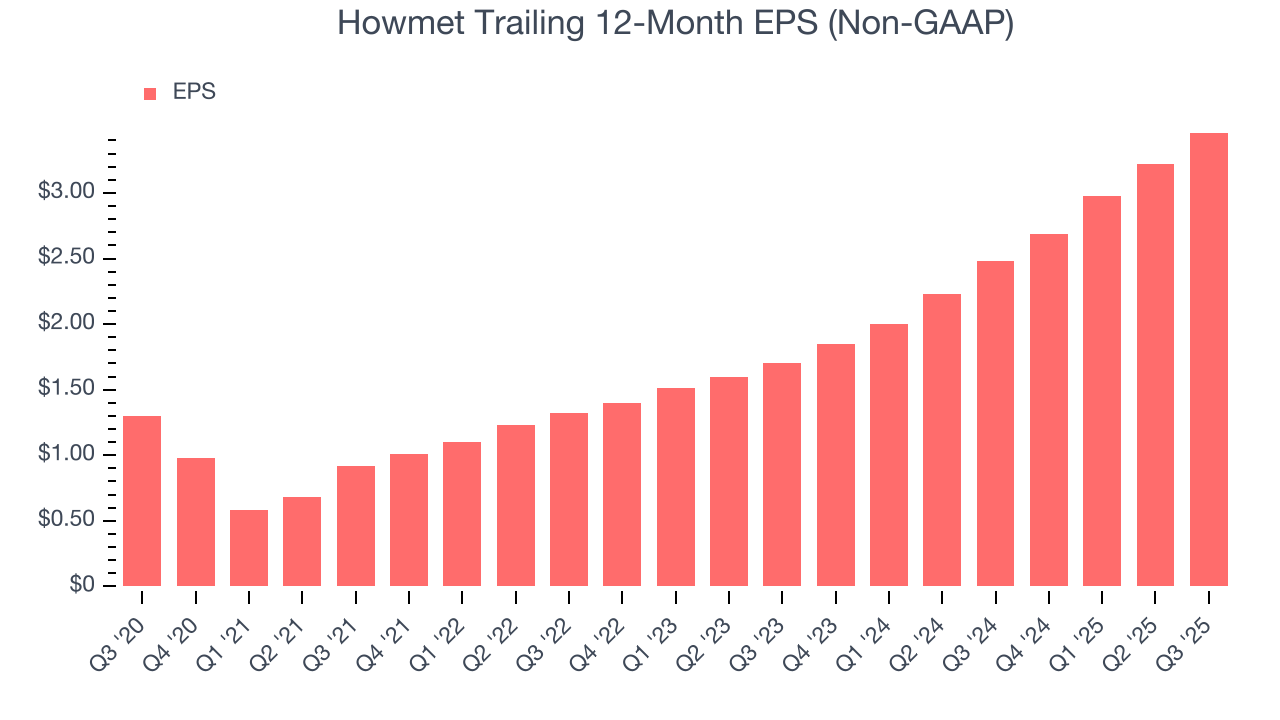

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Howmet’s EPS grew at an astounding 21.6% compounded annual growth rate over the last five years, higher than its 6.8% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

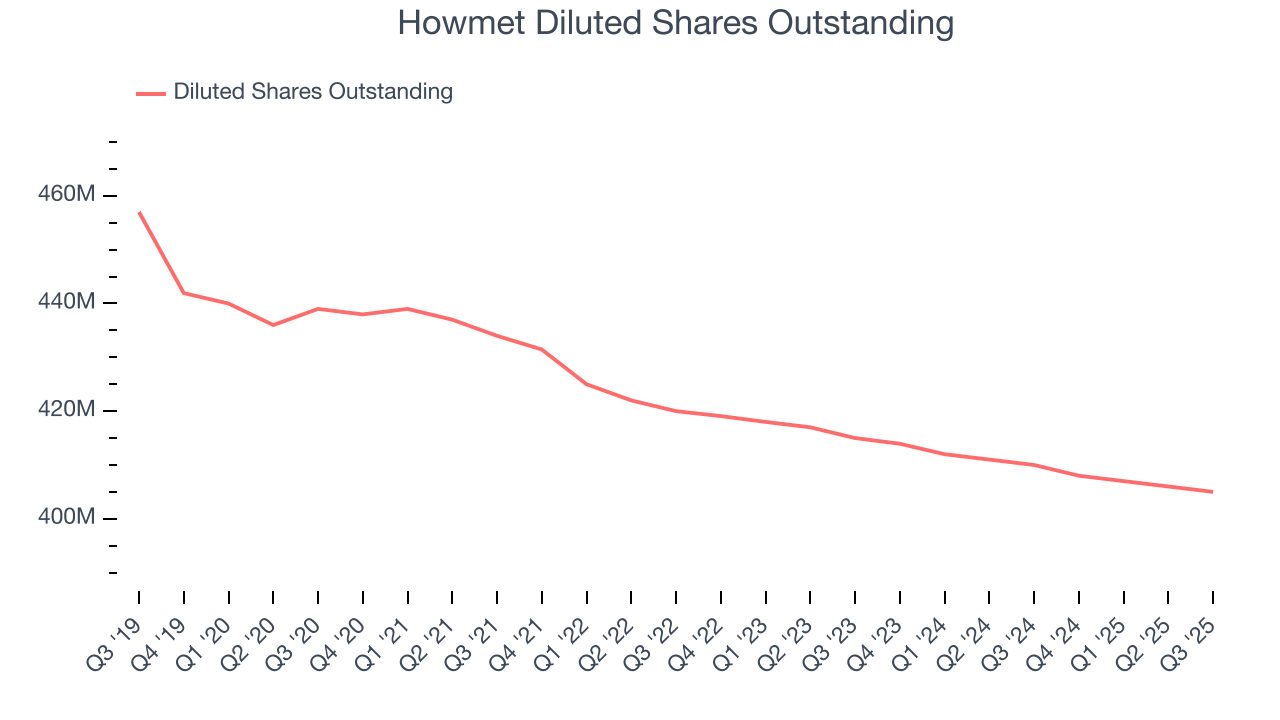

Diving into the nuances of Howmet’s earnings can give us a better understanding of its performance. As we mentioned earlier, Howmet’s operating margin expanded by 8.4 percentage points over the last five years. On top of that, its share count shrank by 7.7%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Howmet, its two-year annual EPS growth of 42.7% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q3, Howmet reported adjusted EPS of $0.95, up from $0.71 in the same quarter last year. This print beat analysts’ estimates by 4.5%. Over the next 12 months, Wall Street expects Howmet’s full-year EPS of $3.46 to grow 18.1%.

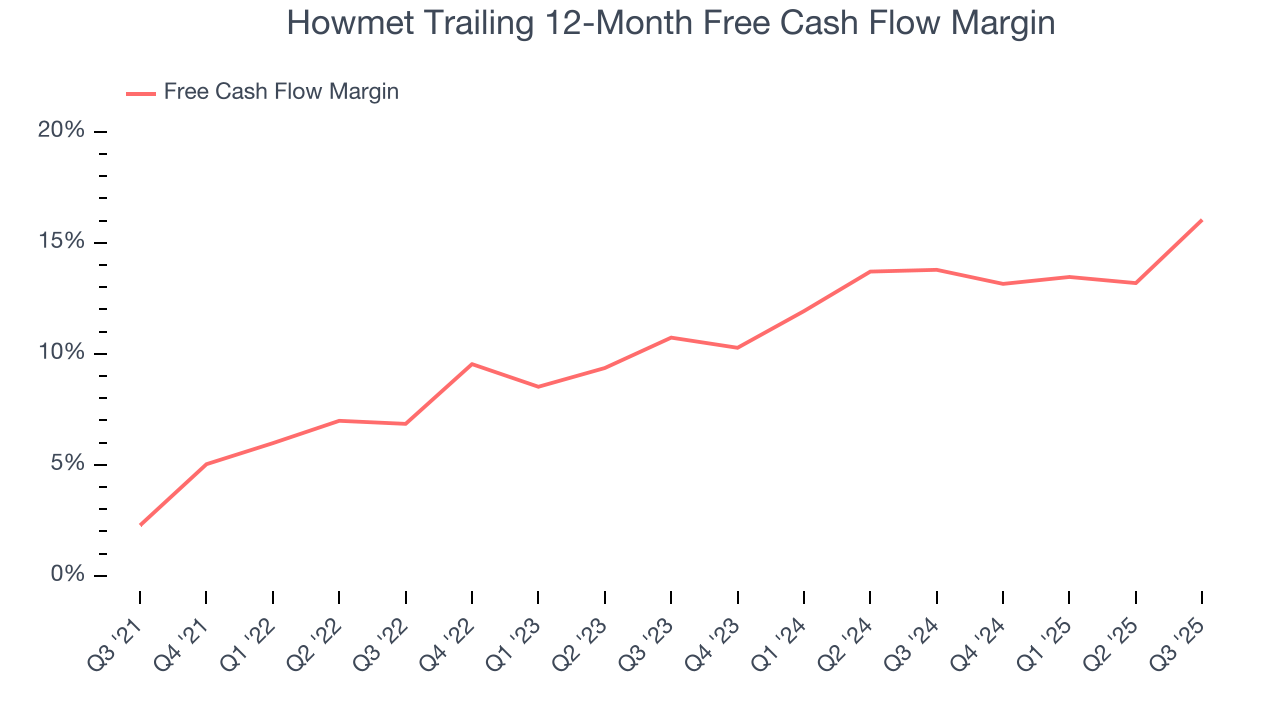

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Howmet has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 10.8% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Howmet’s margin expanded by 13.8 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Howmet’s free cash flow clocked in at $423 million in Q3, equivalent to a 20.2% margin. This result was good as its margin was 11.4 percentage points higher than in the same quarter last year, building on its favorable historical trend.

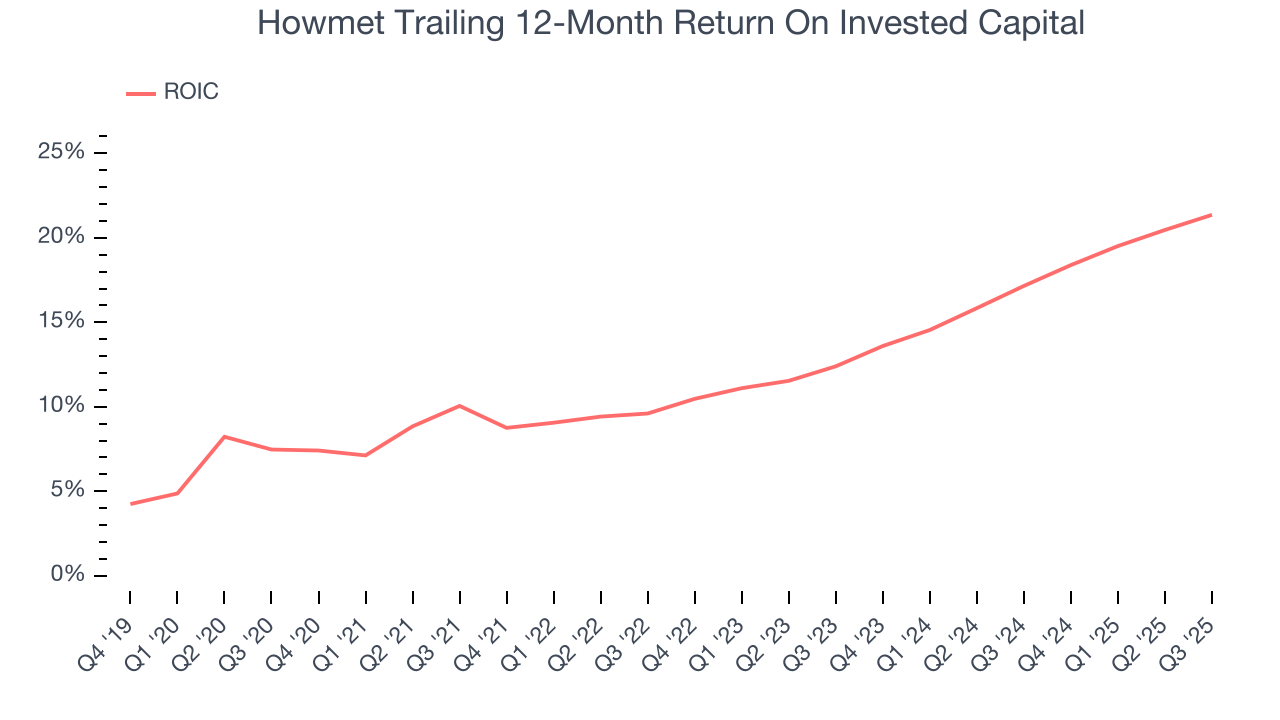

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Howmet’s five-year average ROIC was 14.1%, beating other industrials companies by a wide margin. This illustrates its management team’s ability to invest in attractive growth opportunities and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Howmet’s has increased over the last few years. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

10. Balance Sheet Assessment

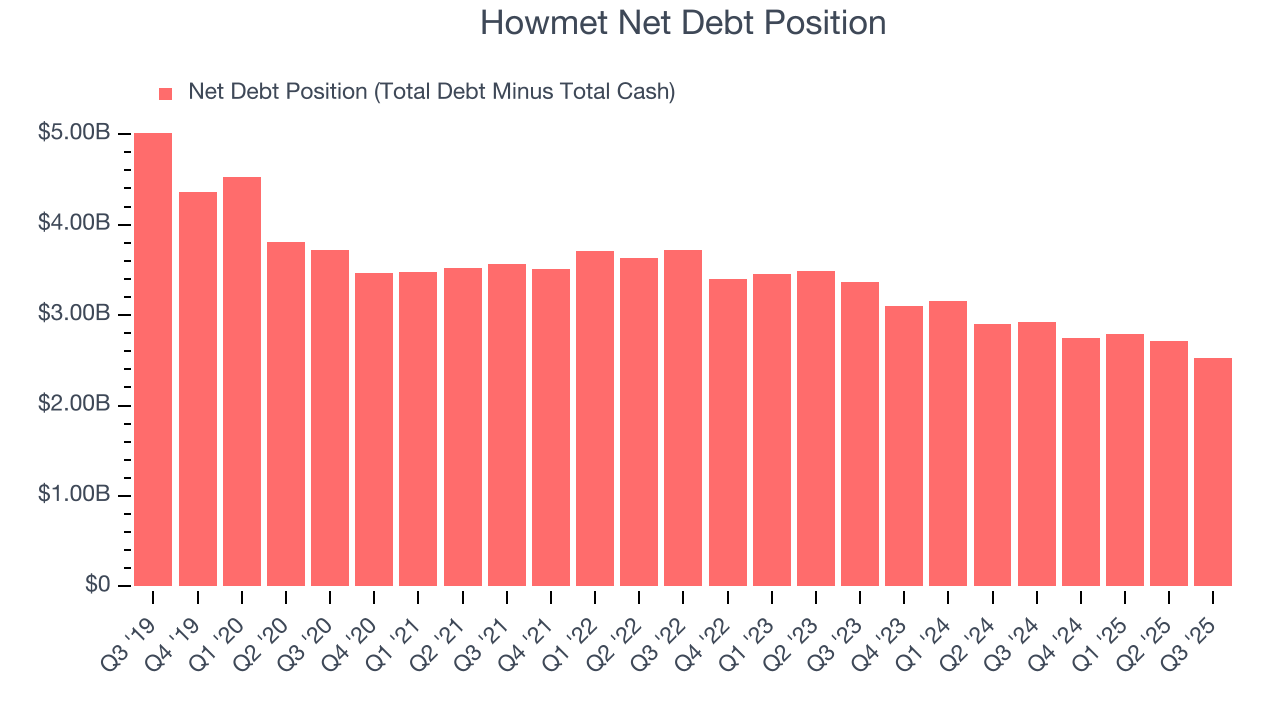

Howmet reported $659 million of cash and $3.19 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $2.27 billion of EBITDA over the last 12 months, we view Howmet’s 1.1× net-debt-to-EBITDA ratio as safe. We also see its $67 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Howmet’s Q3 Results

Revenue and EBITDA in the quarter exceeded expectations. While revenue guidance for next quarter was only in line, full-year EBITDA guidance came in ahead of expectations. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 3.5% to $196.60 immediately following the results.

12. Is Now The Time To Buy Howmet?

Updated: January 30, 2026 at 10:04 PM EST

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Howmet.

Howmet is an amazing business ranking highly on our list. Although its revenue growth was mediocre over the last five years, its growth over the next 12 months is expected to be higher. Plus, its impressive operating margins show it has a highly efficient business model, and its rising cash profitability gives it more optionality.

Howmet’s P/E ratio based on the next 12 months is 49.7x. Expectations are high given its premium multiple, but we’ll happily own Howmet as its fundamentals illustrate it’s clearly doing something special. It’s often wise to hold investments like this for at least three to five years, as the power of long-term compounding negates short-term price swings that can accompany high valuations.

Wall Street analysts have a consensus one-year price target of $246.75 on the company (compared to the current share price of $207.85).