Jabil (JBL)

Jabil doesn’t excite us. Its underwhelming revenue growth and failure to generate meaningful free cash flow is a concerning trend.― StockStory Analyst Team

1. News

2. Summary

Why Jabil Is Not Exciting

With manufacturing facilities spanning the globe from China to Mexico to the United States, Jabil (NYSE:JBL) provides electronics design, manufacturing, and supply chain solutions to companies across various industries, from healthcare to automotive to cloud computing.

- Large revenue base makes it harder to increase sales quickly, and its annual revenue growth of 2.4% over the last five years was below our standards for the business services sector

- Poor expense management has led to an adjusted operating margin that is below the industry average

- The good news is that its massive revenue base of $31.11 billion makes it a well-known name that influences purchasing decisions

Jabil doesn’t live up to our standards. More profitable opportunities exist elsewhere.

Why There Are Better Opportunities Than Jabil

Jabil is trading at $266.16 per share, or 21.5x forward P/E. Not only is Jabil’s multiple richer than most business services peers, but it’s also expensive for its revenue characteristics.

We prefer to invest in similarly-priced but higher-quality companies with superior earnings growth.

3. Jabil (JBL) Research Report: Q1 CY2026 Update

Electronics manufacturing services provider Jabil (NYSE:JBL) beat Wall Street’s revenue expectations in Q1 CY2026, with sales up 23.1% year on year to $8.28 billion. On top of that, next quarter’s revenue guidance ($8.5 billion at the midpoint) was surprisingly good and 6% above what analysts were expecting. Its non-GAAP profit of $2.69 per share was 7.2% above analysts’ consensus estimates.

Jabil (JBL) Q1 CY2026 Highlights:

- Revenue: $8.28 billion vs analyst estimates of $7.75 billion (23.1% year-on-year growth, 6.8% beat)

- Adjusted EPS: $2.69 vs analyst estimates of $2.51 (7.2% beat)

- The company lifted its revenue guidance for the full year to $34 billion at the midpoint from $32.4 billion, a 4.9% increase

- Management raised its full-year Adjusted EPS guidance to $12.25 at the midpoint, a 6.1% increase

- Operating Margin: 4.5%, in line with the same quarter last year

- Free Cash Flow Margin: 4.3%, similar to the same quarter last year

- Market Capitalization: $27.7 billion

Company Overview

With manufacturing facilities spanning the globe from China to Mexico to the United States, Jabil (NYSE:JBL) provides electronics design, manufacturing, and supply chain solutions to companies across various industries, from healthcare to automotive to cloud computing.

Jabil operates as a manufacturing partner for thousands of companies, handling everything from initial product design to final assembly and distribution. The company's services help clients reduce time-to-market, manage inventory more efficiently, and optimize their supply chains without having to build and maintain their own manufacturing infrastructure.

The company is organized into three main segments: Regulated Industries (serving automotive, healthcare, and renewable energy markets), Intelligent Infrastructure (supporting AI infrastructure, cloud data centers, and networking), and Connected Living and Digital Commerce (focusing on consumer products and retail automation).

When a medical device company needs to produce a new health monitoring system, for example, Jabil might handle the entire process—designing the electronics, sourcing components, manufacturing the device, testing it for quality, and even managing distribution to hospitals or retailers.

Jabil's revenue comes from manufacturing contracts with clients across diverse industries. The company maintains long-term relationships with major technology and industrial companies, with Apple being one of its largest customers. Its global manufacturing footprint allows clients to produce products in optimal locations based on cost, logistics, and market access considerations.

Beyond basic manufacturing, Jabil offers specialized design services including electronic hardware design, mechanical engineering, optical systems development, and user experience design. The company has evolved from a traditional electronics manufacturer to a comprehensive solutions provider, helping clients navigate complex technologies like artificial intelligence, electrification, and advanced healthcare devices.

4. Electronic Components & Manufacturing

The sector could see higher demand as the prevalence of advanced electronics increases in industries such as automotive, healthcare, aerospace, and computing. The high-performance components and contract manufacturing expertise required for autonomous vehicles and cloud computing datacenters, for instance, will benefit companies in the space. However, headwinds include geopolitical risks, particularly U.S.-China trade tensions that could disrupt component sourcing and production as the Trump administration takes an increasingly antagonizing stance on foreign relations. Additionally, stringent environmental regulations on e-waste and emissions could force the industry to pivot in potentially costly ways.

Jabil competes with other electronics manufacturing services providers including Foxconn (TPE:2317), Flex Ltd. (NASDAQ:FLEX), Sanmina Corporation (NASDAQ:SANM), and Celestica Inc. (NYSE:CLS).

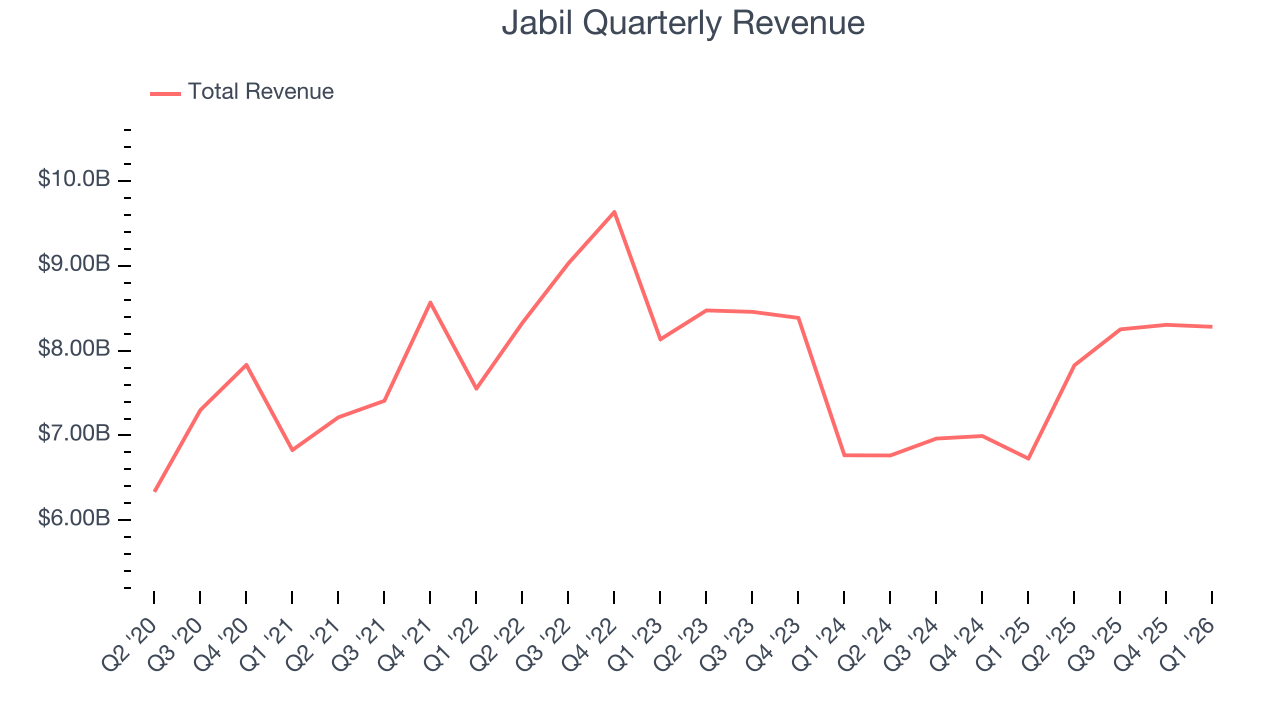

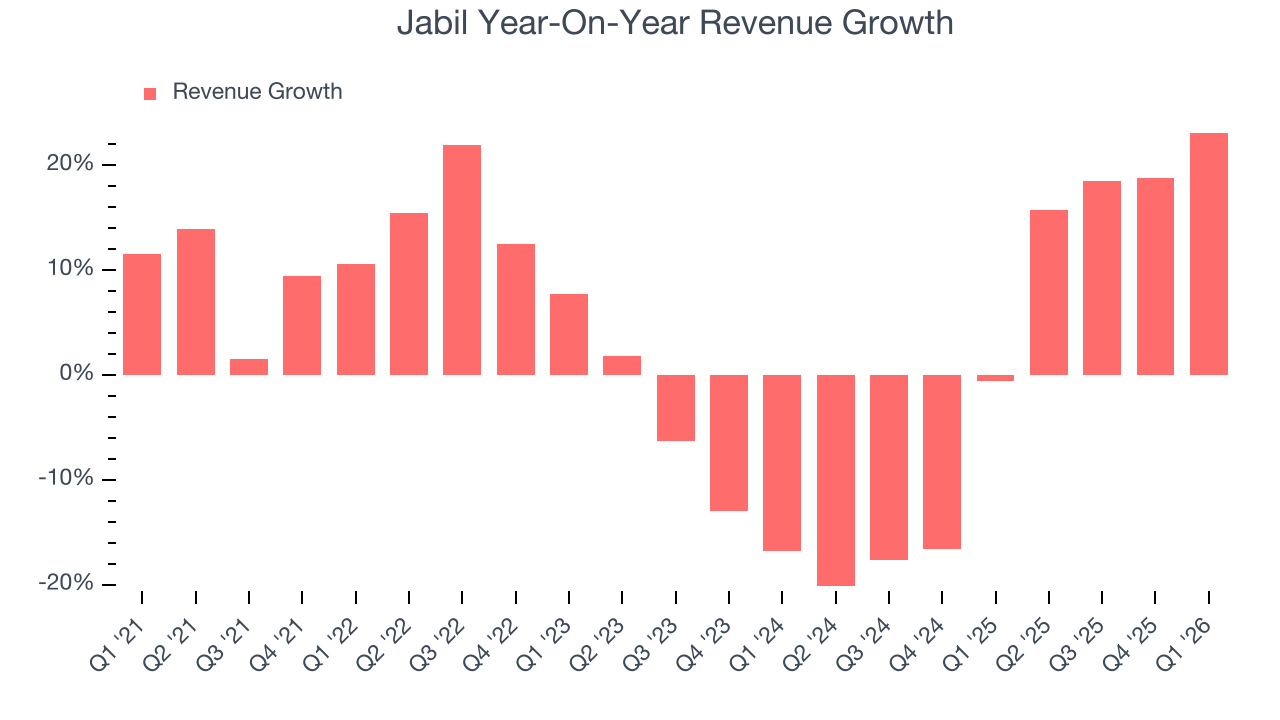

5. Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $32.67 billion in revenue over the past 12 months, Jabil is a behemoth in the business services sector and benefits from economies of scale, giving it an edge in distribution. This also enables it to gain more leverage on its fixed costs than smaller competitors and the flexibility to offer lower prices. However, its scale is a double-edged sword because finding new avenues for growth becomes difficult when you already have a substantial market presence. To expand meaningfully, Jabil likely needs to tweak its prices, innovate with new offerings, or enter new markets.

As you can see below, Jabil’s sales grew at a sluggish 2.9% compounded annual growth rate over the last five years. This shows it failed to generate demand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Jabil’s recent performance shows its demand has slowed as its revenue was flat over the last two years.

This quarter, Jabil reported robust year-on-year revenue growth of 23.1%, and its $8.28 billion of revenue topped Wall Street estimates by 6.8%. Company management is currently guiding for a 8.6% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 2.3% over the next 12 months, similar to its two-year rate. While this projection indicates its newer products and services will fuel better top-line performance, it is still below the sector average.

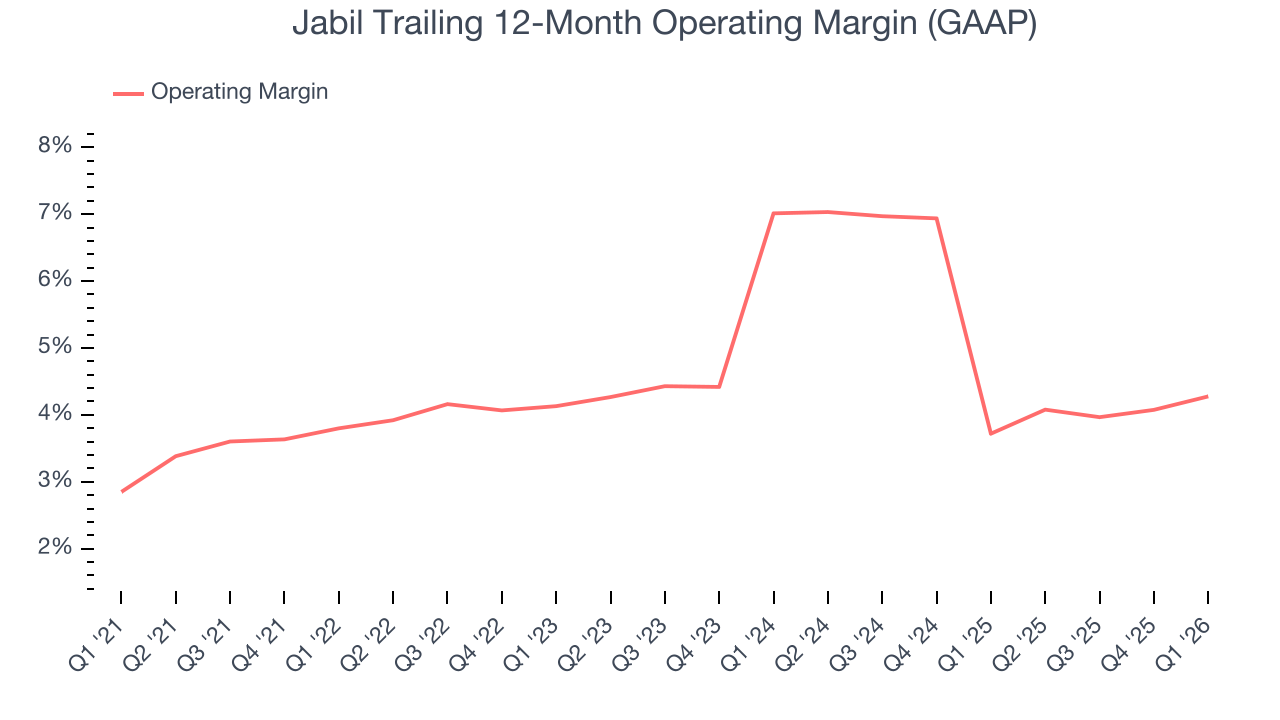

6. Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Jabil’s operating margin has generally stayed the same over the last 12 months, averaging 4.6% over the last five years. This profitability was lousy for a business services business and caused by its suboptimal cost structure.

Analyzing the trend in its profitability, Jabil’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Jabil generated an operating margin profit margin of 4.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

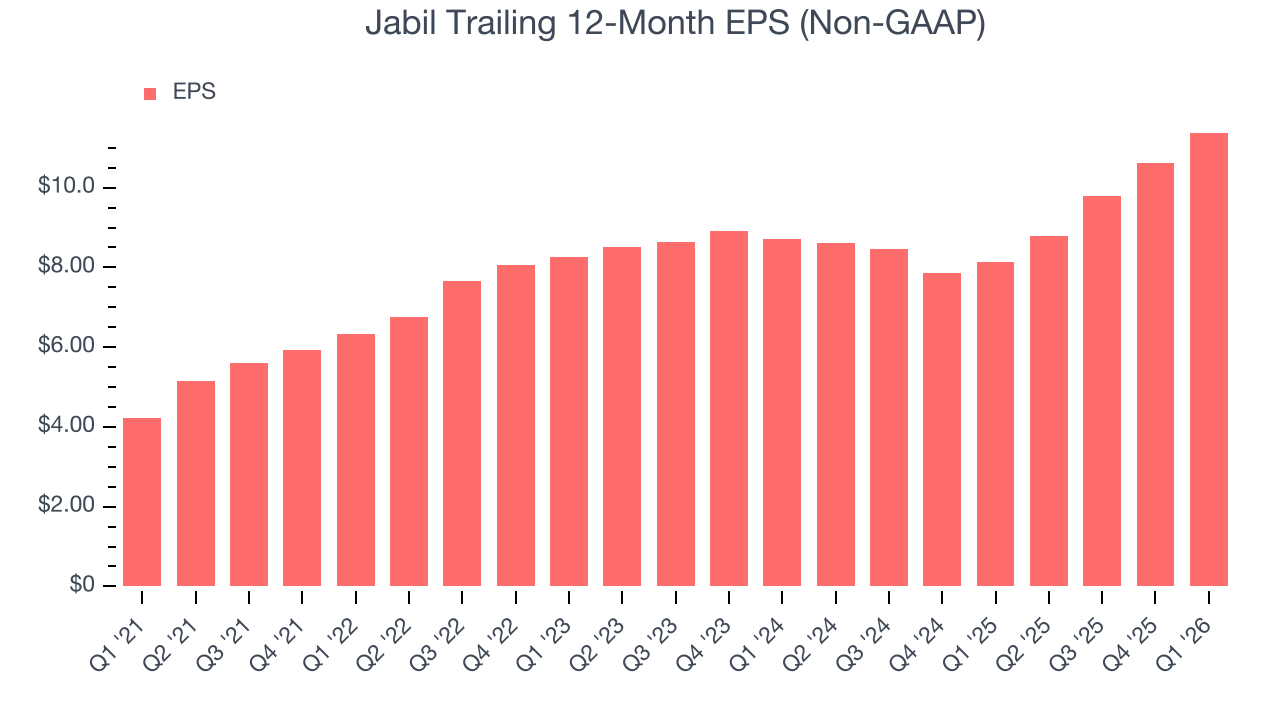

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Jabil’s EPS grew at 21.9% compounded annual growth rate over the last five years, higher than its 2.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Jabil, its two-year annual EPS growth of 14.2% was lower than its five-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q1, Jabil reported adjusted EPS of $2.69, up from $1.94 in the same quarter last year. This print beat analysts’ estimates by 7.2%. Over the next 12 months, Wall Street expects Jabil’s full-year EPS of $11.38 to grow 10.4%.

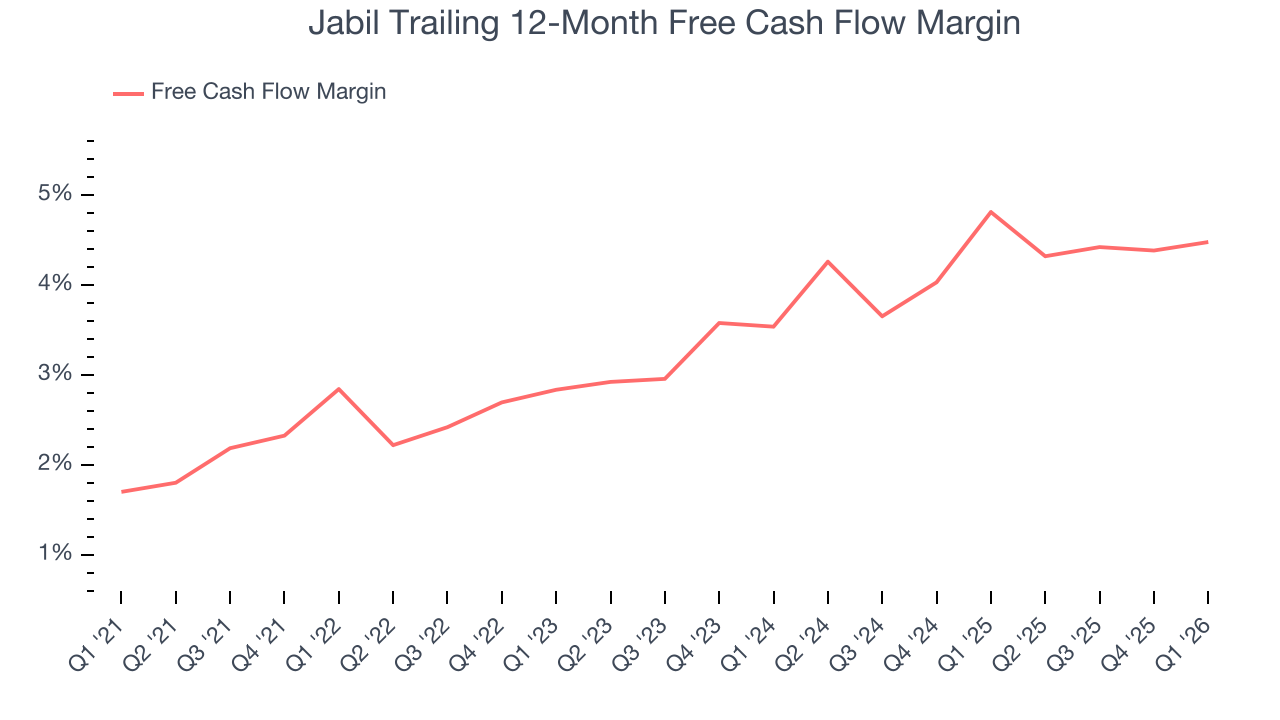

8. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Jabil has shown weak cash profitability relative to peers over the last five years, giving the company fewer opportunities to return capital to shareholders. Its free cash flow margin averaged 3.7%, below what we’d expect for a business services business.

Taking a step back, an encouraging sign is that Jabil’s margin expanded by 1.6 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Jabil’s free cash flow clocked in at $360 million in Q1, equivalent to a 4.3% margin. This cash profitability was in line with the comparable period last year and its five-year average.

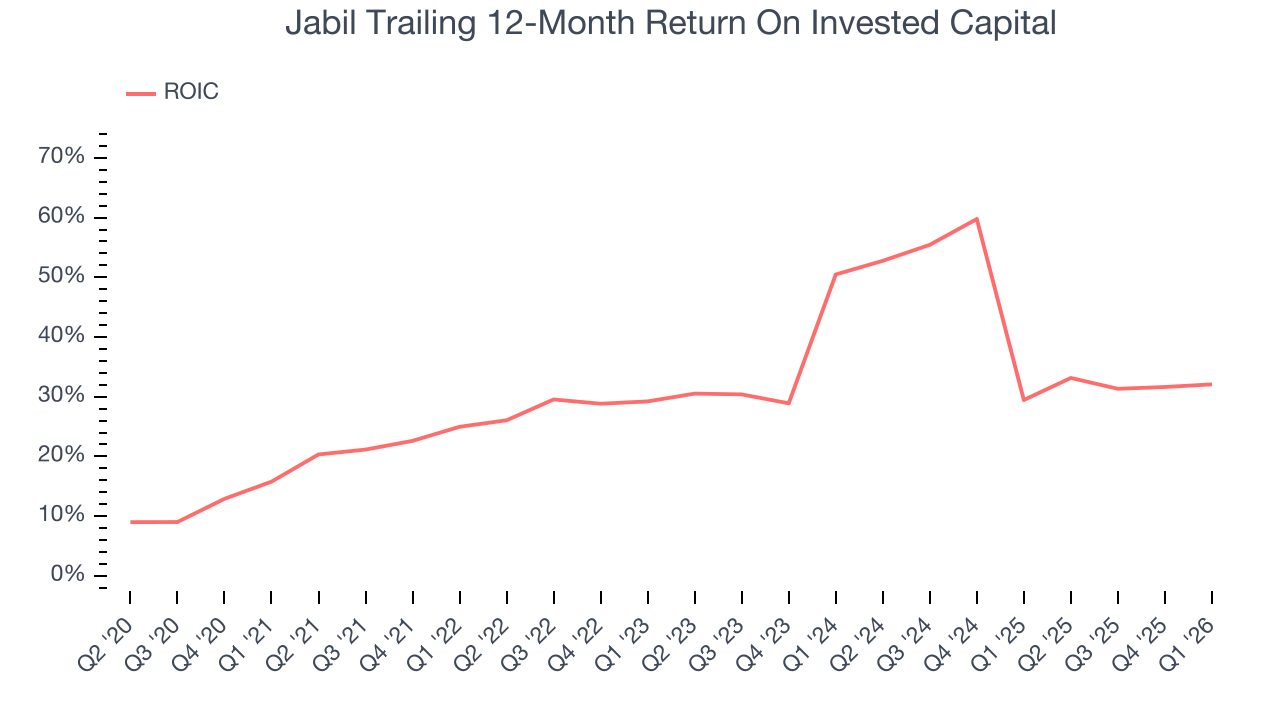

9. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Although Jabil hasn’t been the highest-quality company lately because of its poor top-line performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 33.2%, splendid for a business services business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Jabil’s ROIC averaged 3.7 percentage point increases each year. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

10. Balance Sheet Assessment

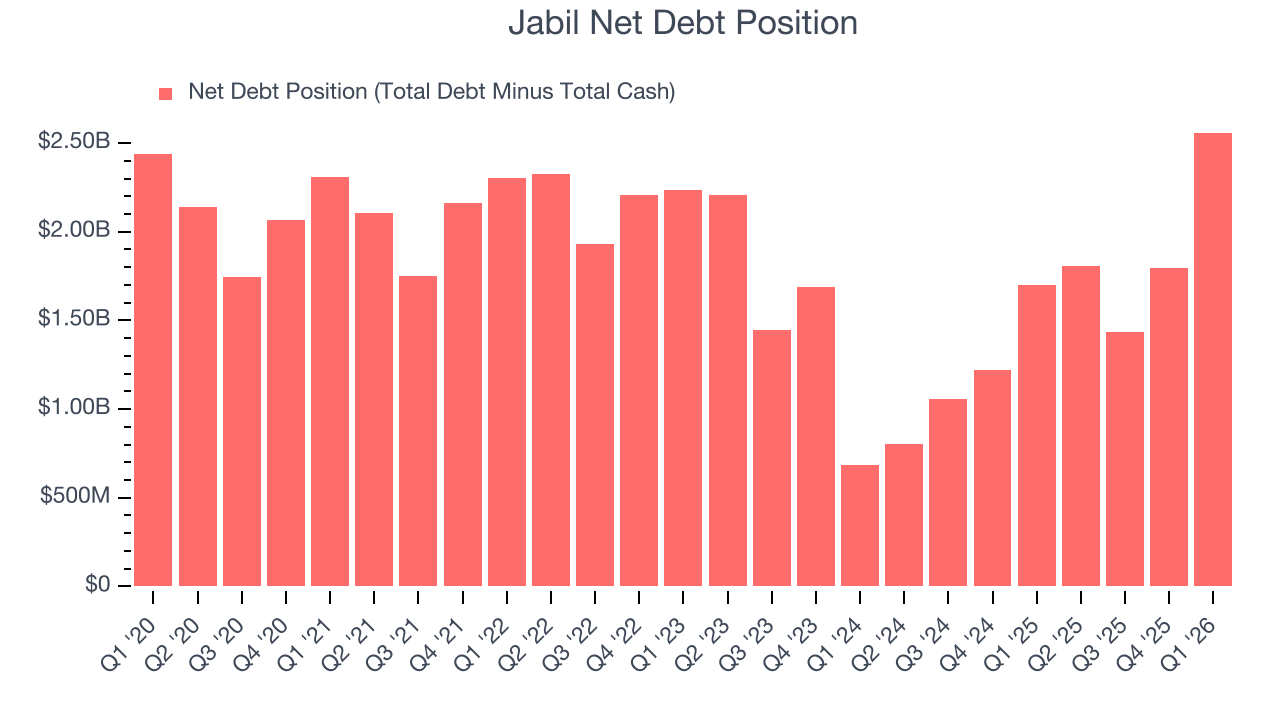

Jabil reported $1.83 billion of cash and $4.39 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $2.45 billion of EBITDA over the last 12 months, we view Jabil’s 1.0× net-debt-to-EBITDA ratio as safe. We also see its $32 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

11. Key Takeaways from Jabil’s Q1 Results

We were impressed by how significantly Jabil blew past analysts’ revenue expectations this quarter. We were also glad its revenue guidance for next quarter trumped Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock remained flat at $263.01 immediately after reporting.

12. Is Now The Time To Buy Jabil?

Updated: March 18, 2026 at 7:38 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Jabil, you should also grasp the company’s longer-term business quality and valuation.

Jabil isn’t a bad business, but we have other favorites. Although its revenue growth was uninspiring over the last five years, its scale makes it a trusted partner with negotiating leverage. Tread carefully with this one, however, as its operating margins reveal poor profitability compared to other business services companies.

Jabil’s P/E ratio based on the next 12 months is 20.9x. Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $270.11 on the company (compared to the current share price of $263.01).