Keysight (KEYS)

We aren’t fans of Keysight. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why We Think Keysight Will Underperform

Spun off from Hewlett-Packard in 2014, Keysight (NYSE:KEYS) offers electronic measurement products for use in various sectors.

- Annual revenue growth of 5.7% over the last five years was below our standards for the industrials sector

- A consolation is that its demand for the next 12 months is expected to accelerate above its two-year trend as Wall Street forecasts robust revenue growth of 18.5%

Keysight doesn’t meet our quality standards. There are more promising prospects in the market.

Why There Are Better Opportunities Than Keysight

Keysight is trading at $288.39 per share, or 30.4x forward P/E. Not only is Keysight’s multiple richer than most industrials peers, but it’s also expensive for its revenue characteristics.

We’d rather invest in similarly-priced but higher-quality companies with more reliable earnings growth.

3. Keysight (KEYS) Research Report: Q4 CY2025 Update

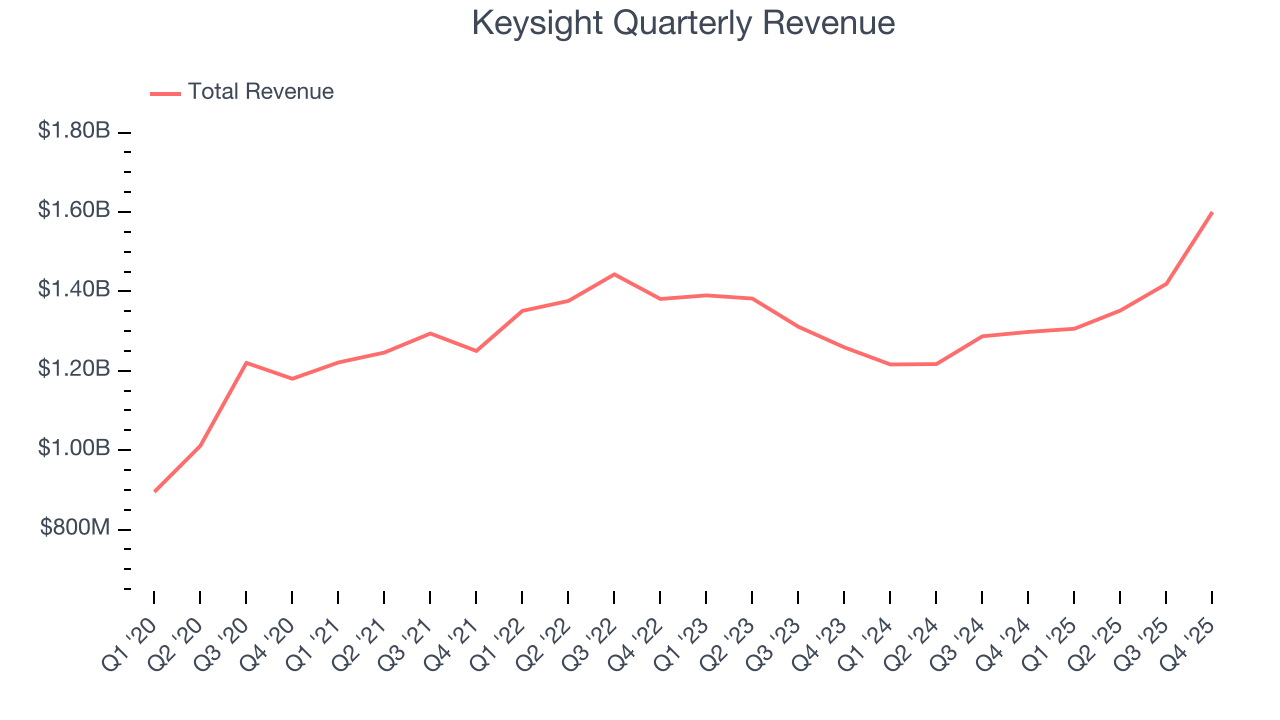

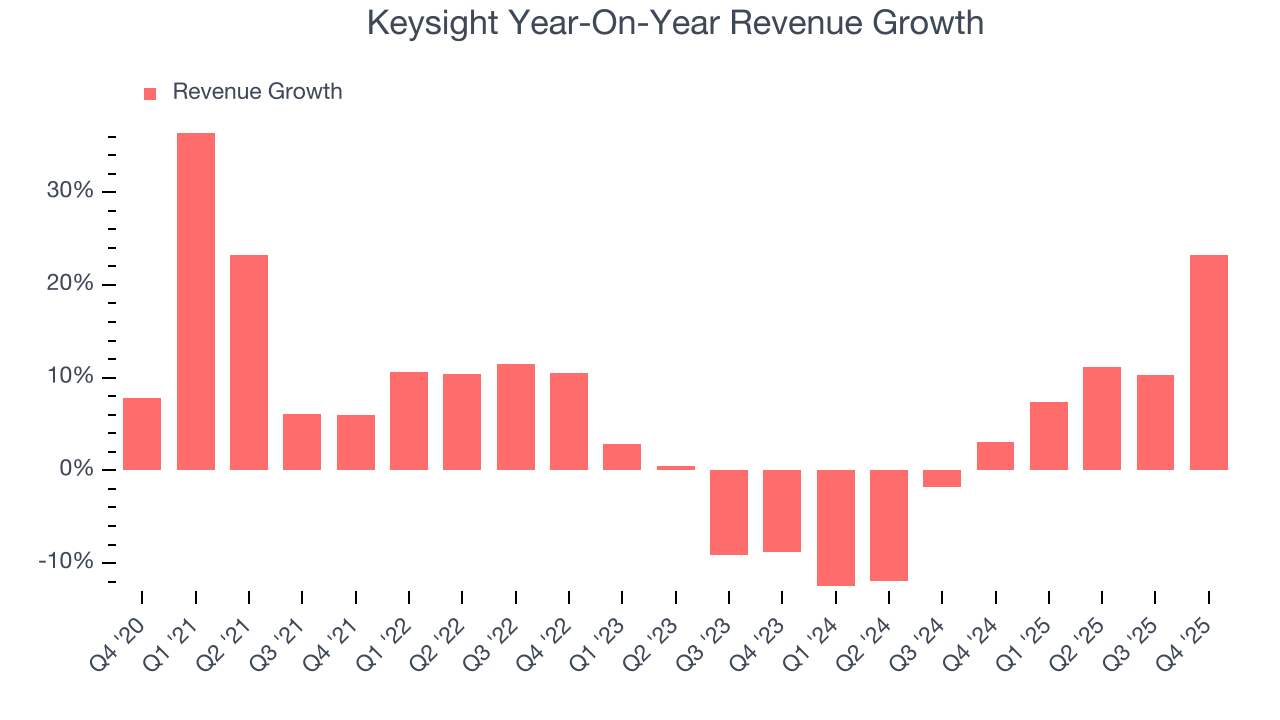

Electronic measurement provider Keysight (NYSE:KEYS) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 23.3% year on year to $1.6 billion. On top of that, next quarter’s revenue guidance ($1.7 billion at the midpoint) was surprisingly good and 13.1% above what analysts were expecting. Its non-GAAP profit of $2.17 per share was 8.8% above analysts’ consensus estimates.

Keysight (KEYS) Q4 CY2025 Highlights:

- Revenue: $1.6 billion vs analyst estimates of $1.54 billion (23.3% year-on-year growth, 3.9% beat)

- Adjusted EPS: $2.17 vs analyst estimates of $2.00 (8.8% beat)

- Revenue Guidance for Q1 CY2026 is $1.7 billion at the midpoint, above analyst estimates of $1.50 billion

- Adjusted EPS guidance for Q1 CY2026 is $2.30 at the midpoint, above analyst estimates of $1.91

- Operating Margin: 15.5%, down from 16.8% in the same quarter last year

- Free Cash Flow Margin: 25.4%, down from 26.7% in the same quarter last year

- Market Capitalization: $41.77 billion

Company Overview

Spun off from Hewlett-Packard in 2014, Keysight (NYSE:KEYS) offers electronic measurement products for use in various sectors.

The company became an independent entity to sharpen its focus, and since its separation, has made 10+ acquisitions totaling over $1 billion to scale and expand its product portfolio.

Today, Keysight provides products to ensure electronic components and systems work properly. Its product portfolio includes oscilloscopes (show how electronic signals change over time), signal generators (create electronic signals to test and fix electronic devices), and spectrum analyzers (check the strength and frequency of signals). These products ensure new technologies work correctly and expedite product readiness for sale.

In addition to its hardware products, Keysight provides software and services that enhance the capabilities of its own products and generate additional revenue for the company. Through its combination of software and hardware products, Keysight serves the telecommunications, aerospace & defense, and electronics industries.

Keysight primarily sells to large corporations, government agencies, and research institutions using a direct sales force and distributors. It engages in long-term supply agreements, government contracts, and project-based contracts, often offering volume discounts. Furthermore, its software solutions give it recurring revenue and it has established long-term partnerships with original equipment manufacturers (OEMs).

4. Inspection Instruments

Measurement and inspection instrument companies may enjoy more steady demand because products such as water meters are non-discretionary and mandated for replacement at predictable intervals. In the last decade, digitization and data collection have driven innovation in the space, leading to incremental sales. But like the broader industrials sector, measurement and inspection instrument companies are at the whim of economic cycles. Interest rates, for example, can greatly impact civil, commercial, and residential construction projects that drive demand.

Competitors offering similar products include Tektronix (NASDAQ:TEK), National Instruments (NASDAQ:NATI), and Teradyne (NASDAQ:TER).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Over the last five years, Keysight grew its sales at a tepid 5.7% compounded annual growth rate. This was below our standard for the industrials sector and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Keysight’s recent performance shows its demand has slowed as its annualized revenue growth of 3.1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

This quarter, Keysight reported robust year-on-year revenue growth of 23.3%, and its $1.6 billion of revenue topped Wall Street estimates by 3.9%. Company management is currently guiding for a 30.2% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 10.5% over the next 12 months, an improvement versus the last two years. This projection is admirable and indicates its newer products and services will spur better top-line performance.

6. Gross Margin & Pricing Power

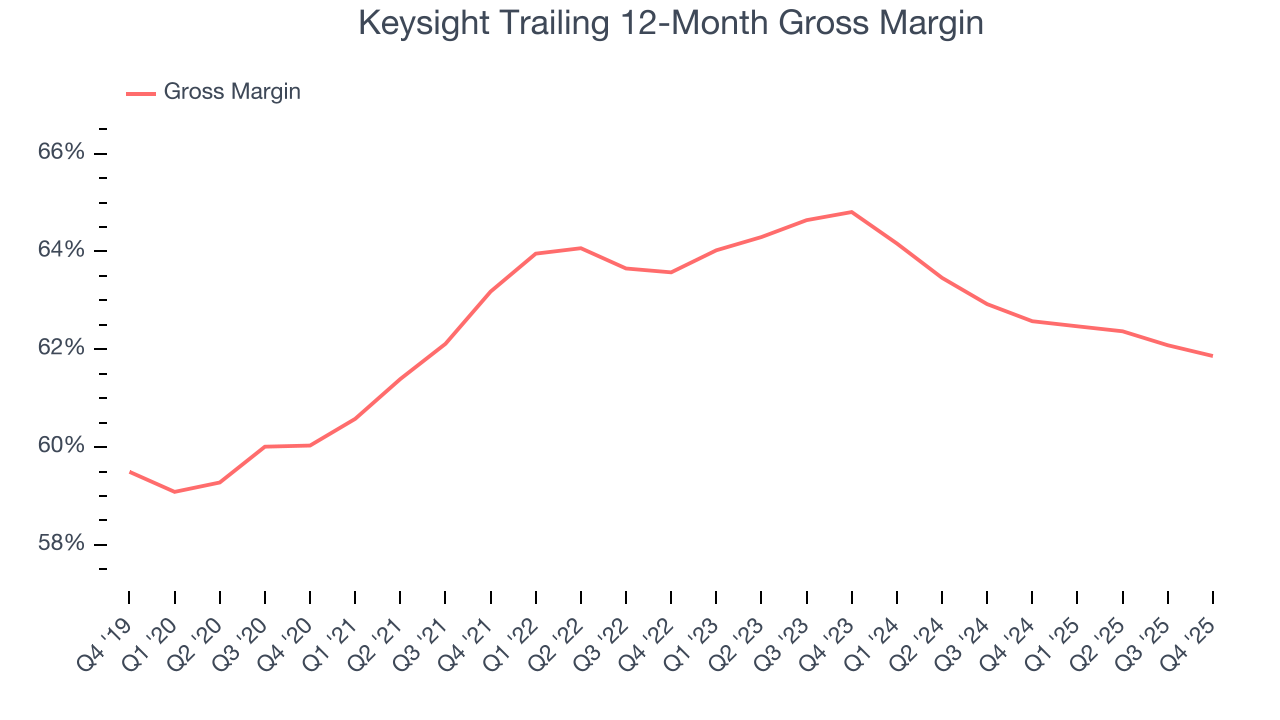

Keysight has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 63.2% gross margin over the last five years. Said differently, roughly $63.19 was left to spend on selling, marketing, R&D, and general administrative overhead for every $100 in revenue.

This quarter, Keysight’s gross profit margin was 62.2%, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

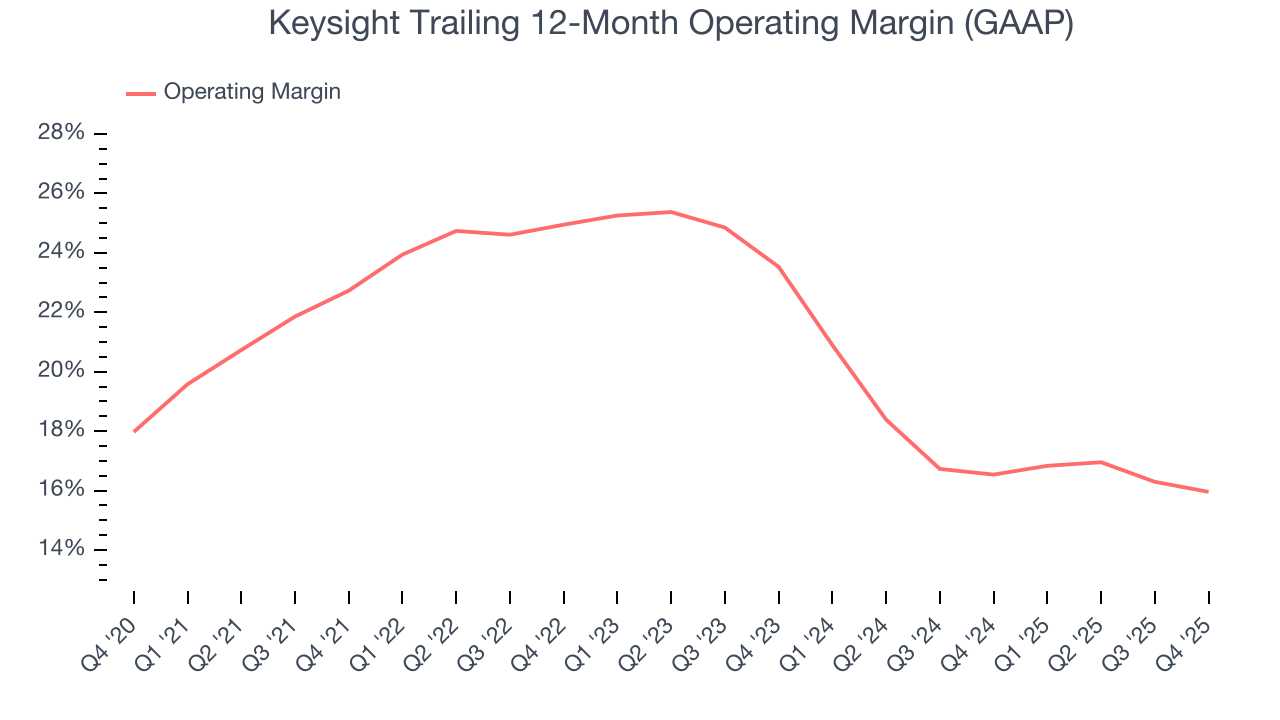

Keysight has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 20.7%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Keysight’s operating margin decreased by 6.8 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Keysight generated an operating margin profit margin of 15.5%, down 1.3 percentage points year on year. Since Keysight’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

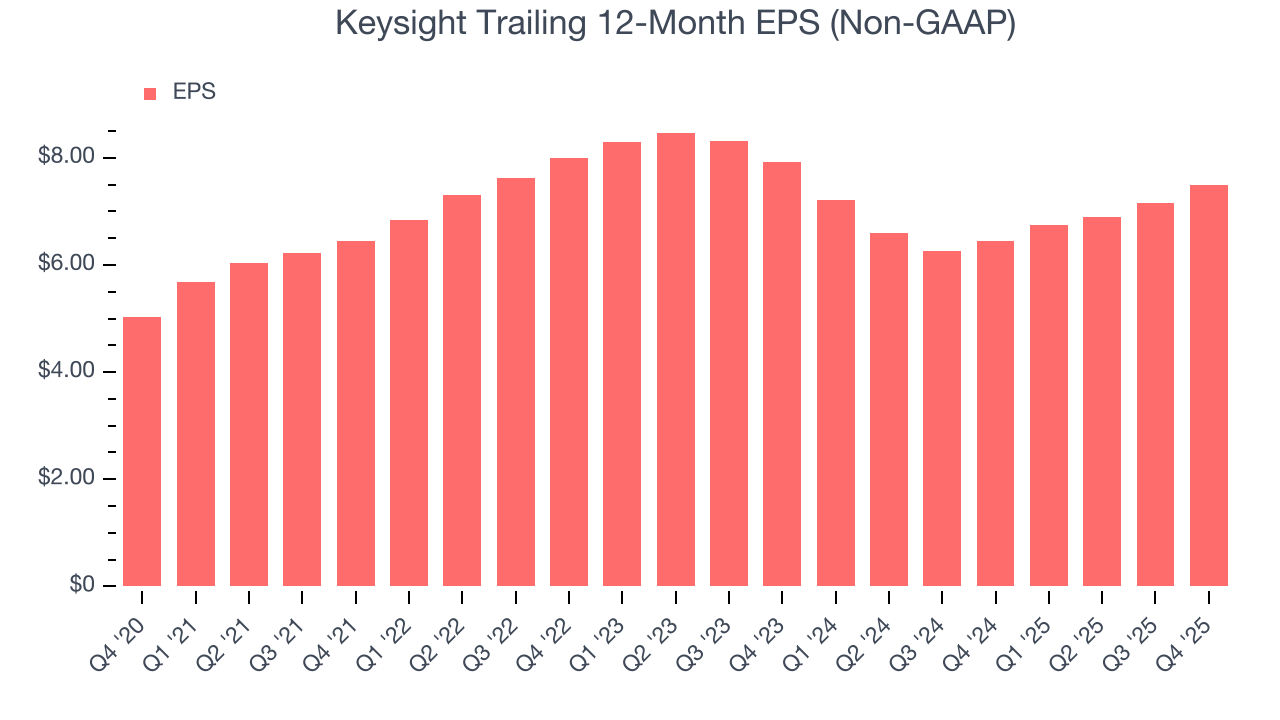

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Keysight’s EPS grew at a decent 8.4% compounded annual growth rate over the last five years, higher than its 5.7% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

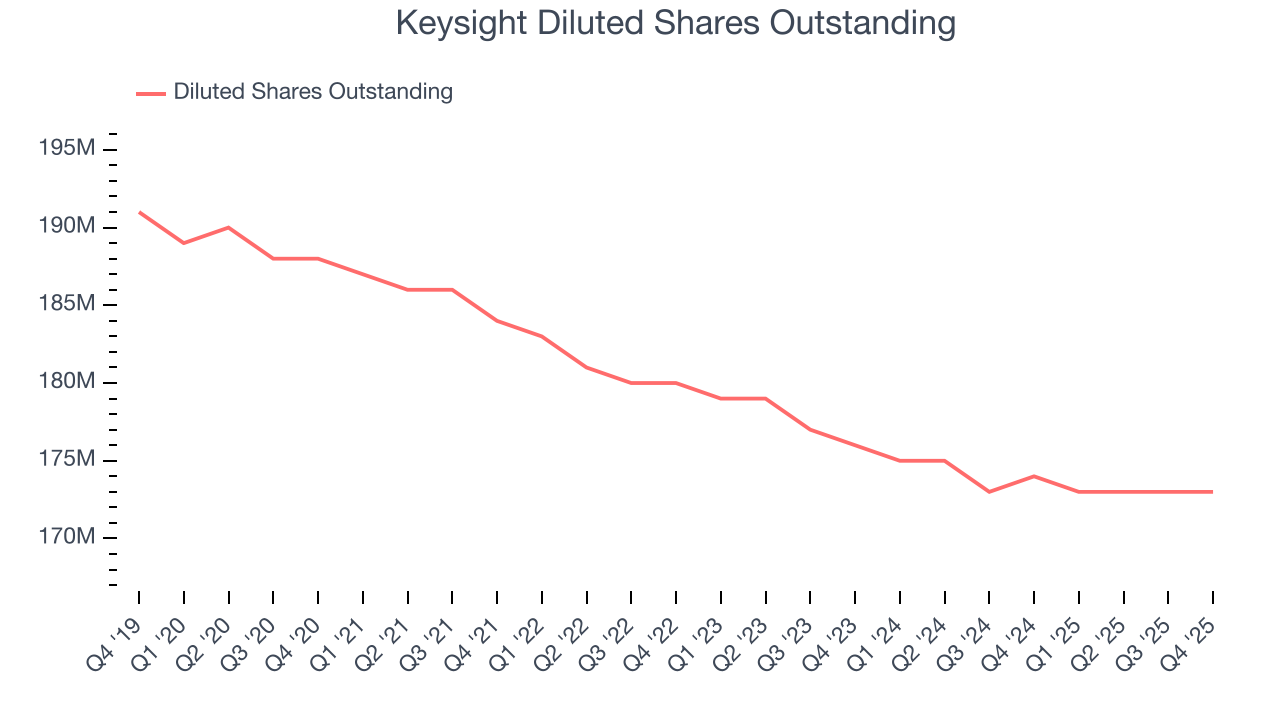

Diving into Keysight’s quality of earnings can give us a better understanding of its performance. A five-year view shows that Keysight has repurchased its stock, shrinking its share count by 8%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Keysight, its two-year annual EPS declines of 2.7% mark a reversal from its five-year trend. We hope Keysight can return to earnings growth in the future.

In Q4, Keysight reported adjusted EPS of $2.17, up from $1.82 in the same quarter last year. This print beat analysts’ estimates by 8.8%. Over the next 12 months, Wall Street expects Keysight’s full-year EPS of $7.50 to grow 11.9%.

9. Cash Is King

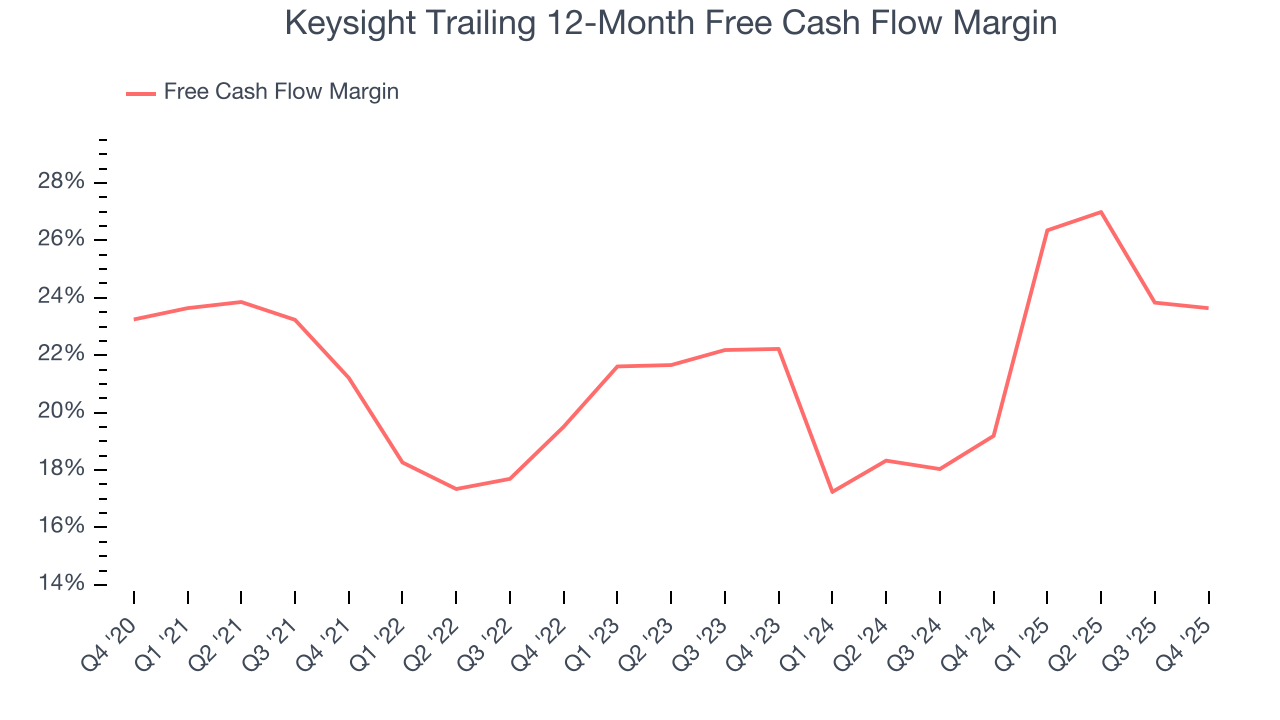

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Keysight has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 21.2% over the last five years.

Taking a step back, we can see that Keysight’s margin expanded by 2.4 percentage points during that time. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability fell.

Keysight’s free cash flow clocked in at $407 million in Q4, equivalent to a 25.4% margin. The company’s cash profitability regressed as it was 1.2 percentage points lower than in the same quarter last year, but it’s still above its five-year average. We wouldn’t read too much into this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends are more important.

10. Return on Invested Capital (ROIC)

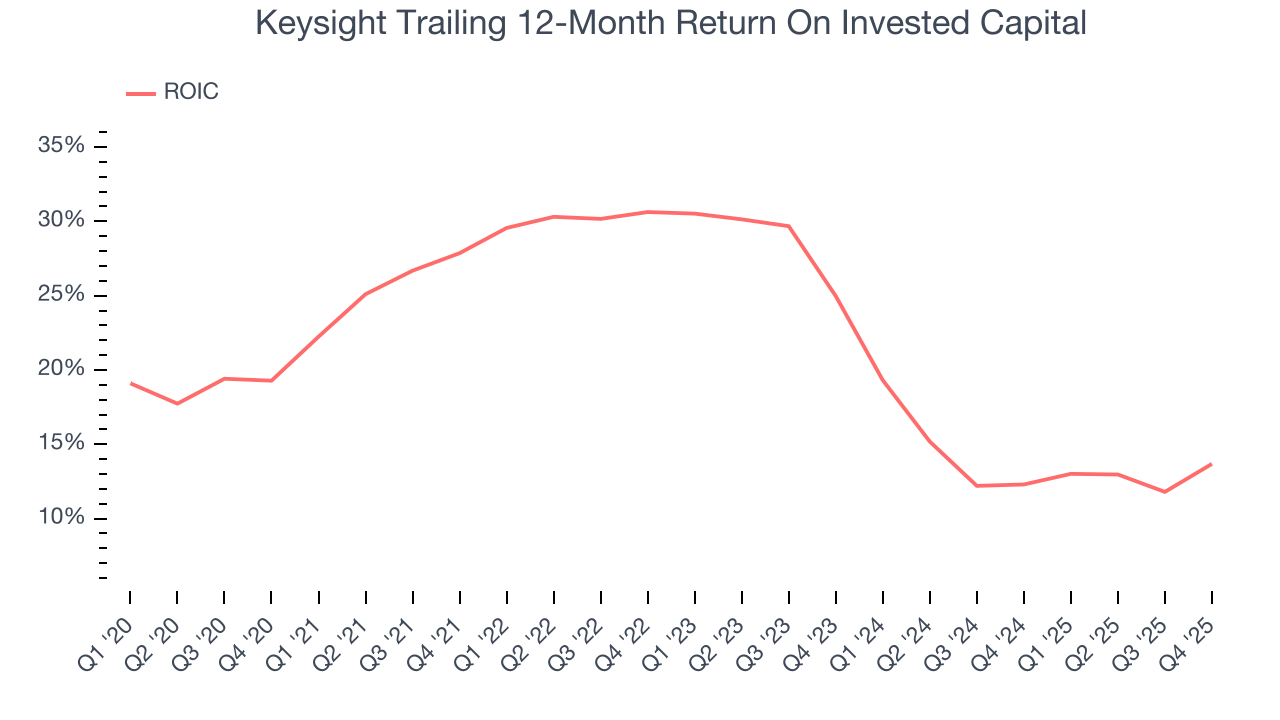

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Keysight hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 21.9%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, Keysight’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

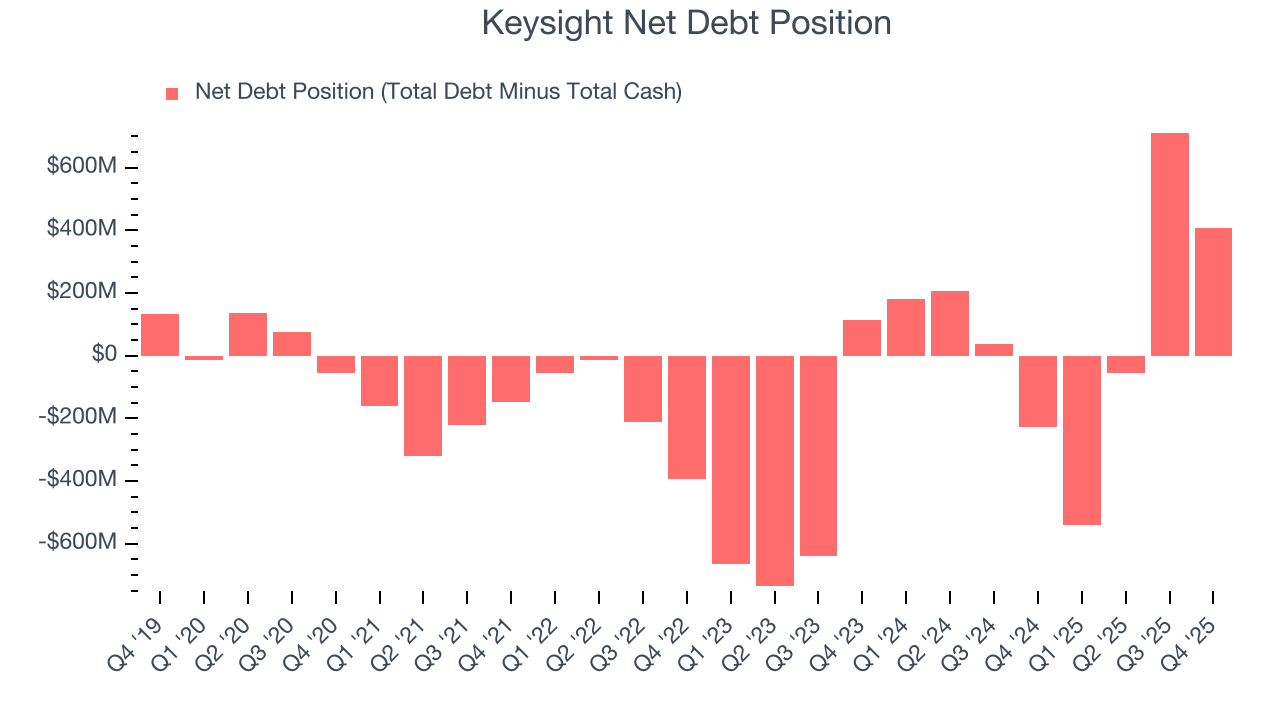

11. Balance Sheet Assessment

Keysight reported $2.18 billion of cash and $2.59 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.61 billion of EBITDA over the last 12 months, we view Keysight’s 0.3× net-debt-to-EBITDA ratio as safe. We also see its $6 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Keysight’s Q4 Results

We were impressed by Keysight’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 13.9% to $277.85 immediately following the results.

13. Is Now The Time To Buy Keysight?

Updated: March 24, 2026 at 11:29 PM EDT

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Keysight’s business quality ultimately falls short of our standards. To begin with, its revenue growth was uninspiring over the last five years. While its admirable gross margins indicate the mission-critical nature of its offerings, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its declining operating margin shows the business has become less efficient.

Keysight’s P/E ratio based on the next 12 months is 31.6x. This multiple tells us a lot of good news is priced in - we think there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $301.54 on the company (compared to the current share price of $301.45).