Morgan Stanley (MS)

Morgan Stanley doesn’t meet our bar, but we get that it isn’t a bad business. While we’d invest elsewhere, beauty is in the eye of the beholder.― StockStory Analyst Team

1. News

2. Summary

Why Morgan Stanley Is Not Exciting

Founded in 1924 during the post-WWI economic boom by former JP Morgan partners, Morgan Stanley (NYSE:MS) is a global financial services firm that provides investment banking, wealth management, and investment management services to corporations, governments, institutions, and individuals.

- Annual tangible book value per share growth of 3.6% over the last five years lagged behind its financials peers as its large balance sheet made it difficult to generate incremental capital growth

- Earnings per share lagged its peers over the last five years as they only grew by 9.3% annually

- On the plus side, its adequate return on equity shows management makes decent investment decisions

Morgan Stanley doesn’t pass our quality test. We see more favorable opportunities in the market.

Why There Are Better Opportunities Than Morgan Stanley

At $154.03 per share, Morgan Stanley trades at 13.5x forward P/E. This multiple expensive for its subpar fundamentals.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. Morgan Stanley (MS) Research Report: Q4 CY2025 Update

Global financial services firm Morgan Stanley (NYSE:MS) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 10.3% year on year to $17.89 billion. Its GAAP profit of $2.68 per share was 9.4% above analysts’ consensus estimates.

Morgan Stanley (MS) Q4 CY2025 Highlights:

- Revenue: $17.89 billion vs analyst estimates of $17.66 billion (10.3% year-on-year growth, 1.3% beat)

- Efficiency Ratio: 68% vs analyst estimates of 69.8% (176 basis point beat)

- EPS (GAAP): $2.68 vs analyst estimates of $2.45 (9.4% beat)

- Tangible Book Value per Share: $50 vs analyst estimates of $49.54 (12.2% year-on-year growth, 0.9% beat)

- Market Capitalization: $287.3 billion

Company Overview

Founded in 1924 during the post-WWI economic boom by former JP Morgan partners, Morgan Stanley (NYSE:MS) is a global financial services firm that provides investment banking, wealth management, and investment management services to corporations, governments, institutions, and individuals.

Morgan Stanley operates through three main business segments. The Institutional Securities segment serves as the company's investment banking arm, helping corporations and governments raise capital through debt and equity underwriting, providing strategic advice on mergers and acquisitions, and offering sales and trading services in equities and fixed income markets. For example, when a technology company plans to go public, Morgan Stanley might serve as the lead underwriter, helping determine the offering price and connecting the company with institutional investors.

The Wealth Management segment caters to individual investors and small-to-medium businesses, offering financial advisor-led services, investment advisory, financial planning, lending products, and retirement solutions. A high-net-worth client might work with a Morgan Stanley advisor to develop a comprehensive wealth strategy spanning investments, estate planning, and philanthropic goals.

The Investment Management segment develops and manages investment strategies across asset classes for institutional clients like pension funds and sovereign wealth funds, as well as individual investors through intermediaries. The firm's investment vehicles range from traditional mutual funds to alternative investments like private equity and real estate.

Morgan Stanley generates revenue primarily through fees for advisory services, commissions on trades, interest income from lending, and management fees from investment products. As a bank holding company, it operates under comprehensive regulation by the Federal Reserve and must comply with capital requirements, the Volcker Rule (limiting proprietary trading), and consumer protection laws. The company conducts business globally, with significant operations across the Americas, Europe, and Asia-Pacific regions.

4. Investment Banking & Brokerage

Investment banks and brokerages facilitate capital raises, mergers and acquisitions, and securities trading. The sector benefits from corporate activity during economic expansion, increased retail trading participation, and advisory opportunities in emerging sectors. Headwinds include economic cycle vulnerability affecting deal flow, compressed trading commissions due to electronic platforms, and regulatory capital requirements constraining certain higher-risk activities.

Morgan Stanley's primary competitors include other major global investment banks such as Goldman Sachs (NYSE:GS), JPMorgan Chase (NYSE:JPM), Bank of America Merrill Lynch (NYSE:BAC), and Citigroup (NYSE:C), as well as wealth management firms like Charles Schwab (NYSE:SCHW) and asset managers including BlackRock (NYSE:BLK).

5. Revenue Growth

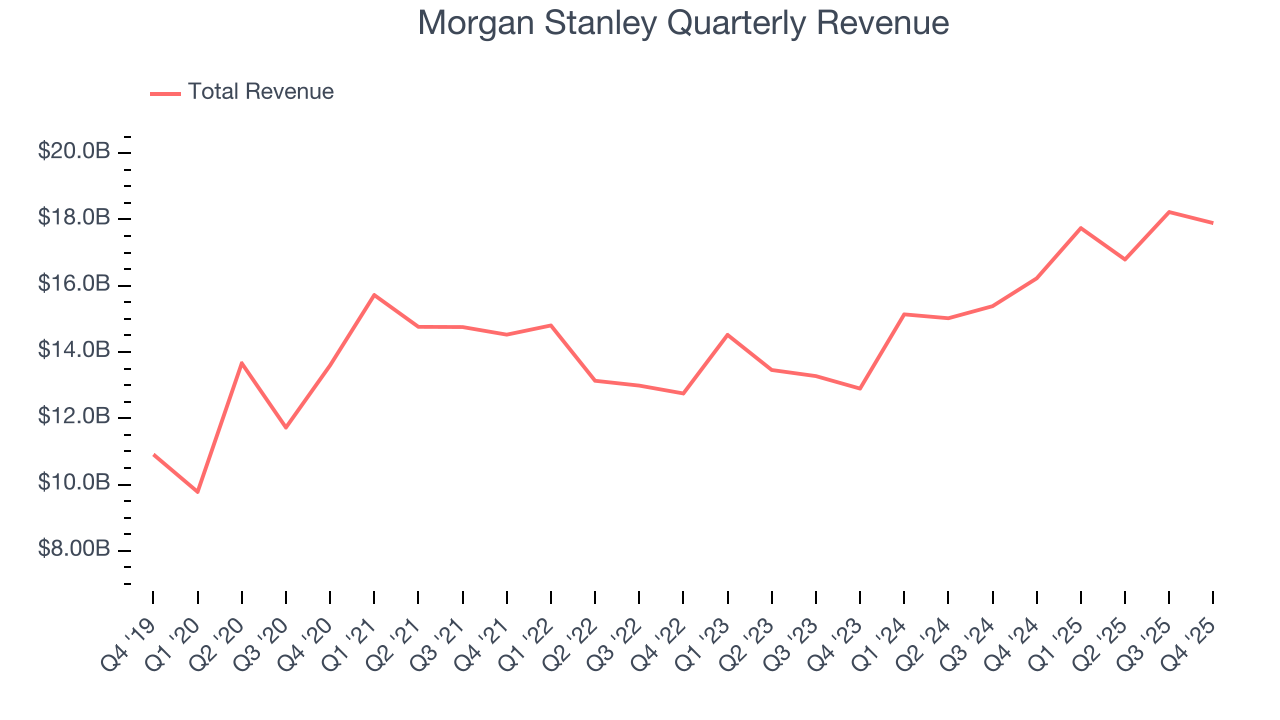

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Morgan Stanley grew its revenue at a decent 7.7% compounded annual growth rate. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

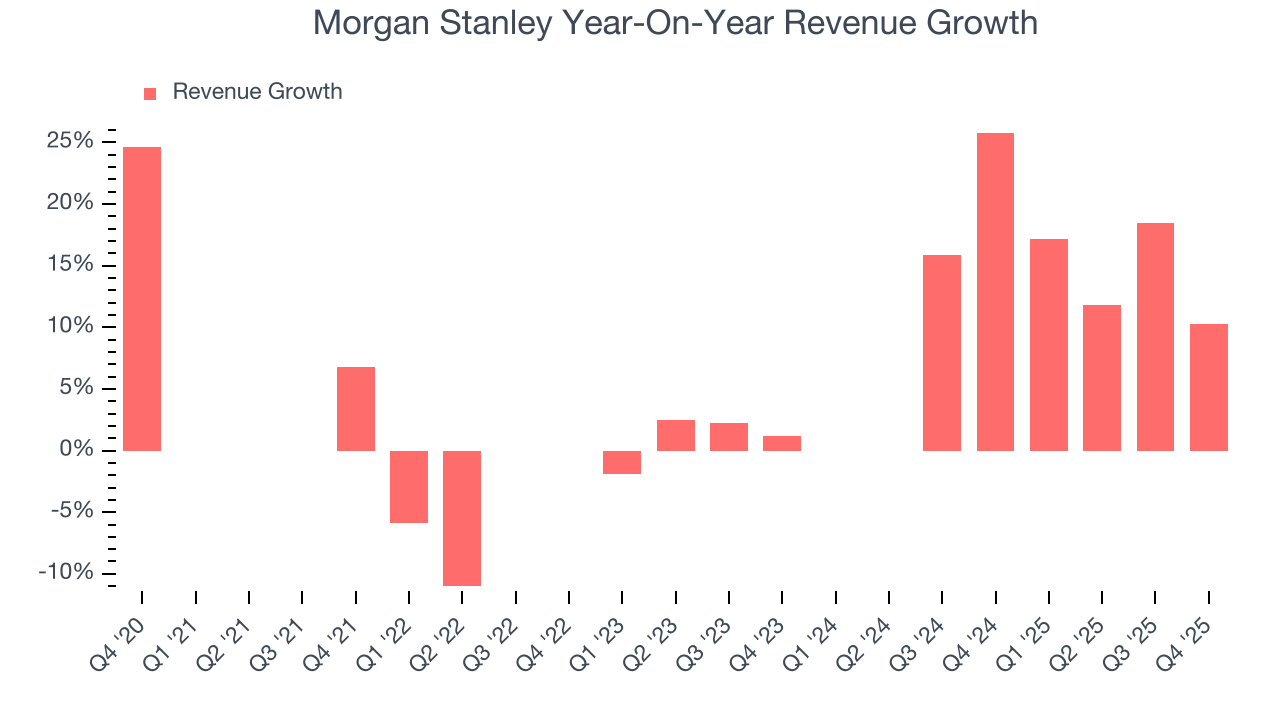

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Morgan Stanley’s annualized revenue growth of 14.2% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

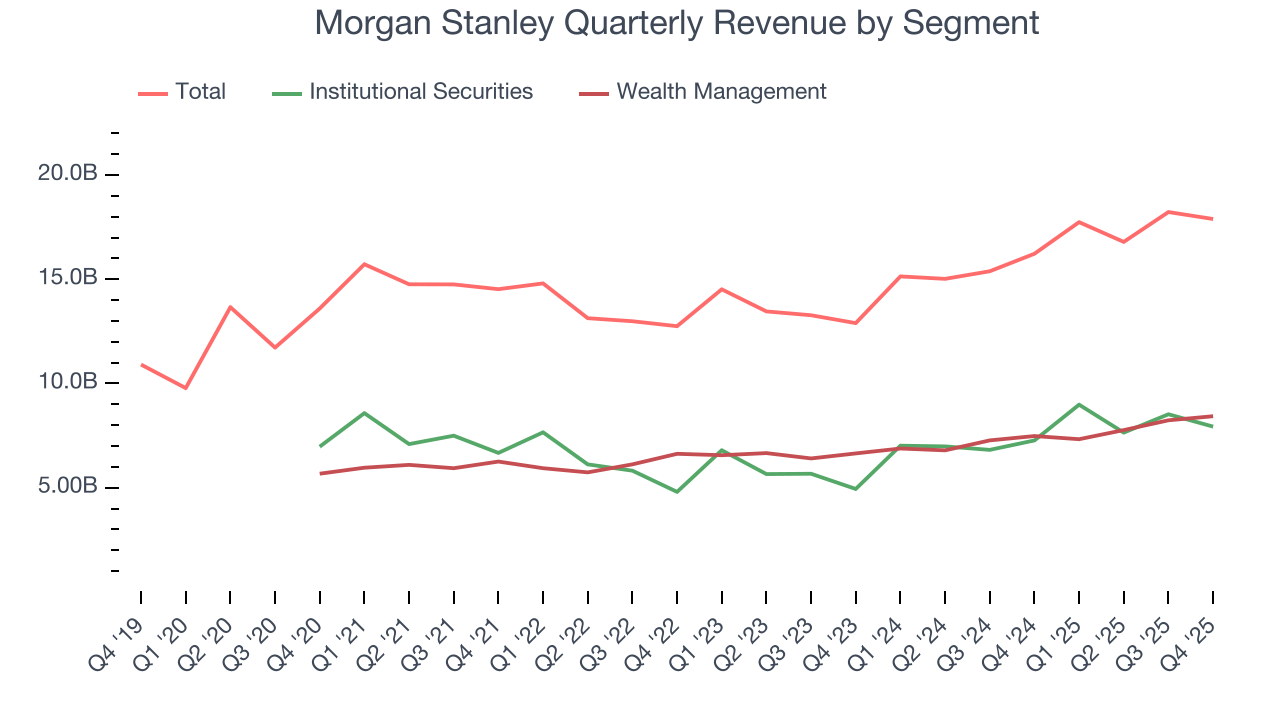

We can better understand the company’s revenue dynamics by analyzing its most important segments, Institutional Securities and Wealth Management, which are 44.3% and 47.1% of total revenue. Institutional Securities revenue grew by 4.6% and 19.8% annually over the past five and two years, respectively. At the same time, Wealth Management revenue increased by 10.7% and 9.9% per year over the past five and two years, respectively.

This quarter, Morgan Stanley reported year-on-year revenue growth of 10.3%, and its $17.89 billion of revenue exceeded Wall Street’s estimates by 1.3%.

6. Efficiency Ratio

Topline growth is certainly important, but the overall profitability of this growth matters for the bottom line. For Investment Banking & Brokerage companies, we look at efficiency ratio, which is non-interest expense (salaries, rent, IT, marketing, excluding interest paid out to depositors) as a percentage of total revenue.

We pay attention to efficiency ratios, but we and the market care most about how they’ve trended over time. Said differently, has the company become more or less efficient? It’s somewhat counterintuitive, but a lower efficiency ratio is better.

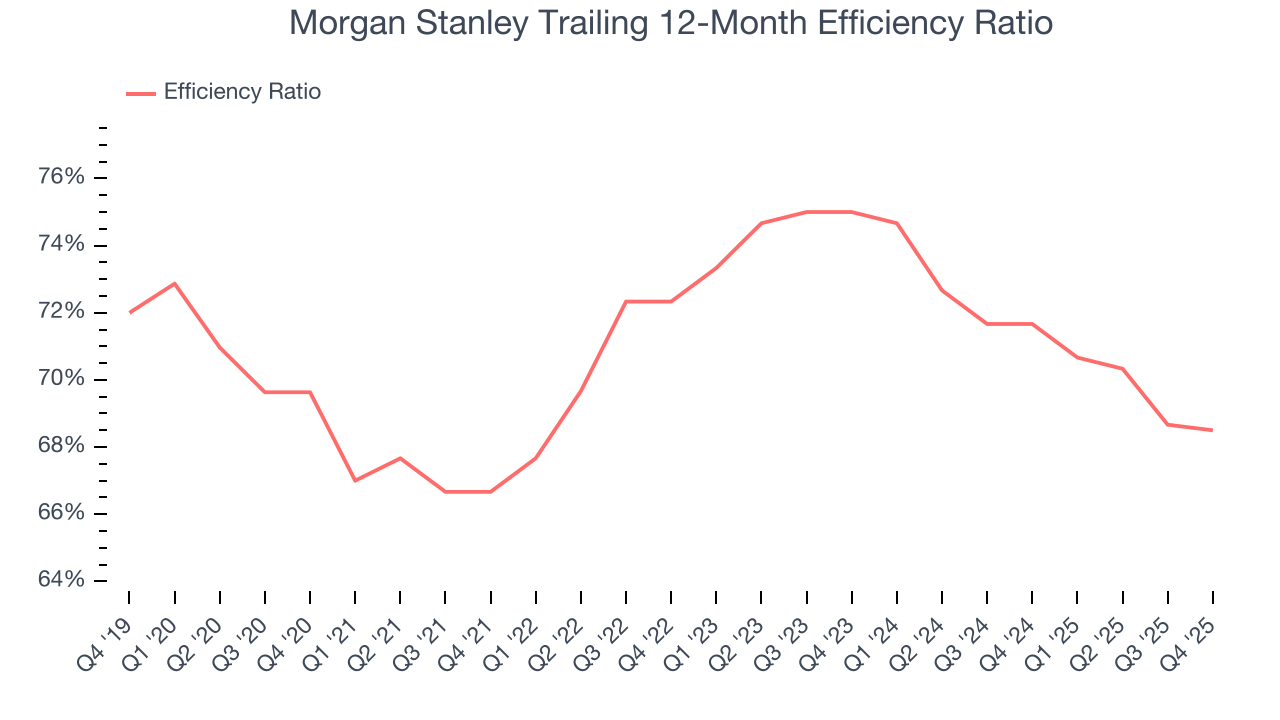

Over the last five years, Morgan Stanley’s efficiency ratio has swelled by 1.1 percentage points, going from 66.7% to 68.5%. It has also improved by 6.5 percentage points on a two-year basis, showing its expenses have consistently grown at a slower rate than revenue. This typically signals prudent management.

Morgan Stanley’s efficiency ratio came in at 68% this quarter, beating analysts’ expectations by 176 basis points (100 basis points = 1 percentage point).

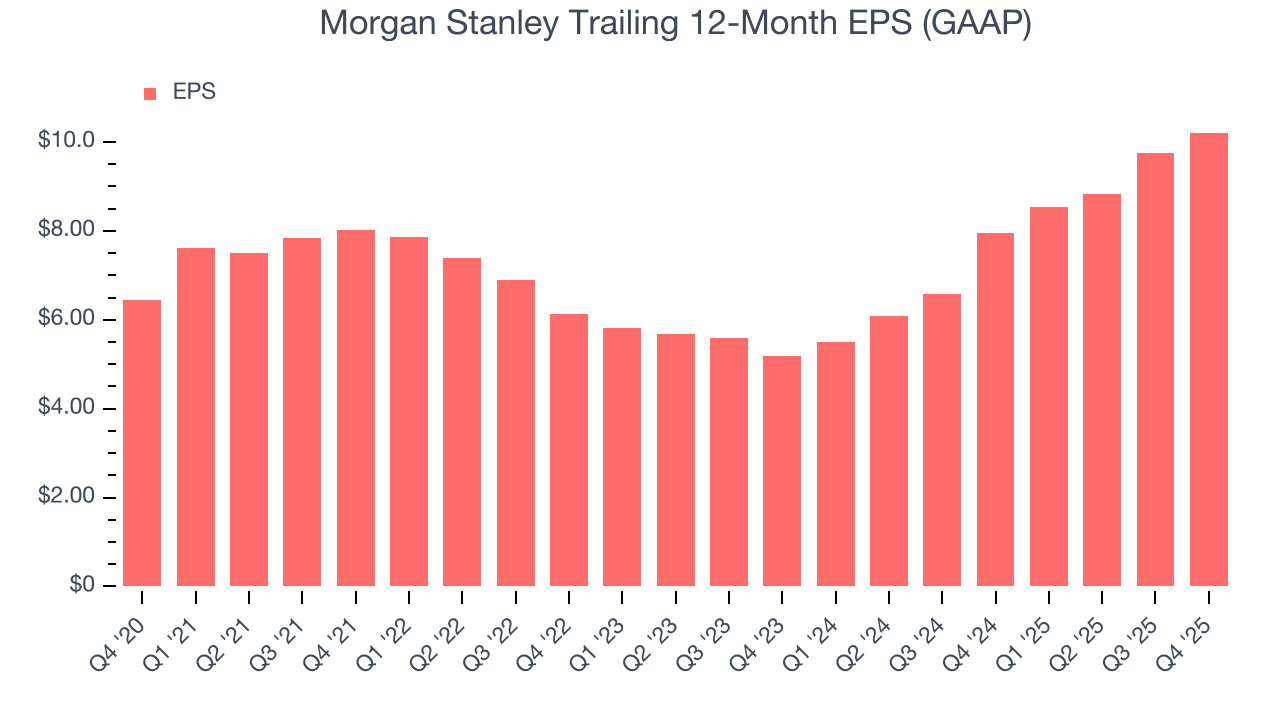

7. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Morgan Stanley’s unimpressive 9.7% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Morgan Stanley’s two-year annual EPS growth of 40.5% was fantastic and topped its 14.2% two-year revenue growth.

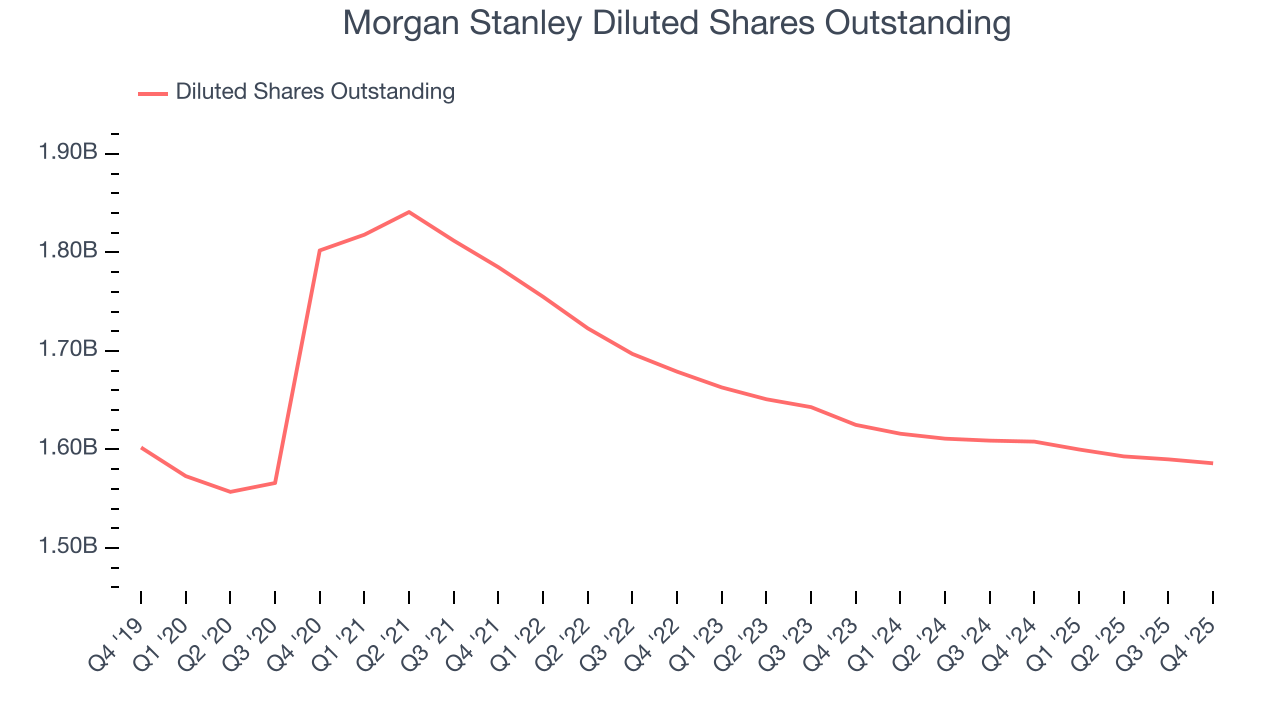

Diving into Morgan Stanley’s quality of earnings can give us a better understanding of its performance. Morgan Stanley’s efficiency ratio has improved over the last two yearswhile its share count has shrunk 2.4%. Improving profitability and share buybacks are positive signs for shareholders as they juice EPS growth relative to revenue growth.

In Q4, Morgan Stanley reported EPS of $2.68, up from $2.22 in the same quarter last year. This print beat analysts’ estimates by 9.4%. Over the next 12 months, Wall Street expects Morgan Stanley’s full-year EPS of $10.21 to grow 7.4%.

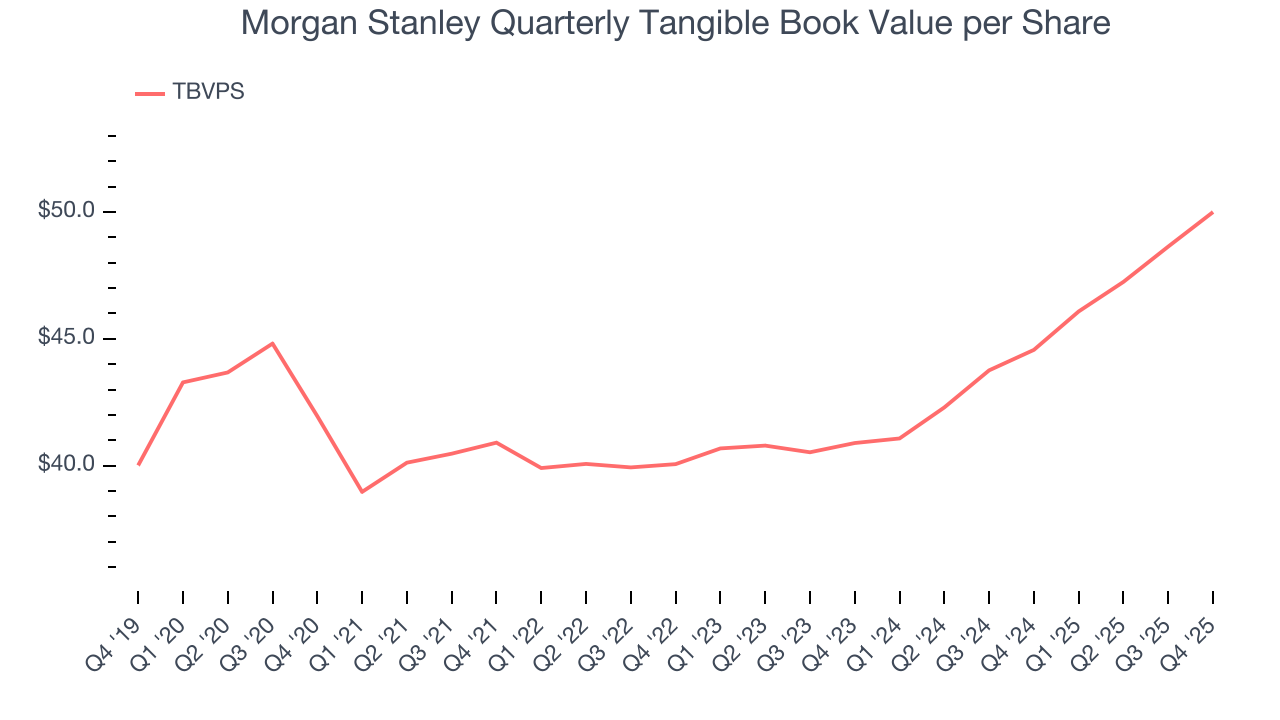

8. Tangible Book Value Per Share (TBVPS)

Financial firms profit by providing a wide range of services, making them fundamentally balance sheet-driven enterprises with multiple intermediation roles. Market participants emphasize balance sheet quality and sustained book value growth when evaluating these multifaceted institutions.

This is why we consider tangible book value per share (TBVPS) an important metric for the sector. TBVPS represents the real net worth per share across all business segments, providing a clear measure of shareholder equity regardless of the complexity of operations. On the other hand, EPS is often distorted by the diverse nature of operations, mergers, and various accounting treatments across different business units. Book value provides clearer performance insights.

Morgan Stanley’s TBVPS grew at a sluggish 3.6% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 10.6% annually over the last two years from $40.89 to $50 per share.

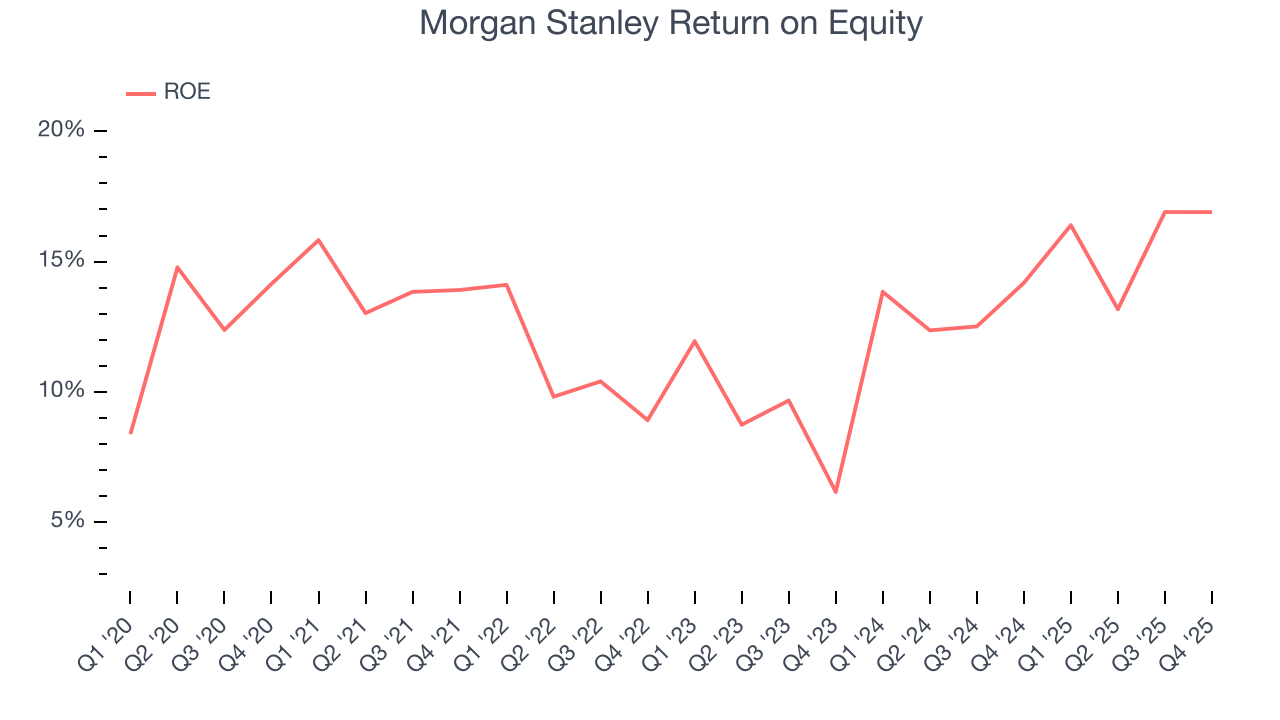

9. Return on Equity

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, Morgan Stanley has averaged an ROE of 12.6%, respectable for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired.

10. Balance Sheet Assessment

Leverage is core to a financial firm’s business model (loans funded by deposits). To ensure economic stability and avoid a repeat of the 2008 GFC, regulators require certain levels of capital and liquidity, focusing on the Tier 1 capital ratio.

Tier 1 capital is the highest-quality capital that a firm holds, consisting primarily of common stock and retained earnings, but also physical gold. It serves as the primary cushion against losses and is the first line of defense in times of financial distress.

This capital is divided by risk-weighted assets to derive the Tier 1 capital ratio. Risk-weighted means that cash and US treasury securities are assigned little risk while unsecured consumer loans and equity investments get much higher risk weights, for example.

New regulation after the 2008 financial crisis requires that all firms must maintain a Tier 1 capital ratio greater than 4.5%. On top of this, there are additional buffers based on scale, risk profile, and other regulatory classifications, so that at the end of the day, firms generally must maintain a 7-10% ratio at minimum.

Over the last two years, Morgan Stanley has averaged a Tier 1 capital ratio of 15.5%, which is considered safe and well capitalized in the event that macro or market conditions suddenly deteriorate.

11. Key Takeaways from Morgan Stanley’s Q4 Results

We enjoyed seeing Morgan Stanley beat analysts’ Institutional Securities segment expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its efficiency ratio missed. Overall, we think this was a solid quarter with some key areas of upside. The stock remained flat at $179.94 immediately after reporting.

12. Is Now The Time To Buy Morgan Stanley?

Updated: March 14, 2026 at 12:38 AM EDT

Are you wondering whether to buy Morgan Stanley or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Morgan Stanley doesn’t top our investment wishlist, but we understand that it’s not a bad business. First off, its revenue growth was decent over the last five years, and analysts believe it can continue growing at these levels. And while Morgan Stanley’s TBVPS growth was weak over the last five years, its above-average ROE suggests its management team has made good investment decisions.

Morgan Stanley’s P/E ratio based on the next 12 months is 13.5x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $195.81 on the company (compared to the current share price of $154.03).