Mettler-Toledo (MTD)

Mettler-Toledo doesn’t impress us. Its poor sales growth and falling returns on capital suggest its growth opportunities are shrinking.― StockStory Analyst Team

1. News

2. Summary

Why Mettler-Toledo Is Not Exciting

With roots dating back to the precision balance innovations of Swiss engineer Erhard Mettler, Mettler-Toledo (NYSE:MTD) manufactures precision weighing instruments, analytical equipment, and product inspection systems used in laboratories, industrial settings, and food retail.

- Organic revenue growth fell short of our benchmarks over the past two years and implies it may need to improve its products, pricing, or go-to-market strategy

- Sales trends were unexciting over the last five years as its 5.5% annual growth was below the typical healthcare company

- A bright spot is that its ROIC punches in at 49.4%, illustrating management’s expertise in identifying profitable investments

Mettler-Toledo doesn’t fulfill our quality requirements. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Mettler-Toledo

Mettler-Toledo is trading at $1,210 per share, or 27.1x forward P/E. Not only does Mettler-Toledo trade at a premium to companies in the healthcare space, but this multiple is also high for its top-line growth.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Mettler-Toledo (MTD) Research Report: Q4 CY2025 Update

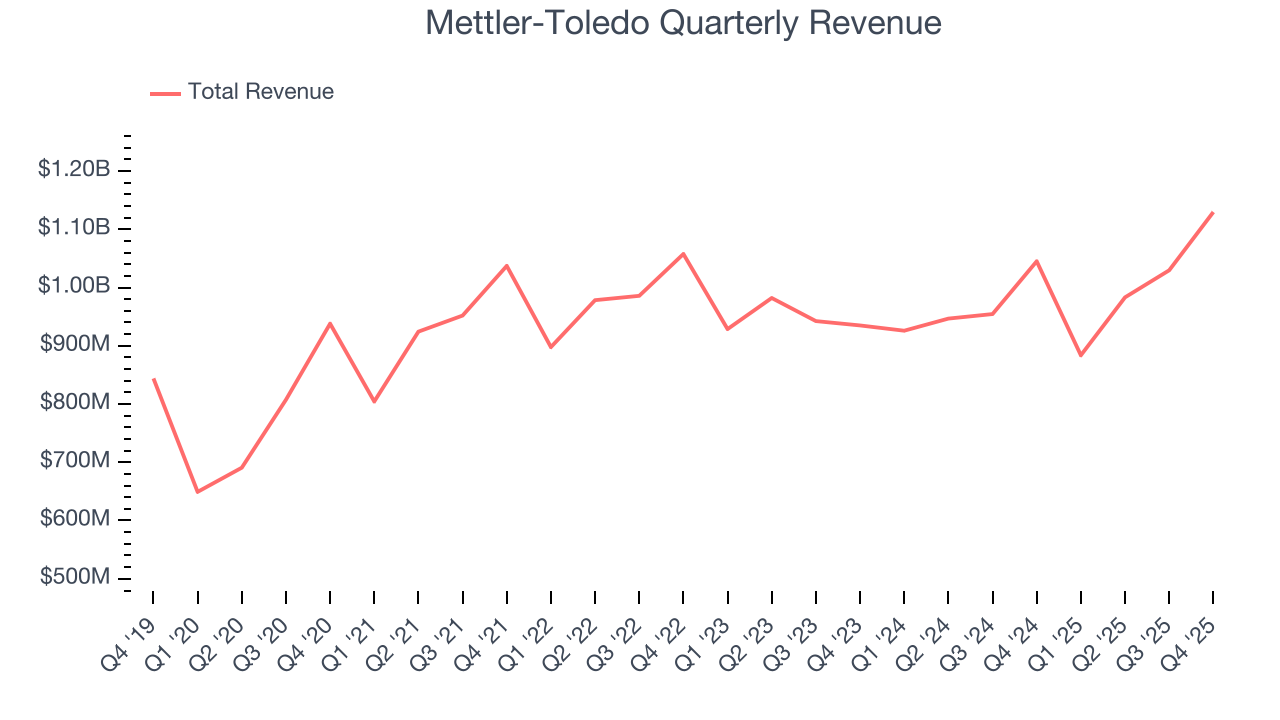

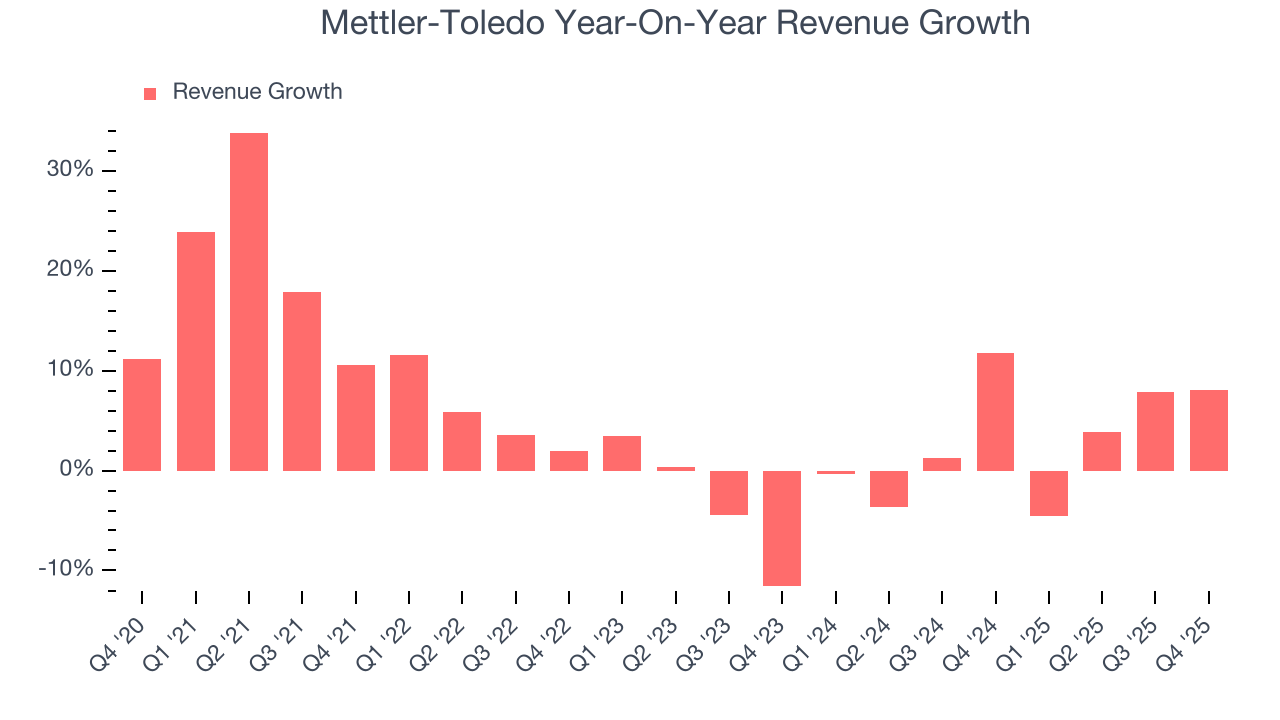

Precision measurement company Mettler-Toledo (NYSE:MTD) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 8.1% year on year to $1.13 billion. On the other hand, next quarter’s revenue guidance of $910.3 million was less impressive, coming in 3.1% below analysts’ estimates. Its non-GAAP profit of $13.36 per share was 4.3% above analysts’ consensus estimates.

Mettler-Toledo (MTD) Q4 CY2025 Highlights:

- Revenue: $1.13 billion vs analyst estimates of $1.10 billion (8.1% year-on-year growth, 2.3% beat)

- Adjusted EPS: $13.36 vs analyst estimates of $12.81 (4.3% beat)

- Revenue Guidance for Q1 CY2026 is $910.3 million at the midpoint, below analyst estimates of $939.6 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $46.38 at the midpoint, beating analyst estimates by 1.2%

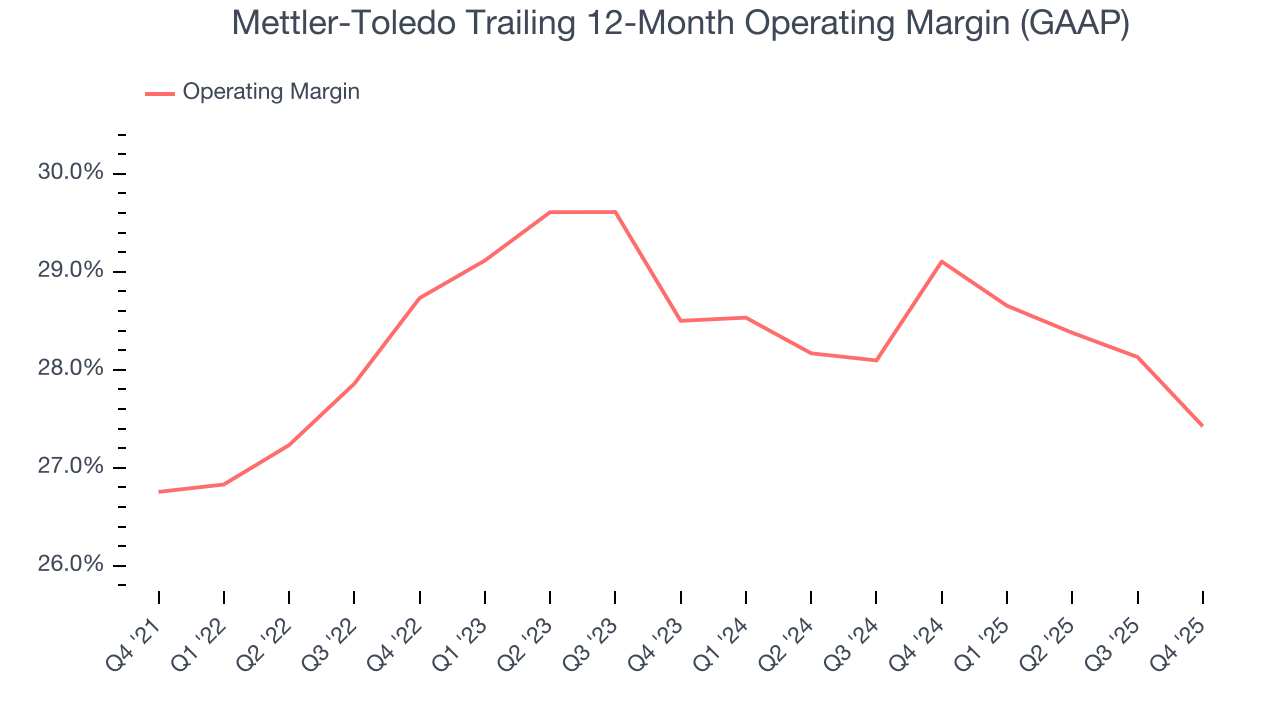

- Operating Margin: 29.1%, down from 31.9% in the same quarter last year

- Free Cash Flow Margin: 16.3%, down from 21.5% in the same quarter last year

- Market Capitalization: $28.39 billion

Company Overview

With roots dating back to the precision balance innovations of Swiss engineer Erhard Mettler, Mettler-Toledo (NYSE:MTD) manufactures precision weighing instruments, analytical equipment, and product inspection systems used in laboratories, industrial settings, and food retail.

The company's product portfolio spans several categories, each serving specific market needs. In laboratories, Mettler-Toledo's balances can measure weights from one ten-millionth of a gram up to 64 kilograms, while its analytical instruments like titrators, pH meters, and thermal analysis systems help scientists analyze chemical compositions and material properties. For industrial customers, the company provides weighing instruments, terminals, and software that integrate into manufacturing processes for quality control and automation.

Product inspection represents another key business area, where Mettler-Toledo's metal detectors, x-ray systems, and checkweighers ensure product safety and compliance in food processing, pharmaceuticals, and consumer goods. The company also serves food retailers with weighing and labeling solutions for fresh goods management.

A pharmaceutical researcher might use a Mettler-Toledo analytical balance to precisely weigh compounds for drug formulation, then employ the company's automated chemistry solutions to monitor the reaction in real-time, ensuring consistent quality. Meanwhile, a food manufacturer might install Mettler-Toledo's checkweighers and metal detectors on production lines to verify product weight and detect potential contaminants before packaging.

The company generates revenue through equipment sales and a substantial service business that provides calibration, compliance, and maintenance services. With manufacturing facilities across China, Switzerland, the United States, Germany, the United Kingdom, and Mexico, Mettler-Toledo maintains a global presence, selling its products in more than 140 countries with direct operations in approximately 40 nations.

Mettler-Toledo's business is organized into five reportable segments: U.S. Operations, Swiss Operations, Western European Operations, Chinese Operations, and Other Operations, reflecting its geographically diversified structure with sales derived from North and South America, Europe, and Asia.

4. Research Tools & Consumables

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

Mettler-Toledo's competitors include Sartorius (OTC:SARTF), Thermo Fisher Scientific (NYSE:TMO), Shimadzu Corporation (OTC:SHMDF), and Agilent Technologies (NYSE:A), which all manufacture various types of precision instruments and analytical equipment.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $4.03 billion in revenue over the past 12 months, Mettler-Toledo has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Mettler-Toledo grew its sales at a mediocre 5.5% compounded annual growth rate. This fell short of our benchmark for the healthcare sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Mettler-Toledo’s recent performance shows its demand has slowed as its annualized revenue growth of 3.1% over the last two years was below its five-year trend.

This quarter, Mettler-Toledo reported year-on-year revenue growth of 8.1%, and its $1.13 billion of revenue exceeded Wall Street’s estimates by 2.3%. Company management is currently guiding for a 3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months, similar to its two-year rate. While this projection suggests its newer products and services will catalyze better top-line performance, it is still below average for the sector.

7. Operating Margin

Mettler-Toledo’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 28.1% over the last five years. This profitability was top-notch for a healthcare business, showing it’s an well-run company with an efficient cost structure.

Looking at the trend in its profitability, Mettler-Toledo’s operating margin of 27.4% for the trailing 12 months may be around the same as five years ago, but it has decreased by 1.1 percentage points over the last two years.

In Q4, Mettler-Toledo generated an operating margin profit margin of 29.1%, down 2.8 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

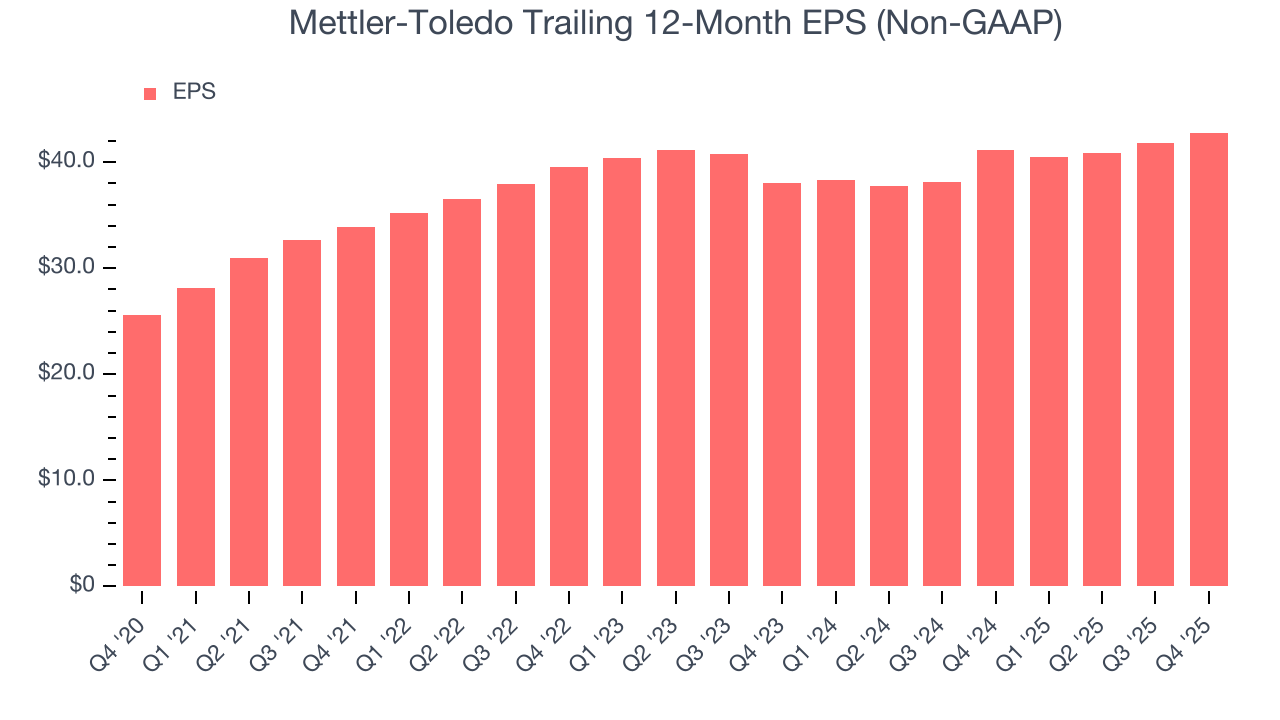

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Mettler-Toledo’s EPS grew at a remarkable 10.8% compounded annual growth rate over the last five years, higher than its 5.5% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

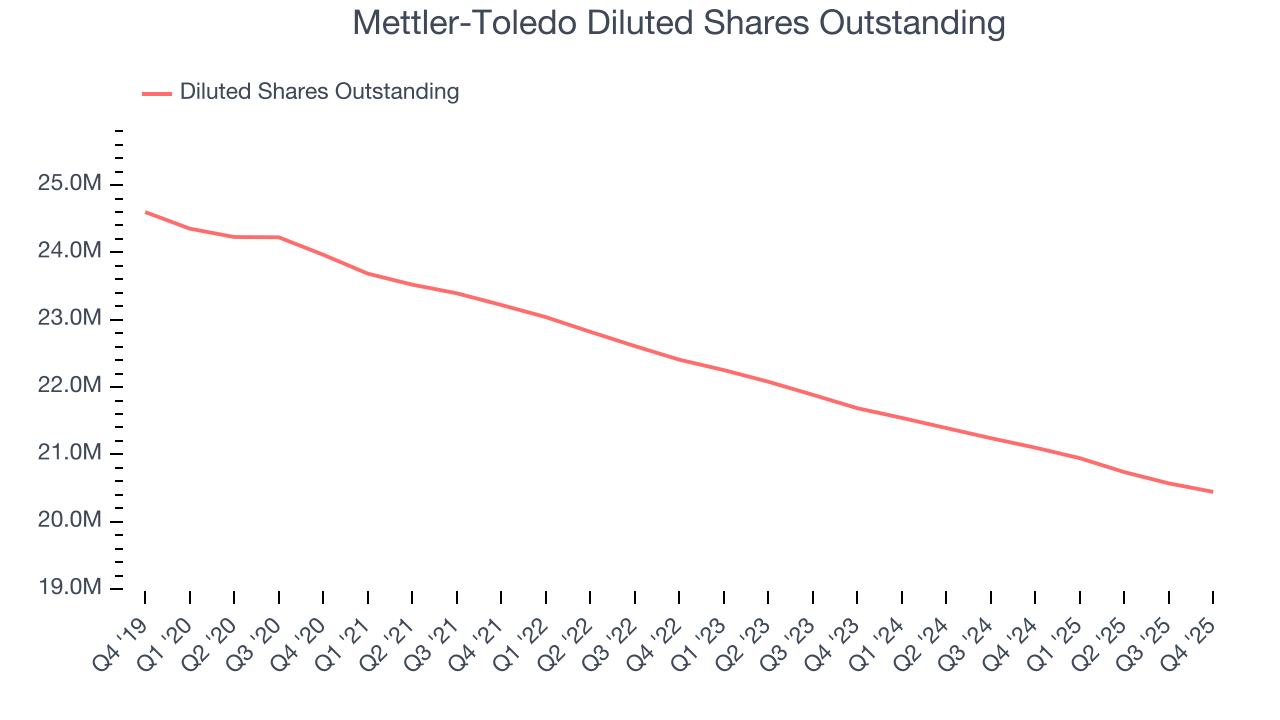

We can take a deeper look into Mettler-Toledo’s earnings quality to better understand the drivers of its performance. A five-year view shows that Mettler-Toledo has repurchased its stock, shrinking its share count by 14.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Mettler-Toledo reported adjusted EPS of $13.36, up from $12.41 in the same quarter last year. This print beat analysts’ estimates by 4.3%. Over the next 12 months, Wall Street expects Mettler-Toledo’s full-year EPS of $42.79 to grow 7.2%.

9. Cash Is King

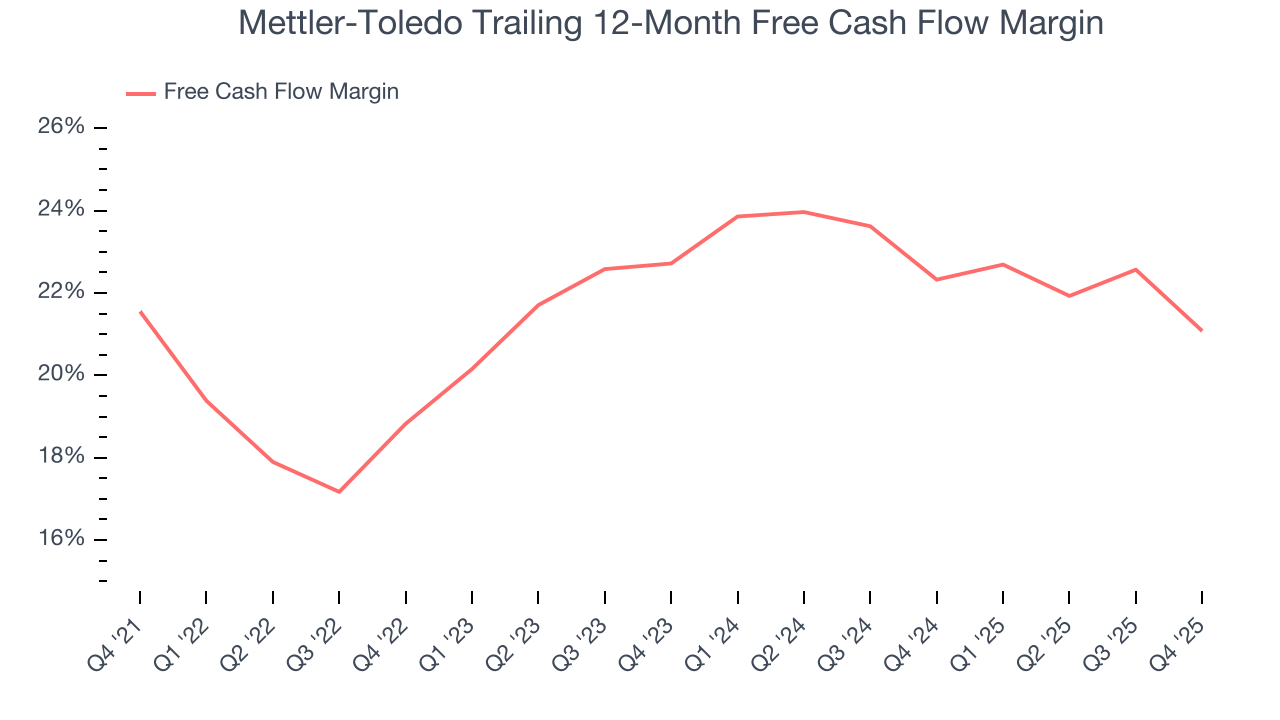

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Mettler-Toledo has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 21.3% over the last five years, quite impressive for a healthcare business.

Mettler-Toledo’s free cash flow clocked in at $184.1 million in Q4, equivalent to a 16.3% margin. The company’s cash profitability regressed as it was 5.2 percentage points lower than in the same quarter last year, prompting us to pay closer attention. Short-term fluctuations typically aren’t a big deal because investment needs can be seasonal, but we’ll be watching to see if the trend extrapolates into future quarters.

10. Return on Invested Capital (ROIC)

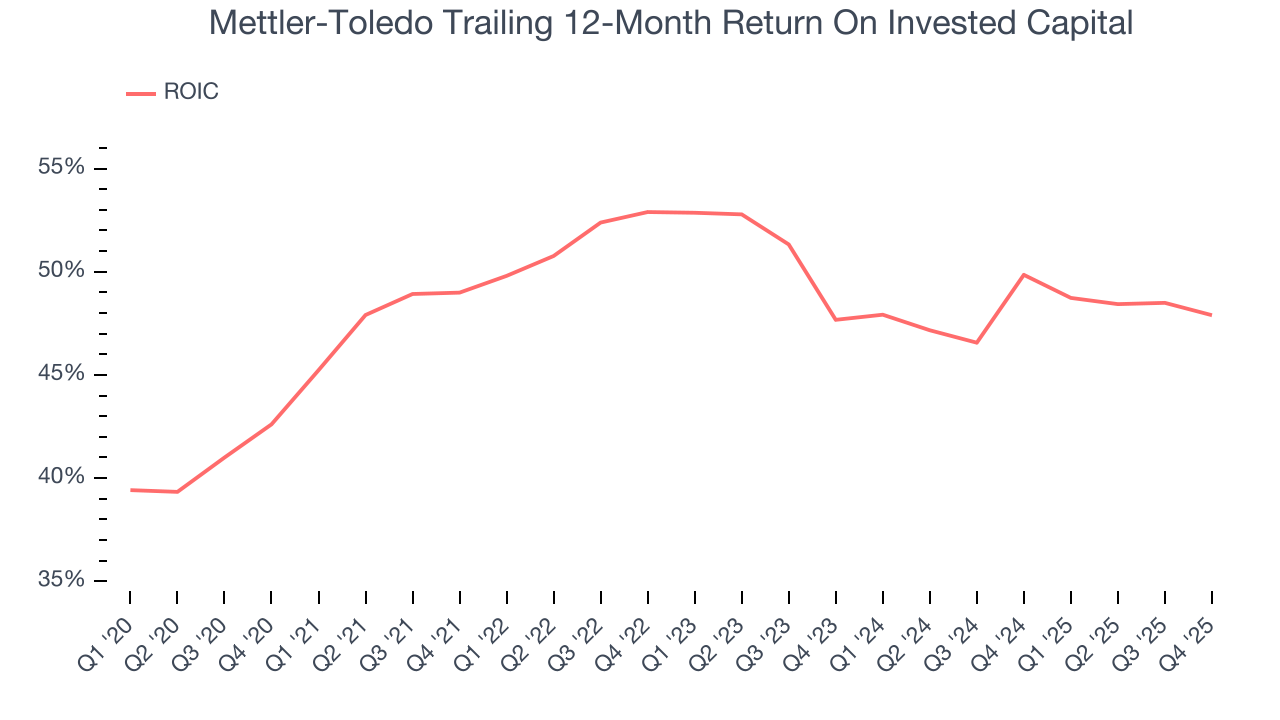

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Mettler-Toledo hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 49.5%, splendid for a healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Mettler-Toledo’s ROIC averaged 2.1 percentage point decreases each year. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

11. Balance Sheet Assessment

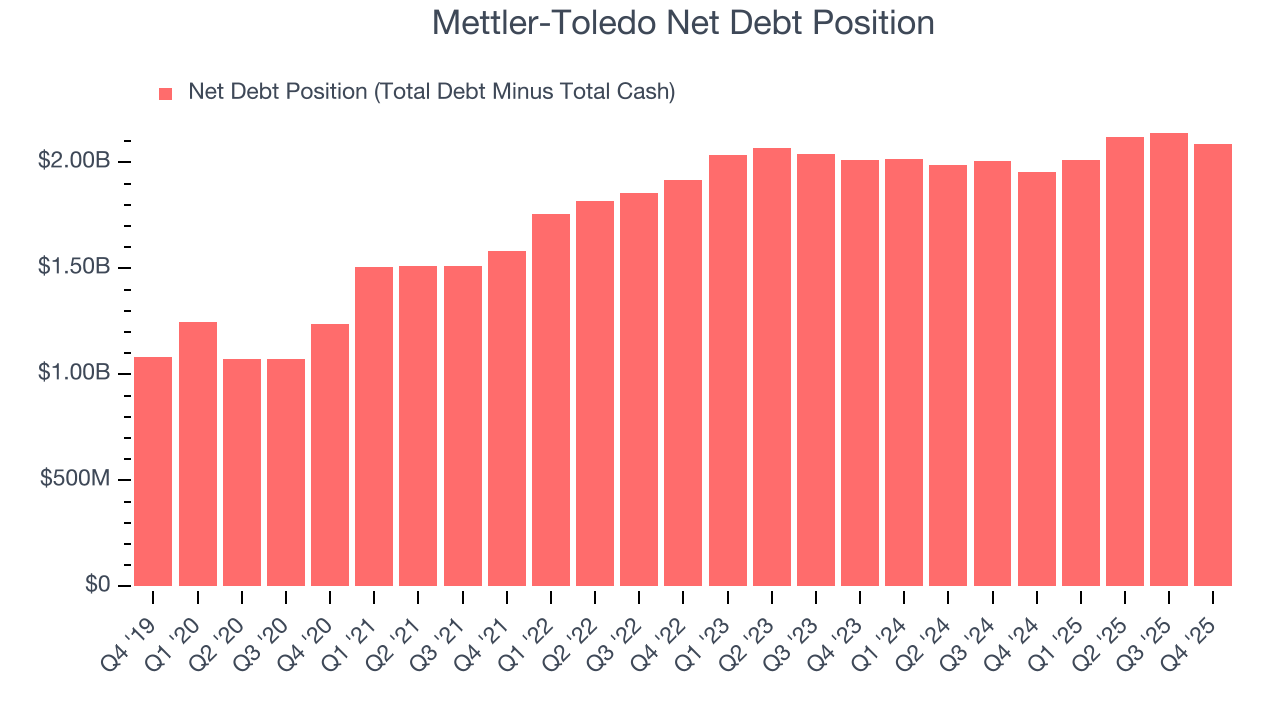

Mettler-Toledo reported $66.89 million of cash and $2.15 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.28 billion of EBITDA over the last 12 months, we view Mettler-Toledo’s 1.6× net-debt-to-EBITDA ratio as safe. We also see its $33.74 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Mettler-Toledo’s Q4 Results

It was encouraging to see Mettler-Toledo beat analysts’ revenue expectations this quarter. We were also happy its full-year EPS guidance narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $1,384 immediately after reporting.

13. Is Now The Time To Buy Mettler-Toledo?

Updated: March 9, 2026 at 1:04 AM EDT

Before investing in or passing on Mettler-Toledo, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

When it comes to Mettler-Toledo’s business quality, there are some positives, but it ultimately falls short. Although its revenue growth was mediocre over the last five years, its stellar ROIC suggests it has been a well-run company historically. Investors should still be cautious, however, as Mettler-Toledo’s organic revenue growth has disappointed.

Mettler-Toledo’s P/E ratio based on the next 12 months is 27.1x. Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $1,501 on the company (compared to the current share price of $1,210).