Annaly Capital Management (NLY)

Annaly Capital Management keeps us up at night. Not only are its sales cratering but also its low returns on capital suggest it struggles to generate profits.― StockStory Analyst Team

1. News

2. Summary

Why We Think Annaly Capital Management Will Underperform

Operating as a real estate investment trust since 1996 with a focus on generating income from interest rate spreads, Annaly Capital Management (NYSE:NLY) is a diversified capital manager that invests in agency mortgage-backed securities, residential mortgage loans, and mortgage servicing rights.

- Products and services are facing significant end-market challenges during this cycle as sales have declined by 12.9% annually over the last five years

- Earnings per share have contracted by 7.9% annually over the last five years, a headwind for returns as stock prices often echo long-term EPS performance

- Loan losses and capital returns have eroded its tangible book value per share this cycle as its tangible book value per share declined by 10.6% annually over the last five years

Annaly Capital Management’s quality is insufficient. You should search for better opportunities.

Why There Are Better Opportunities Than Annaly Capital Management

Annaly Capital Management is trading at $22.10 per share, or 1x forward P/B. This multiple is lower than most banking companies, but for good reason.

We’d rather pay up for companies with elite fundamentals than get a bargain on weak ones. Cheap stocks can be value traps, and as their performance deteriorates, they will stay cheap or get even cheaper.

3. Annaly Capital Management (NLY) Research Report: Q4 CY2025 Update

Mortgage finance REIT Annaly Capital Management (NYSE:NLY) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 74.8% year on year to $921.8 million. Its GAAP profit of $1.40 per share was 66.7% above analysts’ consensus estimates.

Annaly Capital Management (NLY) Q4 CY2025 Highlights:

- Net Interest Income: $366.6 million vs analyst estimates of $484.4 million (81.9% year-on-year decline, 24.3% miss)

- Net Interest Margin: 1.7% vs analyst estimates of 1.6% (13 basis point beat)

- Revenue: $921.8 million vs analyst estimates of $729.8 million (74.8% year-on-year growth, 26.3% beat)

- Efficiency Ratio: 5.6%

- EPS (GAAP): $1.40 vs analyst estimates of $0.84 (66.7% beat)

- Tangible Book Value per Share: $20.21 vs analyst estimates of $20.06 (5.7% year-on-year growth, 0.8% beat)

- Market Capitalization: $16.64 billion

Company Overview

Operating as a real estate investment trust since 1996 with a focus on generating income from interest rate spreads, Annaly Capital Management (NYSE:NLY) is a diversified capital manager that invests in agency mortgage-backed securities, residential mortgage loans, and mortgage servicing rights.

Annaly operates through three main investment groups, each focusing on different segments of the mortgage market. The Annaly Agency Group invests in mortgage-backed securities guaranteed by government-sponsored enterprises like Fannie Mae and Freddie Mac. The Residential Credit Group focuses on non-Agency residential whole loans and securitized products, while the Mortgage Servicing Rights Group invests in the rights to service residential mortgage loans.

The company finances its investments primarily through repurchase agreements with multiple counterparties to diversify exposure. Its wholly-owned subsidiary, Arcola Securities, provides direct access to third-party funding as a FINRA member broker-dealer. Another subsidiary, Onslow Bay Financial, sponsors private-label securitizations that help finance residential mortgage loan investments.

Annaly has established strategic relationships with key mortgage loan originators and aggregators, including major banks, to source proprietary originations. A notable partnership includes a joint venture with GIC Private Limited, a sovereign wealth fund, to invest in residential credit assets. The company has also partnered with Fifth Wall Ventures to identify innovative real estate technology platforms.

As a Real Estate Investment Trust (REIT), Annaly must distribute at least 90% of its taxable income to shareholders annually. This structure provides tax advantages but requires the company to carefully monitor its investments to maintain REIT qualification. The company operates within a complex regulatory framework that includes oversight from FINRA, the SEC, and various state agencies, particularly for its subsidiaries involved in mortgage aggregation and servicing.

4. Thrifts & Mortgage Finance

Thrifts & Mortgage Finance institutions operate by accepting deposits and extending loans primarily for residential mortgages, earning revenue through interest rate spreads (difference between lending rates and borrowing costs) and origination fees. The industry benefits from demographic tailwinds as millennials enter prime homebuying age, technological advancements streamlining the loan approval process, and potential interest rate stabilization improving affordability. However, significant headwinds include net interest margin compression during rate volatility, increased competition from fintech disruptors offering digital-first experiences, mounting regulatory compliance costs, and potential housing market corrections that could impact loan portfolios and default rates.

Annaly's main competitors include other mortgage REITs such as AGNC Investment Corp (NASDAQ:AGNC), Starwood Property Trust (NYSE:STWD), and New Residential Investment Corp (NYSE:NRZ), as well as diversified REITs and financial institutions that invest in mortgage-backed securities.

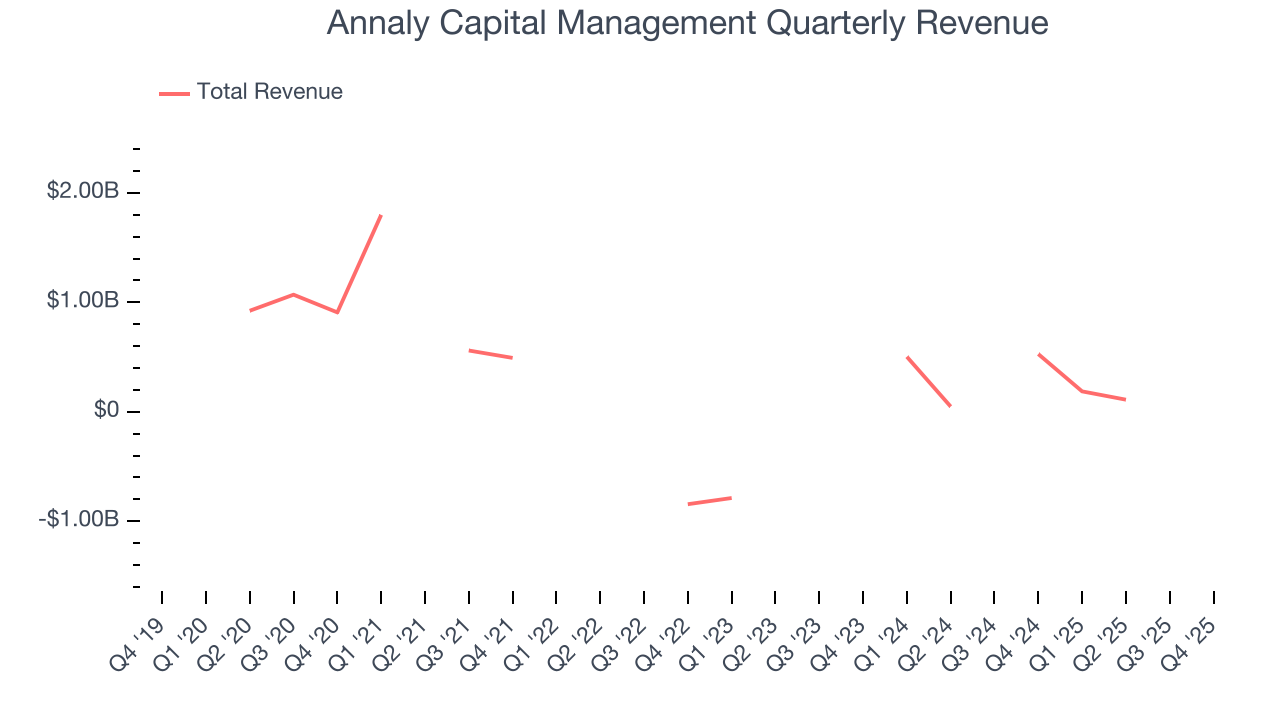

5. Sales Growth

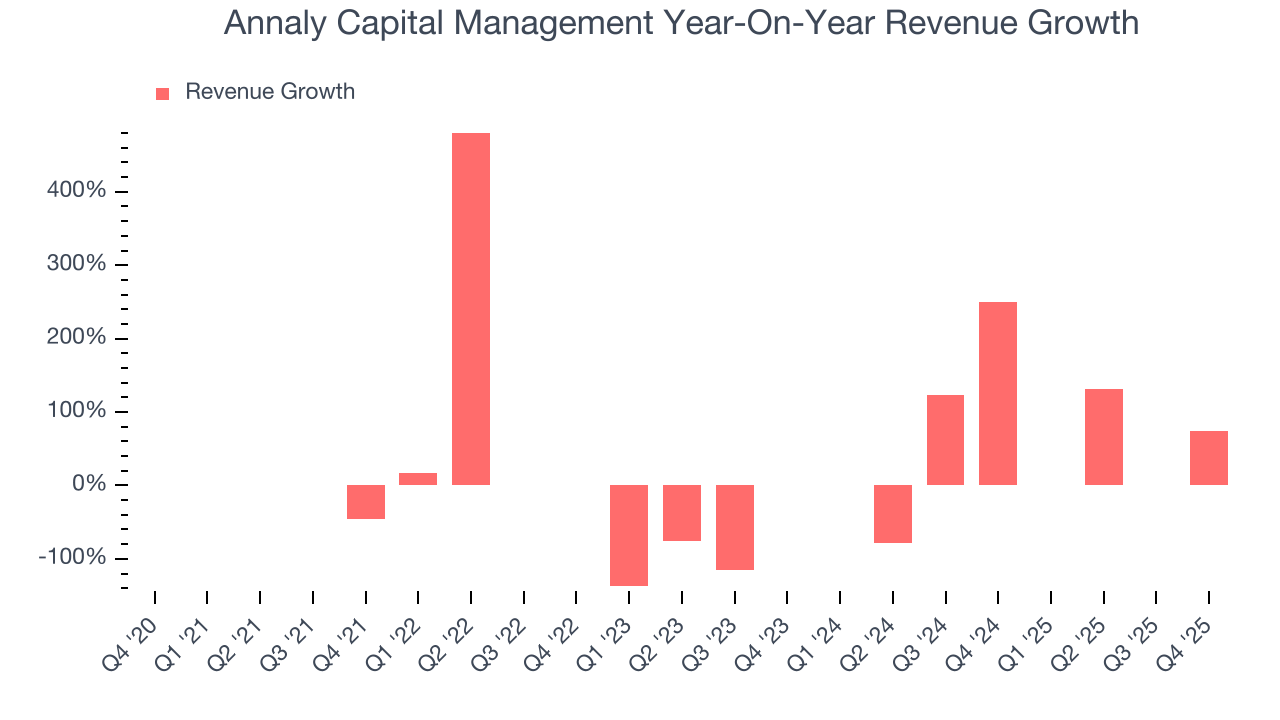

Net interest income and and fee-based revenue are the two pillars supporting bank earnings. The former captures profit from the gap between lending rates and deposit costs, while the latter encompasses charges for banking services, credit products, wealth management, and trading activities. Annaly Capital Management struggled to consistently generate demand over the last five years as its revenue dropped at a 12.9% annual rate. This was below our standards and is a sign of poor business quality.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Annaly Capital Management’s recent performance shows its demand remained suppressed as its revenue has declined by 46% annually over the last two years.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Annaly Capital Management reported magnificent year-on-year revenue growth of 74.8%, and its $921.8 million of revenue beat Wall Street’s estimates by 26.3%.

Net interest income made up 69.8% of the company’s total revenue during the last five years, meaning lending operations are Annaly Capital Management’s largest source of revenue.

Net interest income commands greater market attention due to its reliability and consistency, whereas non-interest income is often seen as lower-quality revenue that lacks the same dependable characteristics.

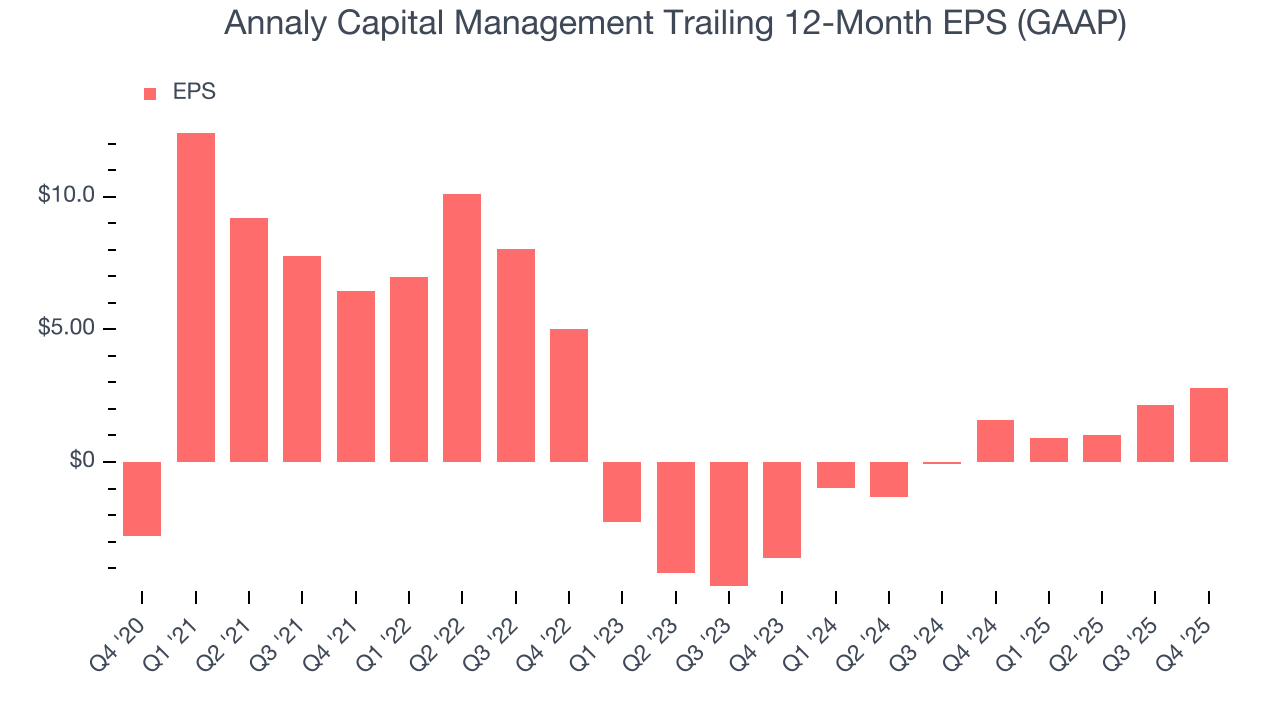

6. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Annaly Capital Management’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Annaly Capital Management, its two-year annual EPS growth of 66.4% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q4, Annaly Capital Management reported EPS of $1.40, up from $0.78 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Annaly Capital Management’s full-year EPS of $2.78 to grow 18.7%.

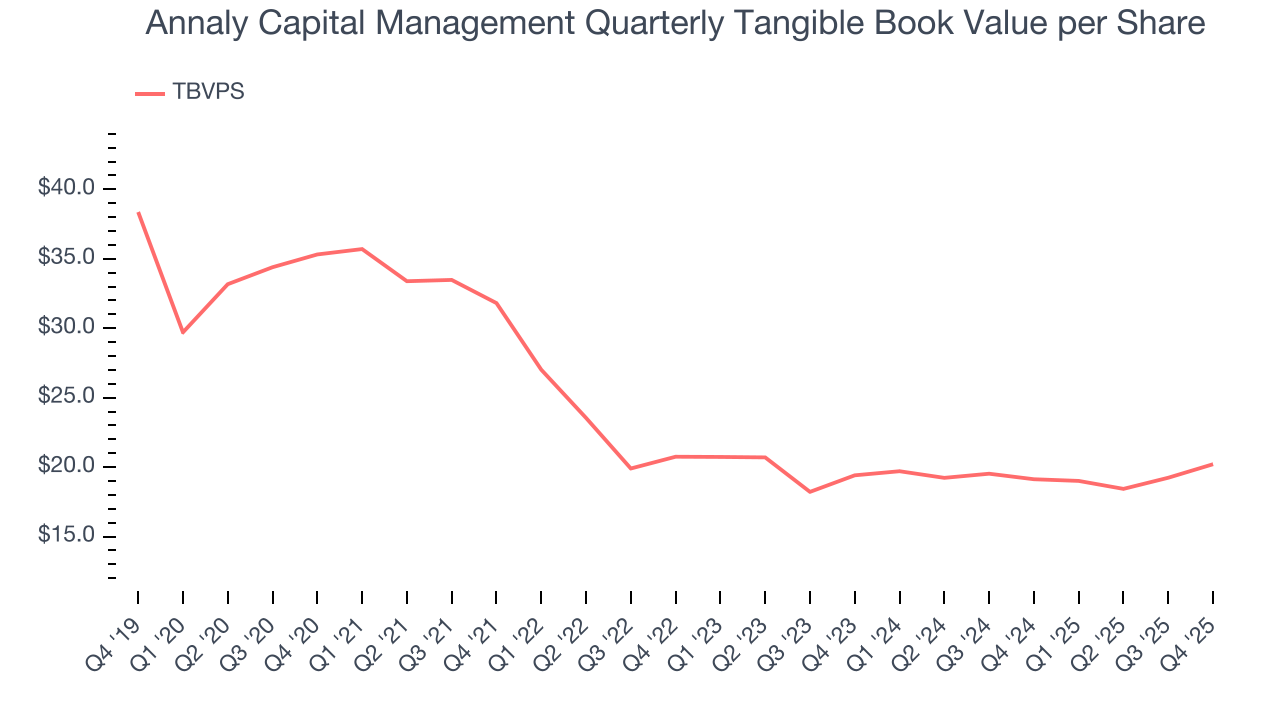

7. Tangible Book Value Per Share (TBVPS)

The balance sheet drives banking profitability since earnings flow from the spread between borrowing and lending rates. As such, valuations for these companies concentrate on capital strength and sustainable equity accumulation potential.

This explains why tangible book value per share (TBVPS) stands as the premier banking metric. TBVPS strips away questionable intangible assets, revealing concrete per-share net worth that investors can trust. Other (and more commonly known) per-share metrics like EPS can sometimes be murky due to M&A or accounting rules allowing for loan losses to be spread out.

Annaly Capital Management’s TBVPS declined at a 10.6% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 2% annually over the last two years from $19.41 to $20.21 per share.

Over the next 12 months, Consensus estimates call for Annaly Capital Management’s TBVPS to remain flat at roughly $20.33, a disappointing projection.

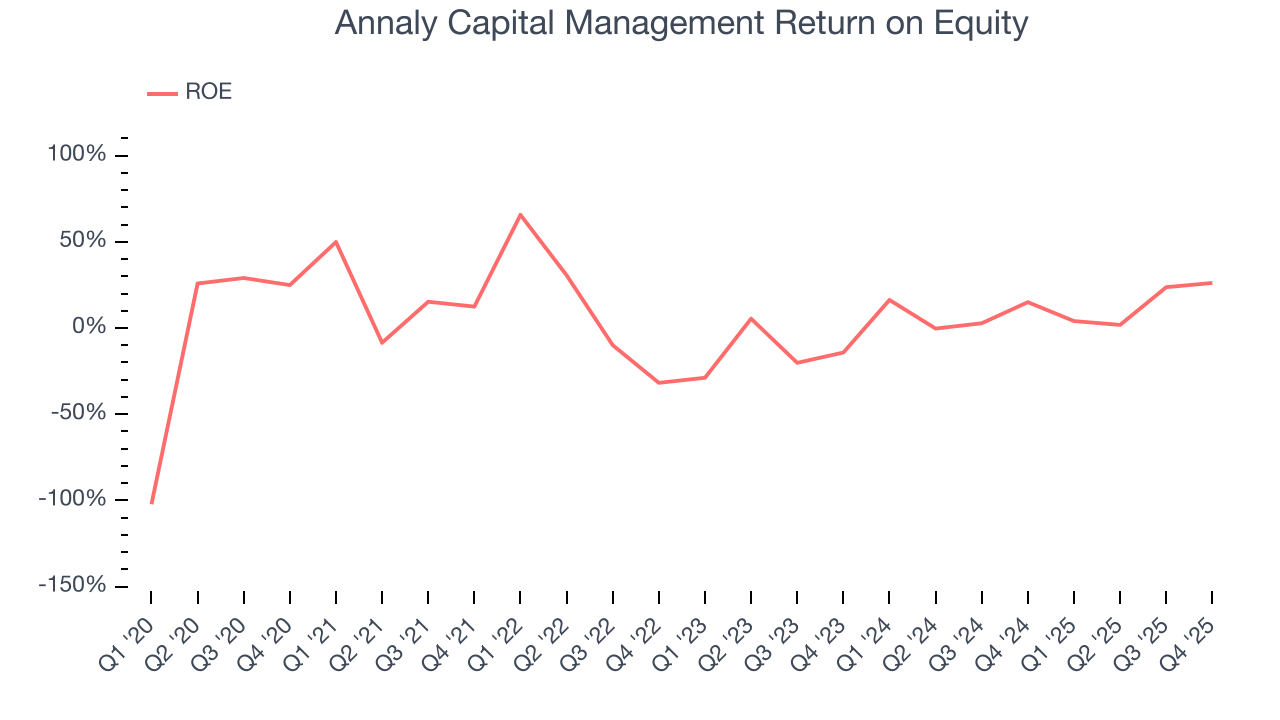

8. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Annaly Capital Management has averaged an ROE of 7.8%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

9. Key Takeaways from Annaly Capital Management’s Q4 Results

It was good to see Annaly Capital Management beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. On the other hand, its net interest income missed. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $24.38 immediately after reporting.

10. Is Now The Time To Buy Annaly Capital Management?

Updated: March 17, 2026 at 1:05 AM EDT

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Annaly Capital Management, you should also grasp the company’s longer-term business quality and valuation.

Annaly Capital Management falls short of our quality standards. To begin with, its revenue has declined over the last five years. While its estimated net interest income growth for the next 12 months is great, the downside is its TBVPS has declined over the last five years. On top of that, its declining EPS over the last five years makes it a less attractive asset to the public markets.

Annaly Capital Management’s P/B ratio based on the next 12 months is 1x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $24.45 on the company (compared to the current share price of $22.10).