Nelnet (NNI)

Nelnet doesn’t impress us. Its low returns on capital raise concerns about its ability to deliver profits, a must for quality companies.― StockStory Analyst Team

1. News

2. Summary

Why Nelnet Is Not Exciting

Starting as a student loan servicer in the 1970s and evolving through the changing landscape of education finance, Nelnet (NYSE:NNI) provides student loan servicing, education technology, payment processing, and banking services while managing a portfolio of education loans.

- Performance over the past five years shows its incremental sales were less profitable, as its 4.3% annual earnings per share growth trailed its revenue gains

- ROE of 9% reflects management’s challenges in identifying attractive investment opportunities

- A positive is that its 8.6% annual revenue growth over the last five years was better than the sector average, highlighting the value of its products and services

Nelnet’s quality doesn’t meet our hurdle. We see more lucrative opportunities elsewhere.

Why There Are Better Opportunities Than Nelnet

Nelnet is trading at $131.78 per share, or 14.8x forward P/E. This multiple rich for the business quality. Not a great combination.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. Nelnet (NNI) Research Report: Q4 CY2025 Update

Education finance company Nelnet (NYSE:NNI) beat Wall Street’s revenue expectations in Q4 CY2025, with sales up 5% year on year to $392 million. Its GAAP profit of $1.60 per share was 1.8% below analysts’ consensus estimates.

Nelnet (NNI) Q4 CY2025 Highlights:

- Net Interest Income: $107.1 million vs analyst estimates of $84 million

- Revenue: $392 million vs analyst estimates of $382 million (5% year-on-year growth, 2.6% beat)

- Pre-tax Profit: $46.38 million (11.8% margin)

- EPS (GAAP): $1.60 vs analyst expectations of $1.63 (1.8% miss)

- Market Capitalization: $4.70 billion

Company Overview

Starting as a student loan servicer in the 1970s and evolving through the changing landscape of education finance, Nelnet (NYSE:NNI) provides student loan servicing, education technology, payment processing, and banking services while managing a portfolio of education loans.

Nelnet operates through four main segments that work together to serve students, families, schools, and financial institutions. Its Loan Servicing and Systems segment handles the administration of student loans for the Department of Education—Nelnet's largest customer—as well as for private lenders. The company processes payments, manages applications, provides customer service, and handles compliance requirements for millions of borrowers.

The Education Technology Services and Payments segment offers financial management tools, school information systems, and payment processing solutions. Through its FACTS brand, Nelnet provides tuition management services to nearly 12,000 K-12 schools, helping families make recurring payments over time while offering schools grant assessment and accounting services. For higher education, Nelnet Campus Commerce delivers payment technologies to over 1,000 colleges and universities worldwide.

Nelnet's Asset Generation and Management segment maintains a portfolio of student loans, primarily federally insured FFELP loans, generating income from the spread between loan yields and financing costs. Meanwhile, Nelnet Bank, launched as an internet industrial bank, focuses on private education loans and unsecured consumer lending.

Beyond these core operations, Nelnet has diversified into renewable energy investments, real estate, and venture capital. The company has invested in solar projects nationwide, providing tax equity investments and developing solar assets. Its venture capital portfolio includes investments in 91 entities, with its largest stake in Hudl, a sports performance analysis company. Nelnet also maintains a significant investment in ALLO, a fiber communications company serving communities across Nebraska, Colorado, and Arizona.

4. Student Loan

Student loan providers finance higher education expenses. Growth opportunities exist in private loan offerings, refinancing existing debt, and international education funding. Challenges include political uncertainty around potential loan forgiveness programs, default risk correlation with employment markets, and increasing scrutiny of educational outcomes relative to debt burdens.

Nelnet's competitors in loan servicing include Navient (NASDAQ:NAVI), MOHELA, and Maximus Federal Services. In the education technology and payment processing space, it competes with Blackbaud (NASDAQ:BLKB), Ellucian, and PowerSchool (NYSE:PWSC). For its banking operations, competitors include Sallie Mae (NASDAQ:SLM) and Discover Financial Services (NYSE:DFS).

5. Revenue Growth

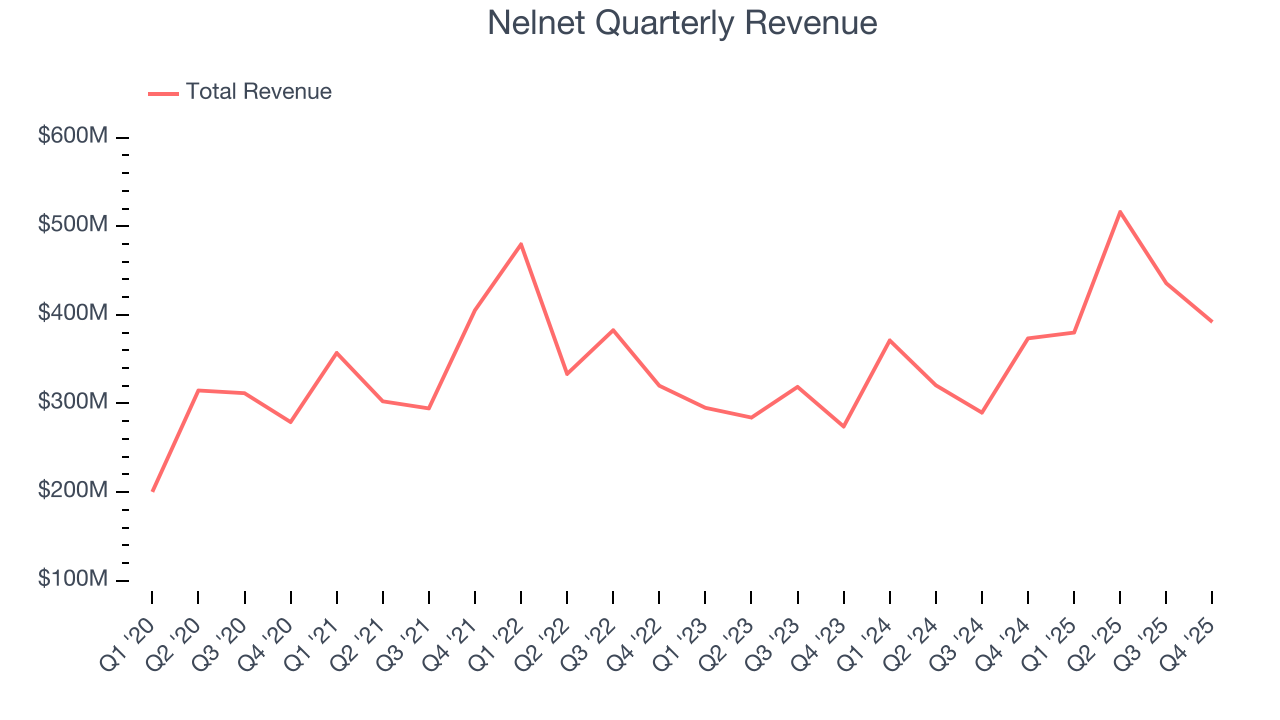

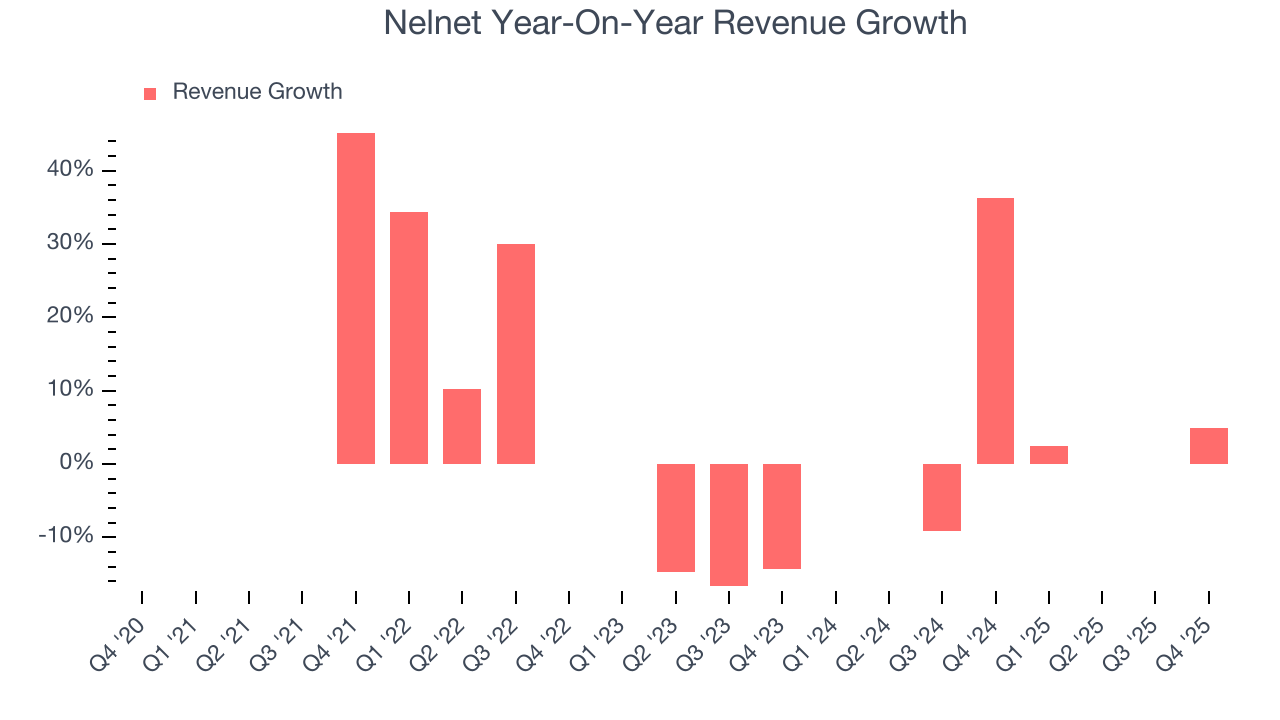

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Thankfully, Nelnet’s 9.3% annualized revenue growth over the last five years was decent. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within financials, a half-decade historical view may miss recent interest rate changes, market returns, and industry trends. Nelnet’s annualized revenue growth of 21.3% over the last two years is above its five-year trend, suggesting its demand recently accelerated.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Nelnet reported modest year-on-year revenue growth of 5% but beat Wall Street’s estimates by 2.6%.

6. Pre-Tax Profit Margin

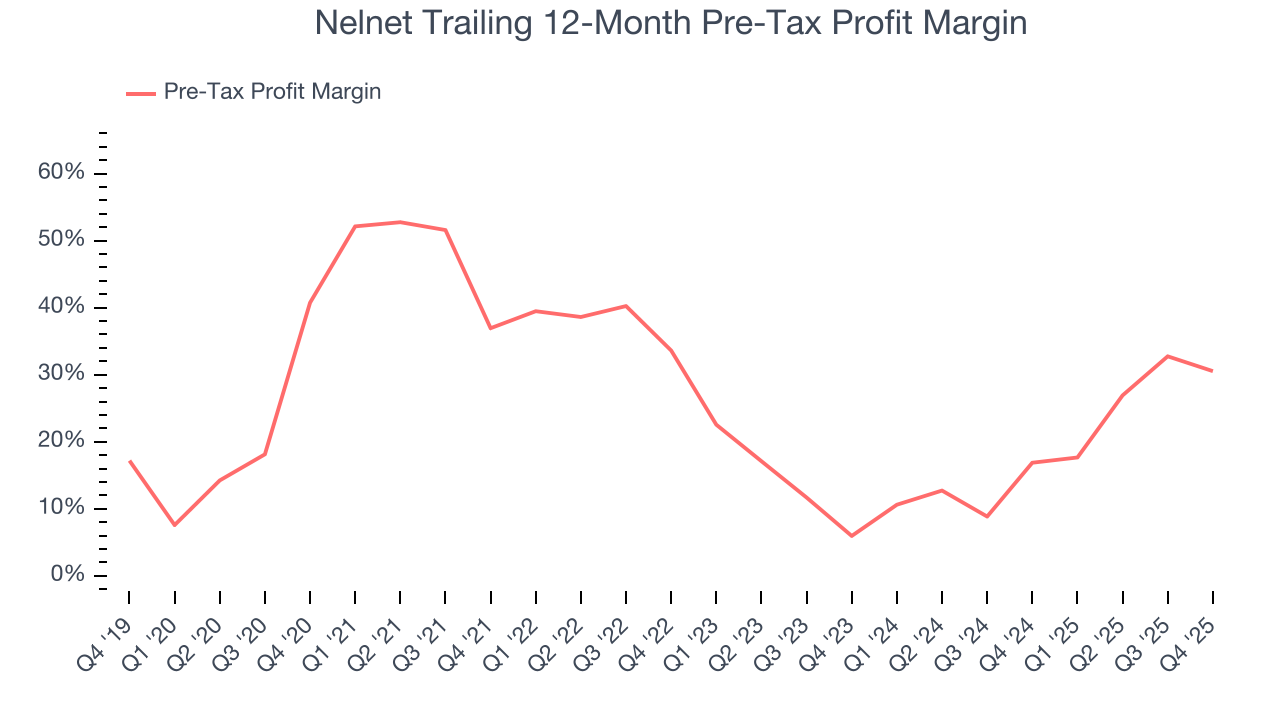

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Student Loan companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

The pre-tax profit margin includes interest because it's central to how financial institutions generate revenue and manage costs. Tax considerations are excluded since they represent government policy rather than operational performance, giving investors a clearer view of business fundamentals.

Over the last five years, Nelnet’s pre-tax profit margin has risen by 10.2 percentage points, going from 36.9% to 30.5%. Luckily, it seems the company has recently taken steps to address its expense base as its pre-tax profit margin expanded by 24.6 percentage points on a two-year basis.

Nelnet’s pre-tax profit margin came in at 11.8% this quarter. This result was 9.2 percentage points worse than the same quarter last year.

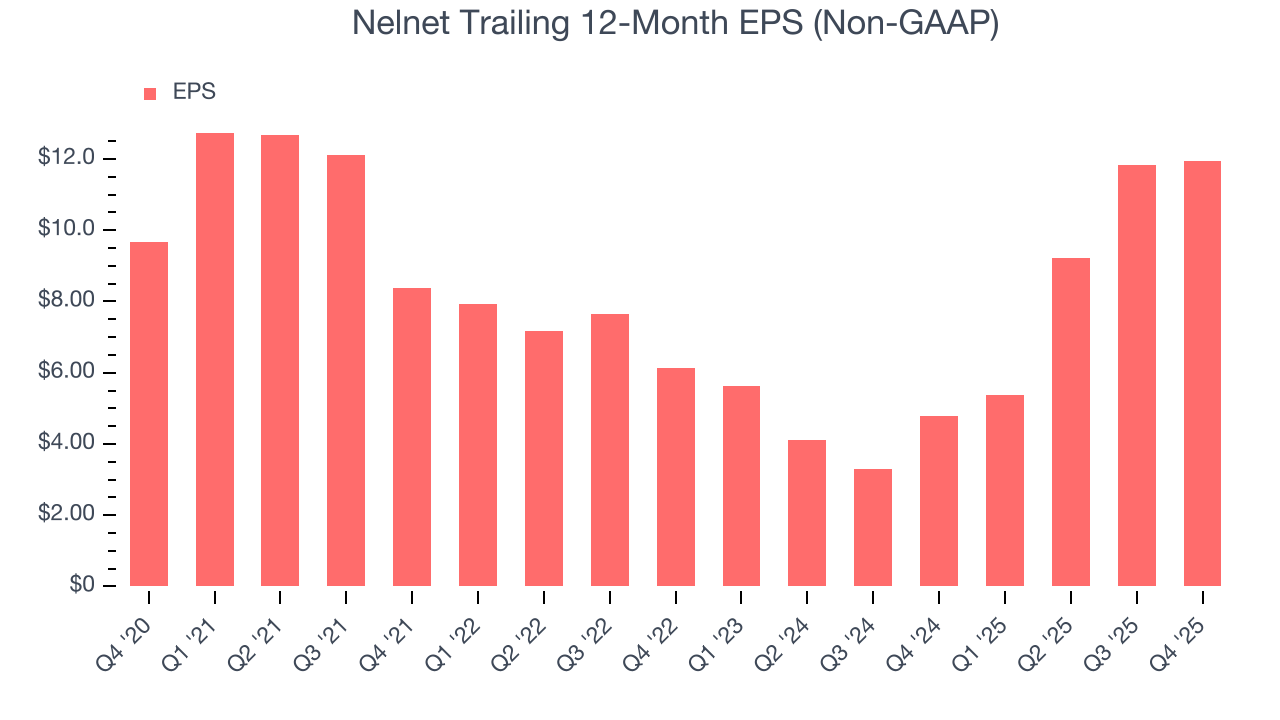

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Nelnet’s EPS grew at a weak 4.3% compounded annual growth rate over the last five years, lower than its 8.7% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded due to factors such as interest expenses and taxes.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Nelnet, its two-year annual EPS growth of 63.5% was higher than its five-year trend. This acceleration made it one of the faster-growing financials companies in recent history.

In Q4, Nelnet reported adjusted EPS of $1.56, up from $1.44 in the same quarter last year. Despite growing year on year, this print missed analysts’ estimates. Over the next 12 months, Wall Street expects Nelnet’s full-year EPS of $11.95 to shrink by 26.3%.

8. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Nelnet has averaged an ROE of 9.3%, uninspiring for a company operating in a sector where the average shakes out around 10%. We’re optimistic Nelnet can turn the ship around given its success in other measures of financial health.

9. Balance Sheet Assessment

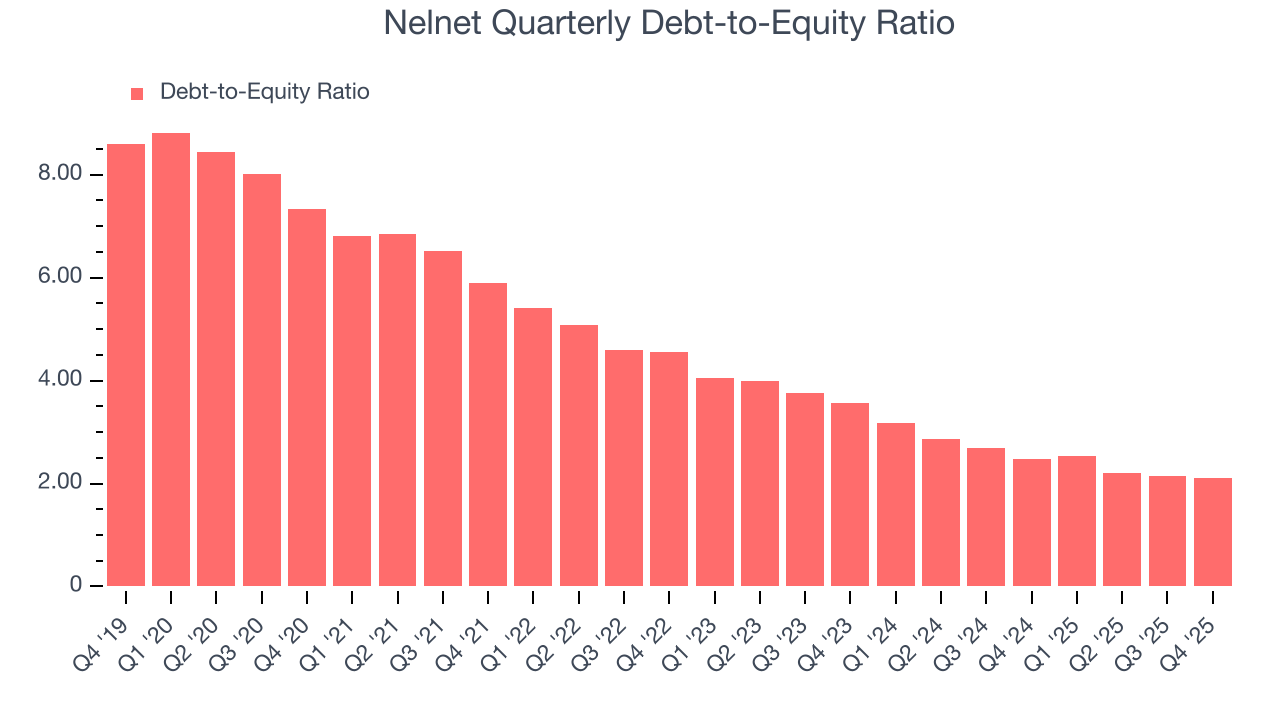

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Nelnet currently has $7.78 billion of debt and $3.69 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 2.2×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

10. Key Takeaways from Nelnet’s Q4 Results

We were impressed by how significantly Nelnet blew past analysts’ net interest income expectations this quarter. We were also happy its revenue outperformed Wall Street’s estimates. On the other hand, its EPS missed. Overall, this print had some key positives. Investors were likely hoping for more, and shares traded down 2.2% to $128.51 immediately following the results.

11. Is Now The Time To Buy Nelnet?

Updated: March 5, 2026 at 11:58 PM EST

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Nelnet doesn’t top our investment wishlist, but we understand that it’s not a bad business. To kick things off, its revenue growth was decent over the last five years. Investors should tread carefully with this one, however, as its declining pre-tax profit margin shows the business has become less efficient.

Nelnet’s P/E ratio based on the next 12 months is 14.8x. Beauty is in the eye of the beholder, but our analysis shows the upside isn’t great compared to the potential downside. We're pretty confident there are superior stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $140 on the company (compared to the current share price of $131.78).