Oscar Health (OSCR)

We’re bullish on Oscar Health. It’s one of the fastest-growing companies we cover, and there’s a solid chance its momentum will continue.― StockStory Analyst Team

1. News

2. Summary

Why We Like Oscar Health

Founded in 2012 to simplify the notoriously complex American healthcare system, Oscar Health (NYSE:OSCR) is a technology-focused health insurance company that offers individual and small group health plans through its cloud-native platform.

- Market share has increased this cycle as its 49% annual revenue growth over the last five years was exceptional

- Market share is on track to rise over the next 12 months as its 60.5% projected revenue growth implies demand will accelerate from its two-year trend

- Earnings per share grew by 13.2% annually over the last four years and trumped its peers

Oscar Health is at the top of our list. The price looks fair when considering its quality, and we think now is a favorable time to buy.

Why Is Now The Time To Buy Oscar Health?

Oscar Health’s stock price of $11.07 implies a valuation ratio of 30.4x forward P/E. Most companies in the healthcare sector may feature a cheaper multiple, but we think Oscar Health is priced fairly given its fundamentals.

By definition, where you buy a stock impacts returns. But according to our work on the topic, business quality is a much bigger determinant of market outperformance over the long term compared to entry price.

3. Oscar Health (OSCR) Research Report: Q4 CY2025 Update

Health insurance company Oscar Health (NYSE:OSCR) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 17.3% year on year to $2.81 billion. On the other hand, the company’s full-year revenue guidance of $18.85 billion at the midpoint came in 47.8% above analysts’ estimates. Its GAAP loss of $1.24 per share was 43.7% below analysts’ consensus estimates.

Oscar Health (OSCR) Q4 CY2025 Highlights:

- Revenue: $2.81 billion vs analyst estimates of $3.12 billion (17.3% year-on-year growth, 10.2% miss)

- EPS (GAAP): -$1.24 vs analyst expectations of -$0.86 (43.7% miss)

- Adjusted EBITDA: -$307.8 million (-11% margin, 173% year-on-year decline)

- Operating Margin: -11.9%, down from -6.2% in the same quarter last year

- Free Cash Flow Margin: 23.6%, up from 14.2% in the same quarter last year

- Market Capitalization: $3.35 billion

Company Overview

Founded in 2012 to simplify the notoriously complex American healthcare system, Oscar Health (NYSE:OSCR) is a technology-focused health insurance company that offers individual and small group health plans through its cloud-native platform.

Oscar Health operates primarily in the Affordable Care Act (ACA) marketplace, offering various metal-tier plans (Bronze, Silver, Gold, and Platinum) that differ in premium costs and cost-sharing structures. The company differentiates itself through its proprietary technology platform that powers both its insurance business and services for other healthcare organizations through its +Oscar offering.

At the core of Oscar's business model is what it calls its "member engagement engine" – a system designed to build trust with members, collect personalized health data, and guide users to appropriate care options. Members interact with features like Care Teams, which help navigate healthcare decisions, and Campaign Builder, which delivers personalized health recommendations based on predictive analytics.

For example, an Oscar member with diabetes might receive targeted communications about preventive care appointments, medication adherence reminders, and connections to in-network specialists – all coordinated through the platform. This approach aims to improve health outcomes while managing costs.

Oscar generates revenue primarily through insurance premiums, including those paid directly by members and government subsidies through the ACA's Advanced Premium Tax Credit program. The company also earns revenue by licensing its technology platform to other healthcare organizations through +Oscar, which serves approximately 500,000 lives beyond Oscar's own insurance members.

Oscar operates in 20 states across the U.S., partnering with health systems and provider networks to create exclusive provider organization (EPO) networks for individual plans, while its small group plans (offered through a partnership with Cigna) utilize broader preferred provider organization (PPO) networks.

4. Health Insurance Providers

Upfront premiums collected by health insurers lead to reliable revenue, but profitability ultimately depends on accurate risk assessments and the ability to control medical costs. Health insurers are also highly sensitive to regulatory changes and economic conditions such as unemployment. Going forward, the industry faces tailwinds from an aging population, increasing demand for personalized healthcare services, and advancements in data analytics to improve cost management. However, continued regulatory scrutiny on pricing practices, the potential for government-led reforms such as expanded public healthcare options, and inflation in medical costs could add volatility to margins. One big debate among investors is the long-term impact of AI and whether it will help underwriting, fraud detection, and claims processing or whether it may wade into ethical grey areas like reinforcing biases and widening disparities in medical care.

Oscar Health competes with major health insurance providers like UnitedHealth Group (NYSE:UNH), Cigna (NYSE:CI), Anthem/Elevance Health (NYSE:ELV), and Centene (NYSE:CNC), as well as other tech-focused insurance companies like Bright Health Group (NYSE:BHG) and Clover Health (NASDAQ:CLOV).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $11.7 billion in revenue over the past 12 months, Oscar Health has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

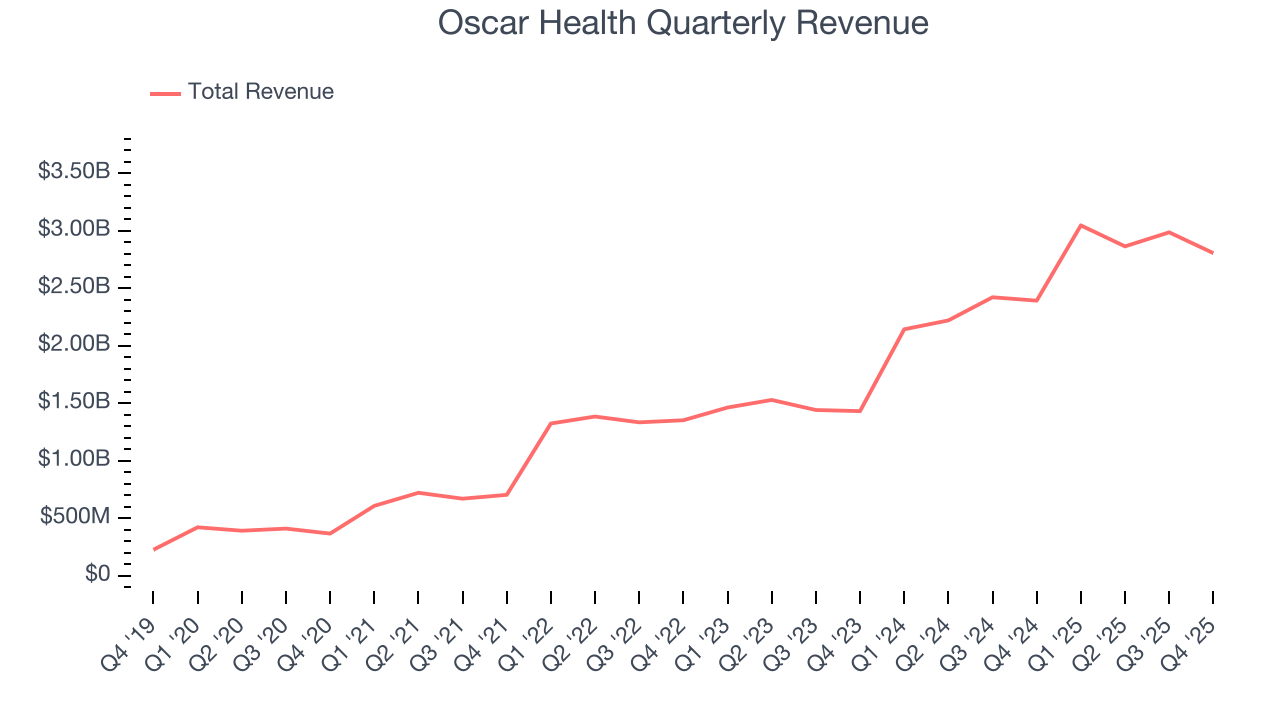

6. Revenue Growth

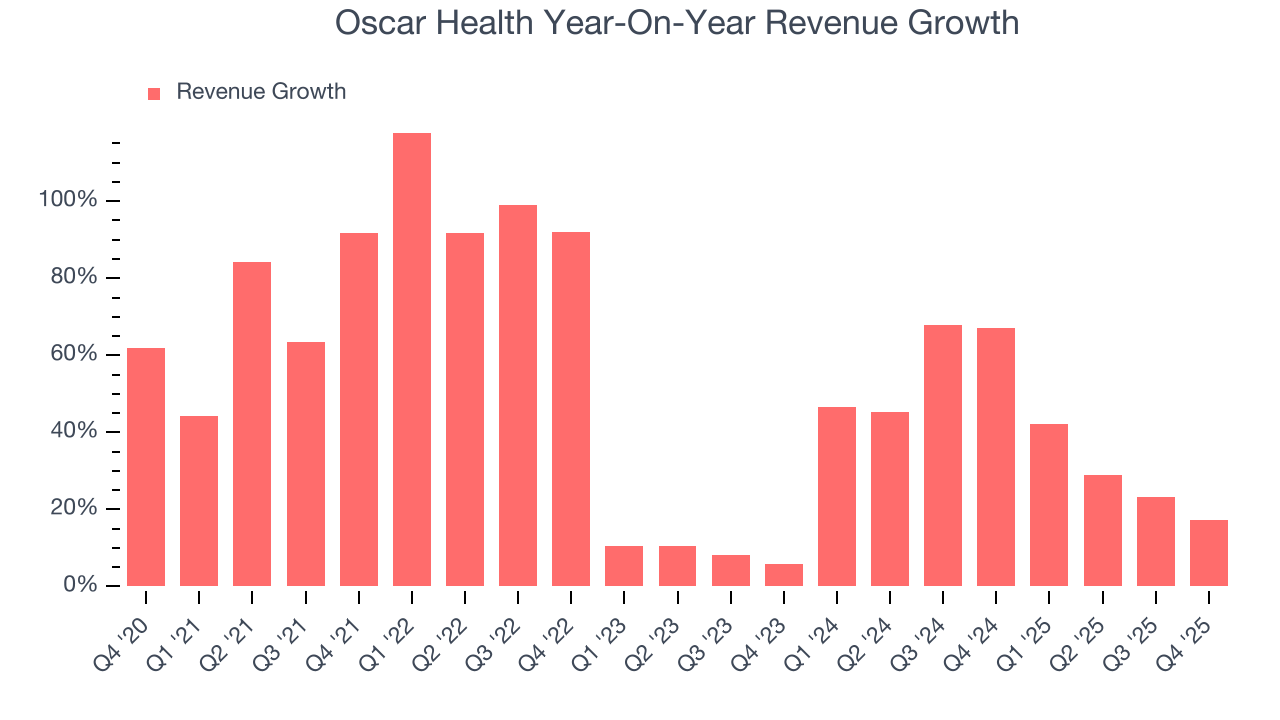

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Oscar Health’s sales grew at an incredible 49% compounded annual growth rate over the last five years. Its growth surpassed the average healthcare company and shows its offerings resonate with customers, a great starting point for our analysis.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Oscar Health’s annualized revenue growth of 41.2% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

This quarter, Oscar Health’s revenue grew by 17.3% year on year to $2.81 billion but fell short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 9.9% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is attractive given its scale and indicates the market is forecasting success for its products and services.

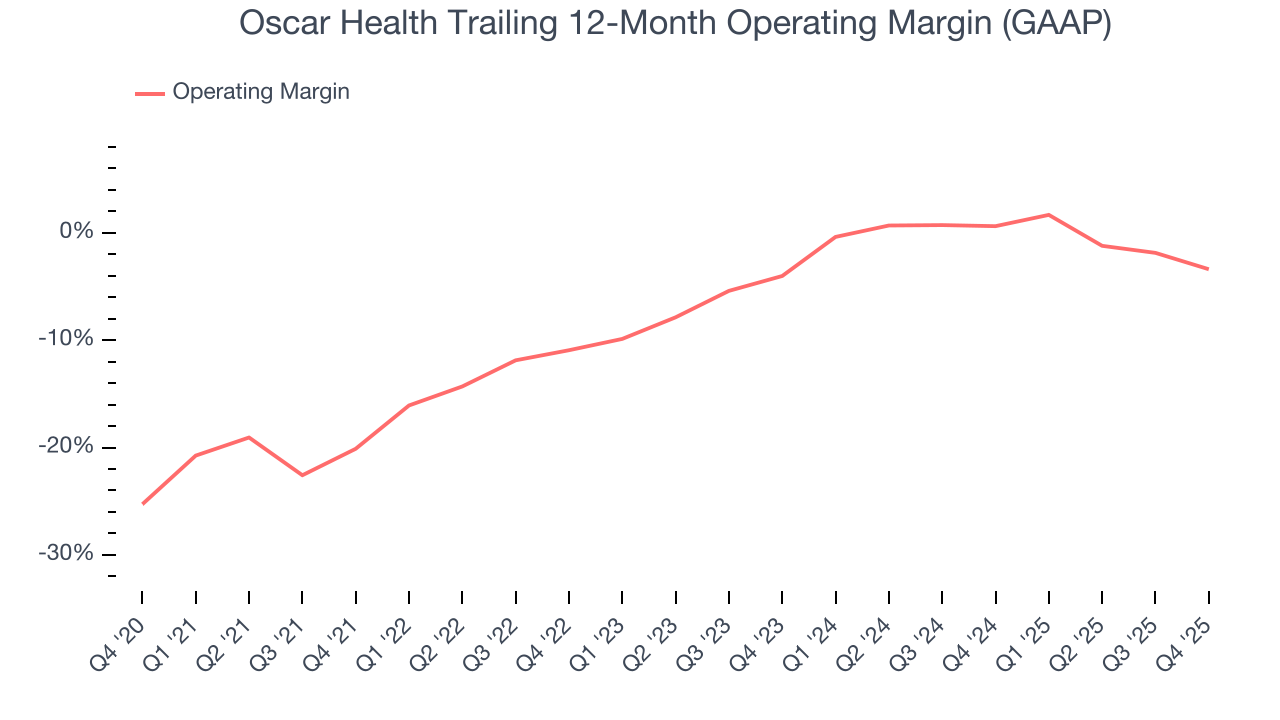

7. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Oscar Health’s high expenses have contributed to an average operating margin of negative 4.9% over the last five years. Unprofitable healthcare companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Oscar Health’s operating margin rose by 16.7 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q4, Oscar Health generated a negative 11.9% operating margin.

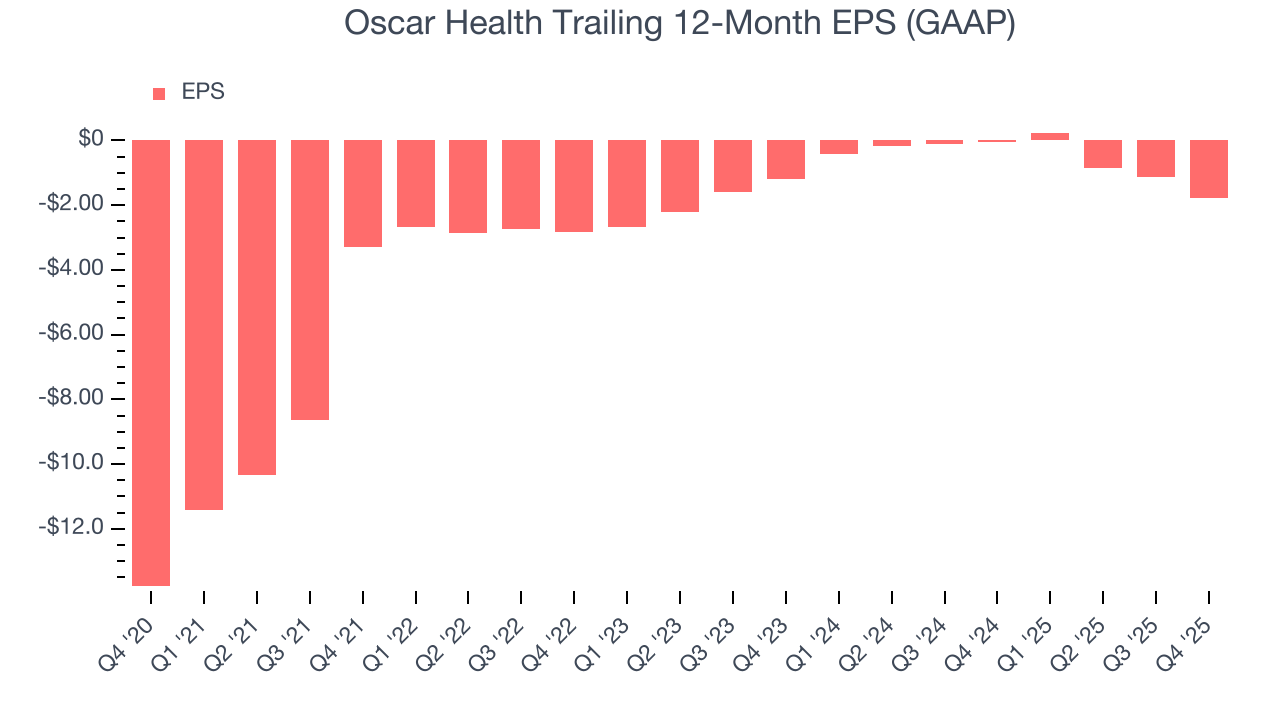

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Although Oscar Health’s full-year earnings are still negative, it reduced its losses and improved its EPS by 33.7% annually over the last five years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

In Q4, Oscar Health reported EPS of negative $1.24, down from negative $0.62 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Oscar Health to improve its earnings losses. Analysts forecast its full-year EPS of negative $1.76 will advance to negative $0.07.

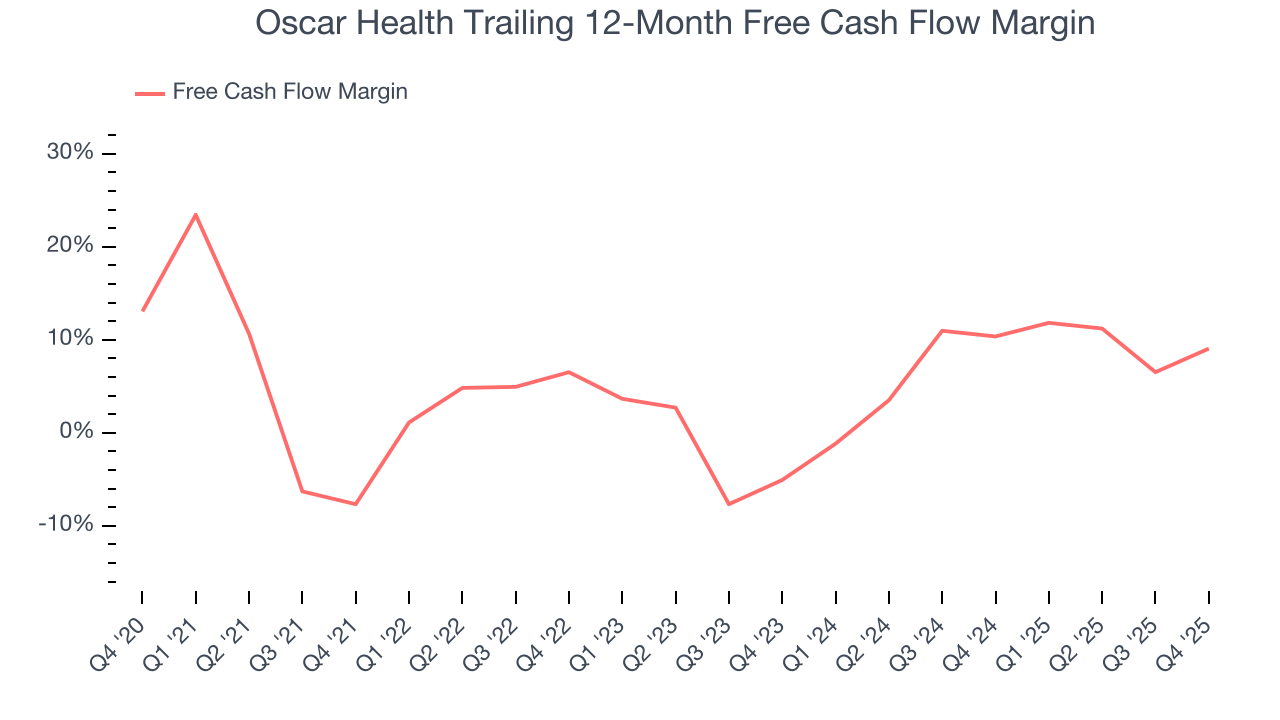

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Oscar Health has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 5.3% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that Oscar Health’s margin expanded by 16.7 percentage points during that time. This is encouraging because it gives the company more optionality.

Oscar Health’s free cash flow clocked in at $662.8 million in Q4, equivalent to a 23.6% margin. This result was good as its margin was 9.4 percentage points higher than in the same quarter last year, building on its favorable historical trend.

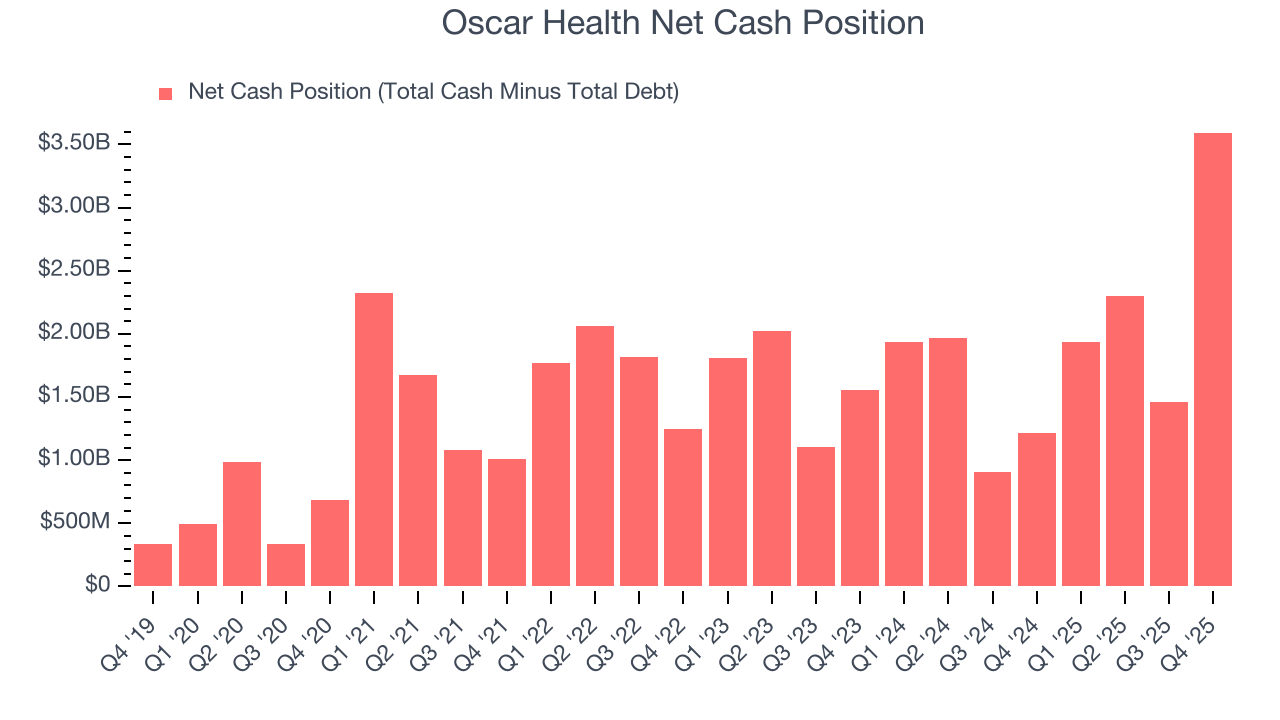

10. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Oscar Health is a well-capitalized company with $4.02 billion of cash and $430.1 million of debt on its balance sheet. This $3.59 billion net cash position is 107% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

11. Key Takeaways from Oscar Health’s Q4 Results

We were impressed by Oscar Health’s optimistic full-year revenue guidance, which blew past analysts’ expectations. On the other hand, its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 1.4% to $12.49 immediately after reporting.

12. Is Now The Time To Buy Oscar Health?

Updated: March 29, 2026 at 12:35 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Oscar Health.

Oscar Health is truly a cream-of-the-crop healthcare company. To begin with, its revenue growth was exceptional over the last five years, and its growth over the next 12 months is expected to accelerate. And while its operating margins reveal poor profitability compared to other healthcare companies, its rising cash profitability gives it more optionality. Additionally, Oscar Health’s expanding adjusted operating margin shows the business has become more efficient.

Oscar Health’s P/E ratio based on the next 12 months is 30.4x. Looking across the spectrum of healthcare businesses, Oscar Health’s fundamentals clearly illustrate it’s a special business. We like the stock at this price.

Wall Street analysts have a consensus one-year price target of $15.40 on the company (compared to the current share price of $11.07), implying they see 39.1% upside in buying Oscar Health in the short term.