Planet Labs (PL)

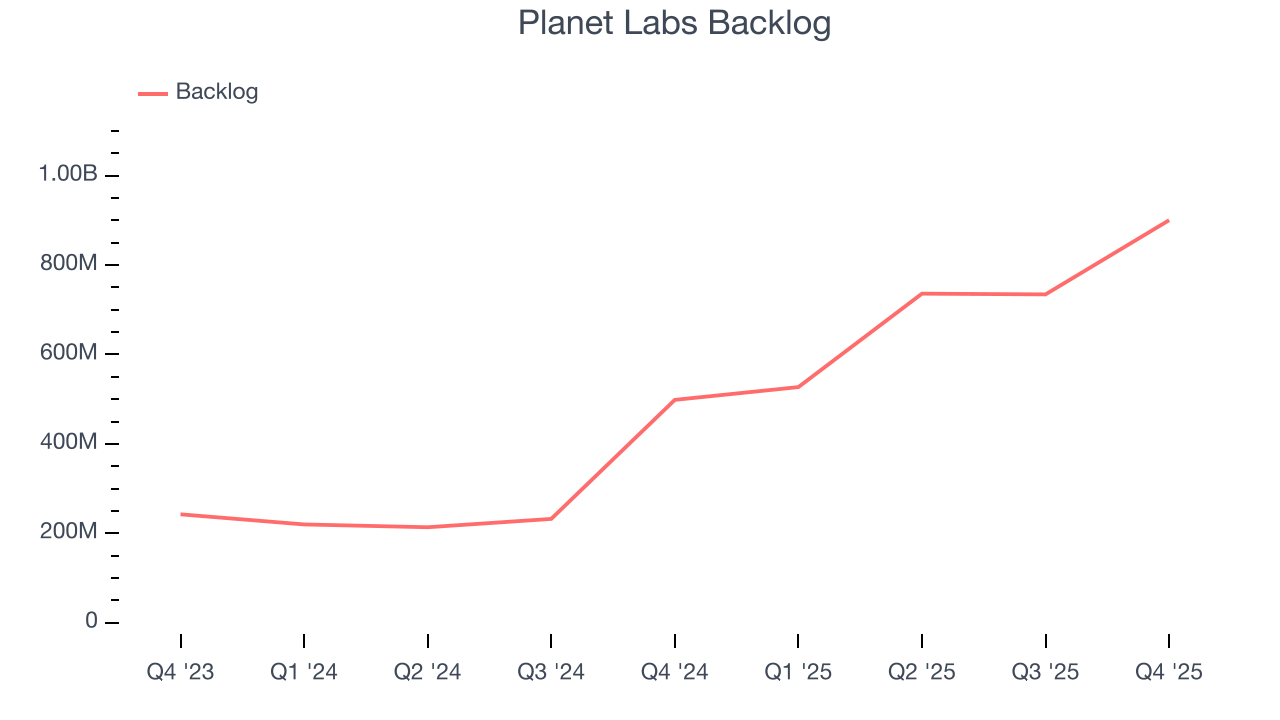

Planet Labs sets the gold standard. Its robust backlog growth shows it has a long tail of demand that will fuel sales for many quarters.― StockStory Analyst Team

1. News

2. Summary

Why We Like Planet Labs

Pioneering the concept of "agile aerospace" with hundreds of small but powerful satellites, Planet Labs (NYSE:PL) operates the world's largest fleet of Earth observation satellites, capturing daily images of our planet to provide insights on deforestation, agriculture, and climate change.

- Annual revenue growth of 22.2% over the past five years was outstanding, reflecting market share gains this cycle

- Earnings growth has trumped its peers over the last four years as its EPS has compounded at 100% annually

- Projected revenue growth of 40.7% for the next 12 months is above its two-year trend, pointing to accelerating demand

Planet Labs is a no-brainer. The valuation looks reasonable in light of its quality, and we think now is a favorable time to buy the stock.

Why Is Now The Time To Buy Planet Labs?

Planet Labs’s stock price of $30.62 implies a valuation ratio of 1,287.7x forward EV-to-EBITDA. Yes, the stock’s seemingly high valuation multiple could mean short-term volatility. But given its business quality, we think the multiple is justified.

Our work shows, time and again, that buying high-quality companies and holding them routinely leads to market outperformance. Over a multi-year investment horizon, entry price doesn’t matter nearly as much as business quality.

3. Planet Labs (PL) Research Report: Q4 CY2025 Update

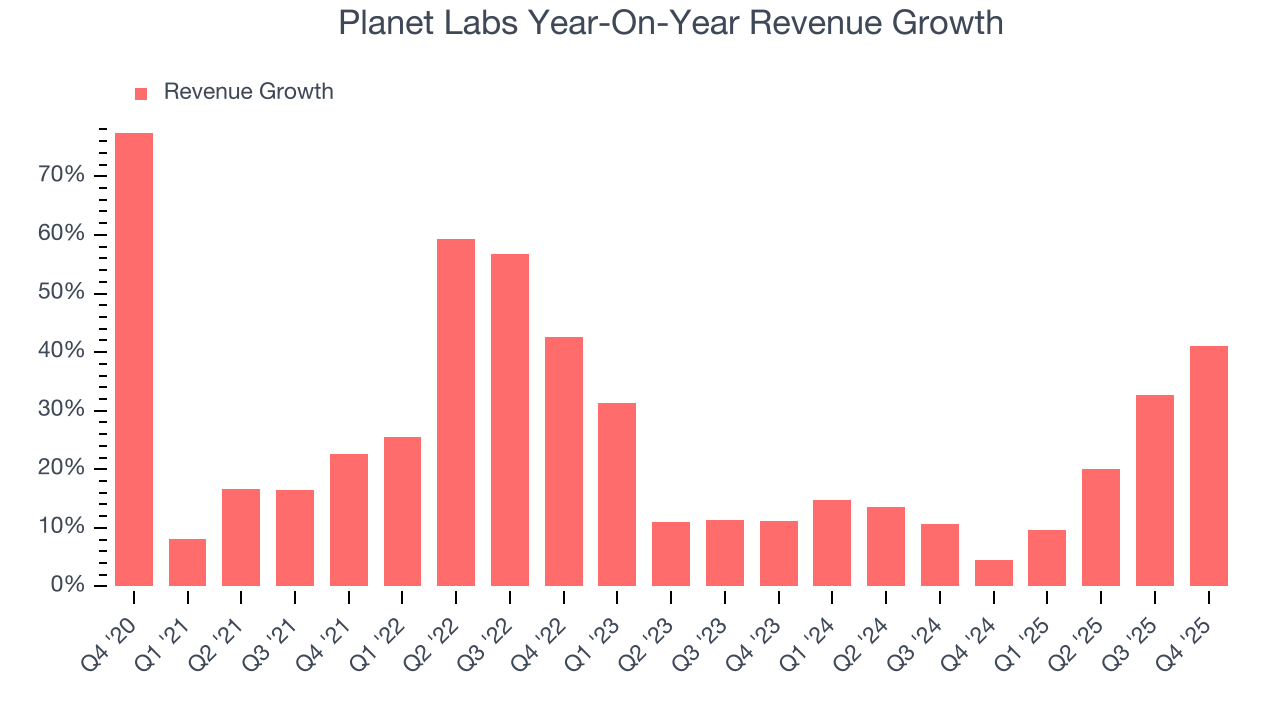

Earth imaging satellite company Planet Labs (NYSE:PL) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 41.1% year on year to $86.82 million. On top of that, next quarter’s revenue guidance ($89 million at the midpoint) was surprisingly good and 5.6% above what analysts were expecting. Its non-GAAP loss of $0 per share was significantly above analysts’ consensus estimates.

Planet Labs (PL) Q4 CY2025 Highlights:

- Revenue: $86.82 million vs analyst estimates of $78.49 million (41.1% year-on-year growth, 10.6% beat)

- Adjusted EPS: $0 vs analyst estimates of -$0.05 (significant beat)

- Adjusted EBITDA: $2.27 million (2.6% margin, 4.4% year-on-year decline)

- Revenue Guidance for Q1 CY2026 is $89 million at the midpoint, above analyst estimates of $84.27 million

- EBITDA guidance for the upcoming financial year 2027 is $5 million at the midpoint, below analyst estimates of $20.75 million

- Operating Margin: -41.5%, down from -31.5% in the same quarter last year

- Backlog: $900.4 million at quarter end, up 80.6% year on year

- Market Capitalization: $8.46 billion

Company Overview

Pioneering the concept of "agile aerospace" with hundreds of small but powerful satellites, Planet Labs (NYSE:PL) operates the world's largest fleet of Earth observation satellites, capturing daily images of our planet to provide insights on deforestation, agriculture, and climate change.

Planet Labs designs, builds, and launches compact satellites that collectively image the entire Earth every day. These satellites collect medium and high-resolution imagery that forms a continuously updating, searchable visual record of our changing planet. The company has amassed an extensive historical archive of over 2,700 images on average for every point on Earth's landmass, creating a unique dataset for analysis.

The company's business model revolves around selling access to this imagery and related analytics through cloud-based subscription and usage-based contracts. Customers can integrate Planet's data directly into their workflows through web applications or APIs, with options ranging from daily monitoring feeds to targeted high-resolution imaging of specific locations.

A forestry company might use Planet's daily imagery to detect illegal logging activities across vast territories that would be impossible to monitor from the ground. An agricultural business could track crop health throughout the growing season to optimize irrigation and fertilizer application. Government agencies might employ the data for disaster response, monitoring flood extent or wildfire spread in near real-time.

Beyond raw imagery, Planet offers derived analytics products that use machine learning to automatically detect objects, classify land use, and measure environmental variables like soil moisture or vegetation biomass. These capabilities transform satellite data into actionable intelligence for customers across sectors including agriculture, forestry, energy, finance, and government.

The company maintains a global presence with operations throughout the United States, Canada, Europe, and Asia. Its satellite fleet represents a significant technological achievement in miniaturization, allowing Planet to deploy hundreds of satellites at a fraction of the cost of traditional satellite systems while maintaining rapid iteration cycles to improve capabilities.

4. Data & Business Process Services

A combination of increasing reliance on data and analytics across various industries and the desire for cost efficiency through outsourcing could mean that companies in this space gain. As functions such as payroll, HR, and credit risk assessment rely on more digitization, key players in the data & business process services industry could be increased demand. On the other hand, the sector faces headwinds from growing regulatory scrutiny on data privacy and security, with laws like GDPR and evolving U.S. regulations potentially limiting data collection and monetization strategies. Additionally, rising cyber threats pose risks to firms handling sensitive personal and financial information, creating outsized headline risk when things go wrong in this area.

Planet Labs competes with other satellite imagery providers including Maxar Technologies (NYSE:MAXR), BlackSky Technology (NYSE:BKSY), and Airbus's Intelligence business unit. The company also faces competition from drone-based imaging services and public satellite programs like NASA/USGS Landsat and the European Space Agency's Copernicus program.

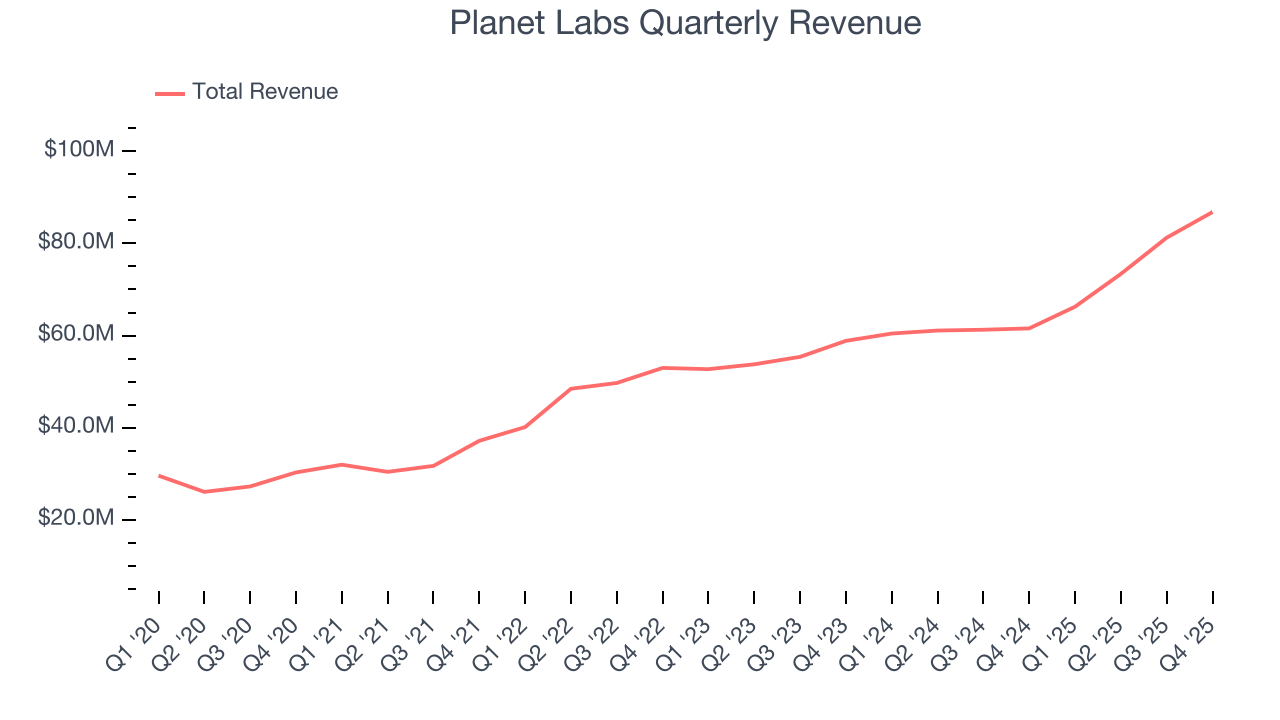

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

With $307.7 million in revenue over the past 12 months, Planet Labs is a small player in the business services space, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and numerous distribution channels. On the bright side, it can grow faster because it has more room to expand.

As you can see below, Planet Labs’s sales grew at an incredible 22.2% compounded annual growth rate over the last five years. This is a great starting point for our analysis because it shows Planet Labs’s demand was higher than many business services companies.

We at StockStory place the most emphasis on long-term growth, but within business services, a half-decade historical view may miss recent innovations or disruptive industry trends. Planet Labs’s annualized revenue growth of 18.1% over the last two years is below its five-year trend, but we still think the results suggest healthy demand.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Planet Labs’s backlog reached $900.4 million in the latest quarter and averaged 157% year-on-year growth over the last two years. Because this number is better than its revenue growth, we can see the company accumulated more orders than it could fulfill and deferred revenue to the future. This could imply elevated demand for Planet Labs’s products and services but raises concerns about capacity constraints.

This quarter, Planet Labs reported magnificent year-on-year revenue growth of 41.1%, and its $86.82 million of revenue beat Wall Street’s estimates by 10.6%. Company management is currently guiding for a 34.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 23.6% over the next 12 months, an improvement versus the last two years. This projection is eye-popping and indicates its newer products and services will catalyze better top-line performance.

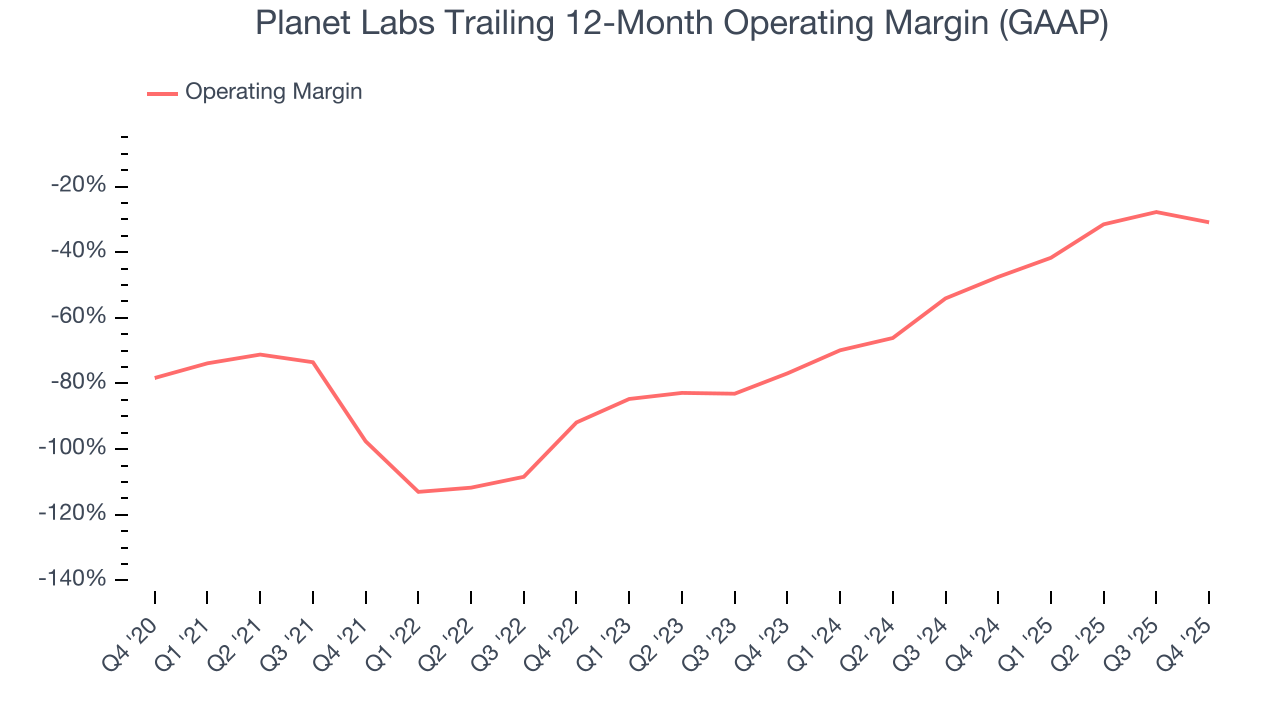

6. Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Planet Labs’s high expenses have contributed to an average operating margin of negative 62.5% over the last five years. Unprofitable business services companies require extra attention because they could get caught swimming naked when the tide goes out.

On the plus side, Planet Labs’s operating margin rose by 66.7 percentage points over the last five years, as its sales growth gave it operating leverage. Still, it will take much more for the company to reach long-term profitability.

In Q4, Planet Labs generated a negative 41.5% operating margin.

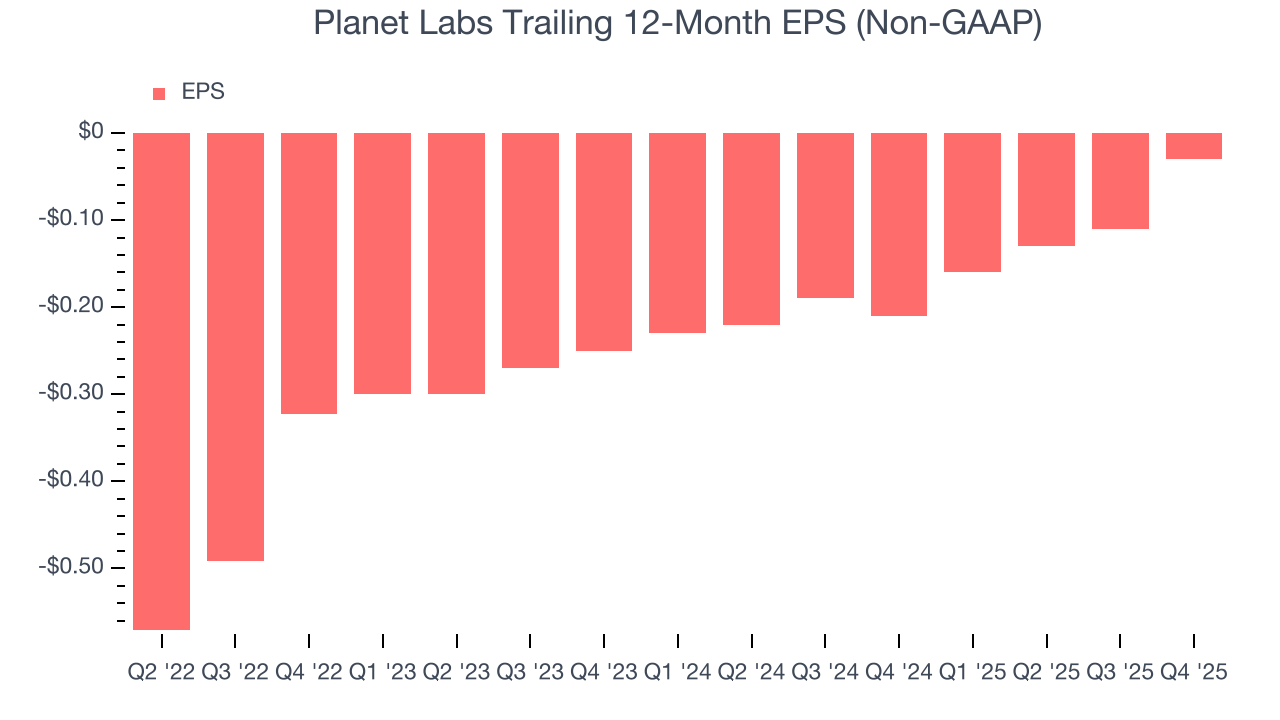

7. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Planet Labs’s full-year earnings are still negative, it reduced its losses and improved its EPS by 100% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Planet Labs, its two-year annual EPS growth of 65.4% was lower than its four-year trend. We still think its growth was good and hope it can accelerate in the future.

In Q4, Planet Labs reported adjusted EPS of $0, up from negative $0.08 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Planet Labs to perform poorly. Analysts forecast its full-year EPS of negative $0.03 will tumble to negative $0.06.

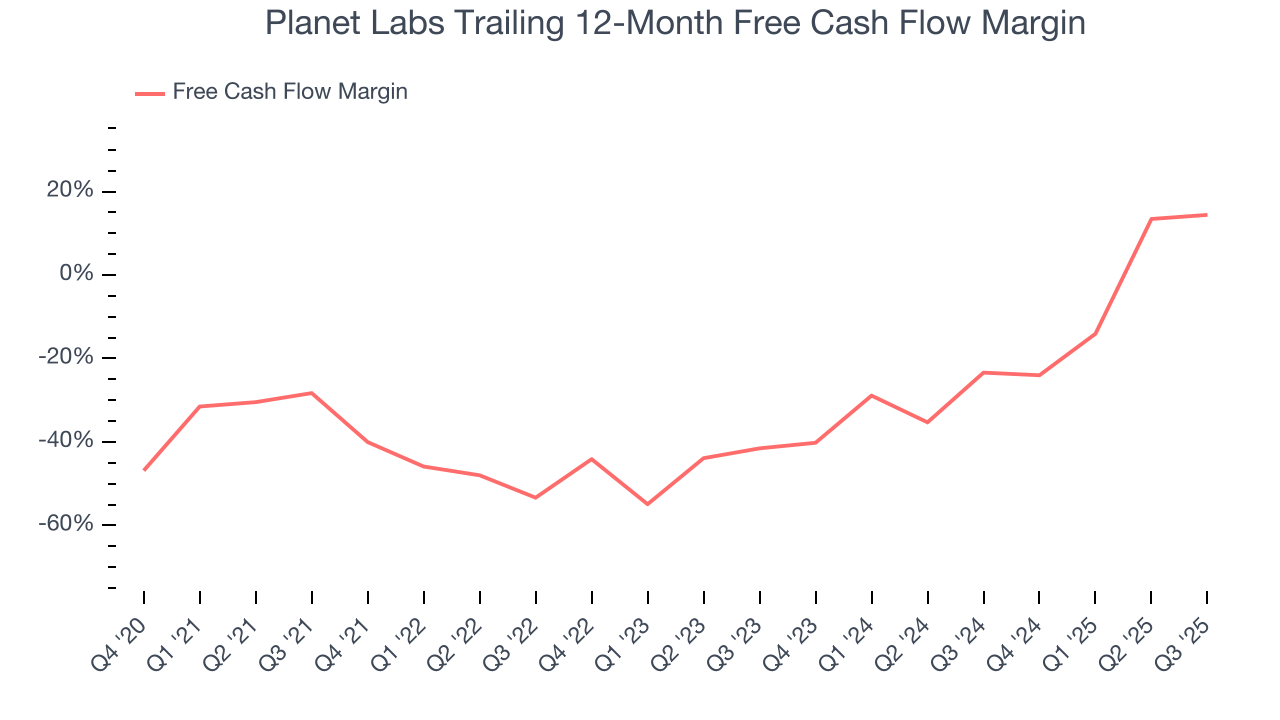

8. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Planet Labs’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 22.4%, meaning it lit $22.38 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Planet Labs’s margin expanded by 55.3 percentage points during that time. In light of its glaring cash burn, however, this improvement is a bucket of hot water in a cold ocean.

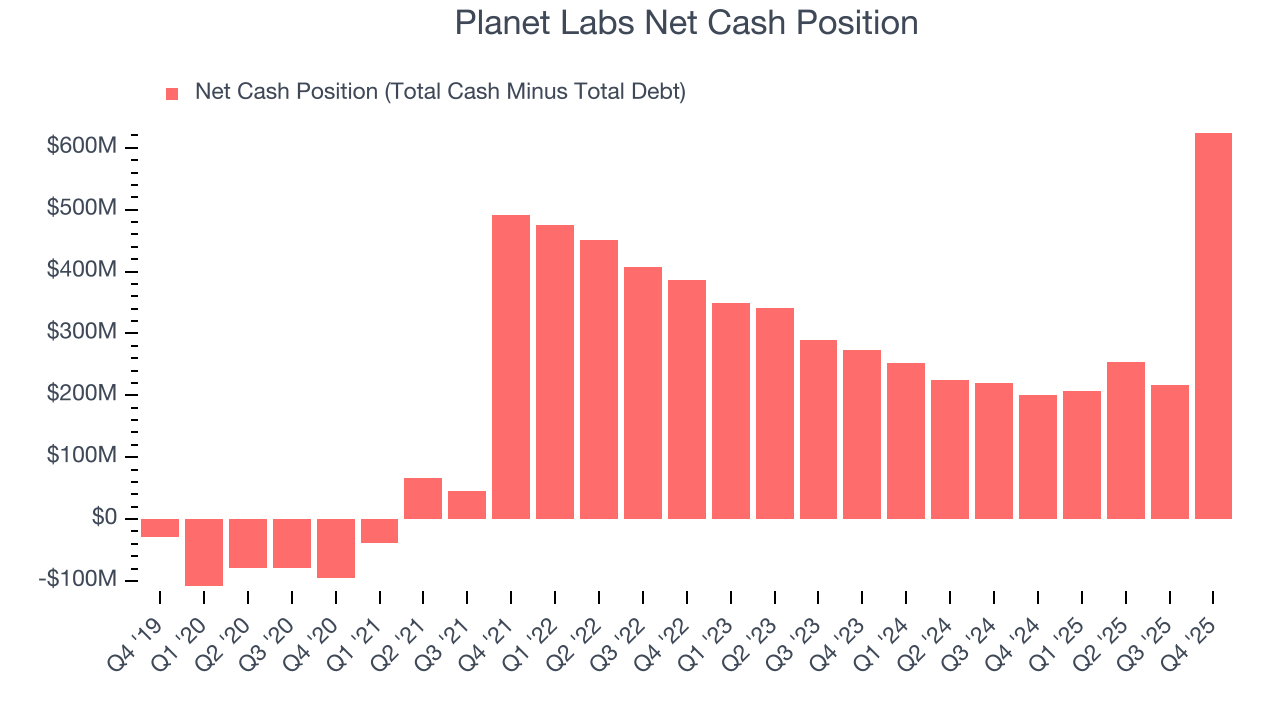

9. Balance Sheet Assessment

Businesses that maintain a cash surplus face reduced bankruptcy risk.

Planet Labs is a well-capitalized company with $640.1 million of cash and $15.6 million of debt on its balance sheet. This $624.5 million net cash position is 6.8% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

10. Key Takeaways from Planet Labs’s Q4 Results

It was good to see Planet Labs beat analysts’ EPS expectations this quarter. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this quarter featured some important positives. The stock traded up 6.3% to $28.72 immediately after reporting.

11. Is Now The Time To Buy Planet Labs?

Updated: March 30, 2026 at 11:49 PM EDT

When considering an investment in Planet Labs, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Planet Labs is a cream-of-the-crop business services company. For starters, its revenue growth was exceptional over the last five years and is expected to accelerate over the next 12 months. And while its projected EPS for the next year is lacking, its backlog growth has been marvelous. On top of that, Planet Labs’s rising cash profitability gives it more optionality.

Planet Labs’s EV-to-EBITDA ratio based on the next 12 months is 1,222.6x. This valuation may appear high at first glance, but the multiple is deserved because Planet Labs’s fundamentals clearly illustrate it’s an elite business. We think the stock is attractive here.

Wall Street analysts have a consensus one-year price target of $34.44 on the company (compared to the current share price of $27.40), implying they see 25.7% upside in buying Planet Labs in the short term.