Revvity (RVTY)

Revvity keeps us up at night. Its low returns on capital and plummeting sales suggest it struggles to generate demand and profits, a red flag.― StockStory Analyst Team

1. News

2. Summary

Why We Think Revvity Will Underperform

Formerly known as PerkinElmer until its rebranding in 2023, Revvity (NYSE:RVTY) provides health science technologies and services that support the complete workflow from discovery to development and diagnosis to cure.

- Earnings per share have dipped by 3.4% annually over the past five years, which is concerning because stock prices follow EPS over the long term

- Sales tumbled by 2.7% annually over the last five years, showing market trends are working against its favor during this cycle

- Core business is underperforming as its organic revenue has disappointed over the past two years, suggesting it might need acquisitions to stimulate growth

Revvity is in the penalty box. There are better opportunities in the market.

Why There Are Better Opportunities Than Revvity

At $108.79 per share, Revvity trades at 20.5x forward P/E. This multiple rich for the business quality. Not a great combination.

We’d rather pay up for companies with elite fundamentals than get a decent price on a poor one. High-quality businesses often have more durable earnings power, helping us sleep well at night.

3. Revvity (RVTY) Research Report: Q4 CY2025 Update

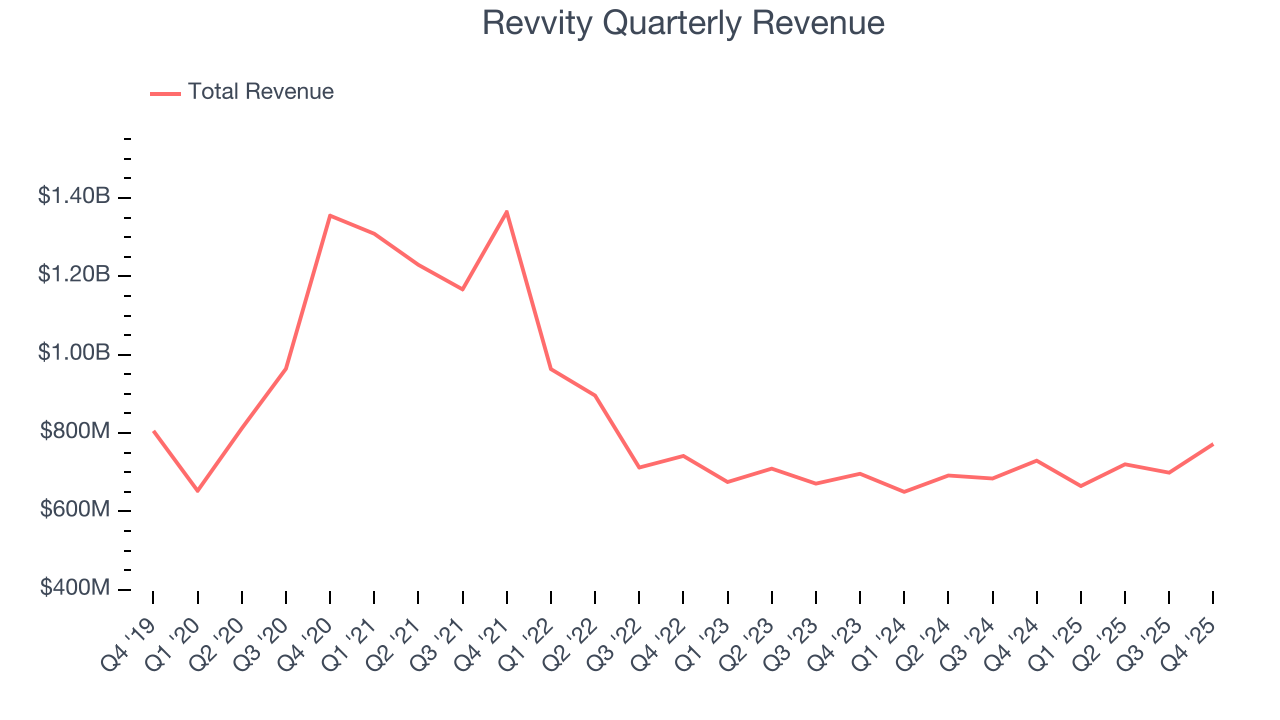

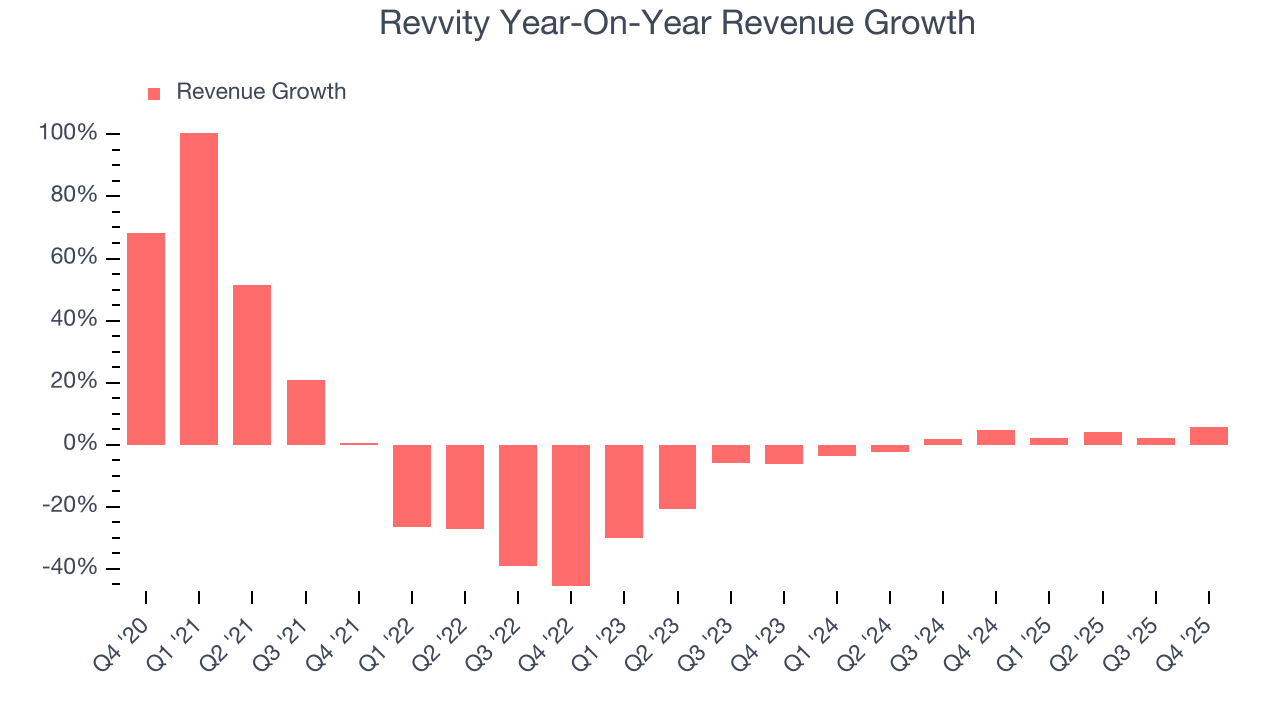

Life sciences company Revvity (NYSE:RVTY) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 5.8% year on year to $772.1 million. The company’s full-year revenue guidance of $2.98 billion at the midpoint came in 1.3% above analysts’ estimates. Its non-GAAP profit of $1.70 per share was 7.8% above analysts’ consensus estimates.

Revvity (RVTY) Q4 CY2025 Highlights:

- Revenue: $772.1 million vs analyst estimates of $763.5 million (5.8% year-on-year growth, 1.1% beat)

- Adjusted EPS: $1.70 vs analyst estimates of $1.58 (7.8% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $5.40 at the midpoint, beating analyst estimates by 1.5%

- Operating Margin: 14.5%, down from 16.3% in the same quarter last year

- Free Cash Flow Margin: 21%, similar to the same quarter last year

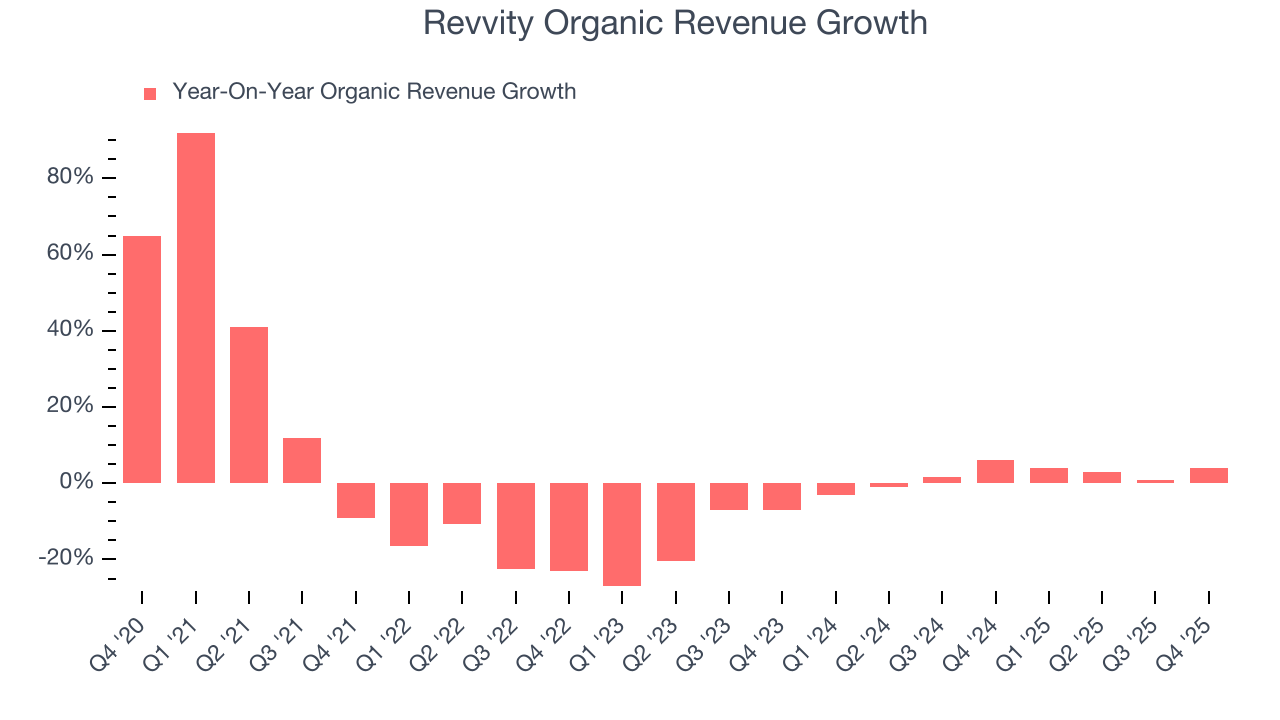

- Organic Revenue rose 4% year on year (beat)

- Market Capitalization: $12.34 billion

Company Overview

Formerly known as PerkinElmer until its rebranding in 2023, Revvity (NYSE:RVTY) provides health science technologies and services that support the complete workflow from discovery to development and diagnosis to cure.

Revvity operates through two main segments: Life Sciences and Diagnostics. The Life Sciences segment offers a comprehensive portfolio of technologies that help researchers better understand diseases and develop treatments. These include radiometric detection solutions, high-content screening systems, reagents for microscopy and imaging, multimode plate readers, and a wide range of assay technologies. These tools enable scientists to visualize cellular behaviors, analyze proteins, and accelerate drug discovery research.

The Diagnostics segment focuses on reproductive health, immunodiagnostics, emerging market diagnostics, and applied genomics. Revvity provides screening products for genetic disorders from pregnancy through early childhood, as well as infectious disease testing. Its prenatal screening platforms help detect conditions like Down syndrome, while its newborn screening technologies identify metabolic disorders from just a drop of blood. The company also offers automated systems for processing immunoassays and molecular diagnostic tests.

A pharmaceutical researcher might use Revvity's Opera Phenix Plus system to screen potential drug compounds against complex cellular models, while a hospital laboratory might employ its DELFIA Xpress platform to conduct prenatal screening tests. In both cases, Revvity's technologies help healthcare professionals make critical decisions that impact patient outcomes.

Revvity markets its products and services in more than 160 countries through specialized sales forces and distributors. Its customers include pharmaceutical and biotechnology companies, laboratories, academic and research institutions, public health authorities, private healthcare organizations, doctors, and government agencies. Many customers use Revvity's products to develop, test, and manufacture their own products.

The company's strategy focuses on developing innovative products in high-growth markets, strengthening its position through both internal research and strategic acquisitions, and driving operational excellence. In 2023, Revvity completed the sale of its Applied, Food and Enterprise Services businesses to focus on its core health science operations.

4. Research Tools & Consumables

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

Revvity competes with other life sciences and diagnostics companies including Thermo Fisher Scientific (NYSE: TMO), Danaher Corporation (NYSE: DHR), Agilent Technologies (NYSE: A), Bio-Rad Laboratories (NYSE: BIO), and Illumina (NASDAQ: ILMN).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $2.86 billion in revenue over the past 12 months, Revvity has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Revvity’s demand was weak over the last five years as its sales fell at a 5.5% annual rate. This was below our standards and is a sign of poor business quality.

Long-term growth is the most important, but within healthcare, a half-decade historical view may miss new innovations or demand cycles. Revvity’s annualized revenue growth of 1.9% over the last two years is above its five-year trend, but we were still disappointed by the results.

We can dig further into the company’s sales dynamics by analyzing its organic revenue, which strips out one-time events like acquisitions and currency fluctuations that don’t accurately reflect its fundamentals. Over the last two years, Revvity’s organic revenue averaged 2% year-on-year growth. Because this number aligns with its two-year revenue growth, we can see the company’s core operations (not acquisitions and divestitures) drove most of its results.

This quarter, Revvity reported year-on-year revenue growth of 5.8%, and its $772.1 million of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 2.8% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not accelerate its top-line performance yet.

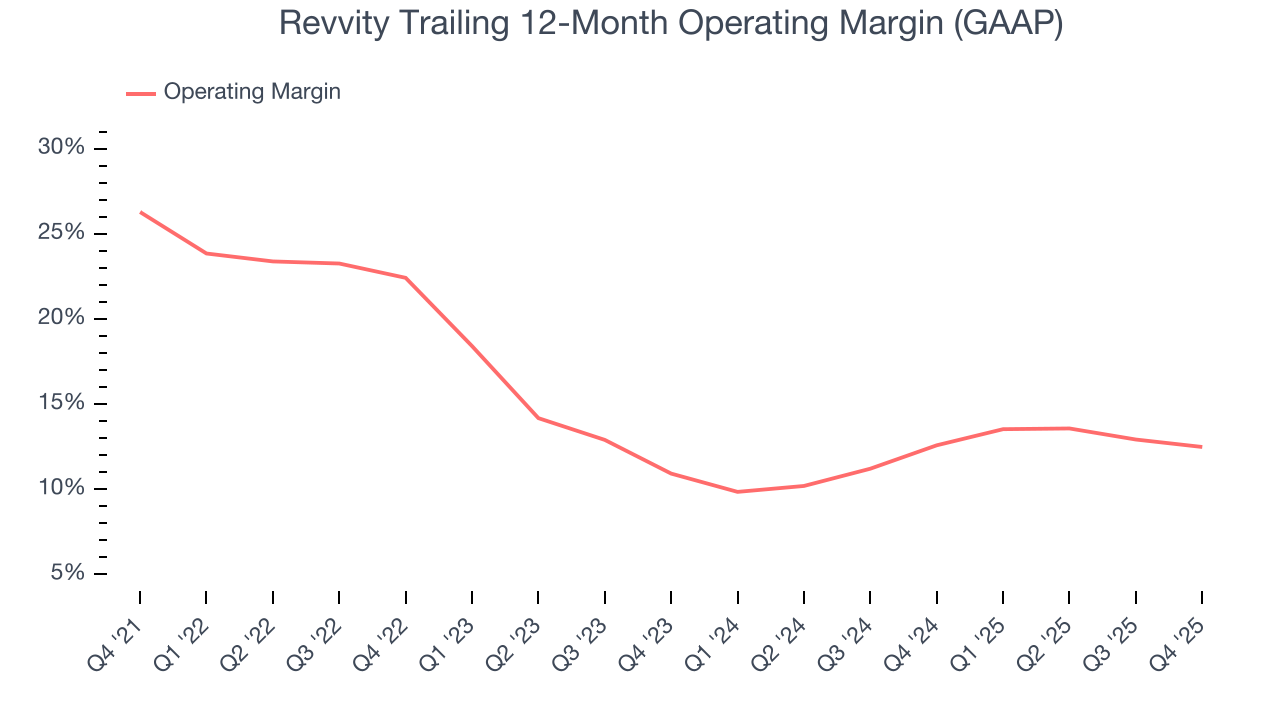

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Revvity has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 18.4%.

Analyzing the trend in its profitability, Revvity’s operating margin decreased by 13.8 percentage points over the last five years, but it rose by 1.6 percentage points on a two-year basis. Still, shareholders will want to see Revvity become more profitable in the future.

In Q4, Revvity generated an operating margin profit margin of 14.5%, down 1.8 percentage points year on year. This reduction is quite minuscule and indicates the company’s overall cost structure has been relatively stable.

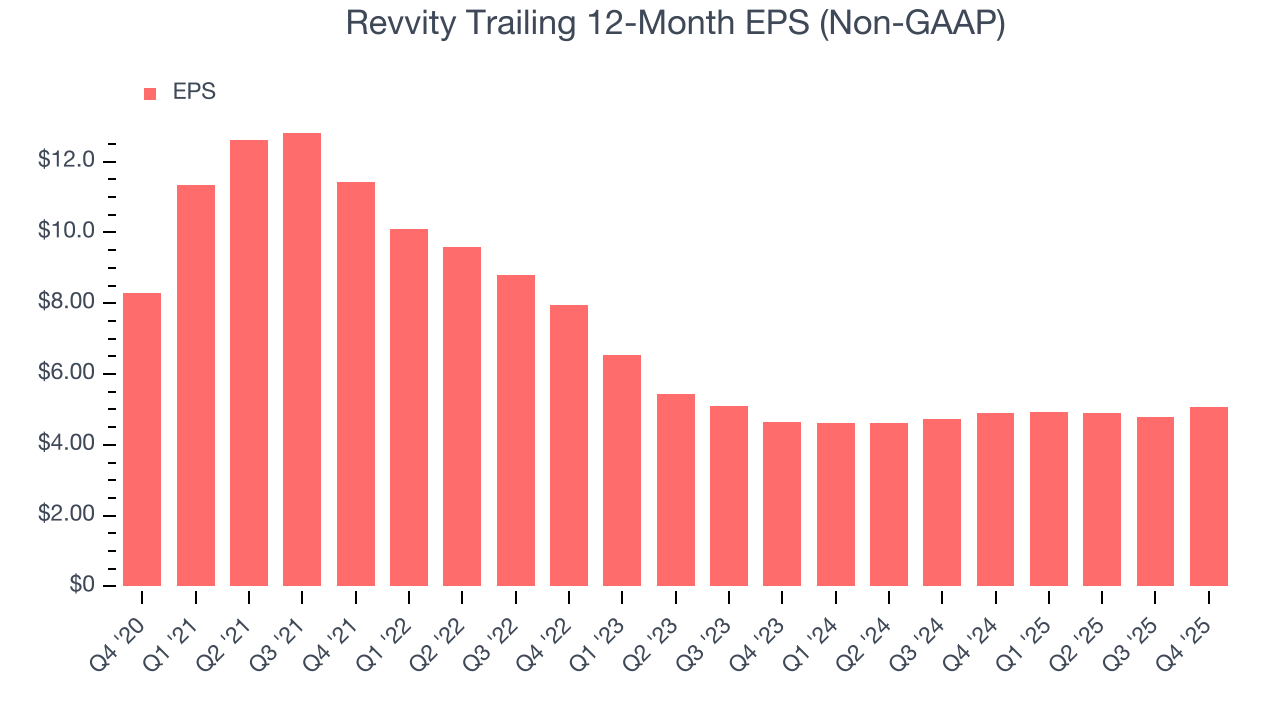

8. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Sadly for Revvity, its EPS declined by 9.4% annually over the last five years, more than its revenue. This tells us the company struggled because its fixed cost base made it difficult to adjust to shrinking demand.

Diving into the nuances of Revvity’s earnings can give us a better understanding of its performance. As we mentioned earlier, Revvity’s operating margin declined by 13.8 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Revvity reported adjusted EPS of $1.70, up from $1.42 in the same quarter last year. This print beat analysts’ estimates by 7.8%. Over the next 12 months, Wall Street expects Revvity’s full-year EPS of $5.07 to grow 4.8%.

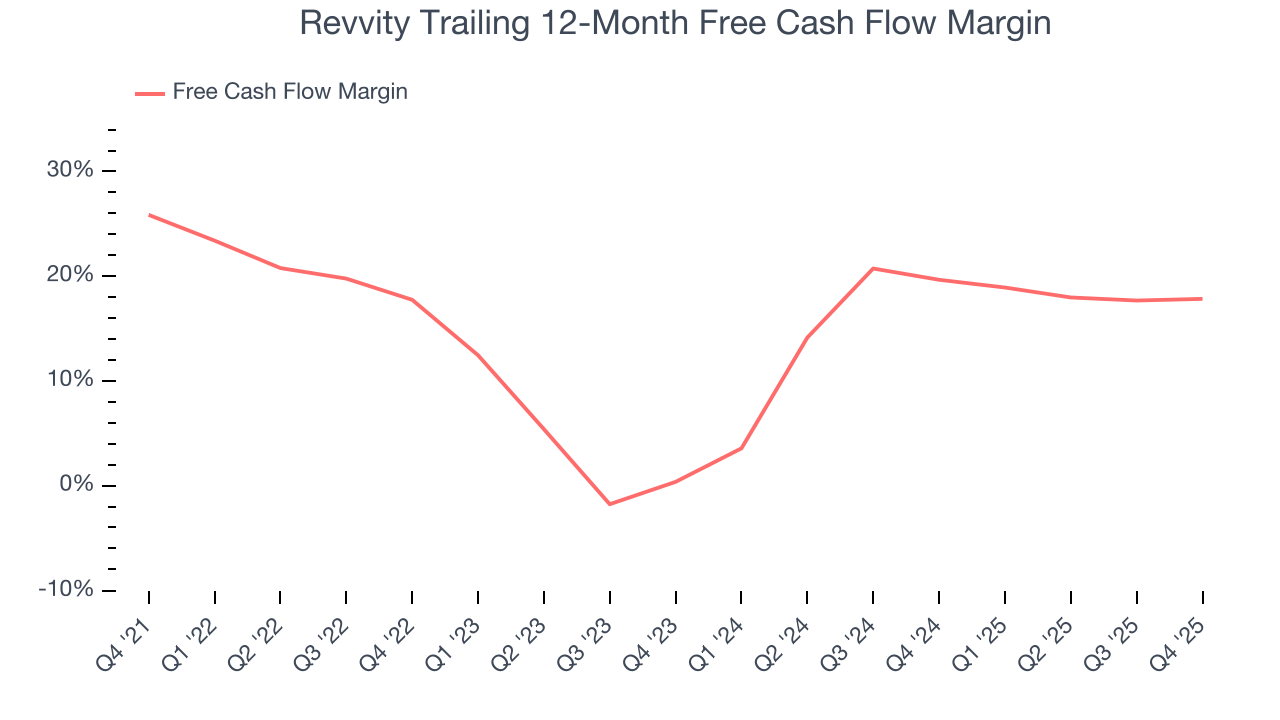

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Revvity has shown robust cash profitability, giving it an edge over its competitors and the ability to reinvest or return capital to investors. The company’s free cash flow margin averaged 17.7% over the last five years, quite impressive for a healthcare business.

Taking a step back, we can see that Revvity’s margin dropped by 8 percentage points during that time. Continued declines could signal it is in the middle of an investment cycle.

Revvity’s free cash flow clocked in at $161.8 million in Q4, equivalent to a 21% margin. This cash profitability was in line with the comparable period last year and above its five-year average.

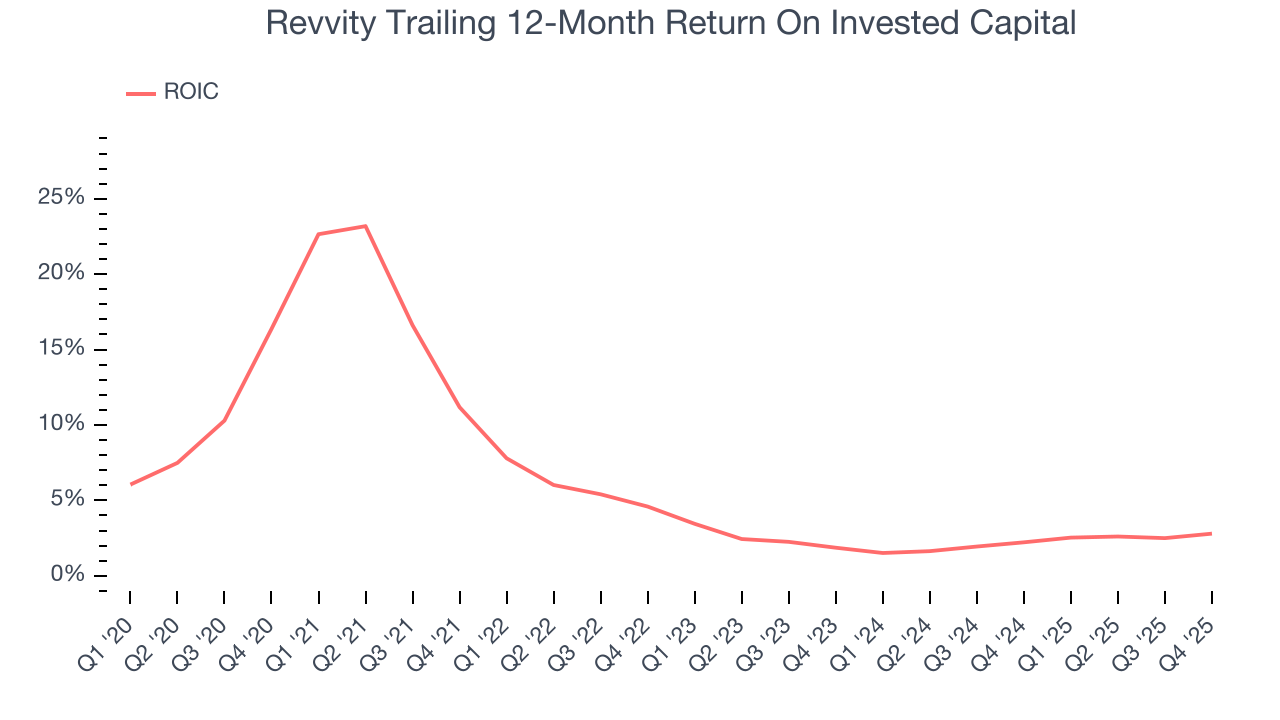

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Revvity historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 4.5%, lower than the typical cost of capital (how much it costs to raise money) for healthcare companies.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Revvity’s ROIC has unfortunately decreased. Paired with its already low returns, these declines suggest its profitable growth opportunities are few and far between.

11. Balance Sheet Assessment

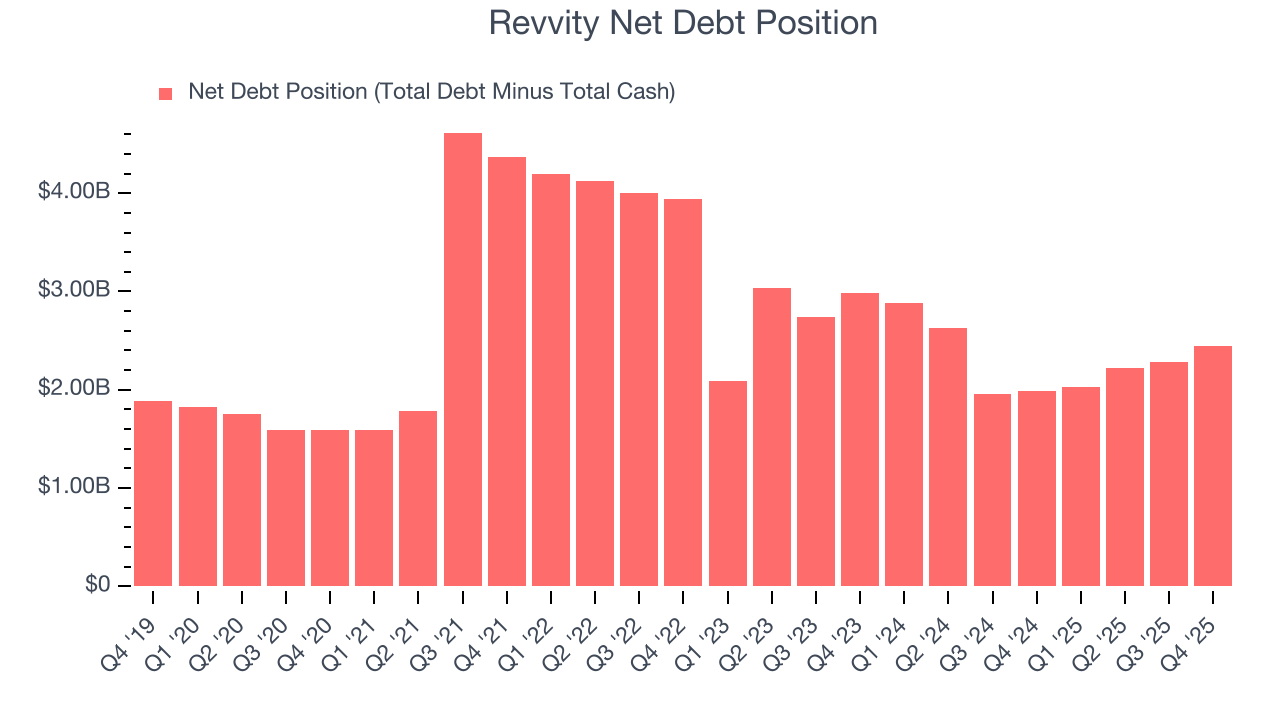

Revvity reported $919.9 million of cash and $3.37 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.06 billion of EBITDA over the last 12 months, we view Revvity’s 2.3× net-debt-to-EBITDA ratio as safe. We also see its $25.56 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Revvity’s Q4 Results

It was good to see Revvity provide full-year revenue guidance that slightly beat analysts’ expectations. We were also happy its organic revenue narrowly outperformed Wall Street’s estimates, leading to an EPS beat. Overall, we think this was a decent quarter with some key metrics above expectations. The stock remained flat at $109.50 immediately after reporting.

13. Is Now The Time To Buy Revvity?

Updated: February 2, 2026 at 6:29 AM EST

Are you wondering whether to buy Revvity or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Revvity doesn’t pass our quality test. To kick things off, its revenue has declined over the last five years. And while its strong free cash flow generation allows it to invest in growth initiatives while maintaining an ample cushion, the downside is its declining EPS over the last five years makes it a less attractive asset to the public markets. On top of that, its declining operating margin shows the business has become less efficient.

Revvity’s P/E ratio based on the next 12 months is 20.5x. This multiple tells us a lot of good news is priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $116.19 on the company (compared to the current share price of $109.50).