Sherwin-Williams (SHW)

We aren’t fans of Sherwin-Williams. Its growth has been lacking and its free cash flow margin has caved, suggesting it’s struggling to adapt.― StockStory Analyst Team

1. News

2. Summary

Why We Think Sherwin-Williams Will Underperform

Widely known for its success in the paint industry, Sherwin-Williams (NYSE:SHW) is a manufacturer of paints, coatings, and related products.

- Absence of organic revenue growth over the past two years suggests it may have to lean into acquisitions to drive its expansion

- Anticipated sales growth of 5% for the next year implies demand will be shaky

- The good news is that its offerings are difficult to replicate at scale and lead to a best-in-class gross margin of 45.8%

Sherwin-Williams fails to meet our quality criteria. We’re on the lookout for more interesting opportunities.

Why There Are Better Opportunities Than Sherwin-Williams

At $344.53 per share, Sherwin-Williams trades at 28.8x forward P/E. Not only does Sherwin-Williams trade at a premium to companies in the industrials space, but this multiple is also high for its top-line growth.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Sherwin-Williams (SHW) Research Report: Q4 CY2025 Update

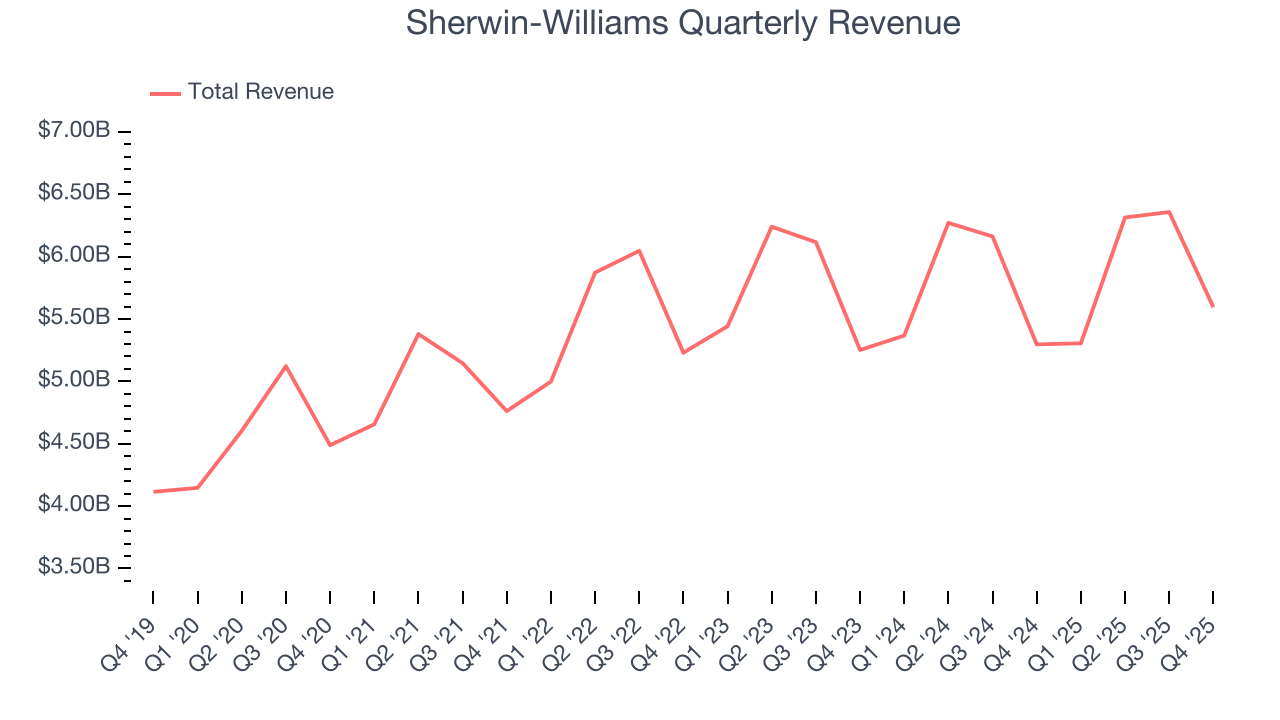

Paint and coating manufacturer Sherwin-Williams (NYSE:SHW) announced better-than-expected revenue in Q4 CY2025, with sales up 5.6% year on year to $5.60 billion. Its non-GAAP profit of $2.23 per share was 3.1% above analysts’ consensus estimates.

Sherwin-Williams (SHW) Q4 CY2025 Highlights:

- Revenue: $5.60 billion vs analyst estimates of $5.55 billion (5.6% year-on-year growth, 0.8% beat)

- Adjusted EPS: $2.23 vs analyst estimates of $2.16 (3.1% beat)

- Adjusted EBITDA: $993.1 million vs analyst estimates of $927.3 million (17.7% margin, 7.1% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $11.70 at the midpoint, missing analyst estimates by 5.5%

- Operating Margin: 13.9%, in line with the same quarter last year

- Market Capitalization: $86.16 billion

Company Overview

Widely known for its success in the paint industry, Sherwin-Williams (NYSE:SHW) is a manufacturer of paints, coatings, and related products.

Sherwin-Williams began its journey as a small partnership selling raw materials to paint manufacturers. Over the years, it transformed into a globally recognized manufacturer of coatings and related products. The company expanded its market presence and product lines through numerous acquisitions, one of the most significant being the acquisition of Valspar in March 2016, for $11.3 billion. The merger integrated Valspar’s extensive offerings into Sherwin-Williams's portfolio, enhancing its presence in architectural paint and industrial coatings.

Today, Sherwin-Williams offers a comprehensive range of paint, coatings, and related products tailored to a variety of markets, from residential DIY enthusiasts to industrial professionals across the globe. The company operates specialty paint stores under its Paint Stores Group in North America and the Caribbean, catering primarily to architectural and industrial paint contractors. These stores distribute Sherwin-Williams and other controlled brands, including architectural paints, coatings, protective and marine products, and OEM product finishes. The company also sells advanced industrial coatings used in a variety of applications from wood finishing to automotive refinish and marine coatings worldwide.

Sherwin-Williams generates revenue through a multifaceted approach that includes sales from its own retail stores, direct sales to large-scale projects, and distribution through third-party retailers and distributors. Its stores serve as a primary sales channel, offering a wide range of products directly to consumers. Beyond retail, the company extends its reach into commercial and industrial markets by partnering with third-party vendors, which helps distribute specialized products for professional use. Additionally, Sherwin-Williams secures steady revenue streams through contracts and partnerships for large-scale industrial sales and government projects, further broadening its market presence.

The company typically experiences the majority of its sales during the second and third quarters, aligning with the warmer months when painting and construction activities are most prevalent. To prepare for this peak season, the company builds its inventories in the first quarter to meet the heightened demand.

4. Building Materials

Traditionally, building materials companies have built competitive advantages with economies of scale, brand recognition, and strong relationships with builders and contractors. More recently, advances to address labor availability and job site productivity have spurred innovation. Additionally, companies in the space that can produce more energy-efficient materials have opportunities to take share. However, these companies are at the whim of construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of building materials companies.

Competitors offering similar products include PPG Industries (NYSE:PPG), RPM International (NYSE:RPM), and Axalta Coating Systems (NYSE:AXTA).

5. Revenue Growth

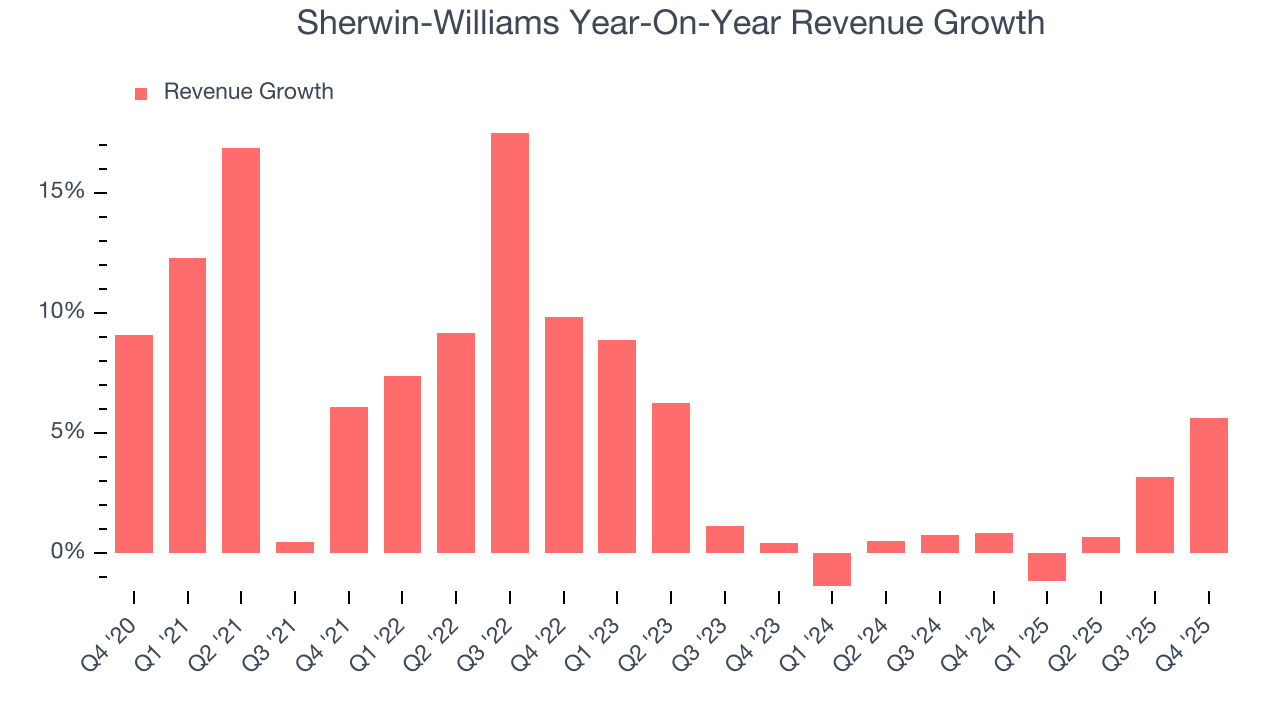

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Regrettably, Sherwin-Williams’s sales grew at a tepid 5.1% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Sherwin-Williams’s recent performance shows its demand has slowed as its annualized revenue growth of 1.1% over the last two years was below its five-year trend.

This quarter, Sherwin-Williams reported year-on-year revenue growth of 5.6%, and its $5.60 billion of revenue exceeded Wall Street’s estimates by 0.8%.

Looking ahead, sell-side analysts expect revenue to grow 4.5% over the next 12 months. Although this projection indicates its newer products and services will spur better top-line performance, it is still below average for the sector.

6. Gross Margin & Pricing Power

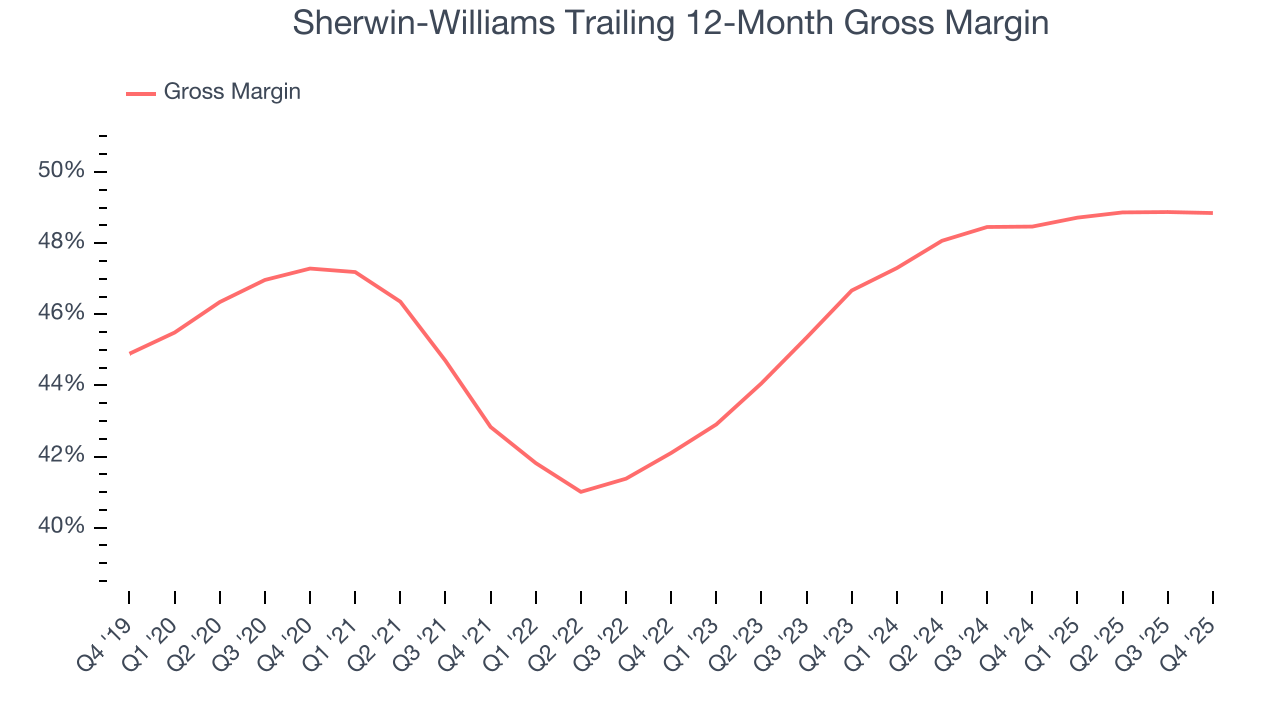

Sherwin-Williams has best-in-class unit economics for an industrials company, enabling it to invest in areas such as research and development. Its margin also signals it sells differentiated products, not commodities. As you can see below, it averaged an elite 45.9% gross margin over the last five years. That means Sherwin-Williams only paid its suppliers $54.09 for every $100 in revenue.

In Q4, Sherwin-Williams produced a 48.5% gross profit margin, in line with the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

7. Operating Margin

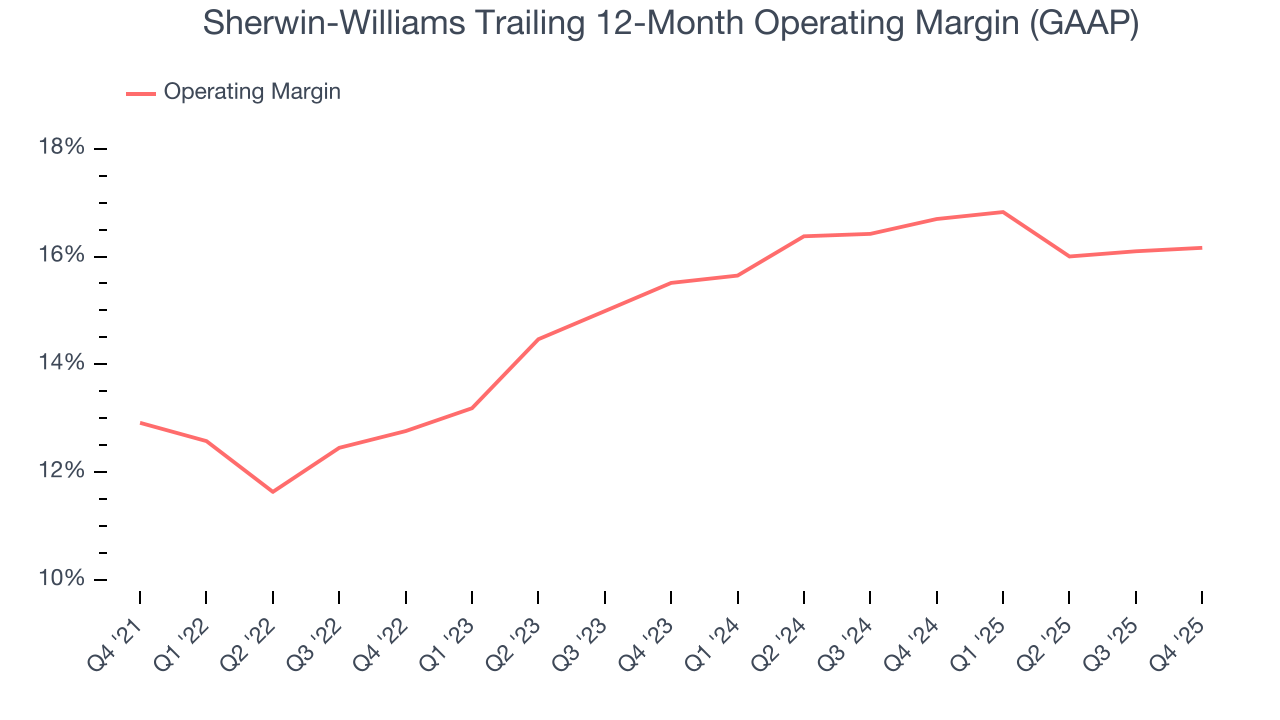

Sherwin-Williams has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 14.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Sherwin-Williams’s operating margin rose by 3.2 percentage points over the last five years, as its sales growth gave it operating leverage.

This quarter, Sherwin-Williams generated an operating margin profit margin of 13.9%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

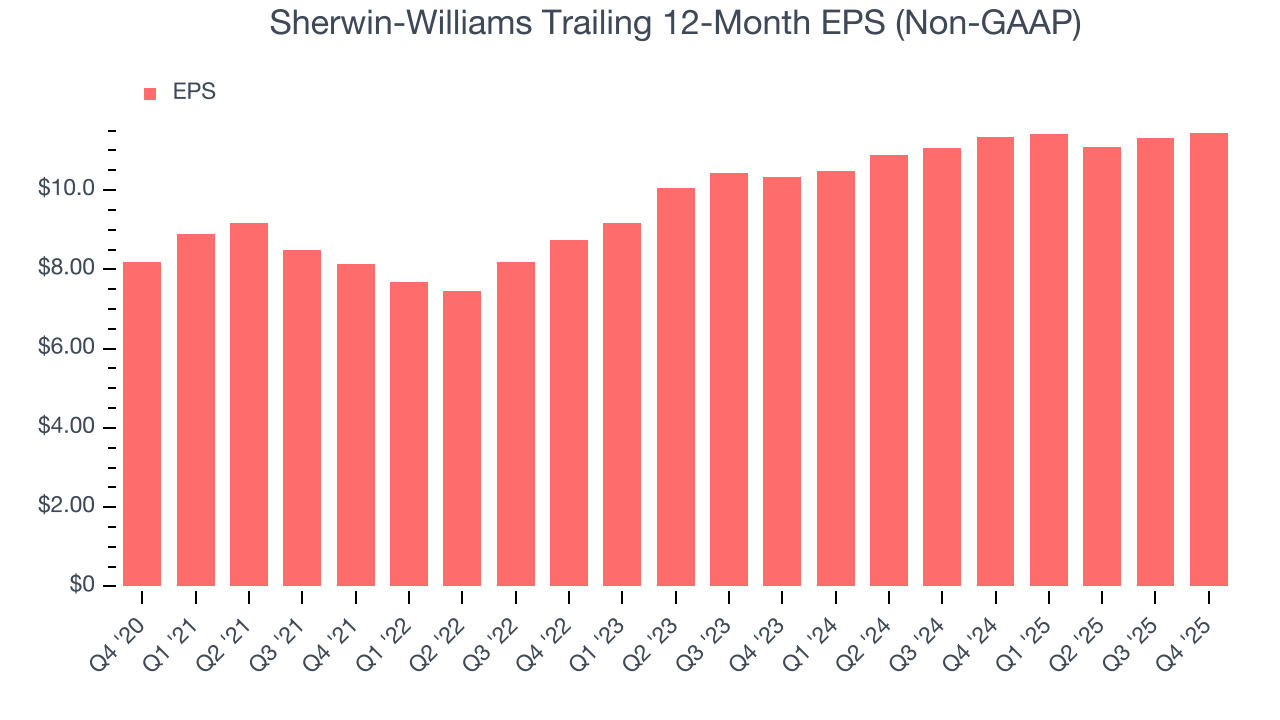

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sherwin-Williams’s unimpressive 6.9% annual EPS growth over the last five years aligns with its revenue performance. On the bright side, this tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Although it wasn’t great, Sherwin-Williams’s two-year annual EPS growth of 5.2% topped its 1.1% two-year revenue growth.

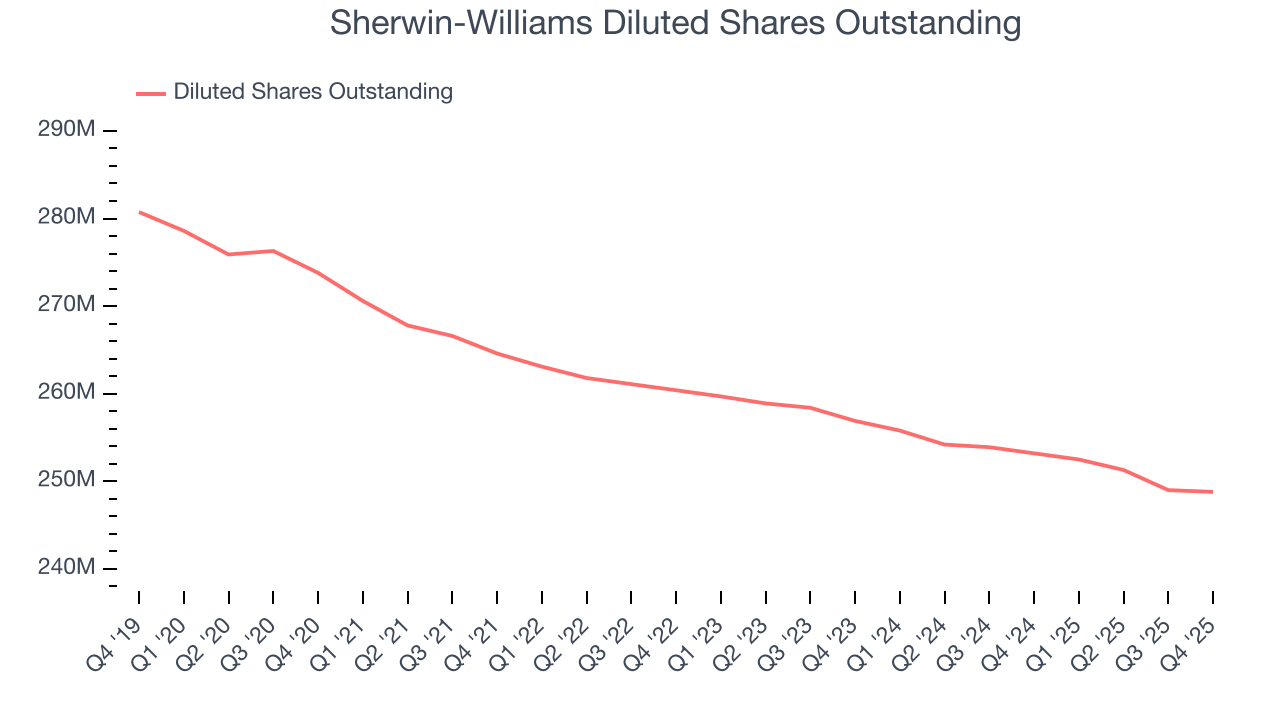

We can take a deeper look into Sherwin-Williams’s earnings to better understand the drivers of its performance. While we mentioned earlier that Sherwin-Williams’s operating margin was flat this quarter, a two-year view shows its margin has expandedwhile its share count has shrunk 3.2%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Sherwin-Williams reported adjusted EPS of $2.23, up from $2.09 in the same quarter last year. This print beat analysts’ estimates by 3.1%. Over the next 12 months, Wall Street expects Sherwin-Williams’s full-year EPS of $11.45 to grow 7%.

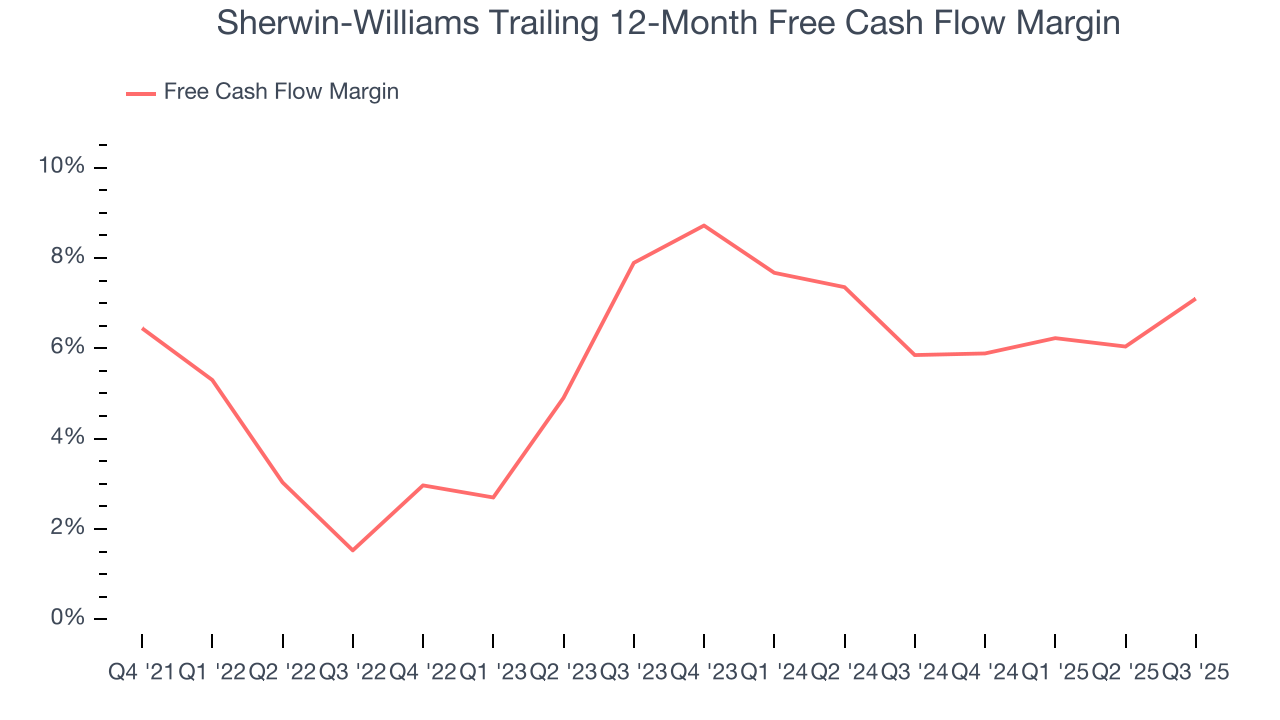

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Sherwin-Williams has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.1% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that Sherwin-Williams’s margin dropped by 2.3 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

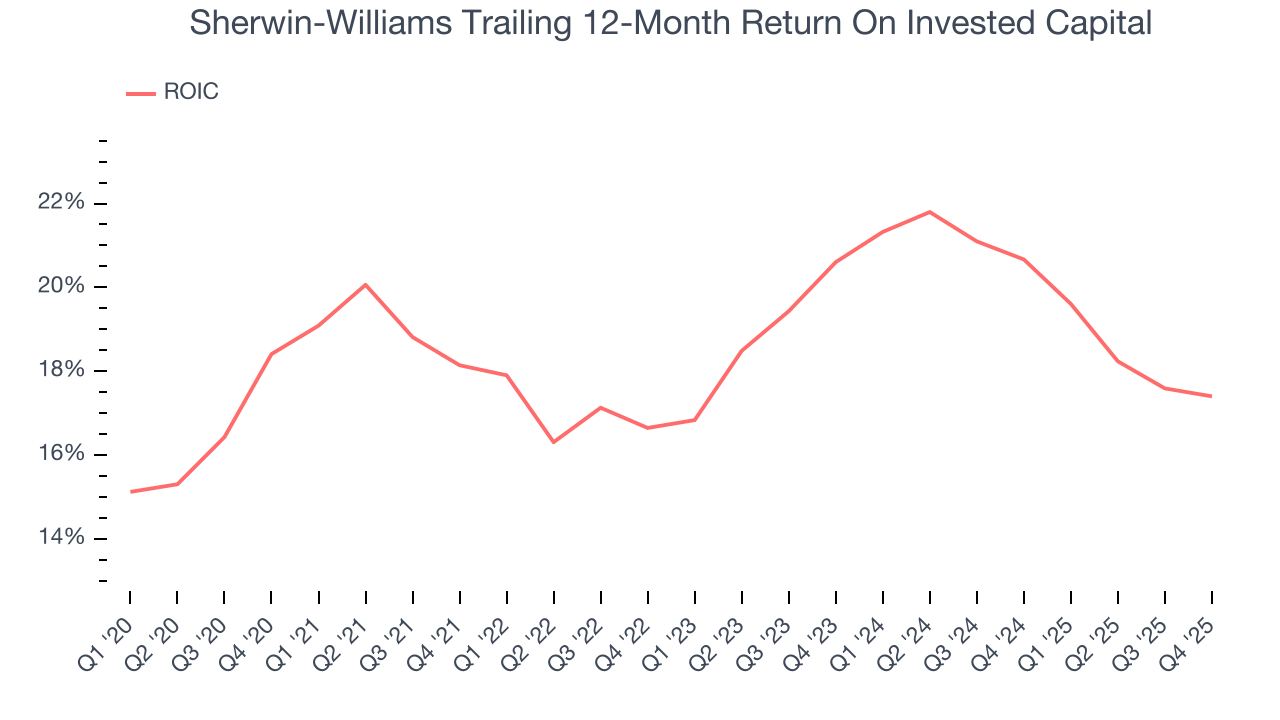

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Sherwin-Williams hasn’t been the highest-quality company lately, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 18.7%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Sherwin-Williams’s ROIC averaged 1.6 percentage point increases each year. This is a good sign, and we hope the company can keep improving.

11. Balance Sheet Assessment

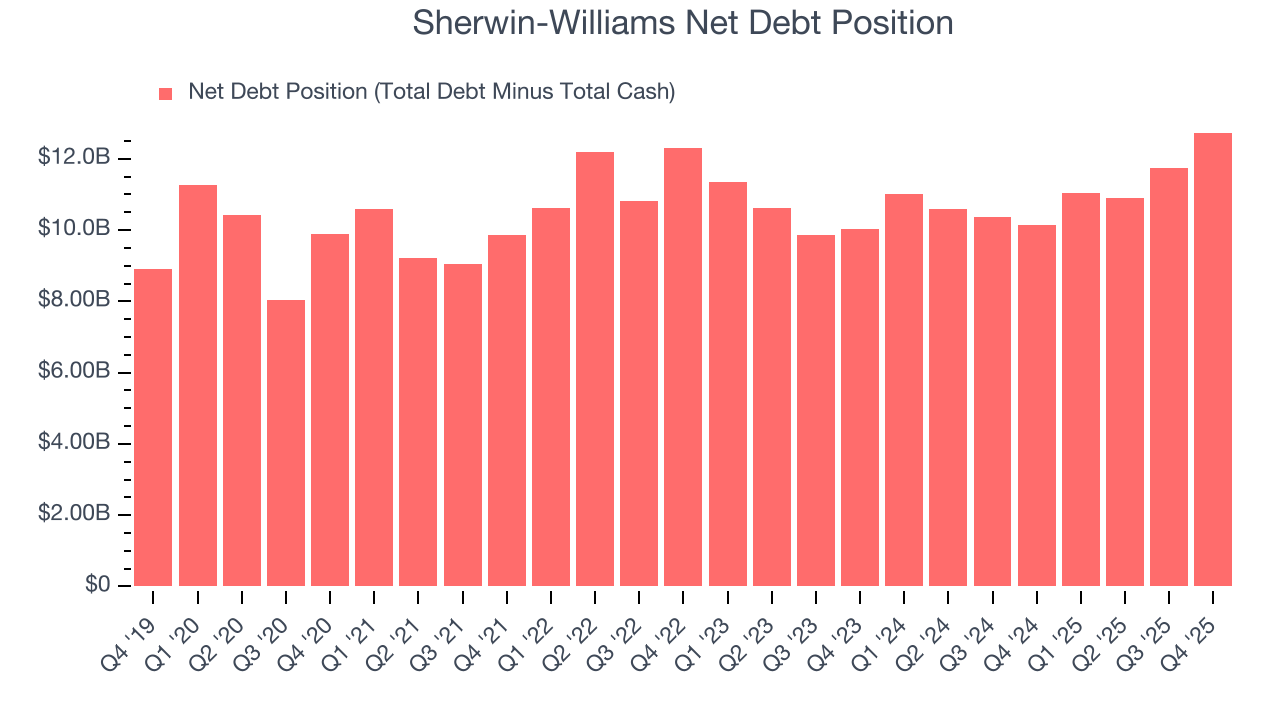

Sherwin-Williams reported $207.2 million of cash and $12.94 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $4.61 billion of EBITDA over the last 12 months, we view Sherwin-Williams’s 2.8× net-debt-to-EBITDA ratio as safe. We also see its $196.4 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Sherwin-Williams’s Q4 Results

We enjoyed seeing Sherwin-Williams beat analysts’ EBITDA expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street’s estimates. On the other hand, its full-year EPS guidance missed, and this is weighing on shares. Zooming out, we think this was a mixed quarter. Investors were likely hoping for more, and shares traded down 1.4% to $344.88 immediately after reporting.

13. Is Now The Time To Buy Sherwin-Williams?

Updated: January 29, 2026 at 8:37 AM EST

Before making an investment decision, investors should account for Sherwin-Williams’s business fundamentals and valuation in addition to what happened in the latest quarter.

Sherwin-Williams isn’t a terrible business, but it doesn’t pass our quality test. First off, its revenue growth was uninspiring over the last five years, and analysts don’t see anything changing over the next 12 months. And while its admirable gross margins indicate the mission-critical nature of its offerings, the downside is its flat organic revenue disappointed. On top of that, its cash profitability fell over the last five years.

Sherwin-Williams’s P/E ratio based on the next 12 months is 28.5x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $386.29 on the company (compared to the current share price of $344.88).