Tenet Healthcare (THC)

Tenet Healthcare piques our interest. Its returns on capital are not only elite but also rising, suggesting its competitive moat is widening.― StockStory Analyst Team

1. News

2. Summary

Why Tenet Healthcare Is Interesting

With a network spanning nine states and serving primarily urban and suburban communities, Tenet Healthcare (NYSE:THC) operates a nationwide network of hospitals, ambulatory surgery centers, and outpatient facilities providing acute care and specialty healthcare services.

- Incremental sales significantly boosted profitability as its annual earnings per share growth of 16.3% over the last five years outstripped its revenue performance

- Industry-leading 22.1% return on capital demonstrates management’s skill in finding high-return investments, and its rising returns show it’s making even more lucrative bets

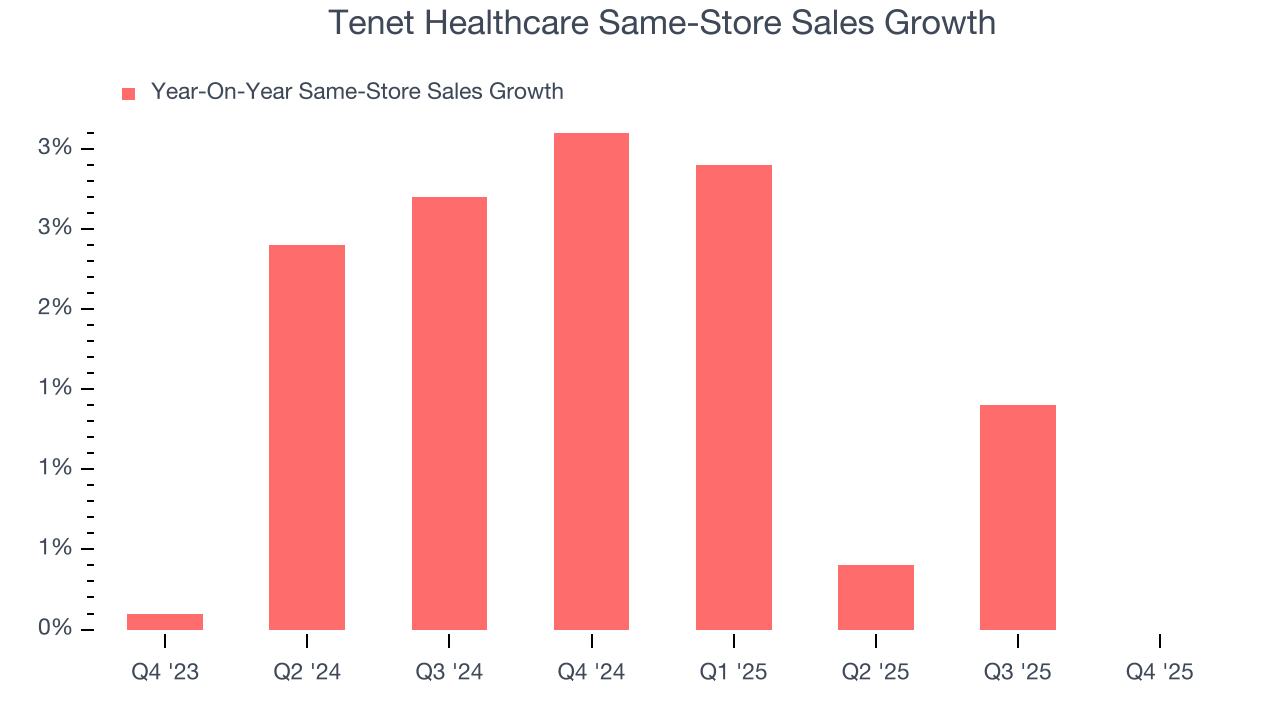

- A drawback is its disappointing comparable store sales over the past two years show customers aren’t responding well to its offerings and value proposition

Tenet Healthcare almost passes our quality test. If you’re a believer, the valuation looks fair.

Why Is Now The Time To Buy Tenet Healthcare?

Tenet Healthcare is trading at $200.01 per share, or 11.9x forward P/E. Many healthcare companies feature higher valuation multiples than Tenet Healthcare. Regardless, we think Tenet Healthcare’s current price is appropriate given the quality you get.

If you think the market is undervaluing the company, now could be a good time to build a position.

3. Tenet Healthcare (THC) Research Report: Q4 CY2025 Update

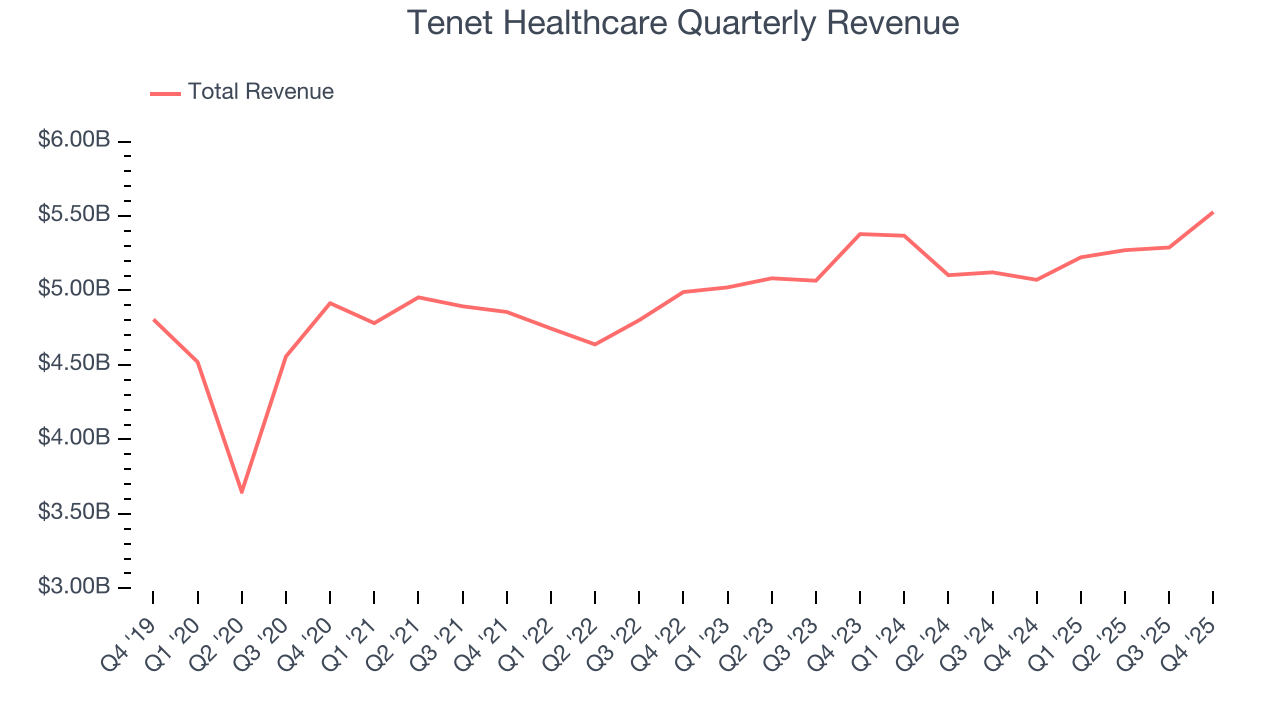

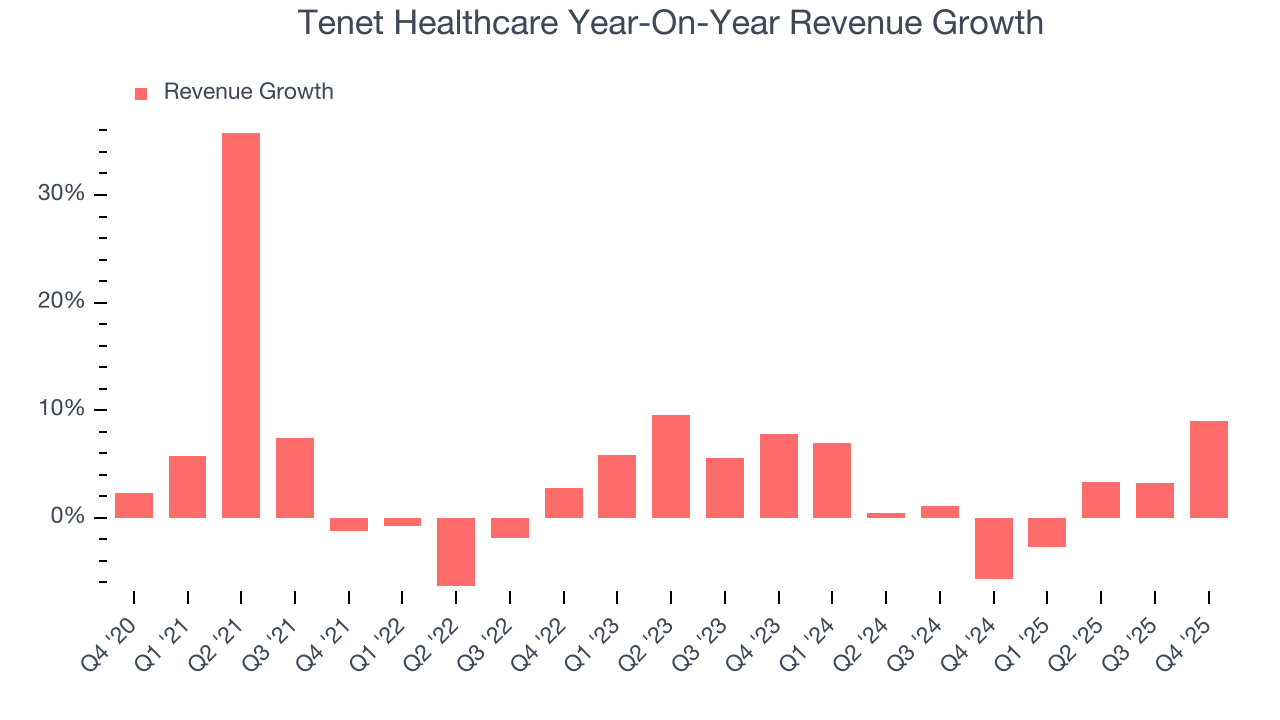

Hospital operator Tenet Healthcare (NYSE:THC) announced better-than-expected revenue in Q4 CY2025, with sales up 9% year on year to $5.53 billion. On the other hand, the company’s full-year revenue guidance of $21.9 billion at the midpoint came in 1.4% below analysts’ estimates. Its non-GAAP profit of $4.70 per share was 16% above analysts’ consensus estimates.

Tenet Healthcare (THC) Q4 CY2025 Highlights:

- Revenue: $5.53 billion vs analyst estimates of $5.47 billion (9% year-on-year growth, 1.1% beat)

- Adjusted EPS: $4.70 vs analyst estimates of $4.05 (16% beat)

- Adjusted EBITDA: $1.18 billion vs analyst estimates of $1.16 billion (21.4% margin, 2.2% beat)

- Adjusted EPS guidance for the upcoming financial year 2026 is $17.33 at the midpoint, beating analyst estimates by 5.3%

- EBITDA guidance for the upcoming financial year 2026 is $4.64 billion at the midpoint, in line with analyst expectations

- Operating Margin: 15.4%, in line with the same quarter last year

- Free Cash Flow was $367 million, up from -$661 million in the same quarter last year

- Same-Store Sales were flat year on year (3.1% in the same quarter last year)

- Market Capitalization: $16.97 billion

Company Overview

With a network spanning nine states and serving primarily urban and suburban communities, Tenet Healthcare (NYSE:THC) operates a nationwide network of hospitals, ambulatory surgery centers, and outpatient facilities providing acute care and specialty healthcare services.

Tenet's business is organized into two main segments: Hospital Operations and Services, and Ambulatory Care. The Hospital Operations segment includes acute care and specialty hospitals, physician practices, and various outpatient facilities including imaging centers, urgent care centers, and micro-hospitals. These facilities offer a range of services from basic acute care to advanced treatments like cardiothoracic surgery, complex spinal procedures, and trauma services.

The Ambulatory Care segment operates through USPI (United Surgical Partners International), which manages over 460 ambulatory surgery centers and 24 surgical hospitals across 35 states. These facilities specialize in high-demand procedures like orthopedics, joint replacements, gastroenterology, and ophthalmology services, typically delivered in more cost-effective outpatient settings.

Tenet's revenue comes from multiple sources, including payments from private insurance companies, government healthcare programs like Medicare and Medicaid, and directly from patients. A patient might visit a Tenet facility for anything from emergency treatment at one of their hospitals to a scheduled outpatient procedure at a USPI surgery center.

The company also provides revenue cycle management and value-based care services through its Conifer joint venture, helping both Tenet and non-Tenet healthcare providers with functions like insurance verification, billing, collections, and clinical documentation improvement.

Tenet continuously refines its portfolio through strategic acquisitions, joint ventures, and divestitures. For example, in 2023, the company acquired interests in 56 urgent care centers in Arizona through a joint venture with NextCare, while also selling several hospitals in South Carolina and California that no longer aligned with its long-term strategy.

4. Hospital Chains

Hospital chains operate scale-driven businesses that rely on patient volumes, efficient operations, and favorable payer contracts to drive revenue and profitability. These organizations benefit from the essential nature of their services, which ensures consistent demand, particularly as populations age and chronic diseases become more prevalent. However, profitability can be pressured by rising labor costs, regulatory requirements, and the challenges of balancing care quality with cost efficiency. Dependence on government and private insurance reimbursements also introduces financial uncertainty. Looking ahead, hospital chains stand to benefit from tailwinds such as increasing healthcare utilization driven by an aging population that generally has higher incidents of disease. AI can also be a tailwind in areas such as predictive analytics for more personalized treatment and efficiency (intake, staffing, resourcing allocation). However, the sector faces potential headwinds such as labor shortages that could push up wages as well as substantial investments needs for digital infrastructure to support telehealth and electronic health records. Regulatory scrutiny, and reimbursement cuts are also looming topics that could further strain margins.

Tenet Healthcare's main competitors include HCA Healthcare (NYSE:HCA), Community Health Systems (NYSE:CYH), Universal Health Services (NYSE:UHS), and Surgery Partners (NASDAQ:SGRY) in the hospital and ambulatory surgery center space.

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $21.31 billion in revenue over the past 12 months, Tenet Healthcare has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, Tenet Healthcare’s 3.9% annualized revenue growth over the last five years was tepid. This wasn’t a great result compared to the rest of the healthcare sector, but there are still things to like about Tenet Healthcare.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Tenet Healthcare’s recent performance shows its demand has slowed as its annualized revenue growth of 1.8% over the last two years was below its five-year trend.

We can better understand the company’s revenue dynamics by analyzing its same-store sales, which show how much revenue its established locations generate. Over the last two years, Tenet Healthcare’s same-store sales averaged 1.8% year-on-year growth. This number doesn’t surprise us as it’s in line with its revenue growth.

This quarter, Tenet Healthcare reported year-on-year revenue growth of 9%, and its $5.53 billion of revenue exceeded Wall Street’s estimates by 1.1%.

Looking ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months. Although this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector. At least the company is tracking well in other measures of financial health.

7. Operating Margin

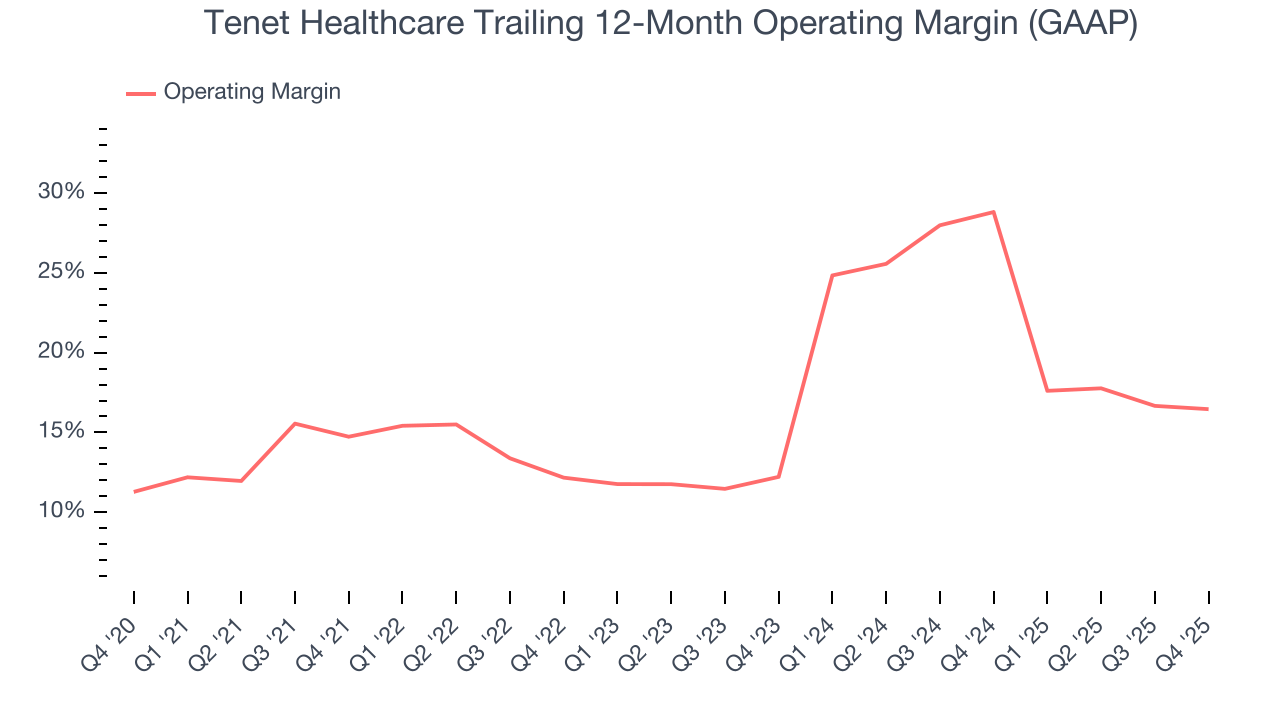

Tenet Healthcare has managed its cost base well over the last five years. It demonstrated solid profitability for a healthcare business, producing an average operating margin of 17%.

Looking at the trend in its profitability, Tenet Healthcare’s operating margin rose by 1.7 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its recent improvements as the company’s margin has increased by 4.2 percentage points on a two-year basis.

This quarter, Tenet Healthcare generated an operating margin profit margin of 15.4%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

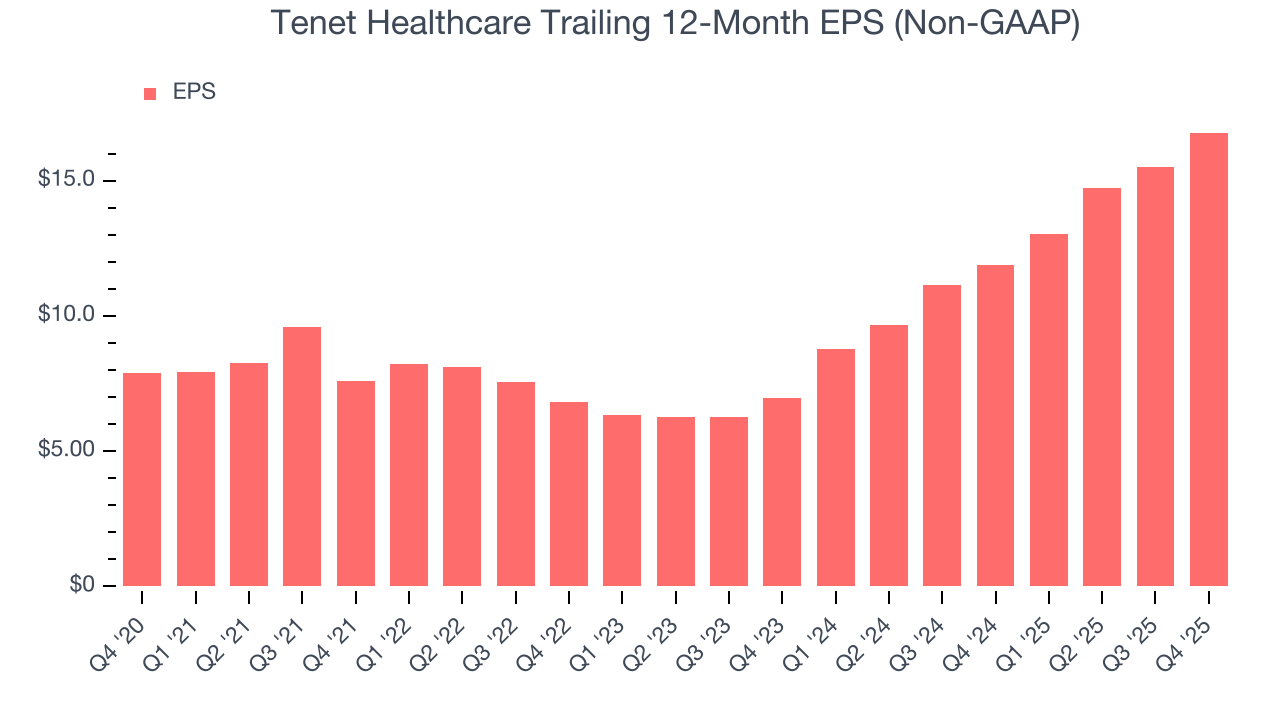

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Tenet Healthcare’s EPS grew at an astounding 16.3% compounded annual growth rate over the last five years, higher than its 3.9% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

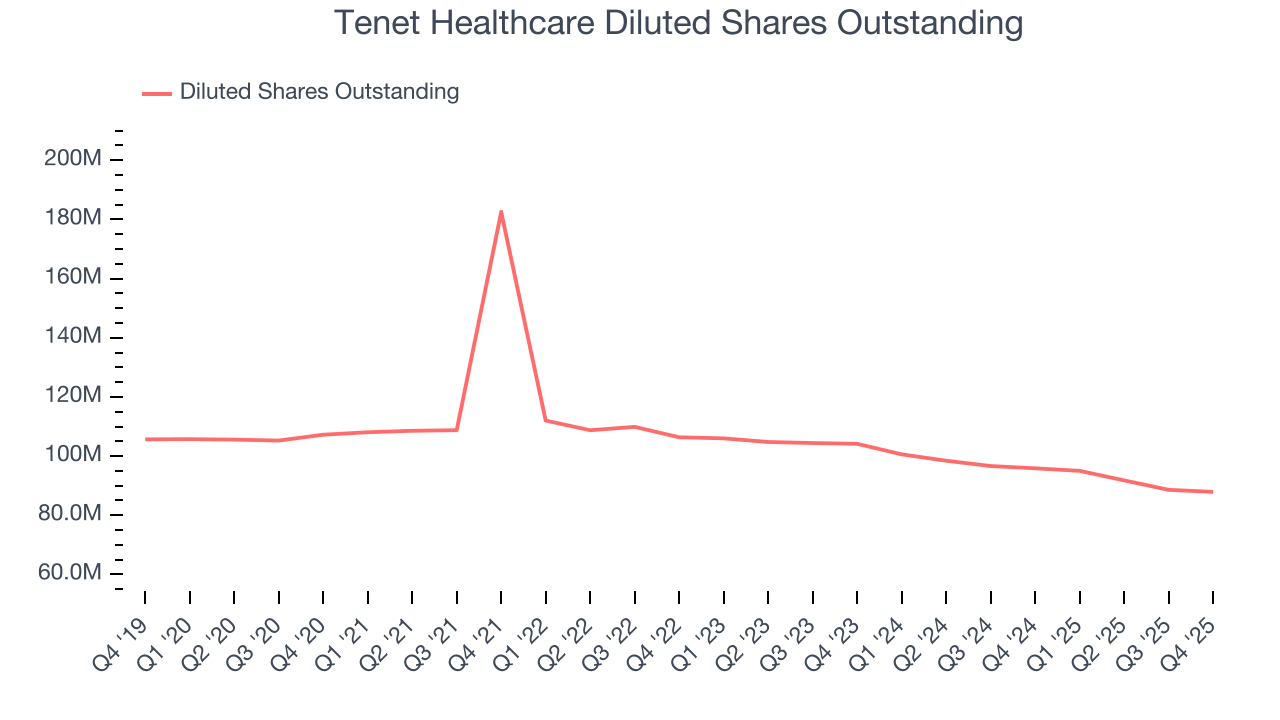

We can take a deeper look into Tenet Healthcare’s earnings to better understand the drivers of its performance. As we mentioned earlier, Tenet Healthcare’s operating margin was flat this quarter but expanded by 1.7 percentage points over the last five years. On top of that, its share count shrank by 18%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Tenet Healthcare reported adjusted EPS of $4.70, up from $3.44 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Tenet Healthcare’s full-year EPS of $16.78 to stay about the same.

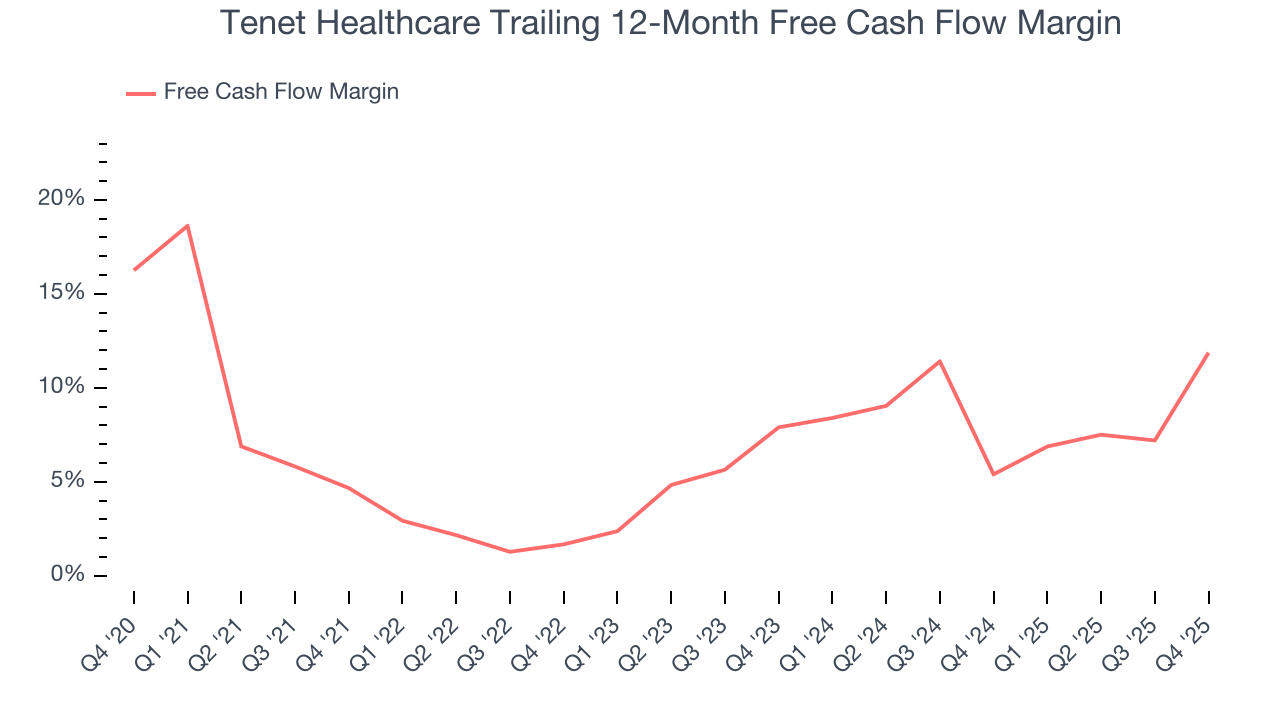

9. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Tenet Healthcare has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 6.4% over the last five years, slightly better than the broader healthcare sector.

Taking a step back, we can see that Tenet Healthcare’s margin expanded by 7.2 percentage points during that time. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Tenet Healthcare’s free cash flow clocked in at $367 million in Q4, equivalent to a 6.6% margin. Its cash flow turned positive after being negative in the same quarter last year, building on its favorable historical trend.

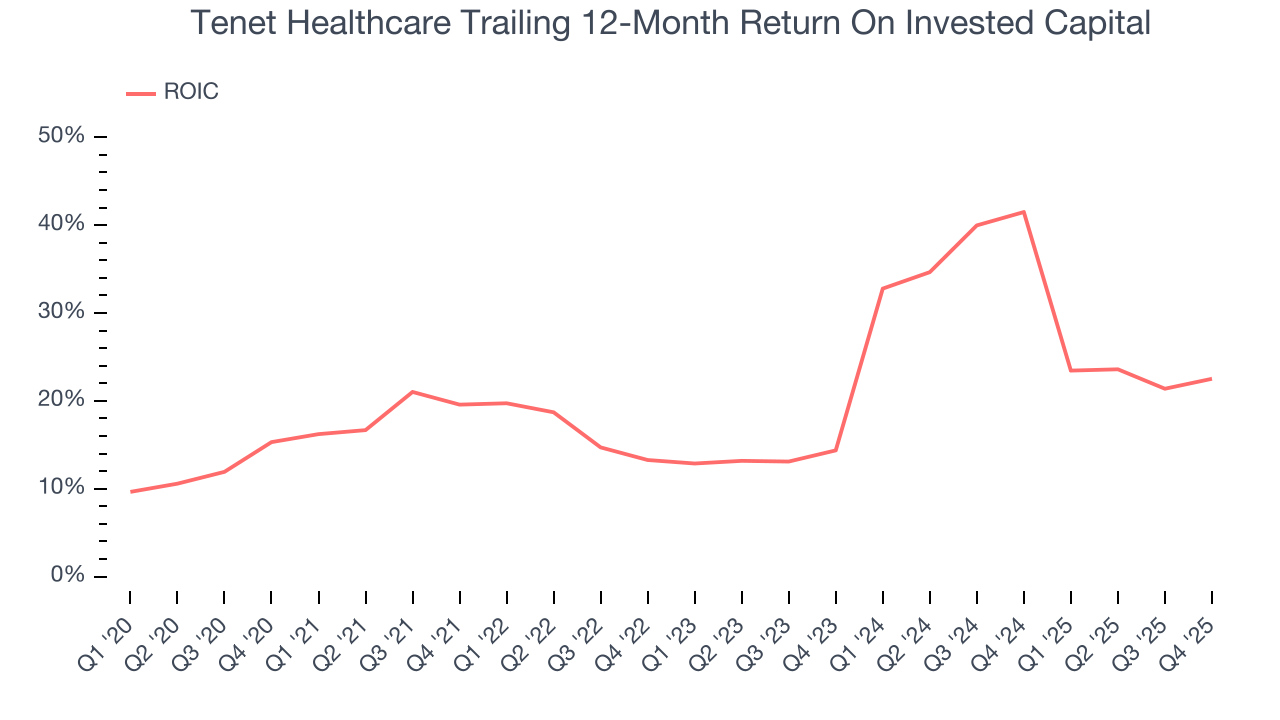

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

Tenet Healthcare’s five-year average ROIC was 22.2%, placing it among the best healthcare companies. This illustrates its management team’s ability to invest in highly profitable ventures and produce tangible results for shareholders.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Tenet Healthcare’s ROIC has increased significantly. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

11. Balance Sheet Assessment

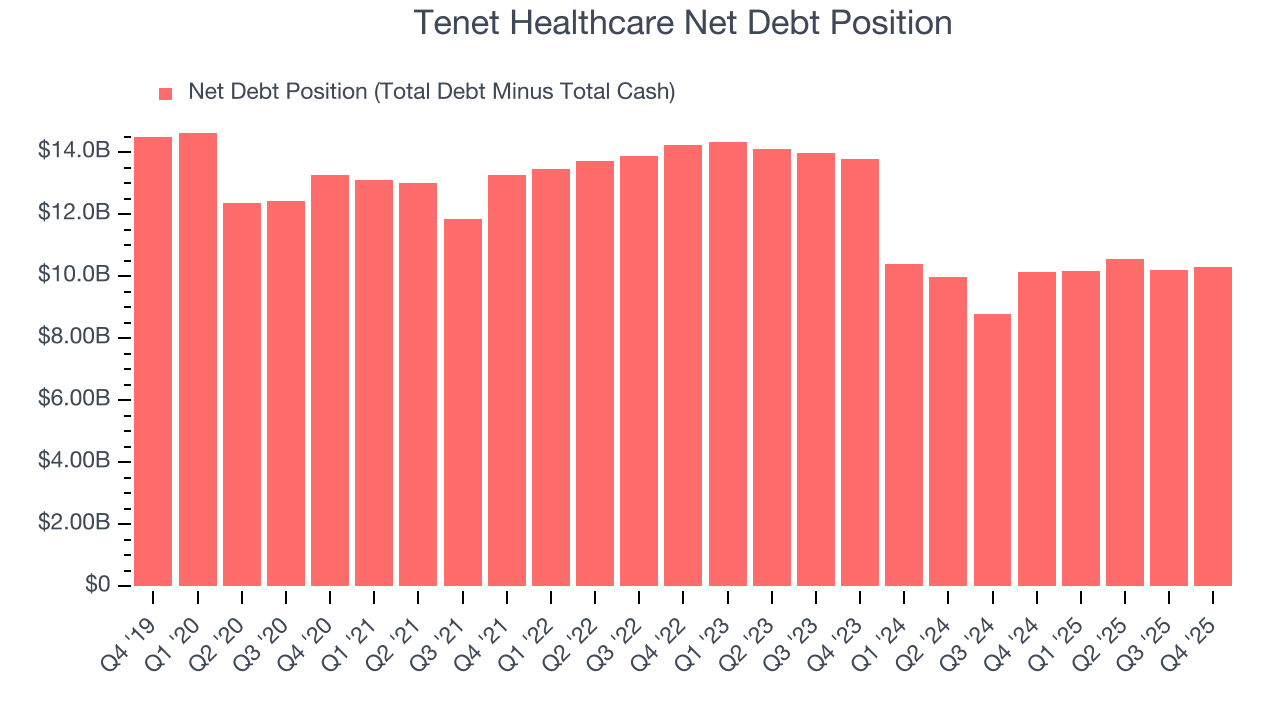

Tenet Healthcare reported $2.88 billion of cash and $13.17 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $4.57 billion of EBITDA over the last 12 months, we view Tenet Healthcare’s 2.3× net-debt-to-EBITDA ratio as safe. We also see its $411 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Tenet Healthcare’s Q4 Results

We were impressed by how significantly Tenet Healthcare blew past analysts’ full-year EPS guidance expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its full-year revenue guidance slightly missed. Overall, this print had some key positives. The stock remained flat at $193.07 immediately after reporting.

13. Is Now The Time To Buy Tenet Healthcare?

Updated: March 21, 2026 at 12:08 AM EDT

The latest quarterly earnings matters, sure, but we actually think longer-term fundamentals and valuation matter more. Investors should consider all these pieces before deciding whether or not to invest in Tenet Healthcare.

Tenet Healthcare is a fine business. Although its revenue growth was uninspiring over the last five years, its rising cash profitability gives it more optionality. And while its same-store sales growth has disappointed, its astounding EPS growth over the last five years shows its profits are trickling down to shareholders.

Tenet Healthcare’s P/E ratio based on the next 12 months is 11.9x. Looking at the healthcare space right now, Tenet Healthcare trades at a compelling valuation. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $261.38 on the company (compared to the current share price of $200.01), implying they see 30.7% upside in buying Tenet Healthcare in the short term.