Tilly's (TLYS)

We wouldn’t buy Tilly's. Not only did its demand evaporate but also its negative returns on capital show it destroyed shareholder value.― StockStory Analyst Team

1. News

2. Summary

Why We Think Tilly's Will Underperform

With an emphasis on skate and surf culture, Tilly’s (NYSE:TLYS) is a specialty retailer that sells clothing, footwear, and accessories geared towards fashion-forward teens and young adults.

- Store closures and poor same-store sales reveal weak demand and a push toward operational efficiency

- Annual revenue declines of 6.3% over the last three years indicate problems with its market positioning

- Unprofitable operations could lead to additional rounds of dilutive equity financing if the credit window closes

Tilly’s quality isn’t up to par. There are more rewarding stocks elsewhere.

Why There Are Better Opportunities Than Tilly's

At $2.63 per share, Tilly's trades at 75.6x forward EV-to-EBITDA. This valuation is extremely expensive, especially for the weaker revenue growth you get.

There are stocks out there featuring similar valuation multiples with better fundamentals. We prefer to invest in those.

3. Tilly's (TLYS) Research Report: Q4 CY2025 Update

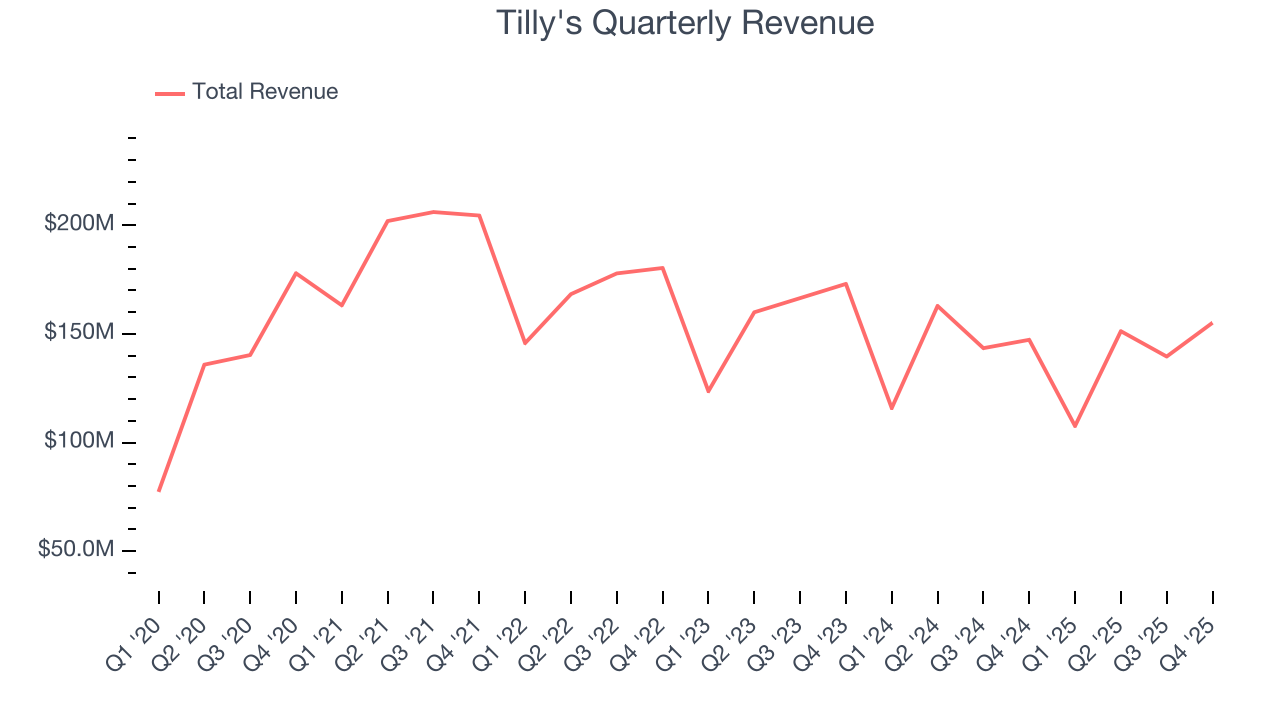

Young adult apparel retailer Tilly’s (NYSE:TLYS) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 5.3% year on year to $155.1 million. On top of that, next quarter’s revenue guidance ($122 million at the midpoint) was surprisingly good and 14.6% above what analysts were expecting. Its GAAP profit of $0.10 per share was significantly above analysts’ consensus estimates.

Tilly's (TLYS) Q4 CY2025 Highlights:

- Revenue: $155.1 million vs analyst estimates of $148.7 million (5.3% year-on-year growth, 4.3% beat)

- EPS (GAAP): $0.10 vs analyst estimates of -$0.15 (significant beat)

- Adjusted EBITDA: $6.96 million (4.5% margin, 153% year-on-year growth)

- Revenue Guidance for Q1 CY2026 is $122 million at the midpoint, above analyst estimates of $106.5 million

- EPS (GAAP) guidance for Q1 CY2026 is -$0.31 at the midpoint, beating analyst estimates by 56.4%

- Operating Margin: 1.7%, up from -9.1% in the same quarter last year

- Free Cash Flow was $7.27 million, up from -$5.36 million in the same quarter last year

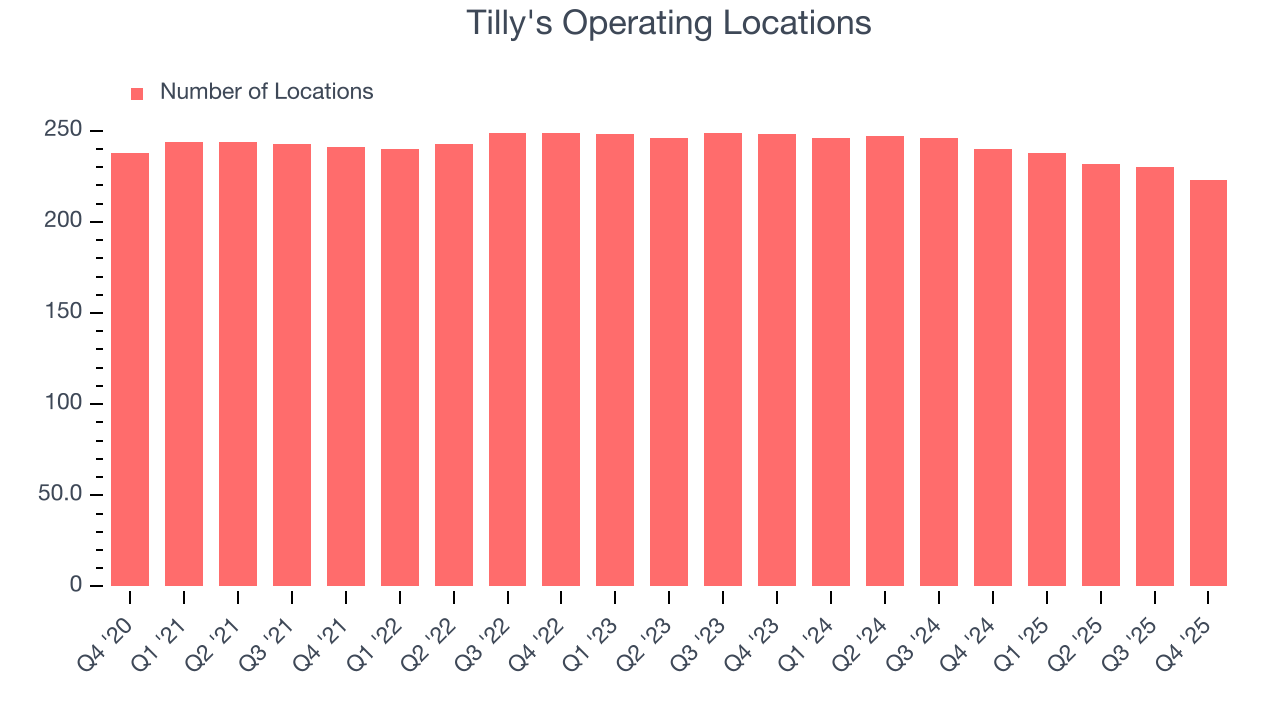

- Locations: 223 at quarter end, down from 240 in the same quarter last year

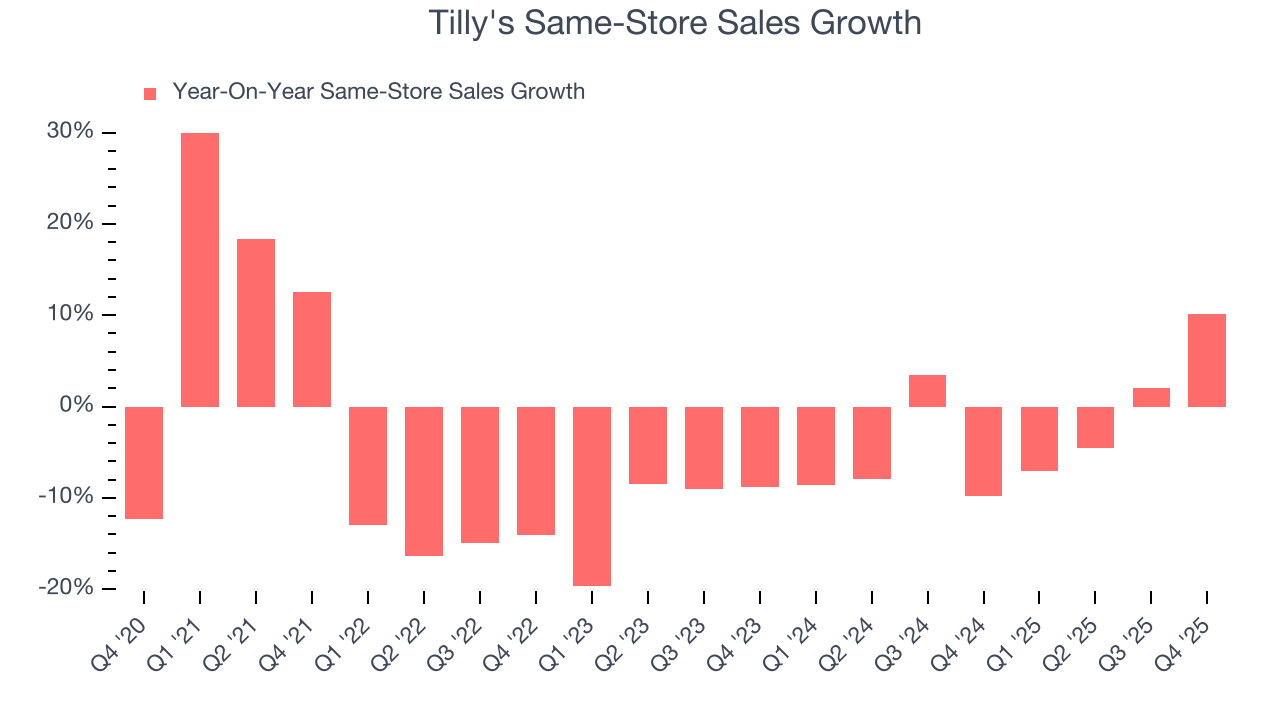

- Same-Store Sales rose 10.1% year on year (-9.8% in the same quarter last year)

- Market Capitalization: $48.15 million

Company Overview

With an emphasis on skate and surf culture, Tilly’s (NYSE:TLYS) is a specialty retailer that sells clothing, footwear, and accessories geared towards fashion-forward teens and young adults.

Vans, Billabong, Hurley, and Volcom are some of the brands that can be commonly found for sale. The core Tilly’s customer is usually a teen or young adult steeped in skate and surf culture who has a desire to signal these interests through fashion.

On average, stores tend to be moderate in size, roughly 7,500 square feet. They are often located in suburban malls or shopping centers alongside other mass market retailers. Upon entering a Tilly’s store, a shopper will likely notice the vibrant and colorful displays and signage as well as music that fits with the prevailing skate and surf lifestyle. A store is usually divided into men’s, women’s and kid’s clothing. There may also be a limited selection of skate decks and other equipment, although this is not the primary focus.

4. Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Competitors that sell edgy or skate-inspired young adult clothing include Urban Outfitters (NASDAQ:URBN), Zumiez (NASDAQ:ZUMZ), and Genesco’s (NYSE:GCO) Journeys banner.

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can have short-term success, but a top-tier one grows for years.

With $553.6 million in revenue over the past 12 months, Tilly's is a small retailer, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with suppliers.

As you can see below, Tilly’s demand was weak over the last three years. Its sales fell by 6.3% annually as it closed stores and observed lower sales at existing, established locations.

This quarter, Tilly's reported year-on-year revenue growth of 5.3%, and its $155.1 million of revenue exceeded Wall Street’s estimates by 4.3%. Company management is currently guiding for a 13.4% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products will catalyze better top-line performance, it is still below the sector average.

6. Store Performance

Number of Stores

A retailer’s store count often determines how much revenue it can generate.

Tilly's listed 223 locations in the latest quarter and has generally closed its stores over the last two years, averaging 3.5% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

A company's store base only paints one part of the picture. When demand is high, it makes sense to open more. But when demand is low, it’s prudent to close some locations and use the money in other ways. Same-store sales provides a deeper understanding of this issue because it measures organic growth at brick-and-mortar shops for at least a year.

Tilly’s demand has been shrinking over the last two years as its same-store sales have averaged 2.8% annual declines. This performance isn’t ideal, and Tilly's is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Tilly’s same-store sales rose 10.1% year on year. This growth was a well-appreciated turnaround from its historical levels, showing the business is regaining momentum.

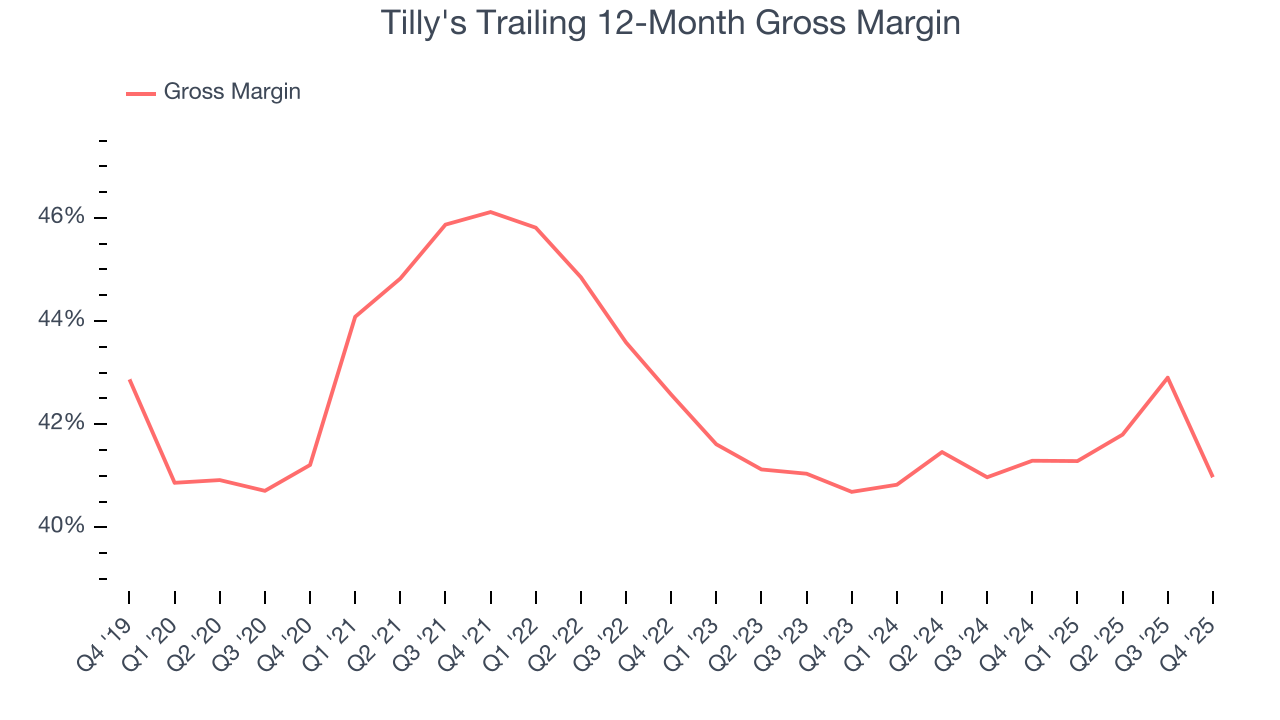

7. Gross Margin & Pricing Power

At StockStory, we prefer high gross margin businesses because they indicate pricing power or differentiated products, giving the company a chance to generate higher operating profits.

Tilly’s unit economics are higher than the typical retailer, giving it the flexibility to invest in areas such as marketing and talent to reach more consumers. As you can see below, it averaged a decent 41.1% gross margin over the last two years. That means for every $100 in revenue, $58.87 went towards paying for inventory, transportation, and distribution.

In Q4, Tilly's produced a 33.8% gross profit margin , marking a 6.8 percentage point decrease from 40.6% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

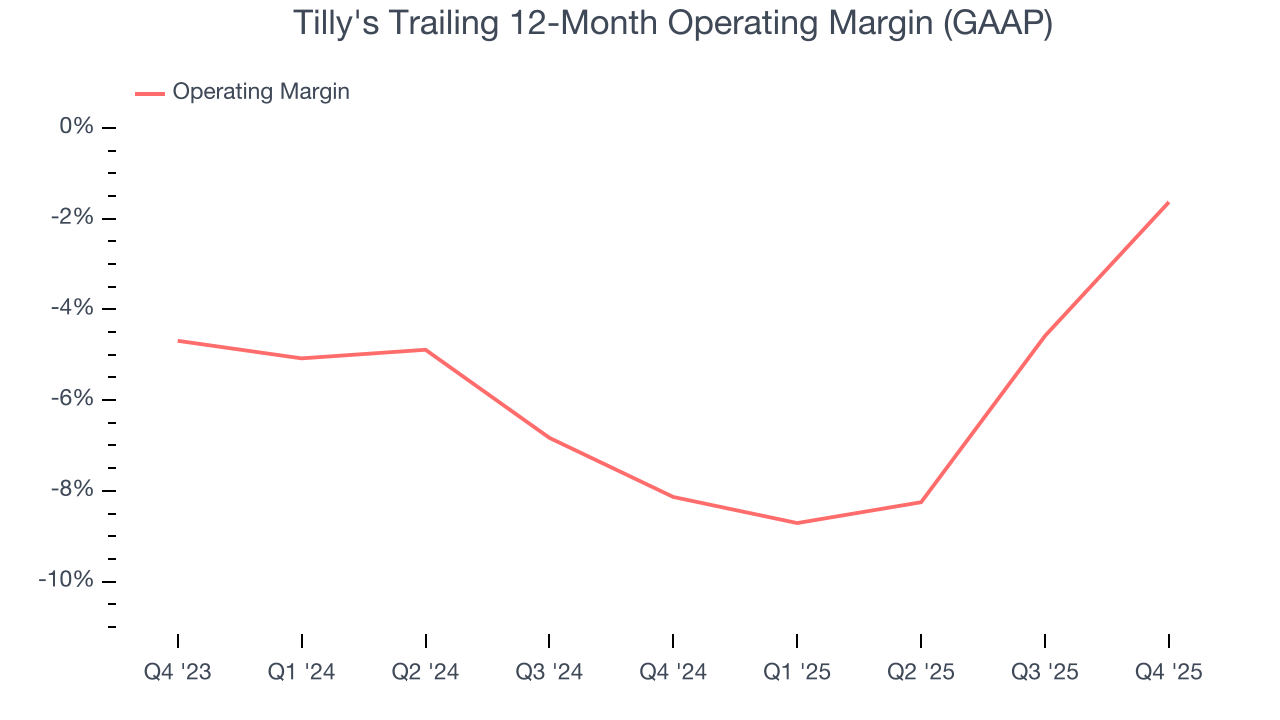

8. Operating Margin

Although Tilly's was profitable this quarter from an operational perspective, it’s generally struggled over a longer time period. Its expensive cost structure has contributed to an average operating margin of negative 4.9% over the last two years. Despite the consumer retail industry’s secular decline, unprofitable public companies are few and far between. It’s unfortunate that Tilly's was one of them.

On the plus side, Tilly’s operating margin rose by 6.5 percentage points over the last year. Still, it will take much more for the company to show consistent profitability.

This quarter, Tilly's generated an operating margin profit margin of 1.7%, up 10.8 percentage points year on year. The increase was solid, and because its gross margin actually decreased, we can assume it was more efficient because its operating expenses like marketing, and administrative overhead grew slower than its revenue.

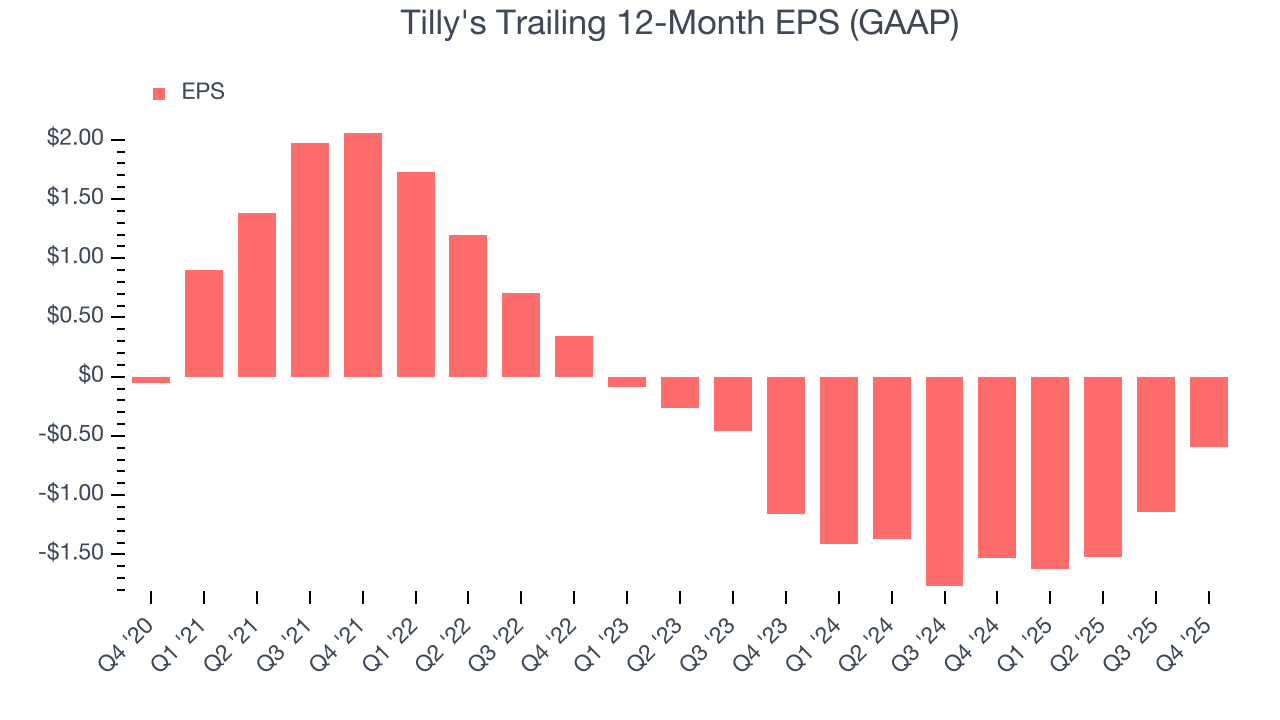

9. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for Tilly's, its EPS declined by 55.2% annually over the last three years, more than its revenue. However, its operating margin actually improved during this time, telling us that non-fundamental factors such as interest expenses and taxes affected its ultimate earnings.

In Q4, Tilly's reported EPS of $0.10, up from negative $0.45 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Tilly's to perform poorly. Analysts forecast its full-year EPS of negative $0.59 will tumble to negative $0.78.

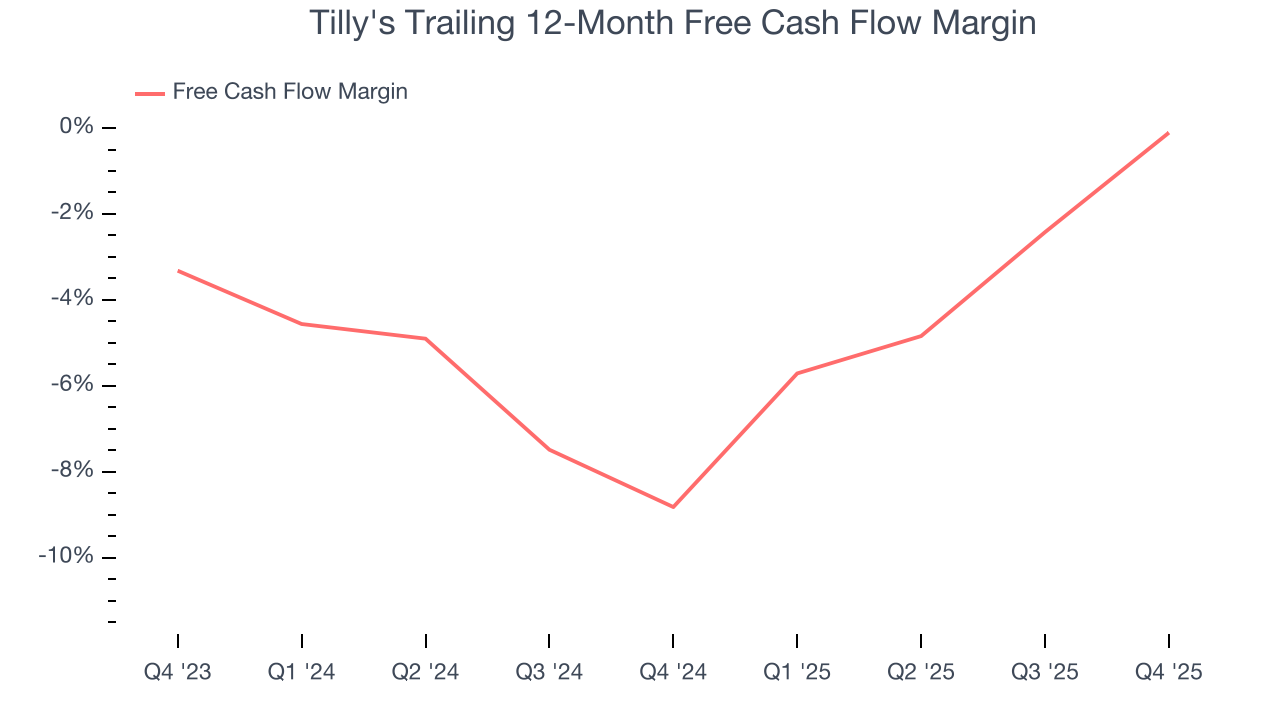

10. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

While Tilly's posted positive free cash flow this quarter, the broader story hasn’t been so clean. Tilly’s demanding reinvestments have consumed many resources over the last two years, contributing to an average free cash flow margin of negative 4.5%. This means it lit $4.53 of cash on fire for every $100 in revenue.

Taking a step back, an encouraging sign is that Tilly’s margin expanded by 8.7 percentage points over the last year. Despite its improvement and recent free cash flow generation, we’d like to see more quarters of positive cash flow before recommending the stock.

Tilly’s free cash flow clocked in at $7.27 million in Q4, equivalent to a 4.7% margin. Its cash flow turned positive after being negative in the same quarter last year, marking a potential inflection point.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Tilly’s five-year average ROIC was negative 6.3%, meaning management lost money while trying to expand the business. Its returns were among the worst in the consumer retail sector.

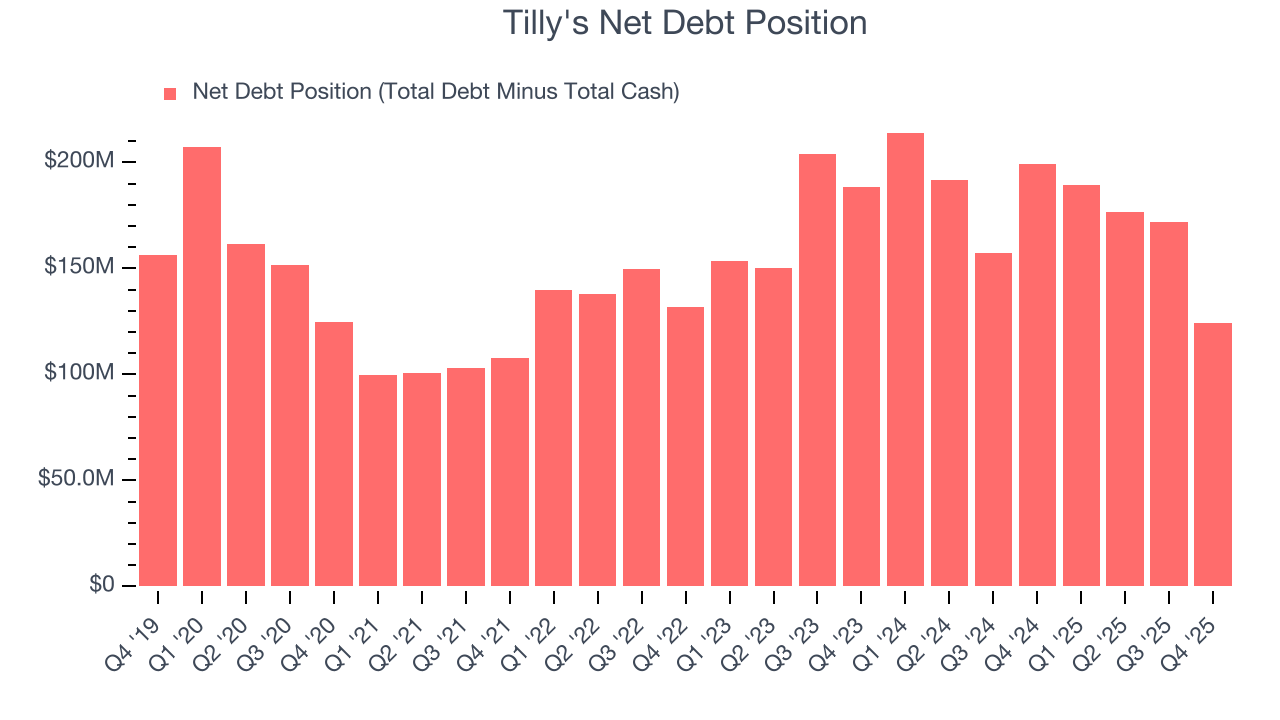

12. Balance Sheet Risk

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

Tilly's posted negative $3.28 million of EBITDA over the last 12 months, and its $170.5 million of debt exceeds the $46.31 million of cash on its balance sheet. This is a deal breaker for us because indebted loss-making companies spell trouble.

We implore our readers to tread carefully because credit agencies could downgrade Tilly's if its unprofitable ways continue, making incremental borrowing more expensive and restricting growth prospects. The company could also be backed into a corner if the market turns unexpectedly. We hope Tilly's can improve its profitability and remain cautious until then.

13. Key Takeaways from Tilly’s Q4 Results

We were impressed by Tilly’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a solid print. The stock traded up 63.2% to $2.64 immediately after reporting.

14. Is Now The Time To Buy Tilly's?

Updated: March 14, 2026 at 10:36 PM EDT

Are you wondering whether to buy Tilly's or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

Tilly's doesn’t pass our quality test. To begin with, its revenue has declined over the last three years. While its projected EPS for the next year implies the company’s fundamentals will improve, the downside is its brand caters to a niche market. On top of that, its declining EPS over the last three years makes it a less attractive asset to the public markets.

Tilly’s EV-to-EBITDA ratio based on the next 12 months is 75.6x. This valuation tells us it’s a bit of a market darling with a lot of good news priced in - you can find more timely opportunities elsewhere.

Wall Street analysts have a consensus one-year price target of $3 on the company (compared to the current share price of $2.63).