Universal Health Services (UHS)

Universal Health Services is a sound business. Its eye-popping 14.3% annualized EPS growth over the last five years has significantly outpaced its peers.― StockStory Analyst Team

1. News

2. Summary

Why Universal Health Services Is Interesting

With a network spanning 39 states and three countries, Universal Health Services (NYSE:UHS) operates acute care hospitals and behavioral health facilities across the United States, United Kingdom, and Puerto Rico.

- Incremental sales over the last five years have been highly profitable as its earnings per share increased by 14.3% annually, topping its revenue gains

- Revenue base of $17.36 billion gives it economies of scale and some negotiating power

- One risk is its lagging comparable store sales over the past two years suggest it might have to change its pricing and marketing strategy to stimulate demand

Universal Health Services is close to becoming a high-quality business. If you like the story, the price seems fair.

Why Is Now The Time To Buy Universal Health Services?

Universal Health Services’s stock price of $186.11 implies a valuation ratio of 8x forward P/E. The current valuation sure seems like a good deal considering Universal Health Services’s business fundamentals.

If you think the market is not giving the company enough credit for its fundamentals, now could be a good time to invest.

3. Universal Health Services (UHS) Research Report: Q4 CY2025 Update

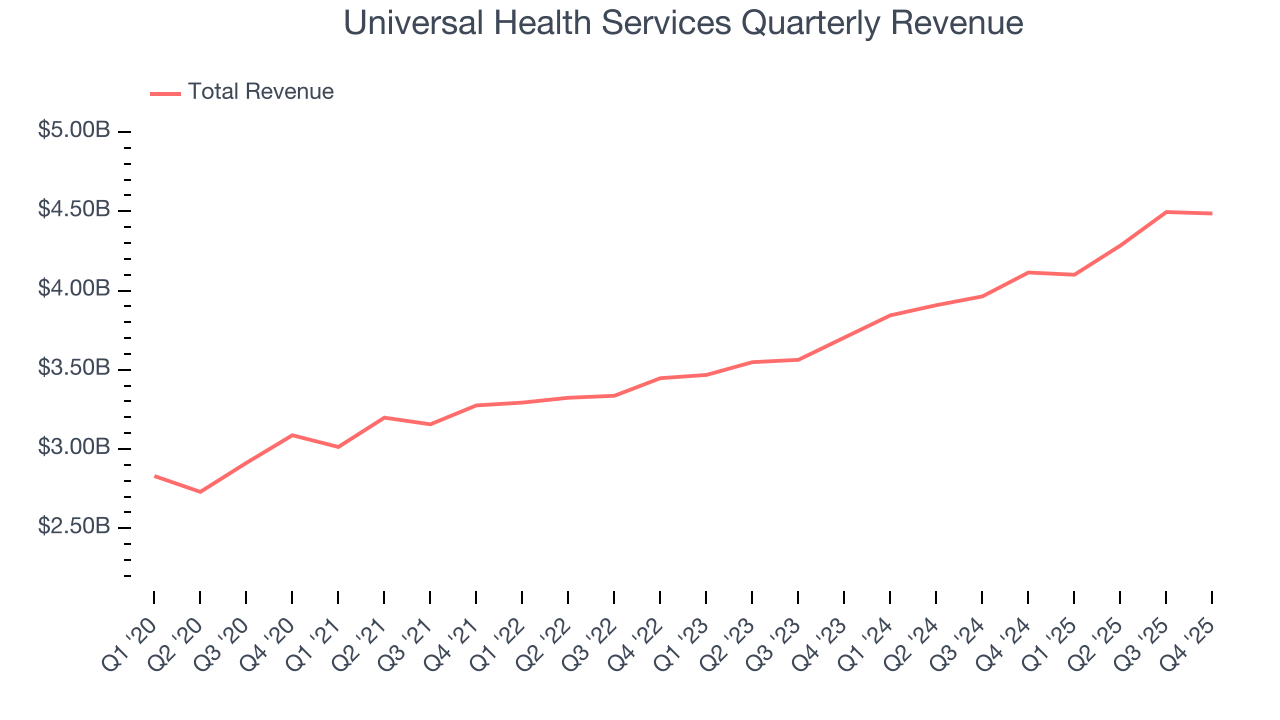

Hospital management company Universal Health Services (NYSE:UHS) missed Wall Street’s revenue expectations in Q4 CY2025, but sales rose 9.1% year on year to $4.49 billion. On the other hand, the company’s full-year revenue guidance of $18.6 billion at the midpoint came in 2% above analysts’ estimates. Its non-GAAP profit of $5.88 per share was 0.5% below analysts’ consensus estimates.

Universal Health Services (UHS) Q4 CY2025 Highlights:

- Revenue: $4.49 billion vs analyst estimates of $4.51 billion (9.1% year-on-year growth, 0.6% miss)

- Adjusted EPS: $5.88 vs analyst expectations of $5.91 (0.5% miss)

- Adjusted EBITDA: $678.7 million vs analyst estimates of $682.6 million (15.1% margin, 0.6% miss)

- Adjusted EPS guidance for the upcoming financial year 2026 is $23.58 at the midpoint, beating analyst estimates by 0.8%

- EBITDA guidance for the upcoming financial year 2026 is $2.72 billion at the midpoint, above analyst estimates of $2.69 billion

- Operating Margin: 11.5%, in line with the same quarter last year

- Free Cash Flow Margin: 19.1%, up from 10% in the same quarter last year

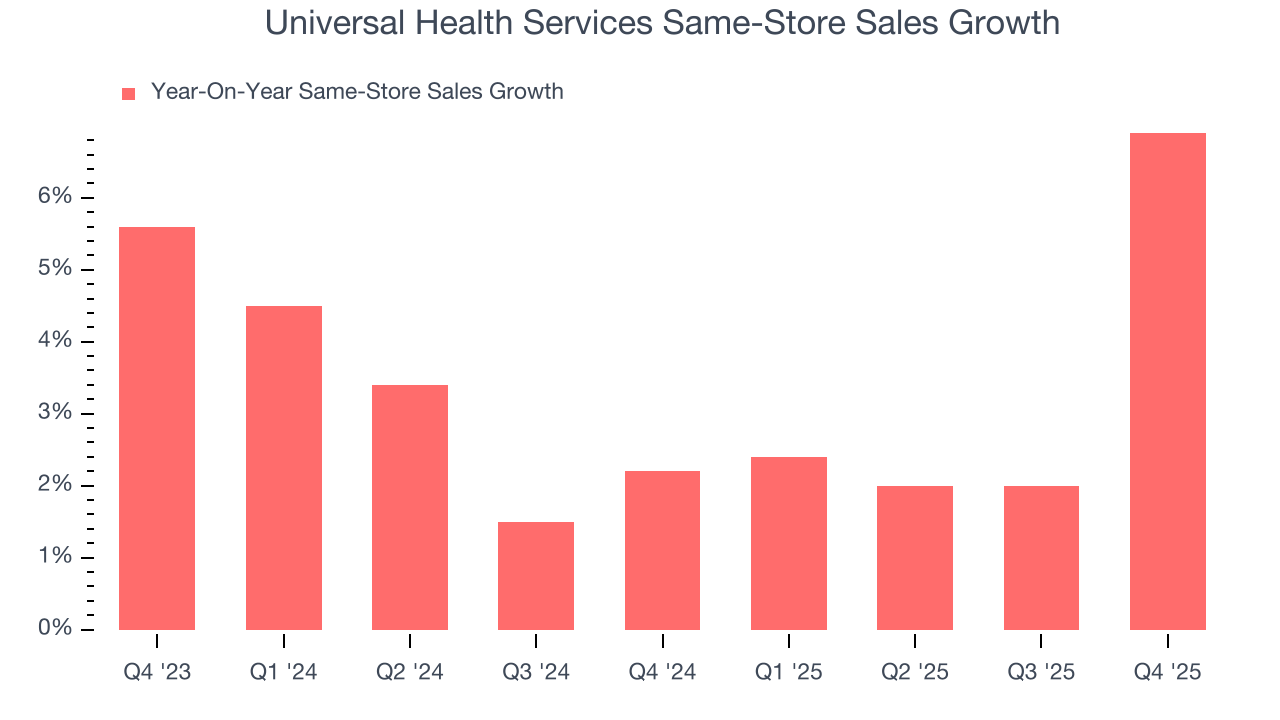

- Same-Store Sales rose 6.9% year on year (2.2% in the same quarter last year)

- Market Capitalization: $14.37 billion

Company Overview

With a network spanning 39 states and three countries, Universal Health Services (NYSE:UHS) operates acute care hospitals and behavioral health facilities across the United States, United Kingdom, and Puerto Rico.

The company's healthcare operations are divided into two main segments. The acute care division includes inpatient hospitals, free-standing emergency departments, outpatient centers, and surgical hospitals. These facilities provide a range of medical services including general and specialty surgery, internal medicine, obstetrics, emergency care, radiology, oncology, and pharmacy services.

The behavioral health division, which generates about 43% of the company's revenue, encompasses inpatient and outpatient mental health facilities. This segment addresses various psychiatric and substance abuse disorders, offering specialized treatment programs for different patient populations.

A patient experiencing a mental health crisis might be admitted to one of UHS's behavioral health facilities, where they would receive a personalized treatment plan that could include therapy, medication management, and specialized care from mental health professionals. Similarly, someone requiring emergency surgery might be treated at a UHS acute care hospital, benefiting from the facility's surgical expertise and comprehensive post-operative care.

UHS generates revenue primarily through payments from commercial health insurers, Medicare, Medicaid, and self-paying patients. The company provides not just medical services but also management expertise to its facilities, including centralized purchasing, information technology systems, financial controls, physician recruitment, and marketing.

Beyond simply operating existing facilities, UHS pursues strategic growth through acquisitions and new construction. The company maintains quality standards through accreditation by The Joint Commission, and its facilities are certified as Medicare and Medicaid providers. UHS must comply with numerous healthcare regulations, including the Emergency Medical Treatment and Active Labor Act, which requires hospitals to provide emergency care regardless of a patient's ability to pay.

4. Hospital Chains

Hospital chains operate scale-driven businesses that rely on patient volumes, efficient operations, and favorable payer contracts to drive revenue and profitability. These organizations benefit from the essential nature of their services, which ensures consistent demand, particularly as populations age and chronic diseases become more prevalent. However, profitability can be pressured by rising labor costs, regulatory requirements, and the challenges of balancing care quality with cost efficiency. Dependence on government and private insurance reimbursements also introduces financial uncertainty. Looking ahead, hospital chains stand to benefit from tailwinds such as increasing healthcare utilization driven by an aging population that generally has higher incidents of disease. AI can also be a tailwind in areas such as predictive analytics for more personalized treatment and efficiency (intake, staffing, resourcing allocation). However, the sector faces potential headwinds such as labor shortages that could push up wages as well as substantial investments needs for digital infrastructure to support telehealth and electronic health records. Regulatory scrutiny, and reimbursement cuts are also looming topics that could further strain margins.

Universal Health Services competes with other major healthcare facility operators including HCA Healthcare (NYSE:HCA), Tenet Healthcare (NYSE:THC), Community Health Systems (NYSE:CYH), and Acadia Healthcare (NASDAQ:ACHC).

5. Economies of Scale

Larger companies benefit from economies of scale, where fixed costs like infrastructure, technology, and administration are spread over a higher volume of goods or services, reducing the cost per unit. Scale can also lead to bargaining power with suppliers, greater brand recognition, and more investment firepower. A virtuous cycle can ensue if a scaled company plays its cards right.

With $17.36 billion in revenue over the past 12 months, Universal Health Services has decent scale. This is important as it gives the company more leverage in a heavily regulated, competitive environment that is complex and resource-intensive.

6. Revenue Growth

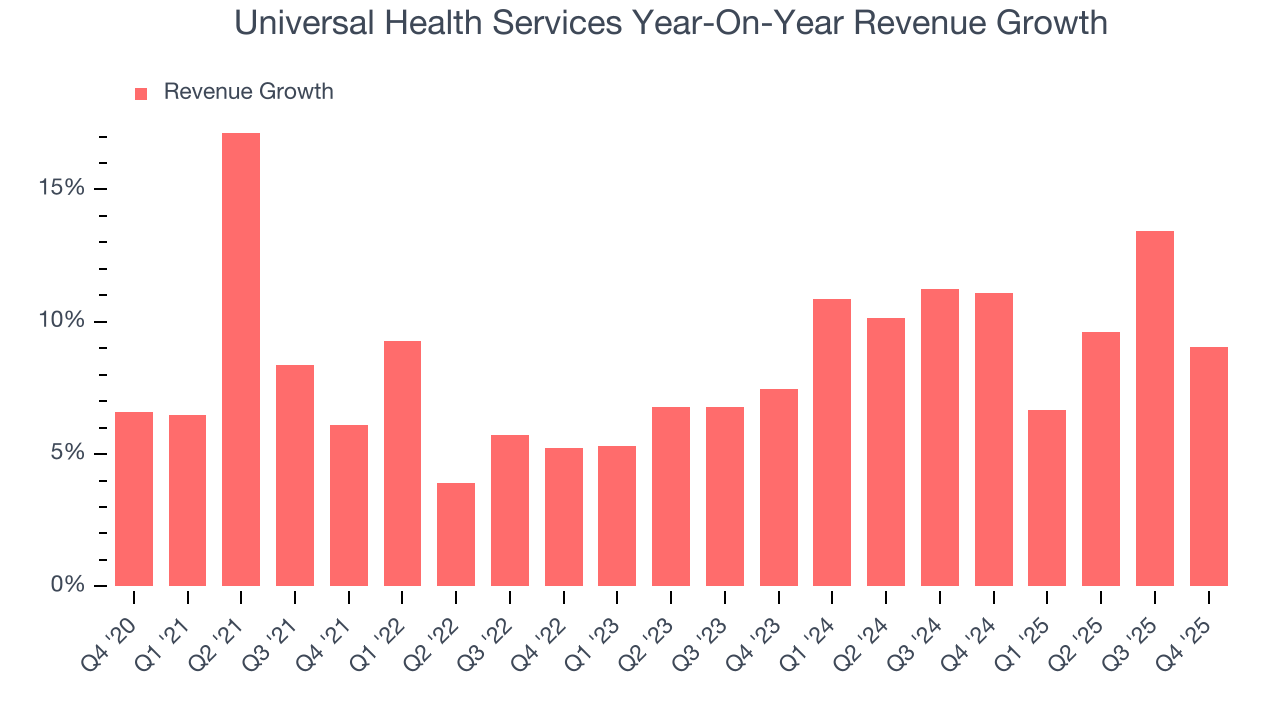

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Luckily, Universal Health Services’s sales grew at a decent 8.5% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Universal Health Services’s annualized revenue growth of 10.3% over the last two years is above its five-year trend, suggesting some bright spots.

Universal Health Services also reports same-store sales, which show how much revenue its established locations generate. Over the last two years, Universal Health Services’s same-store sales averaged 3.1% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Universal Health Services’s revenue grew by 9.1% year on year to $4.49 billion, missing Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5.1% over the next 12 months, a deceleration versus the last two years. We still think its growth trajectory is satisfactory given its scale and suggests the market sees success for its products and services.

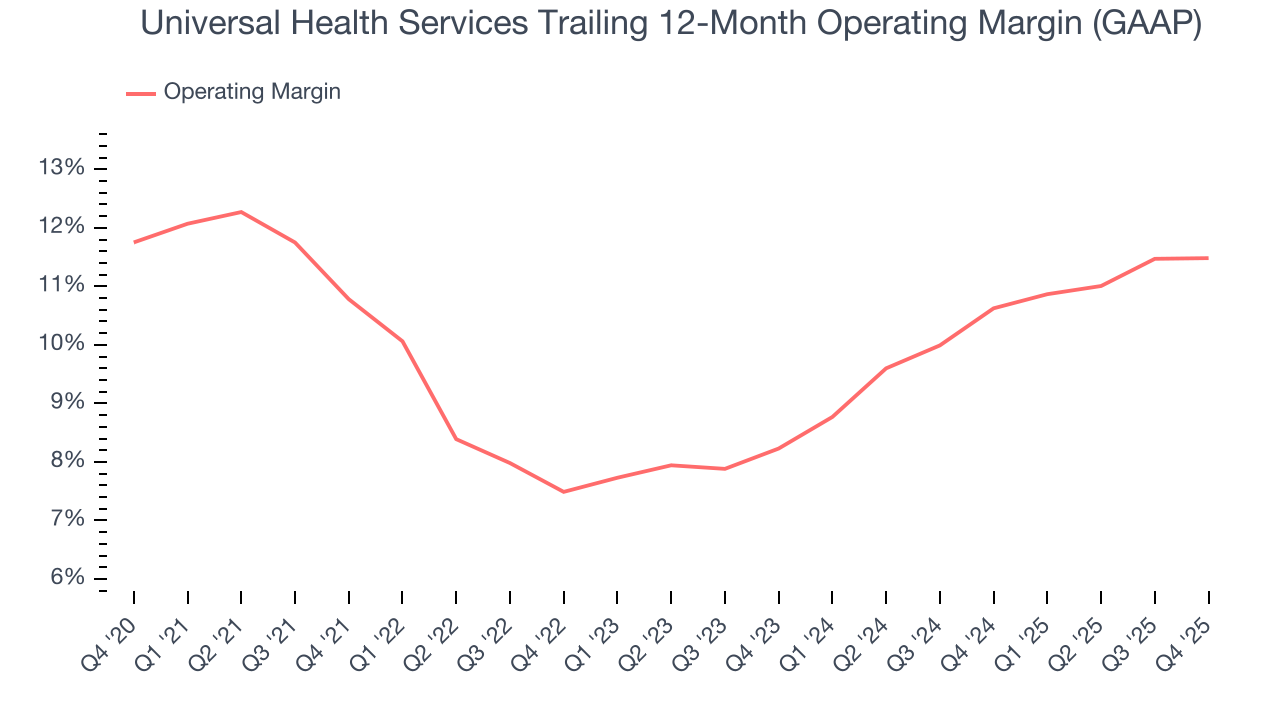

7. Operating Margin

Universal Health Services’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 9.8% over the last five years. This profitability was mediocre for a healthcare business and caused by its suboptimal cost structure.

Analyzing the trend in its profitability, Universal Health Services’s operating margin of 11.5% for the trailing 12 months may be around the same as five years ago, but it has increased by 3.3 percentage points over the last two years. This dynamic unfolded because its sales growth gave it operating leverage and shows it has some momentum on its side.

This quarter, Universal Health Services generated an operating margin profit margin of 11.5%, in line with the same quarter last year. This indicates the company’s overall cost structure has been relatively stable.

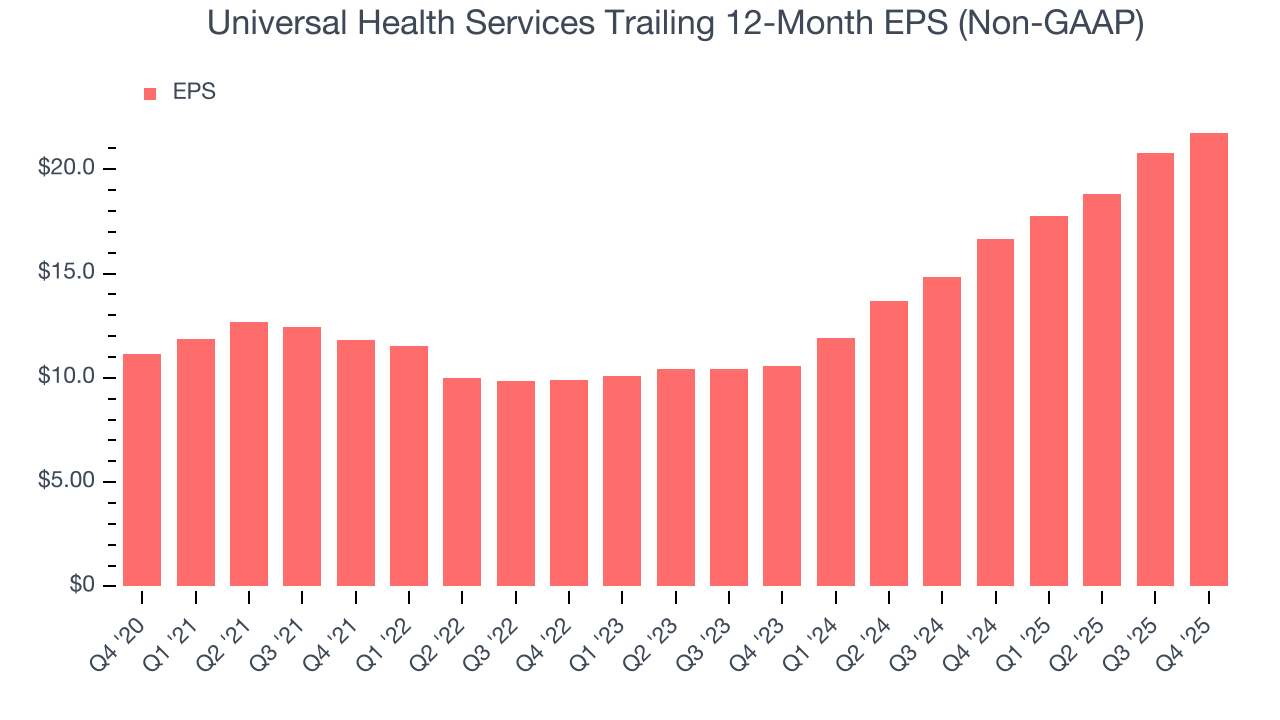

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Universal Health Services’s EPS grew at a spectacular 14.3% compounded annual growth rate over the last five years, higher than its 8.5% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

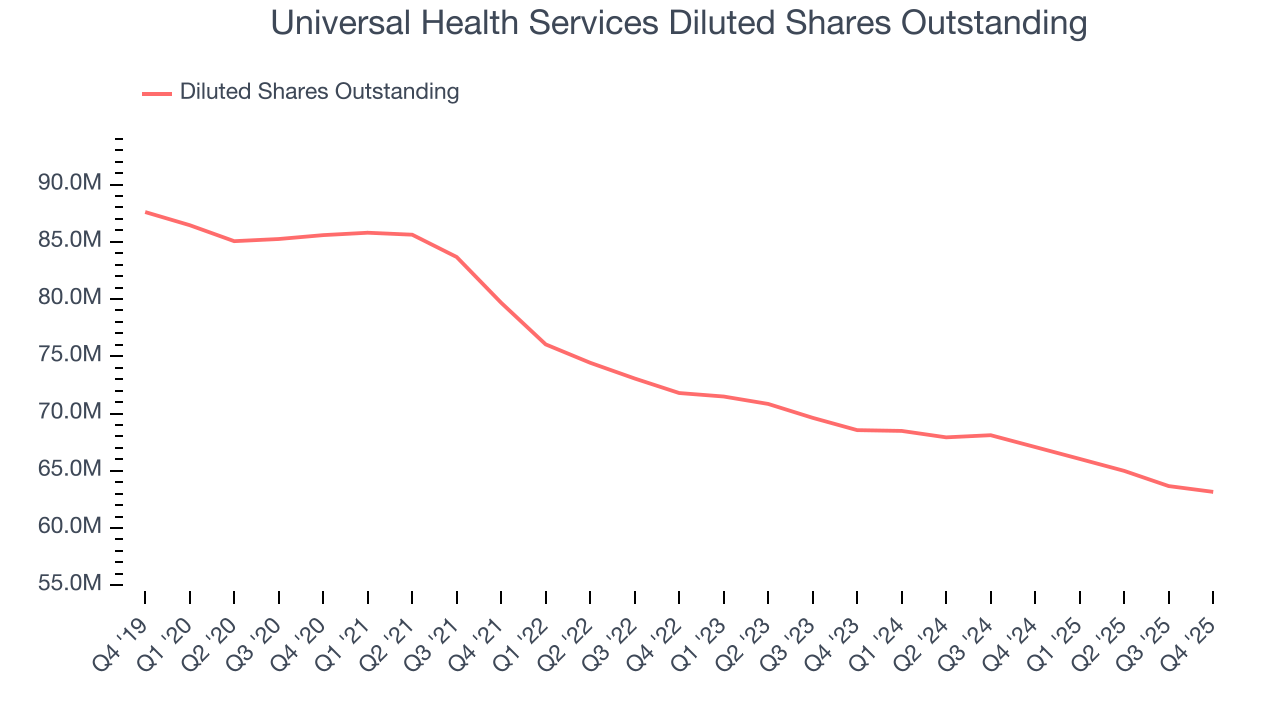

We can take a deeper look into Universal Health Services’s earnings to better understand the drivers of its performance. A five-year view shows that Universal Health Services has repurchased its stock, shrinking its share count by 26.2%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Universal Health Services reported adjusted EPS of $5.88, up from $4.92 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Universal Health Services’s full-year EPS of $21.76 to grow 7.4%.

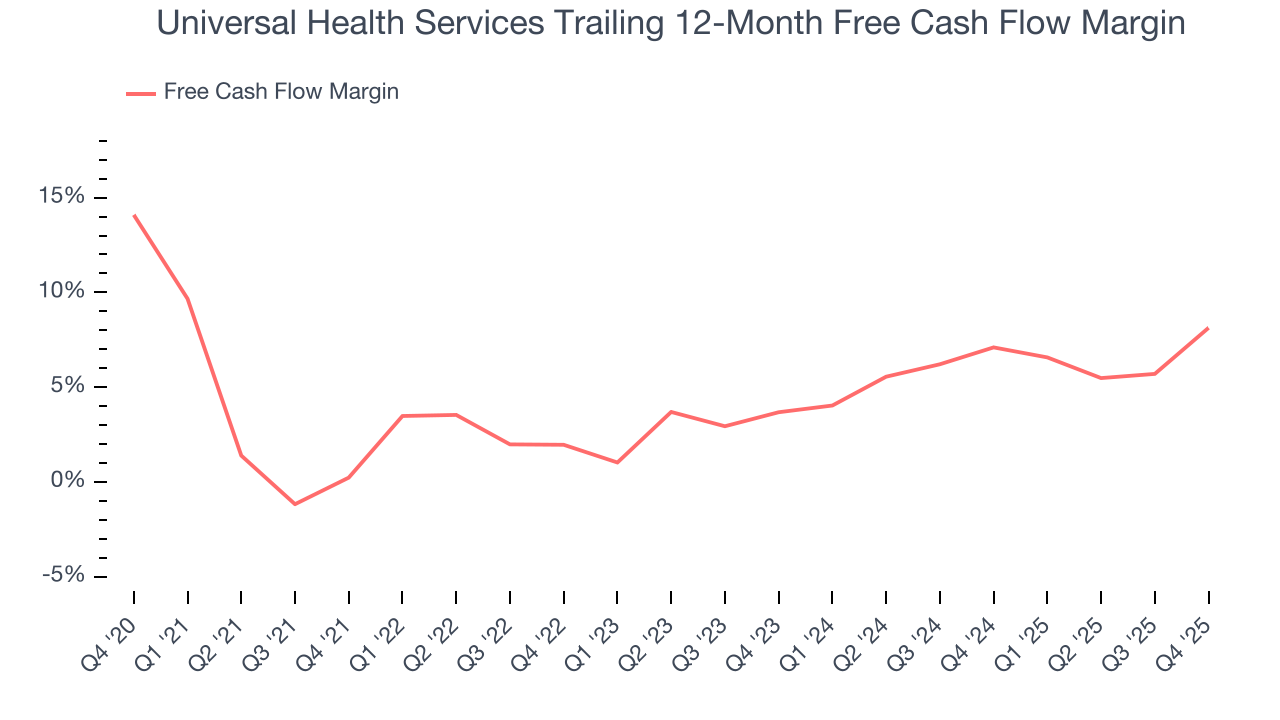

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Universal Health Services has shown mediocre cash profitability over the last five years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 4.6%, subpar for a healthcare business.

Taking a step back, an encouraging sign is that Universal Health Services’s margin expanded by 7.9 percentage points during that time. The company’s improvement shows it’s heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose while its operating profitability was flat.

Universal Health Services’s free cash flow clocked in at $855.9 million in Q4, equivalent to a 19.1% margin. This result was good as its margin was 9.1 percentage points higher than in the same quarter last year, building on its favorable historical trend.

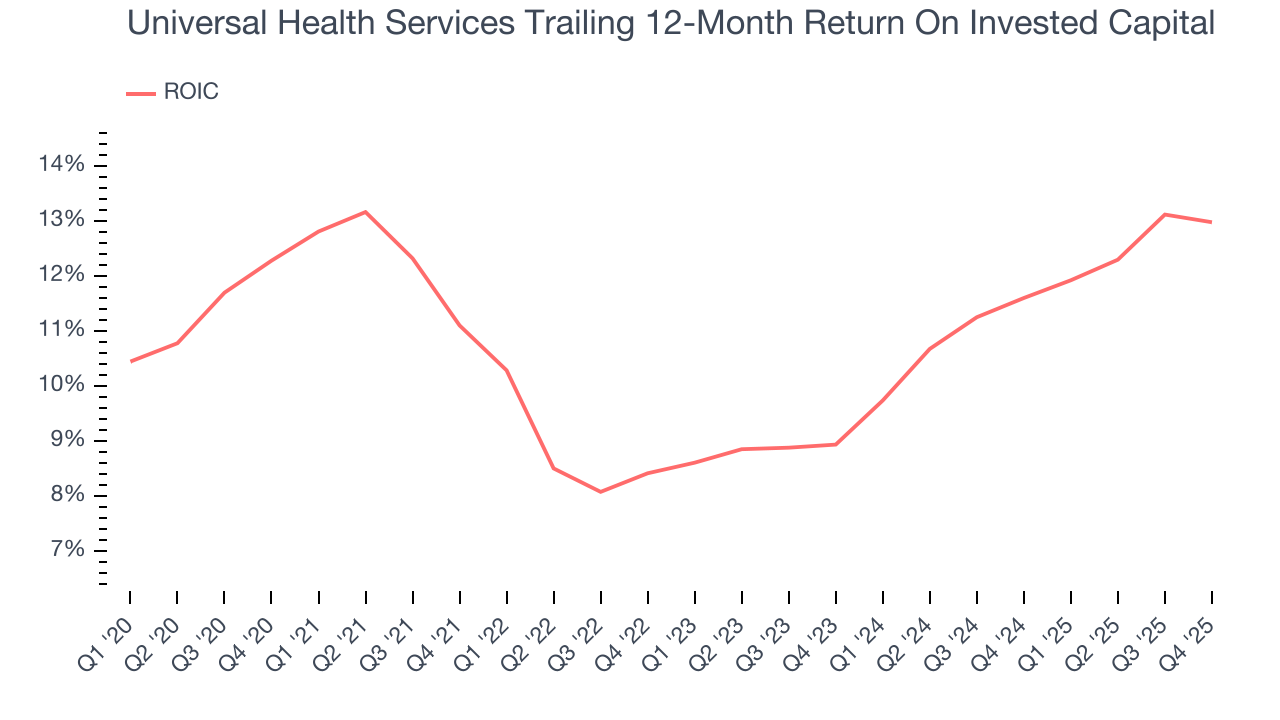

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Universal Health Services’s management team makes decent investment decisions and generates value for shareholders. Its five-year average ROIC was 10.6%, slightly better than typical healthcare business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Over the last few years, Universal Health Services’s ROIC averaged 2.5 percentage point increases each year. This is a great sign when paired with its already strong returns. It could suggest its competitive advantage or profitable growth opportunities are expanding.

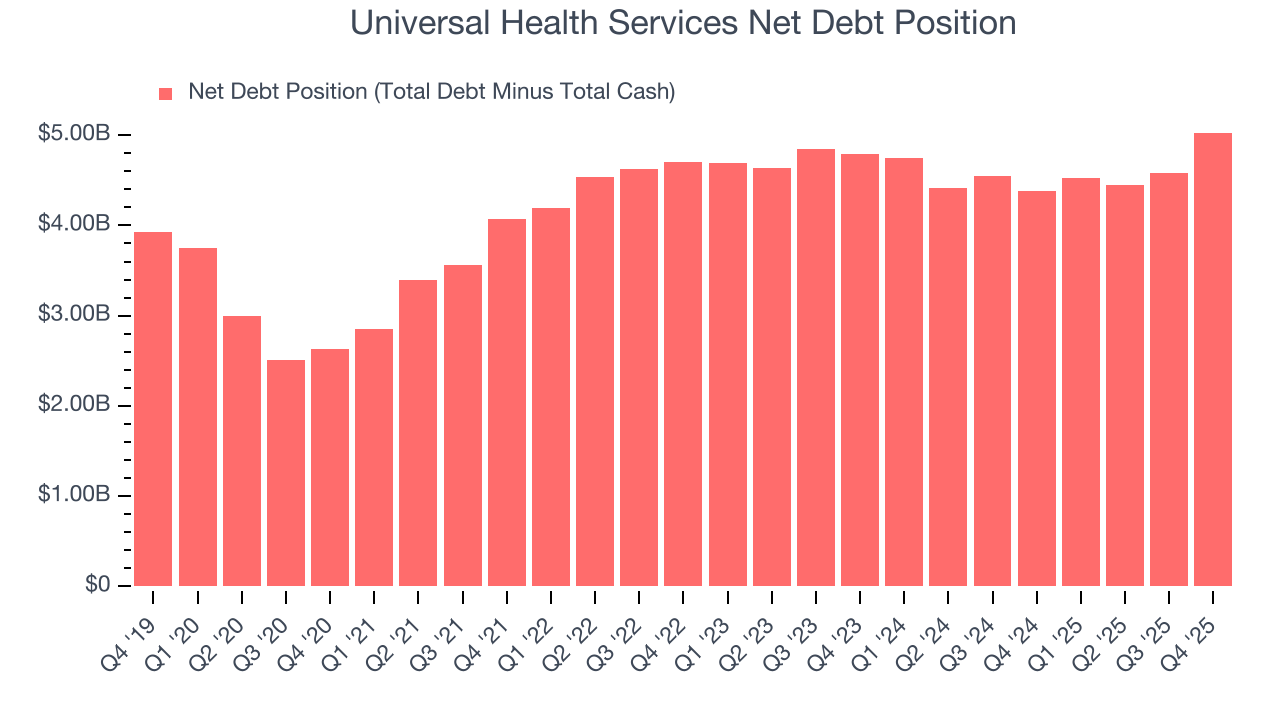

11. Balance Sheet Assessment

Universal Health Services reported $137.8 million of cash and $5.17 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $2.61 billion of EBITDA over the last 12 months, we view Universal Health Services’s 1.9× net-debt-to-EBITDA ratio as safe. We also see its $70.23 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Universal Health Services’s Q4 Results

It was great to see Universal Health Services’s full-year revenue guidance top analysts’ expectations. We were also happy its full-year EPS guidance narrowly outperformed Wall Street’s estimates. On the other hand, its revenue slightly missed and its EPS fell a bit short of Wall Street’s estimates. Overall, this print was mixed but still had some key positives. Investors were likely hoping for more, and shares traded down 1.6% to $227.40 immediately following the results.

13. Is Now The Time To Buy Universal Health Services?

Updated: March 23, 2026 at 12:24 AM EDT

Before investing in or passing on Universal Health Services, we urge you to understand the company’s business quality (or lack thereof), valuation, and the latest quarterly results - in that order.

There are things to like about Universal Health Services. First off, its revenue growth was decent over the last five years. And while its same-store sales growth has disappointed, its spectacular EPS growth over the last five years shows its profits are trickling down to shareholders. On top of that, its rising cash profitability gives it more optionality.

Universal Health Services’s P/E ratio based on the next 12 months is 8x. When scanning the healthcare space, Universal Health Services trades at a fair valuation. If you’re a fan of the business and management team, now is a good time to scoop up some shares.

Wall Street analysts have a consensus one-year price target of $248.76 on the company (compared to the current share price of $186.11), implying they see 33.7% upside in buying Universal Health Services in the short term.