United Parcel Service (UPS)

United Parcel Service faces an uphill battle. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why We Think United Parcel Service Will Underperform

Trademarking its recognizable UPS Brown color, UPS (NYSE:UPS) offers package delivery, supply chain management, and freight forwarding services.

- Customers postponed purchases of its products and services this cycle as its revenue declined by 1.3% annually over the last two years

- Earnings per share fell by 2.7% annually over the last five years while its revenue was flat, showing each sale was less profitable

- Estimated sales for the next 12 months are flat and imply a softer demand environment

United Parcel Service’s quality isn’t up to par. There’s a wealth of better opportunities.

Why There Are Better Opportunities Than United Parcel Service

United Parcel Service’s stock price of $99.65 implies a valuation ratio of 14.5x forward P/E. This multiple is lower than most industrials companies, but for good reason.

Cheap stocks can look like great bargains at first glance, but you often get what you pay for. These mediocre businesses often have less earnings power, meaning there is more reliance on a re-rating to generate good returns - an unlikely scenario for low-quality companies.

3. United Parcel Service (UPS) Research Report: Q4 CY2025 Update

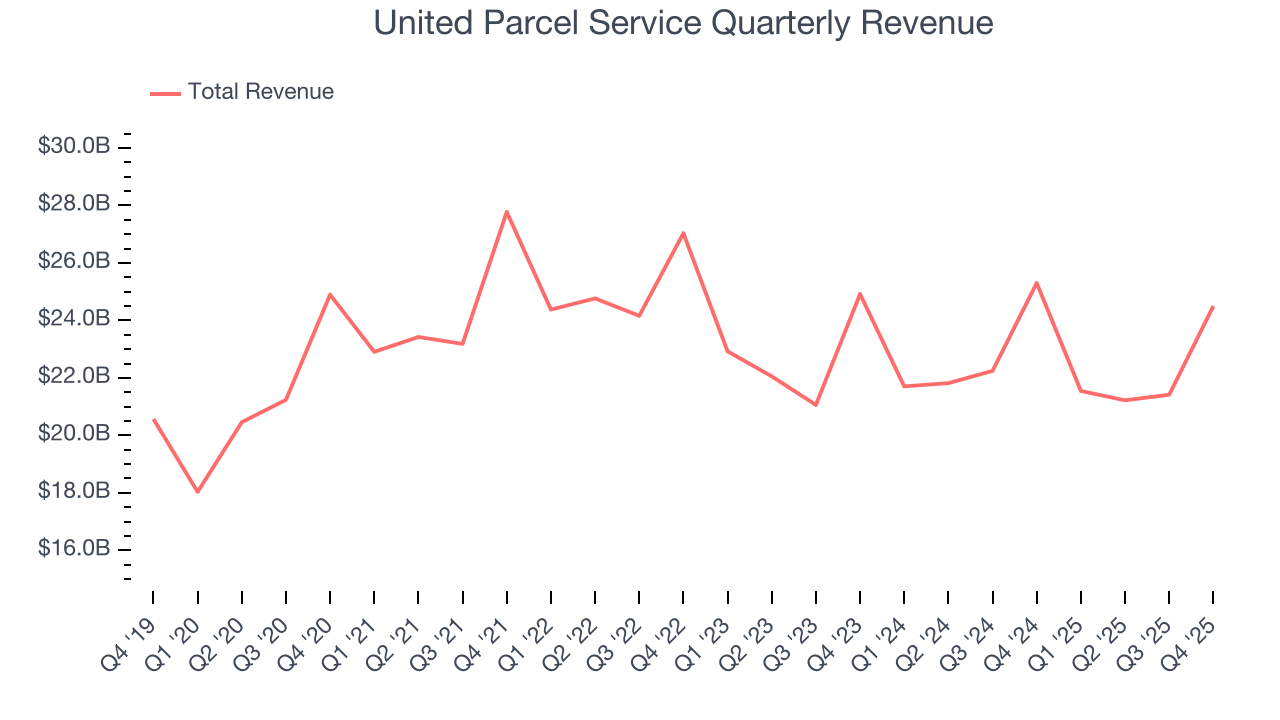

Parcel delivery company UPS (NYSE:UPS) reported revenue ahead of Wall Streets expectations in Q4 CY2025, but sales fell by 3.2% year on year to $24.5 billion. The company’s full-year revenue guidance of $89.7 billion at the midpoint came in 2% above analysts’ estimates. Its non-GAAP profit of $2.38 per share was 8.1% above analysts’ consensus estimates.

United Parcel Service (UPS) Q4 CY2025 Highlights:

- Revenue: $24.5 billion vs analyst estimates of $24.05 billion (3.2% year-on-year decline, 1.9% beat)

- Adjusted EPS: $2.38 vs analyst estimates of $2.20 (8.1% beat)

- Operating Margin: 10.5%, down from 11.6% in the same quarter last year

- Free Cash Flow Margin: 10.6%, up from 8.8% in the same quarter last year

- Market Capitalization: $90.75 billion

Company Overview

Trademarking its recognizable UPS Brown color, UPS (NYSE:UPS) offers package delivery, supply chain management, and freight forwarding services.

UPS was founded in 1907 as a private messenger and delivery service. It was originally named the American Messenger Company, and it started by delivering packages, notes, and luggage by bicycle. Over the decades, UPS grew by acquiring complementary companies like Roadie (enhanced its same-day delivery services) and Cemelog (provided UPS with expertise in handling and transporting sensitive products).

Today, the company provides domestic and international package services through a single pickup and delivery network. This network includes its retail locations, where customers can send and receive packages, and a fleet of trucks and aircraft that fulfill orders. Beyond delivering everyday goods, UPS also handles critical healthcare shipments and manages supply chains for manufacturing companies.

To help customers send, manage, and track shipments, UPS utilizes visibility and billing technologies such as the Digital Access Program which integrates UPS shipping solutions directly into e-commerce platforms, an area of growth. To broaden its e-commerce offerings, UPS acquired Happy Returns in 2023, a technology-focused company that was folded into its Supply Chain Solutions segment.

UPS generates revenue through its package deliveries, freight services, and supply chain services. These offerings provide a mix of transactional (one-time shipments) and contractual revenue streams. On the contractual side, UPS has agreements with businesses that include scheduled pickups and volume-based pricing. The company offers different price points depending on the size and speed of its deliveries.

4. Air Freight and Logistics

The growth of e-commerce and global trade continues to drive demand for expedited shipping services, presenting opportunities for air freight companies. The industry continues to invest in advanced technologies such as automated sorting systems and real-time tracking solutions to enhance operational efficiency. Despite the advantages of speed and global reach, air freight and logistics companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Competitors offering similar products include FedEx (NYSE:FDX), GXO (NYSE:GXO), and Amazon (NASDAQ:AMZN).

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Unfortunately, United Parcel Service struggled to consistently increase demand as its $88.68 billion of sales for the trailing 12 months was close to its revenue five years ago. This was below our standards and suggests it’s a low quality business.

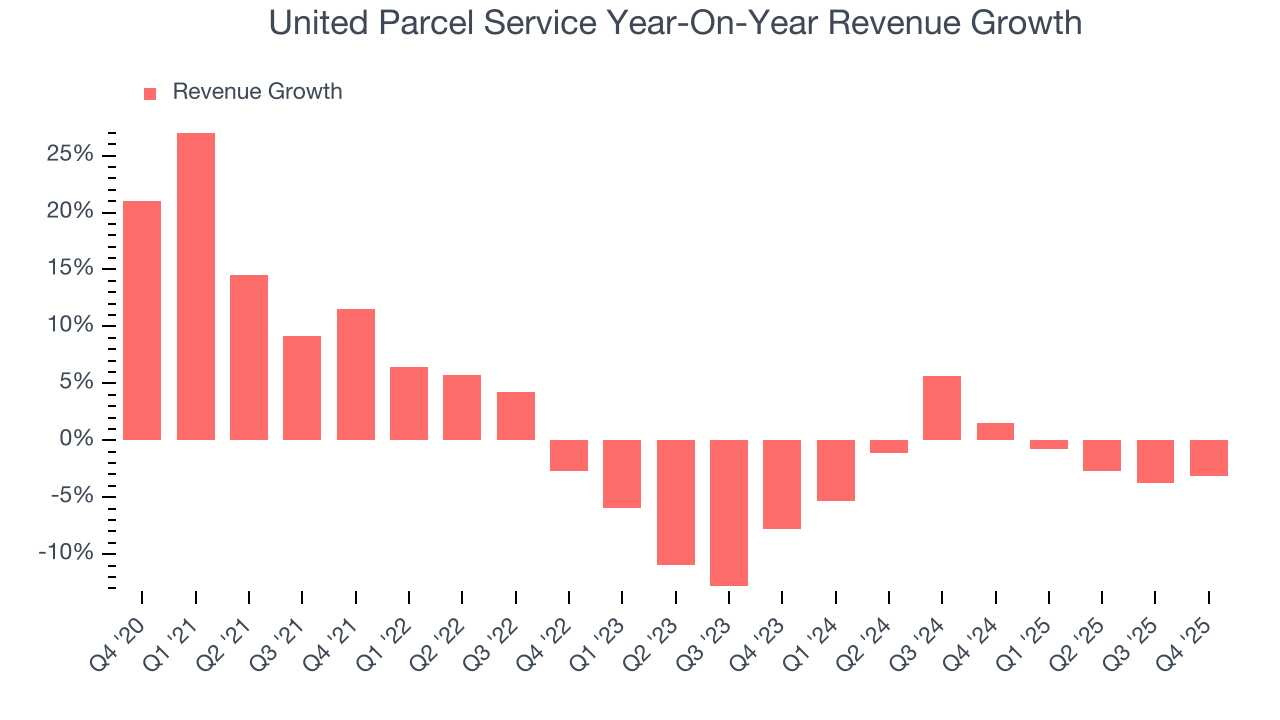

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. United Parcel Service’s recent performance shows its demand remained suppressed as its revenue has declined by 1.3% annually over the last two years. United Parcel Service isn’t alone in its struggles as the Air Freight and Logistics industry experienced a cyclical downturn, with many similar businesses observing lower sales at this time.

This quarter, United Parcel Service’s revenue fell by 3.2% year on year to $24.5 billion but beat Wall Street’s estimates by 1.9%.

Looking ahead, sell-side analysts expect revenue to decline by 1% over the next 12 months, similar to its two-year rate. This projection doesn't excite us and indicates its newer products and services will not lead to better top-line performance yet.

6. Gross Margin & Pricing Power

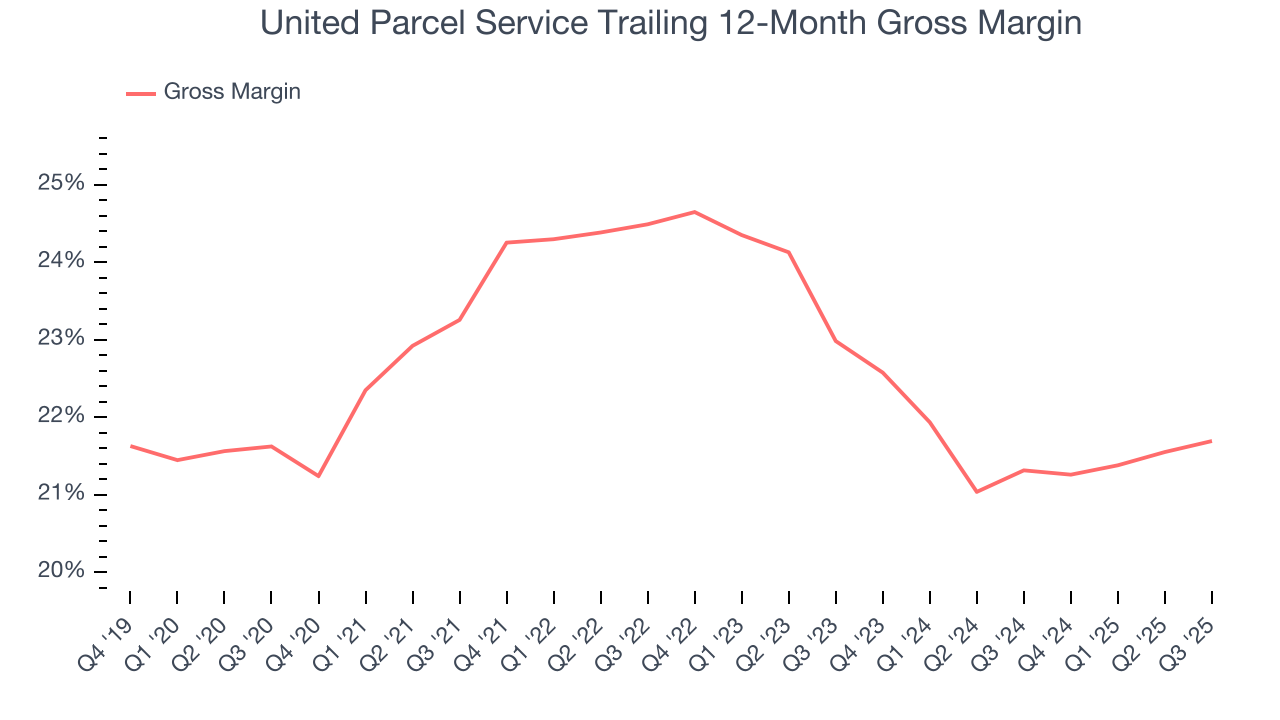

United Parcel Service has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 23.1% gross margin over the last five years. Said differently, United Parcel Service had to pay a chunky $76.92 to its suppliers for every $100 in revenue.

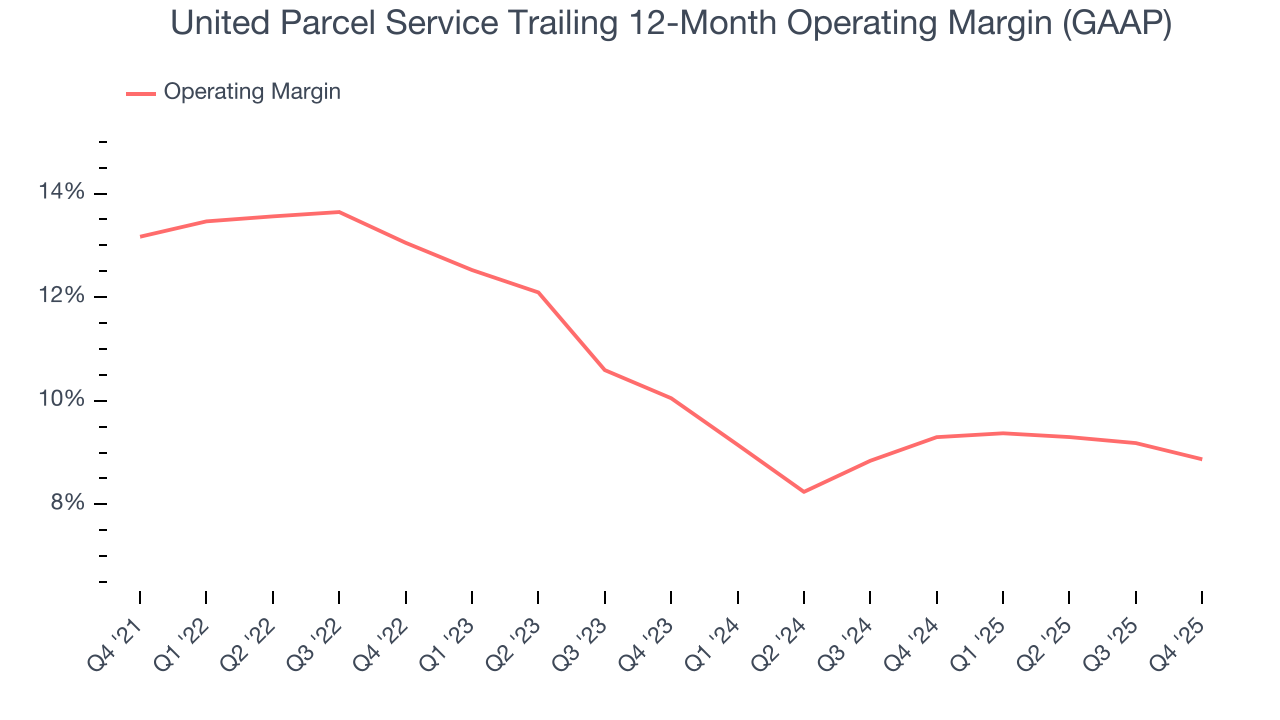

7. Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

United Parcel Service has managed its cost base well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Analyzing the trend in its profitability, United Parcel Service’s operating margin decreased by 4.3 percentage points over the last five years. Many Air Freight and Logistics companies also saw their margins fall (along with revenue, as mentioned above) because the cycle turned in the wrong direction. We hope United Parcel Service can emerge from this a stronger company, as the silver lining of a downturn is that market share can be won and efficiencies found.

This quarter, United Parcel Service generated an operating margin profit margin of 10.5%, down 1.1 percentage points year on year. The reduction is quite minuscule and shareholders shouldn’t weigh the results too heavily.

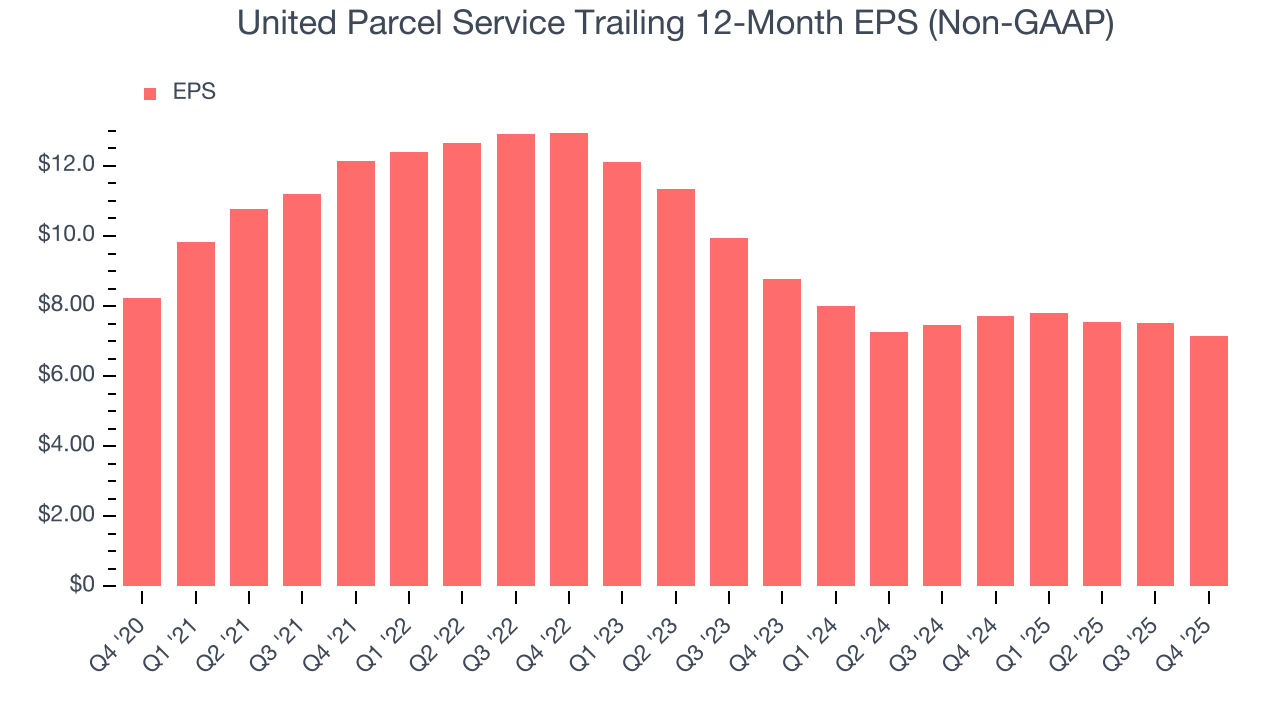

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Sadly for United Parcel Service, its EPS declined by 2.7% annually over the last five years while its revenue was flat. We can see the difference stemmed from higher taxes as the company actually improved its operating margin and repurchased its shares during this time.

We can take a deeper look into United Parcel Service’s earnings to better understand the drivers of its performance. As we mentioned earlier, United Parcel Service’s operating margin declined by 4.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; interest expenses and taxes can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For United Parcel Service, its two-year annual EPS declines of 9.7% show it’s continued to underperform. These results were bad no matter how you slice the data.

In Q4, United Parcel Service reported adjusted EPS of $2.38, down from $2.75 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 8.1%. Over the next 12 months, Wall Street expects United Parcel Service’s full-year EPS of $7.16 to shrink by 1.7%.

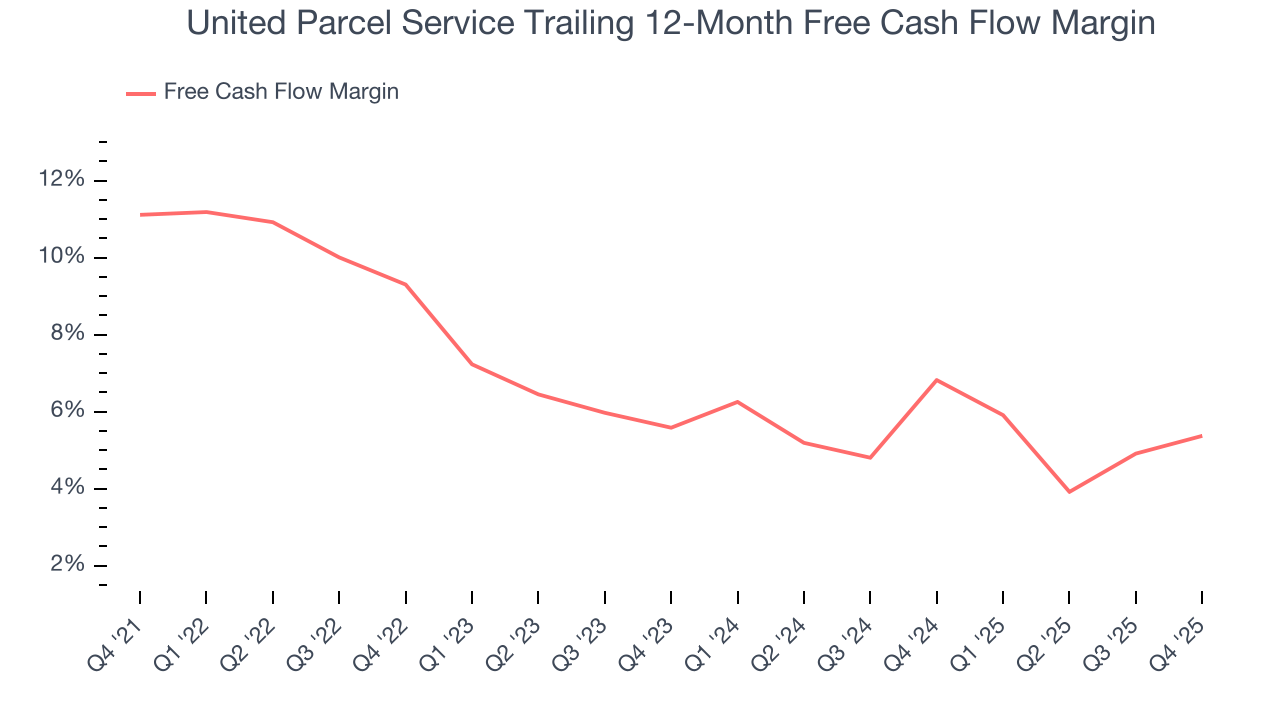

9. Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

United Parcel Service has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 7.7% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that United Parcel Service’s margin dropped by 5.7 percentage points during that time. If its declines continue, it could signal increasing investment needs and capital intensity.

United Parcel Service’s free cash flow clocked in at $2.59 billion in Q4, equivalent to a 10.6% margin. This result was good as its margin was 1.8 percentage points higher than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, leading to temporary swings. Long-term trends are more important.

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although United Parcel Service hasn’t been the highest-quality company lately because of its poor revenue and EPS performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 31.5%, splendid for an industrials business.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Unfortunately, United Parcel Service’s ROIC has decreased significantly over the last few years. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

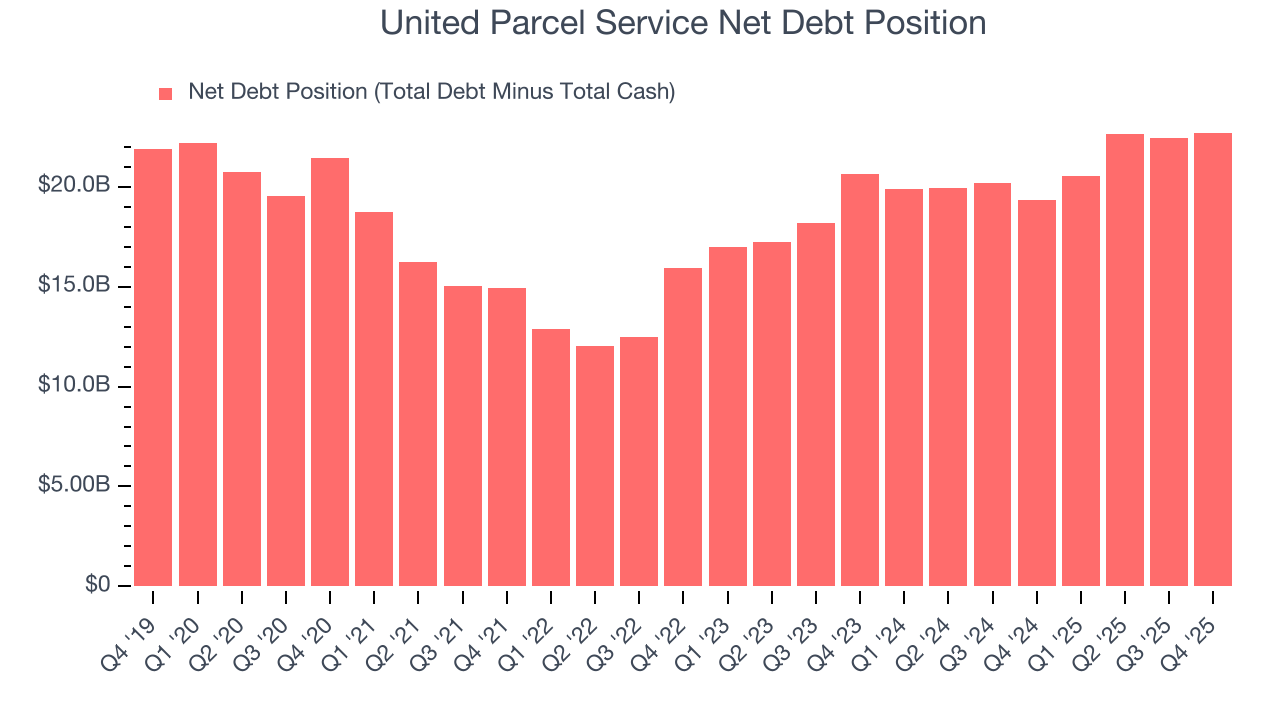

11. Balance Sheet Assessment

United Parcel Service reported $5.89 billion of cash and $28.59 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $12.41 billion of EBITDA over the last 12 months, we view United Parcel Service’s 1.8× net-debt-to-EBITDA ratio as safe. We also see its $375 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from United Parcel Service’s Q4 Results

It was great to see United Parcel Service’s full-year revenue guidance top analysts’ expectations. We were also glad its revenue outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 3.8% to $111.07 immediately following the results.

13. Is Now The Time To Buy United Parcel Service?

Updated: March 10, 2026 at 12:11 AM EDT

Before deciding whether to buy United Parcel Service or pass, we urge investors to consider business quality, valuation, and the latest quarterly results.

United Parcel Service falls short of our quality standards. To kick things off, its revenue growth was weak over the last five years, and analysts don’t see anything changing over the next 12 months. While its stellar ROIC suggests it has been a well-run company historically, the downside is its diminishing returns show management's prior bets haven't worked out. On top of that, its projected EPS for the next year is lacking.

United Parcel Service’s P/E ratio based on the next 12 months is 14.5x. This valuation is reasonable, but the company’s shaky fundamentals present too much downside risk. There are better stocks to buy right now.

Wall Street analysts have a consensus one-year price target of $113.07 on the company (compared to the current share price of $99.65).