Vulcan Materials (VMC)

Vulcan Materials doesn’t excite us. Its underwhelming returns on capital show it struggled to generate meaningful profits for shareholders.― StockStory Analyst Team

1. News

2. Summary

Why Vulcan Materials Is Not Exciting

Founded in 1909, Vulcan Materials (NYSE:VMC) is a producer of construction aggregates, primarily crushed stone, sand, and gravel.

- Sluggish trends in its tons shipped suggest customers aren’t adopting its solutions as quickly as the company hoped

- Estimated sales growth of 4.3% for the next 12 months is soft and implies weaker demand

- A bright spot is that its healthy operating margin shows it’s a well-run company with efficient processes, and it turbocharged its profits by achieving some fixed cost leverage

Vulcan Materials doesn’t check our boxes. We believe there are better businesses elsewhere.

Why There Are Better Opportunities Than Vulcan Materials

Vulcan Materials is trading at $326.01 per share, or 34.9x forward P/E. This multiple is higher than that of industrials peers; it’s also rich for the business quality. Not a great combination.

There are stocks out there similarly priced with better business quality. We prefer owning these.

3. Vulcan Materials (VMC) Research Report: Q4 CY2025 Update

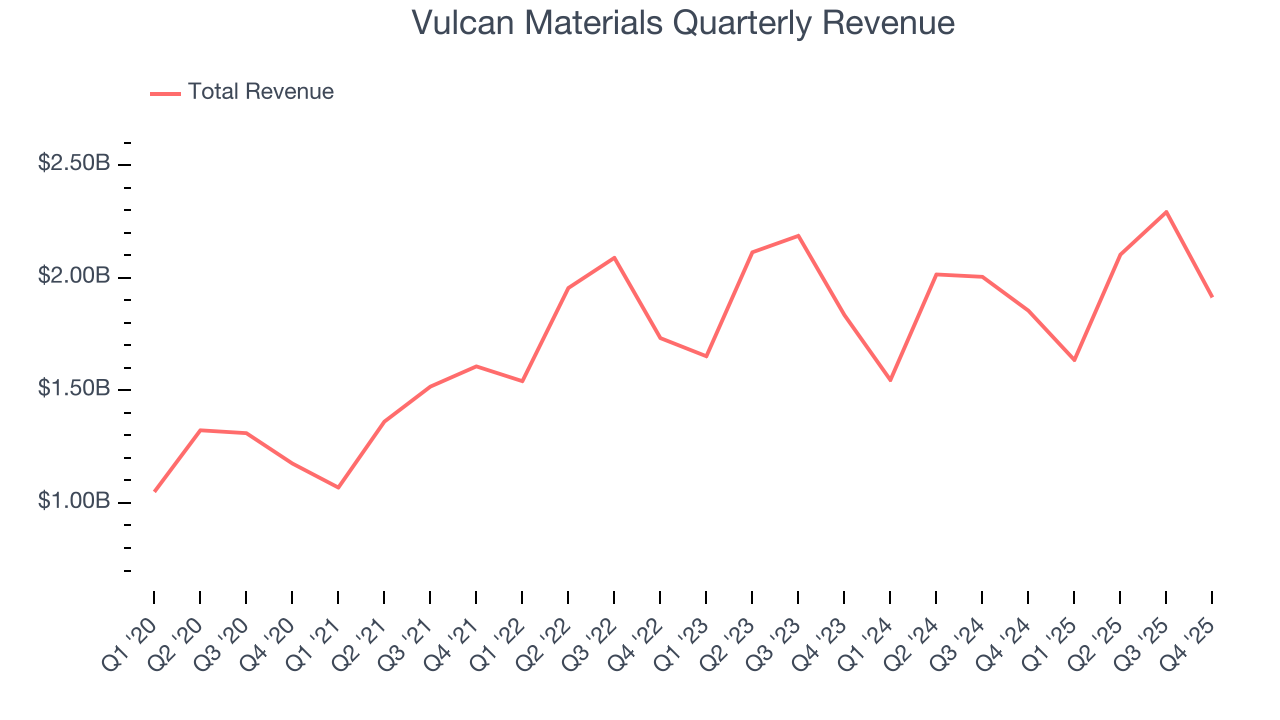

Construction materials company Vulcan Materials (NYSE:VMC) missed Wall Street’s revenue expectations in Q4 CY2025 as sales rose 3.2% year on year to $1.91 billion. Its non-GAAP profit of $1.70 per share was 19.5% below analysts’ consensus estimates.

Vulcan Materials (VMC) Q4 CY2025 Highlights:

- Revenue: $1.91 billion vs analyst estimates of $1.94 billion (3.2% year-on-year growth, 1.7% miss)

- Adjusted EPS: $1.70 vs analyst expectations of $2.11 (19.5% miss)

- Adjusted EBITDA: $518 million vs analyst estimates of $603.8 million (27.1% margin, 14.2% miss)

- EBITDA guidance for the upcoming financial year 2026 is $2.5 billion at the midpoint, below analyst estimates of $2.65 billion

- Operating Margin: 19.8%, down from 21.6% in the same quarter last year

- Free Cash Flow Margin: 18.7%, up from 15% in the same quarter last year

- Tons Shipped: 55.1 million, up 1.2 million year on year

- Market Capitalization: $43.29 billion

Company Overview

Founded in 1909, Vulcan Materials (NYSE:VMC) is a producer of construction aggregates, primarily crushed stone, sand, and gravel.

Vulcan Materials was established as the Birmingham Slag Company initially producing construction aggregates through the processing of slag from steel mills. The company expanded over the decades by acquiring numerous aggregates-related businesses, ultimately changing its name to Vulcan Materials in 1956 to reflect its growing range of construction material products.

Today, Vulcan Materials is a supplier of essential construction materials, particularly focusing on products used in building critical infrastructure like roads, bridges, and airports, as well as various community facilities such as hospitals and schools. The company’s offerings encompass construction aggregates, including gravel, sand, and crushed stone, vital for foundational and structural projects. Vulcan also provides asphalt and ready-mixed concrete, essential for numerous construction applications from paving highways to constructing commercial buildings. Additionally, Vulcan's produces calcium carbonate used in animal feed, plastics, and water treatment industries.

Vulcan Materials generates revenue through the sale of construction aggregates, asphalt, concrete, and calcium products primarily in the United States. Their revenue streams are bolstered by a combination of direct sales to construction companies, infrastructure projects, and through distribution channels that include retailers and wholesalers.

Vulcan serves a diverse customer base in both public and private sectors. The demand for their products is influenced by long-term factors such as population growth, infrastructure investment, and economic cycles. In the public sector, projects like highways and bridges provide steady demand due to consistent government funding, making it less susceptible to economic fluctuations compared to the private sector. Private sector demand, covering residential and nonresidential construction, varies more with the economic climate, driven by factors like job growth, demographic trends, and the availability of financing. Overall, Vulcan's market positioning allows it to capitalize on long-term growth trends in regions with rising construction needs.

4. Building Materials

Traditionally, building materials companies have built competitive advantages with economies of scale, brand recognition, and strong relationships with builders and contractors. More recently, advances to address labor availability and job site productivity have spurred innovation. Additionally, companies in the space that can produce more energy-efficient materials have opportunities to take share. However, these companies are at the whim of construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of building materials companies.

Competitors in the construction materials industry include Martin Marietta (NYSE:MLM), Eagle Materials (NYSE:EXP), and CEMEX (NYSE:CX)

5. Revenue Growth

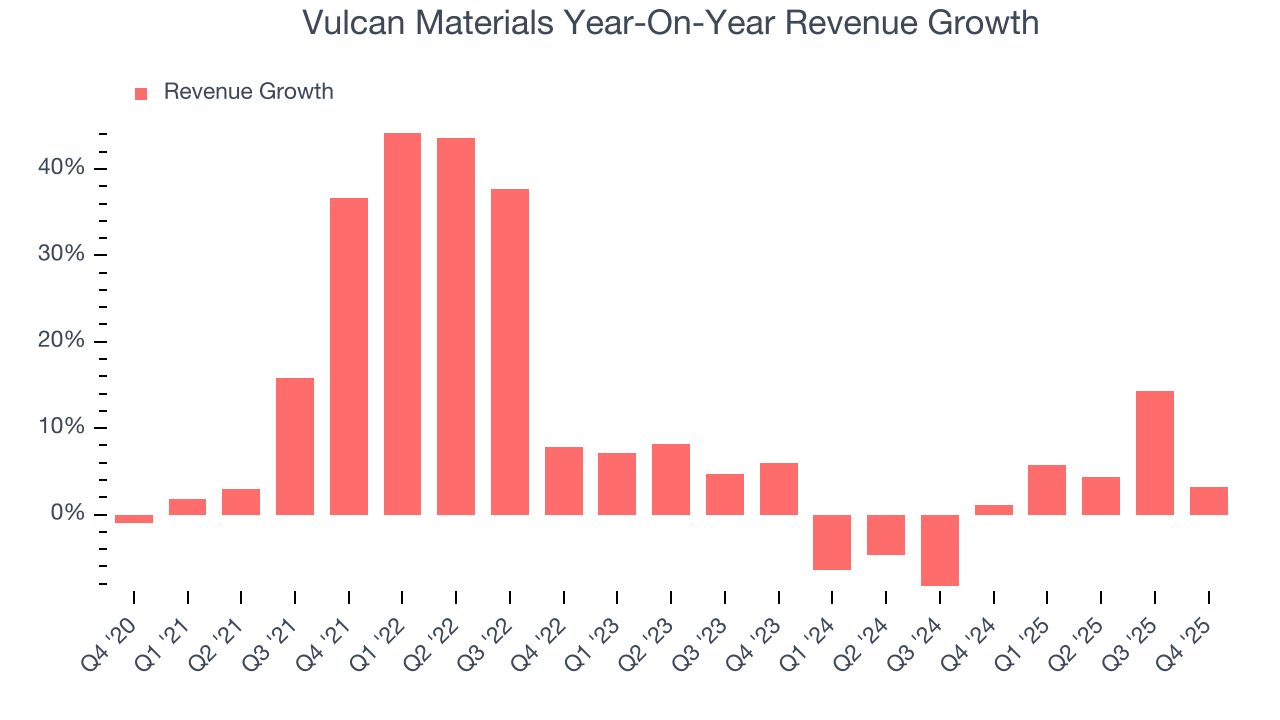

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Vulcan Materials’s 10.3% annualized revenue growth over the last five years was solid. Its growth beat the average industrials company and shows its offerings resonate with customers.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Vulcan Materials’s recent performance shows its demand has slowed as its annualized revenue growth of 1% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs.

We can better understand the company’s revenue dynamics by analyzing its number of tons shipped, which reached 55.1 million in the latest quarter. Over the last two years, Vulcan Materials’s tons shipped averaged 2% year-on-year growth. Because this number aligns with its revenue growth during the same period, we can see the company’s monetization was fairly consistent.

This quarter, Vulcan Materials’s revenue grew by 3.2% year on year to $1.91 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 5% over the next 12 months. While this projection indicates its newer products and services will catalyze better top-line performance, it is still below average for the sector.

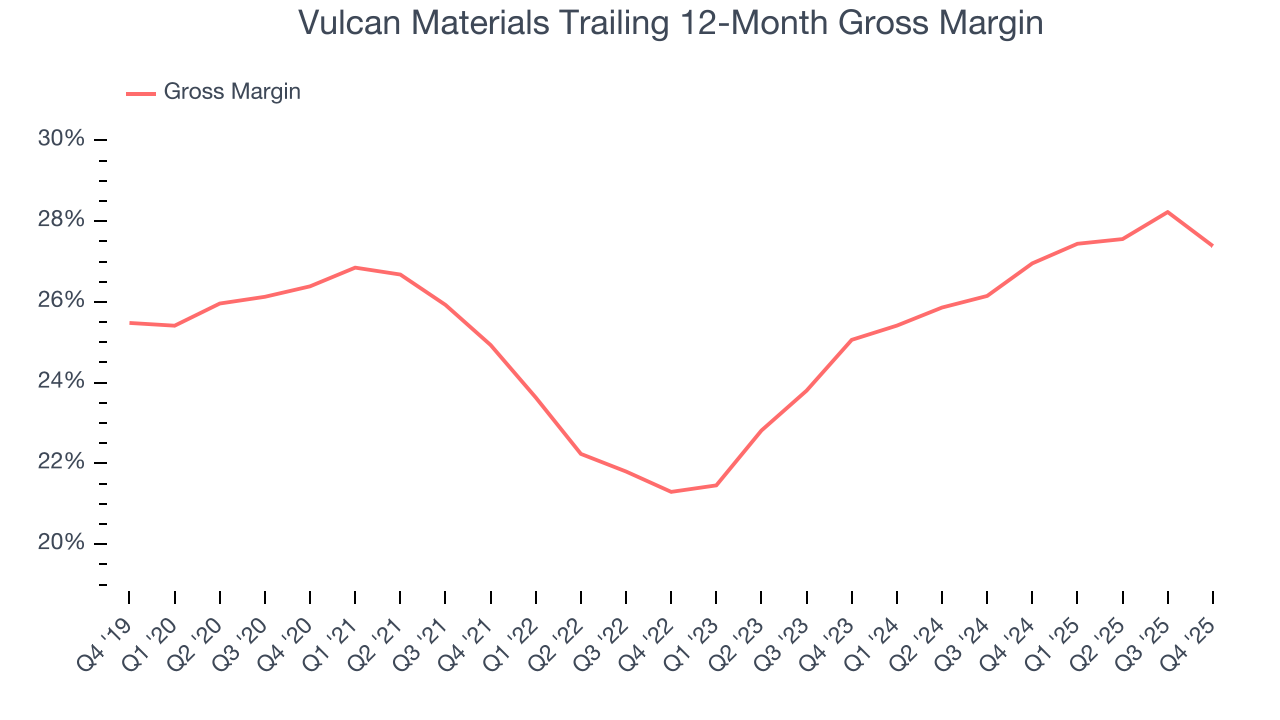

6. Gross Margin & Pricing Power

All else equal, we prefer higher gross margins because they make it easier to generate more operating profits and indicate that a company commands pricing power by offering more differentiated products.

Vulcan Materials has bad unit economics for an industrials company, giving it less room to reinvest and develop new offerings. As you can see below, it averaged a 25.2% gross margin over the last five years. That means Vulcan Materials paid its suppliers a lot of money ($74.82 for every $100 in revenue) to run its business.

This quarter, Vulcan Materials’s gross profit margin was 25.5% , marking a 3.5 percentage point decrease from 29% in the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs (such as raw materials and manufacturing expenses) have been stable and it isn’t under pressure to lower prices.

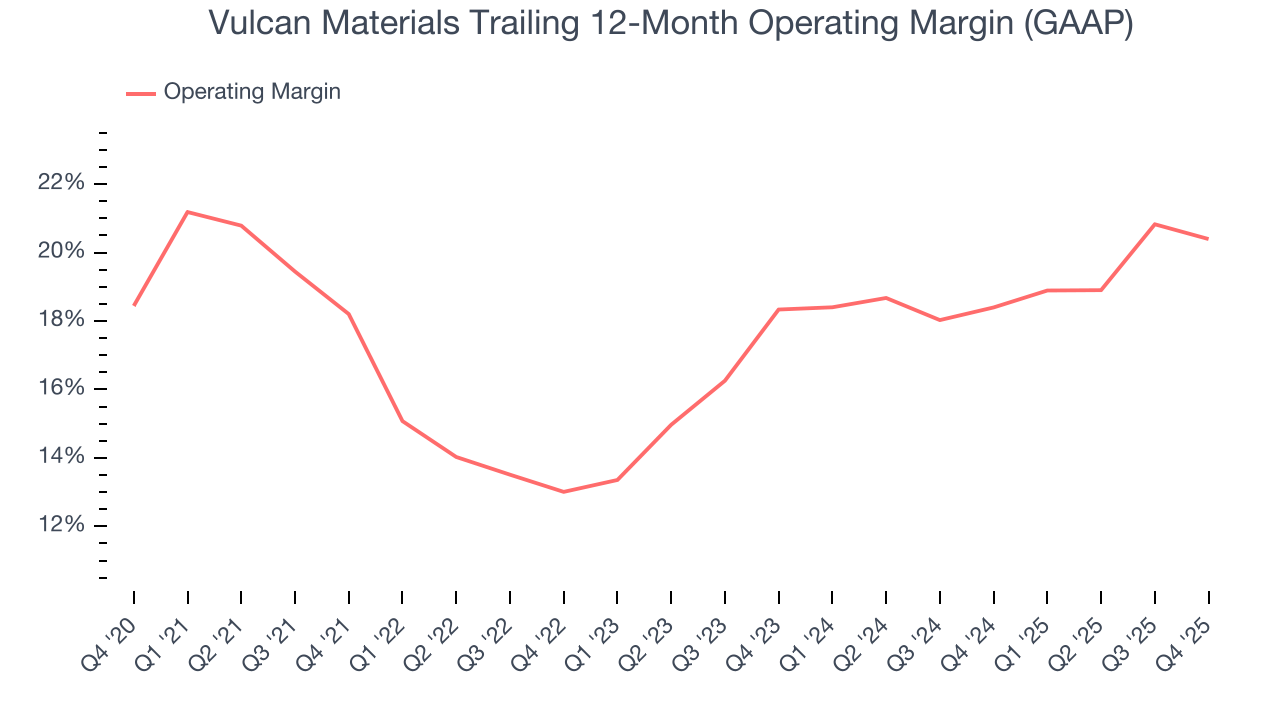

7. Operating Margin

Vulcan Materials has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 17.7%. This result was particularly impressive because of its low gross margin, which is mostly a factor of what it sells and takes huge shifts to move meaningfully. Companies have more control over their operating margins, and it’s a show of well-managed operations if they’re high when gross margins are low.

Looking at the trend in its profitability, Vulcan Materials’s operating margin rose by 2.2 percentage points over the last five years, as its sales growth gave it operating leverage.

In Q4, Vulcan Materials generated an operating margin profit margin of 19.8%, down 1.8 percentage points year on year. Since Vulcan Materials’s gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased marketing, R&D, and administrative overhead expenses.

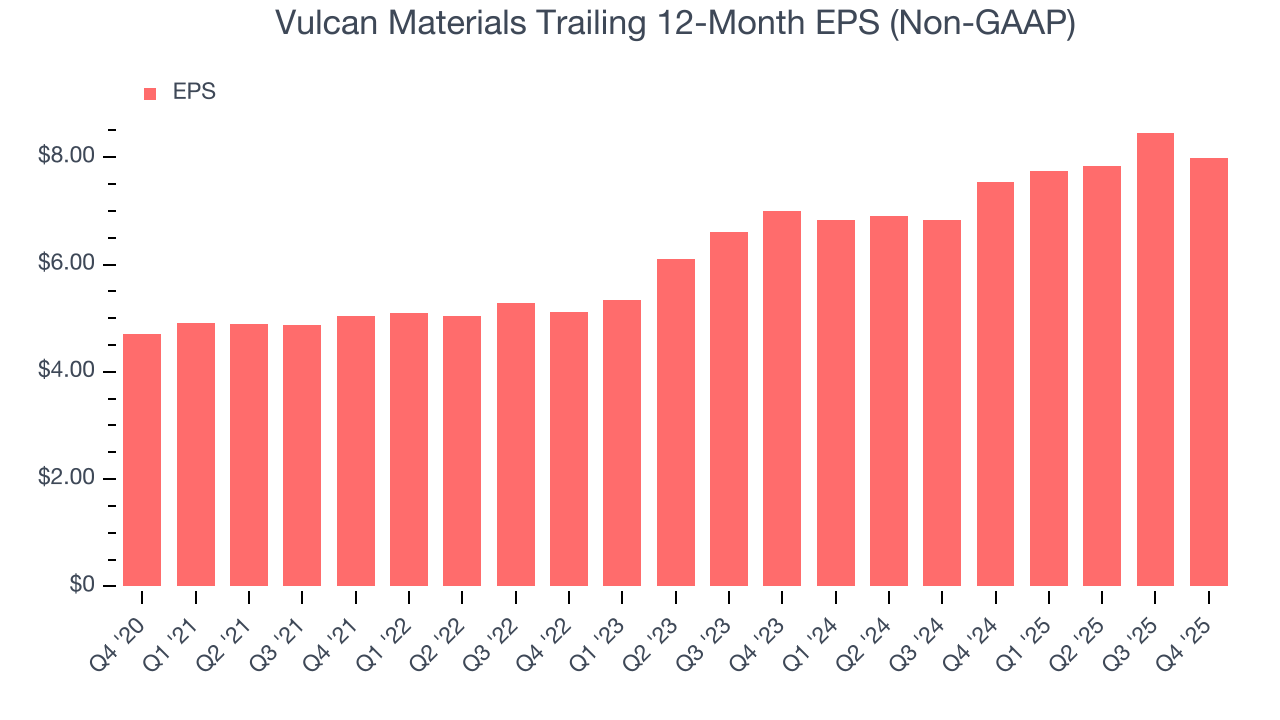

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Vulcan Materials’s solid 11.2% annual EPS growth over the last five years aligns with its revenue performance. This tells us its incremental sales were profitable.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

Although it wasn’t great, Vulcan Materials’s two-year annual EPS growth of 6.9% topped its 1% two-year revenue growth.

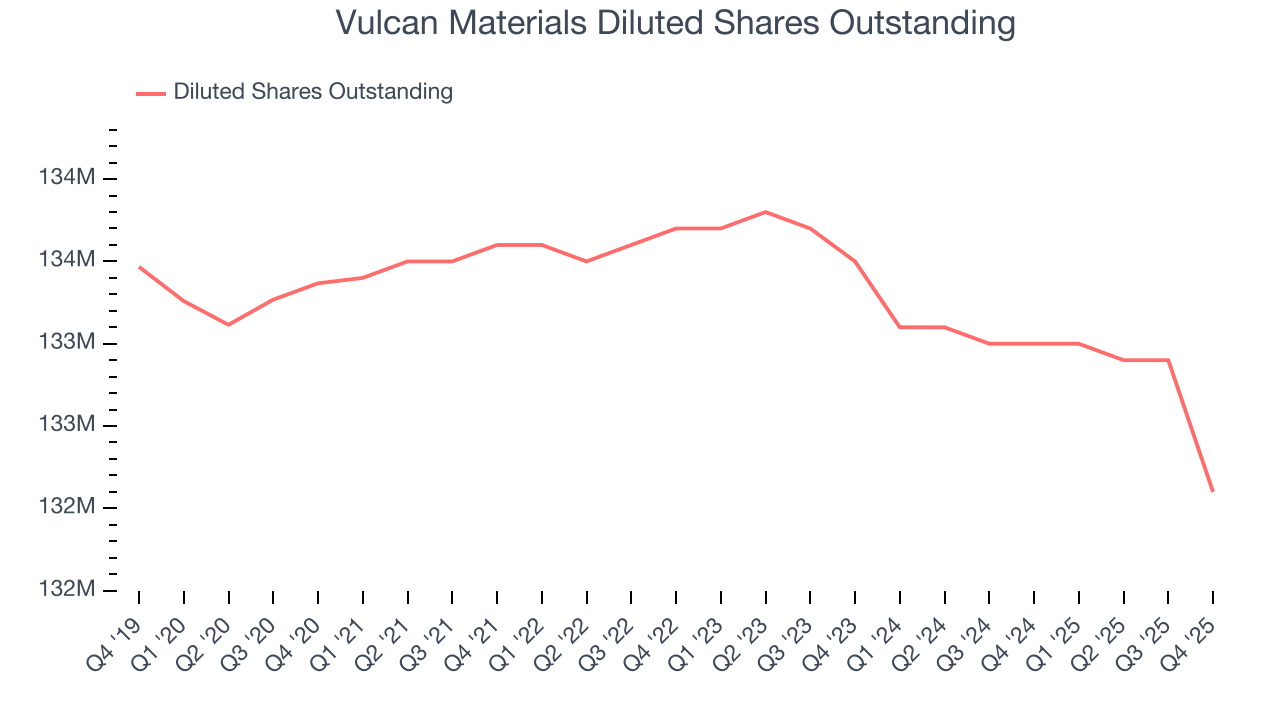

We can take a deeper look into Vulcan Materials’s earnings to better understand the drivers of its performance. A two-year view shows that Vulcan Materials has repurchased its stock, shrinking its share count by 1%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Vulcan Materials reported adjusted EPS of $1.70, down from $2.17 in the same quarter last year. This print missed analysts’ estimates, but we care more about long-term adjusted EPS growth than short-term movements. Over the next 12 months, Wall Street expects Vulcan Materials’s full-year EPS of $7.99 to grow 22%.

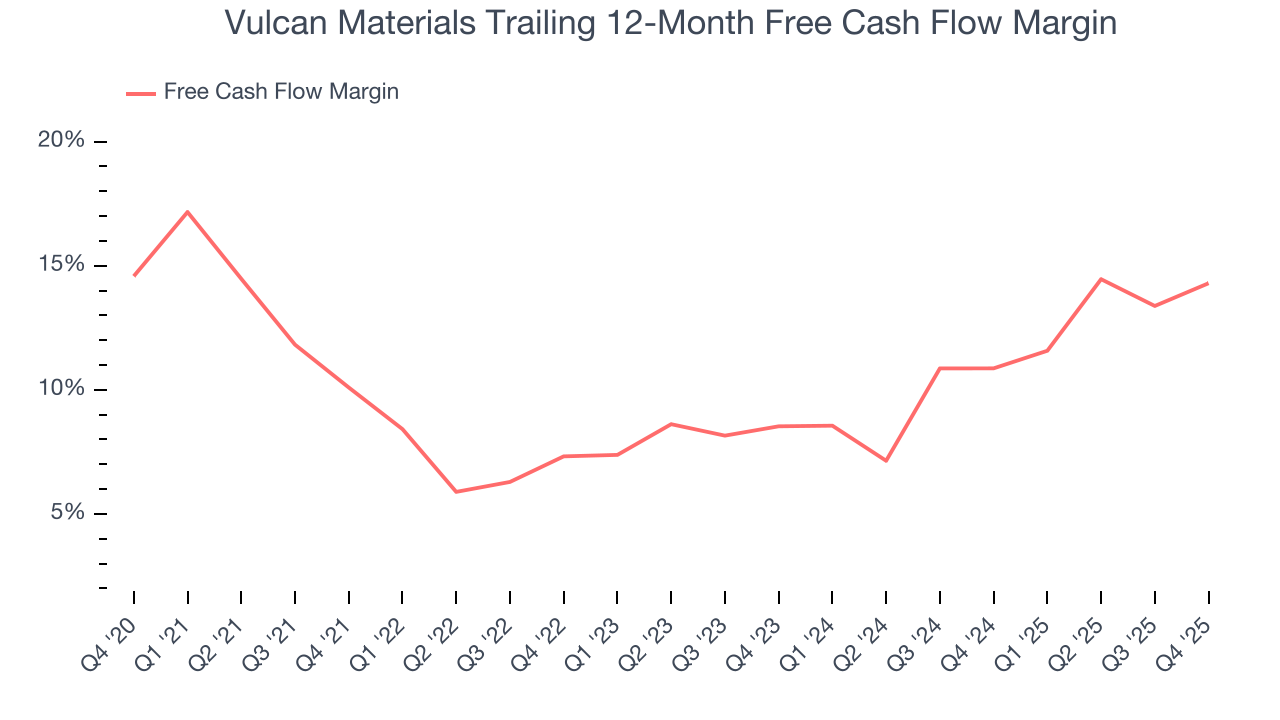

9. Cash Is King

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Vulcan Materials has shown robust cash profitability, enabling it to comfortably ride out cyclical downturns while investing in plenty of new offerings and returning capital to investors. The company’s free cash flow margin averaged 10.3% over the last five years, quite impressive for an industrials business.

Taking a step back, we can see that Vulcan Materials’s margin expanded by 4.2 percentage points during that time. This shows the company is heading in the right direction, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability.

Vulcan Materials’s free cash flow clocked in at $358.2 million in Q4, equivalent to a 18.7% margin. This result was good as its margin was 3.8 percentage points higher than in the same quarter last year, building on its favorable historical trend.

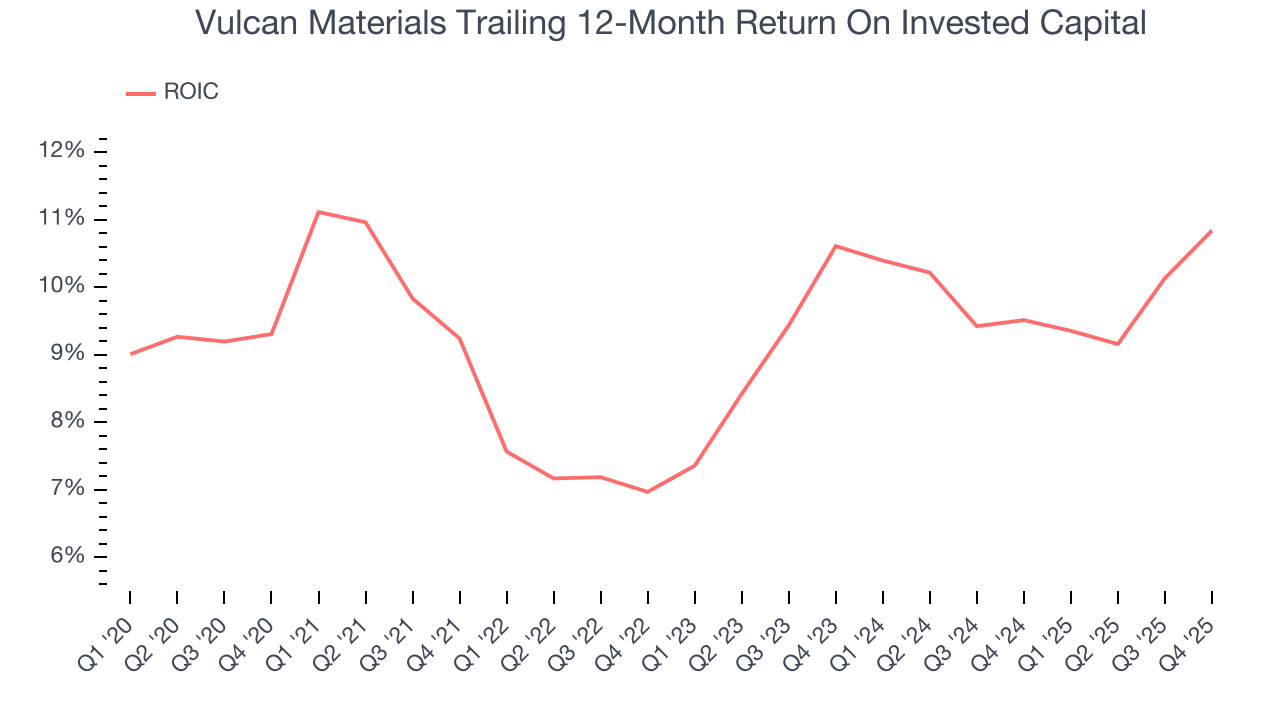

10. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Vulcan Materials historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 9.4%, somewhat low compared to the best industrials companies that consistently pump out 20%+.

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. Fortunately, Vulcan Materials’s ROIC averaged 2.1 percentage point increases each year over the last few years. This is a good sign, and if its returns keep rising, there’s a chance it could evolve into an investable business.

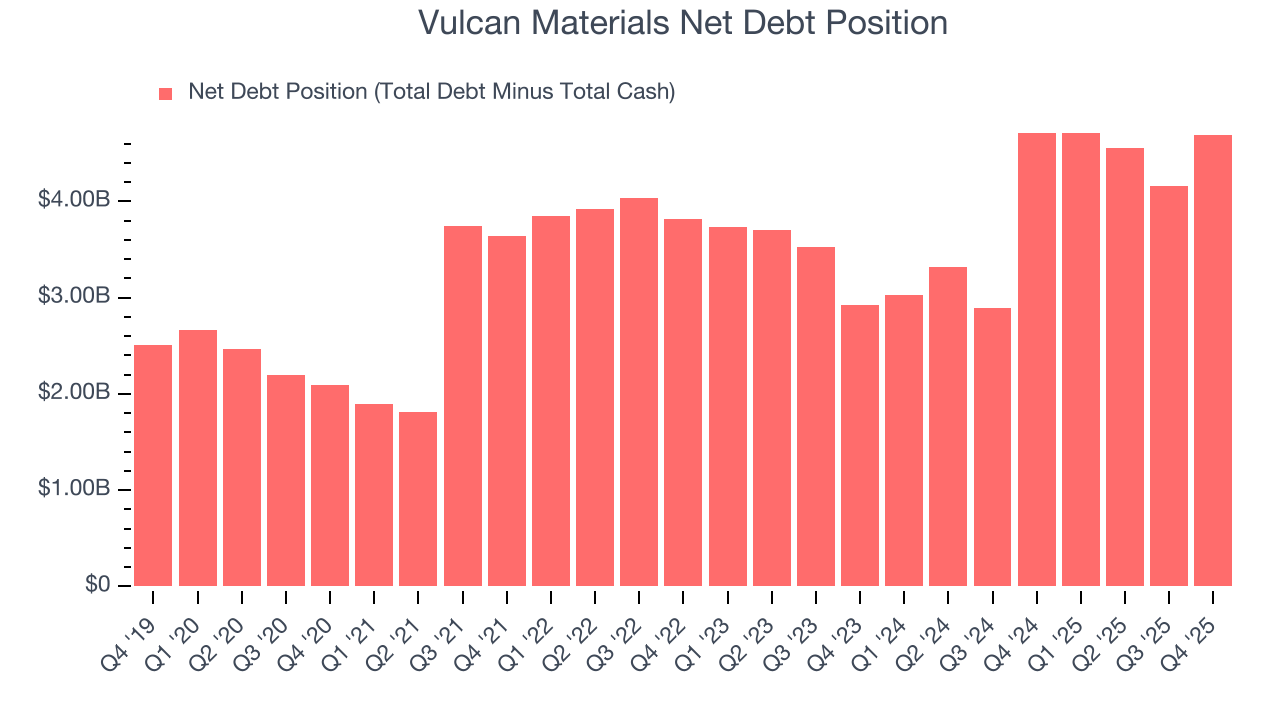

11. Balance Sheet Assessment

Vulcan Materials reported $189.4 million of cash and $4.88 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $2.32 billion of EBITDA over the last 12 months, we view Vulcan Materials’s 2.0× net-debt-to-EBITDA ratio as safe. We also see its $226.3 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

12. Key Takeaways from Vulcan Materials’s Q4 Results

We struggled to find many positives in these results. Its full-year EBITDA guidance missed and its EBITDA fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 7.6% to $302.89 immediately following the results.

13. Is Now The Time To Buy Vulcan Materials?

Updated: February 17, 2026 at 7:19 AM EST

We think that the latest earnings result is only one piece of the bigger puzzle. If you’re deciding whether to own Vulcan Materials, you should also grasp the company’s longer-term business quality and valuation.

When it comes to Vulcan Materials’s business quality, there are some positives, but it ultimately falls short. To kick things off, its revenue growth was solid over the last five years. And while Vulcan Materials’s gross margins are lower than its industrials peers, its impressive operating margins show it has a highly efficient business model.

Vulcan Materials’s P/E ratio based on the next 12 months is 33.6x. At this valuation, there’s a lot of good news priced in - we think other companies feature superior fundamentals at the moment.

Wall Street analysts have a consensus one-year price target of $328.57 on the company (compared to the current share price of $302.89).