Voya Financial (VOYA)

Voya Financial doesn’t excite us. Its sluggish sales growth shows demand is soft, a worrisome sign for investors in high-quality stocks.― StockStory Analyst Team

1. News

2. Summary

Why Voya Financial Is Not Exciting

Originally spun off from Dutch financial giant ING in 2013 and rebranded with a name suggesting "voyage," Voya Financial (NYSE:VOYA) provides workplace benefits and savings solutions to U.S. employers, helping their employees achieve better financial outcomes through retirement plans and insurance products.

- Annual tangible book value per share declines of 14.6% for the past five years show its capital management struggled during this cycle

- Muted 6.8% annual revenue growth over the last five years shows its demand lagged behind its financials peers

- One positive is that its performance over the past five years shows its incremental sales were extremely profitable, as its annual earnings per share growth of 29.3% outpaced its revenue gains

Voya Financial doesn’t check our boxes. You should search for better opportunities.

Why There Are Better Opportunities Than Voya Financial

At $76.16 per share, Voya Financial trades at 8x forward P/E. Voya Financial’s valuation may seem like a bargain, but we think there are valid reasons why it’s so cheap.

Our advice is to pay up for elite businesses whose advantages are tailwinds to earnings growth. Don’t get sucked into lower-quality businesses just because they seem like bargains. These mediocre businesses often never achieve a higher multiple as hoped, a phenomenon known as a “value trap”.

3. Voya Financial (VOYA) Research Report: Q3 CY2025 Update

Financial services company Voya Financial (NYSE:VOYA) beat Wall Street’s revenue expectations in Q3 CY2025, with sales up 14% year on year to $2.13 billion. Its non-GAAP profit of $2.45 per share was 8.9% above analysts’ consensus estimates.

Voya Financial (VOYA) Q3 CY2025 Highlights:

Company Overview

Originally spun off from Dutch financial giant ING in 2013 and rebranded with a name suggesting "voyage," Voya Financial (NYSE:VOYA) provides workplace benefits and savings solutions to U.S. employers, helping their employees achieve better financial outcomes through retirement plans and insurance products.

Voya operates through three main segments: Wealth Solutions, Health Solutions, and Investment Management. The Wealth Solutions segment offers retirement plan administration for approximately 38,000 employers and 7 million plan participants across all market segments, from small businesses to large corporations. This includes recordkeeping services, investment options, and financial guidance tools. The company's myVoyage mobile application helps employees visualize their entire financial picture and engage with their workplace benefits.

The Health Solutions segment provides supplemental health and group benefits covering over 7 million individuals, including stop-loss insurance for self-insured employers, group life insurance, disability coverage, and voluntary benefits like critical illness and accident insurance. Through its 2023 acquisition of Benefitfocus, Voya also offers benefits administration technology that serves approximately 12 million employees, helping them select and manage their workplace benefits through an open-architecture platform.

The Investment Management segment manages assets for both institutional and retail clients globally. It offers fixed income, equity, and alternative investment strategies, with particular strength in private assets like private fixed income and secondary private equity. Following a 2022 transaction with Allianz Global Investors, Voya expanded its international distribution capabilities, particularly in Europe and Asia.

Voya generates revenue through a mix of fee income from asset and participant-based services, premium income from insurance products, and investment income from its general account assets. For employers, Voya's integrated platform helps maximize the value of benefits spending while promoting a healthier and more financially secure workforce. For employees, the company's solutions aim to improve financial outcomes by providing tools to better understand and utilize workplace benefits.

4. Custody Bank

Custody banks safeguard financial assets and provide services like settlement, accounting, and regulatory compliance for institutional investors. Growth opportunities stem from increasing global assets under custody, demand for data analytics, and blockchain technology adoption for settlement efficiency. Challenges include fee pressure from large clients, substantial technology investment requirements, and competition from both traditional players and fintech firms entering the space.

In retirement solutions, Voya competes with Fidelity, Empower, TIAA, Nationwide, Prudential, and MetLife. In health benefits, its competitors include Sun Life, Tokio Marine HCC, Cigna, Aetna, Aflac, MetLife, and Unum. For benefits administration, Voya faces competition from Alight, Businesssolver, and BSwift, while its investment management business competes with Principal Global Investors, Prudential, Ameriprise, Invesco, T. Rowe Price, and Franklin Templeton.

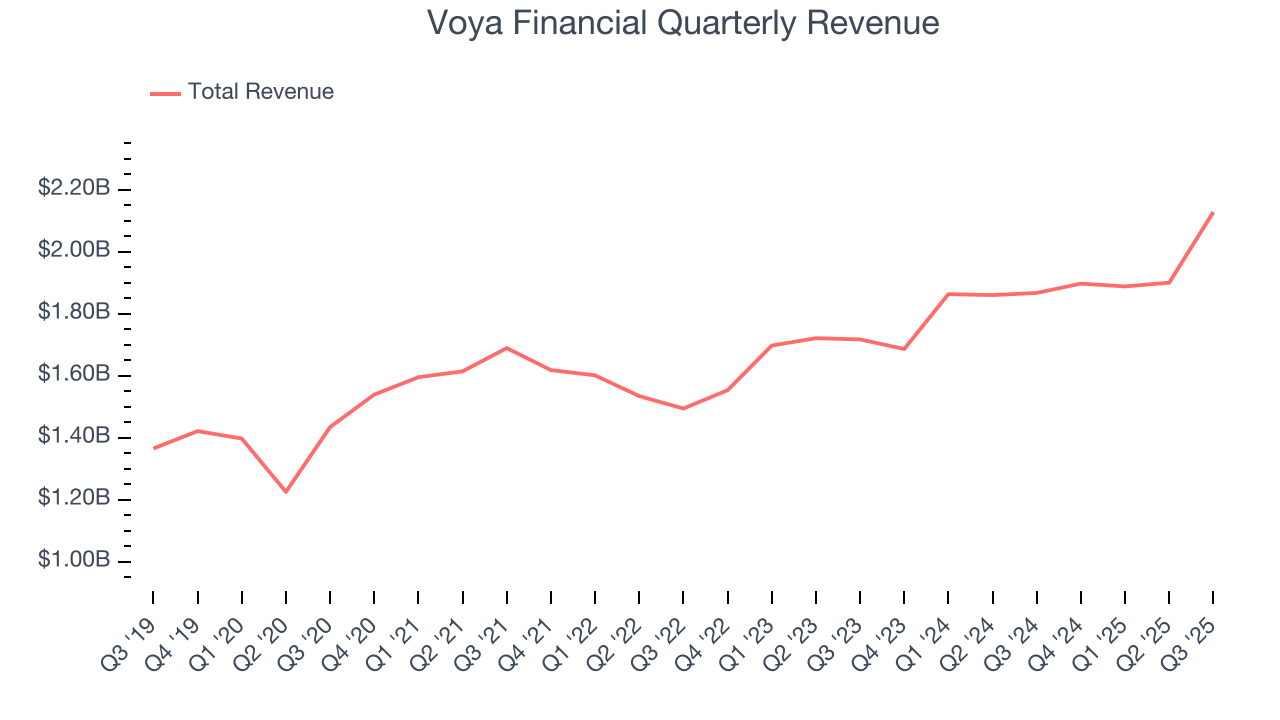

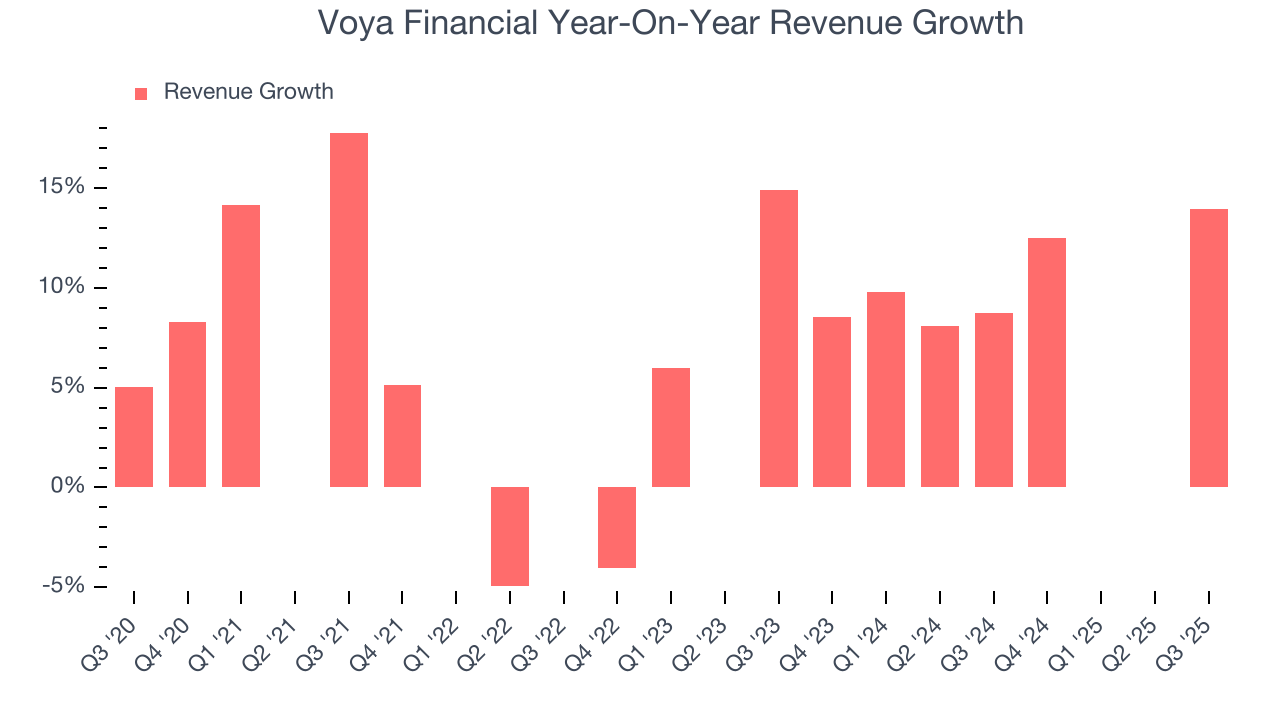

5. Revenue Growth

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Regrettably, Voya Financial’s revenue grew at a mediocre 7.4% compounded annual growth rate over the last five years. This fell short of our benchmark for the financials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within financials, a half-decade historical view may miss recent interest rate changes and market returns. Voya Financial’s annualized revenue growth of 8.1% over the last two years aligns with its five-year trend, suggesting its demand was stable.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

This quarter, Voya Financial reported year-on-year revenue growth of 14%, and its $2.13 billion of revenue exceeded Wall Street’s estimates by 23.8%.

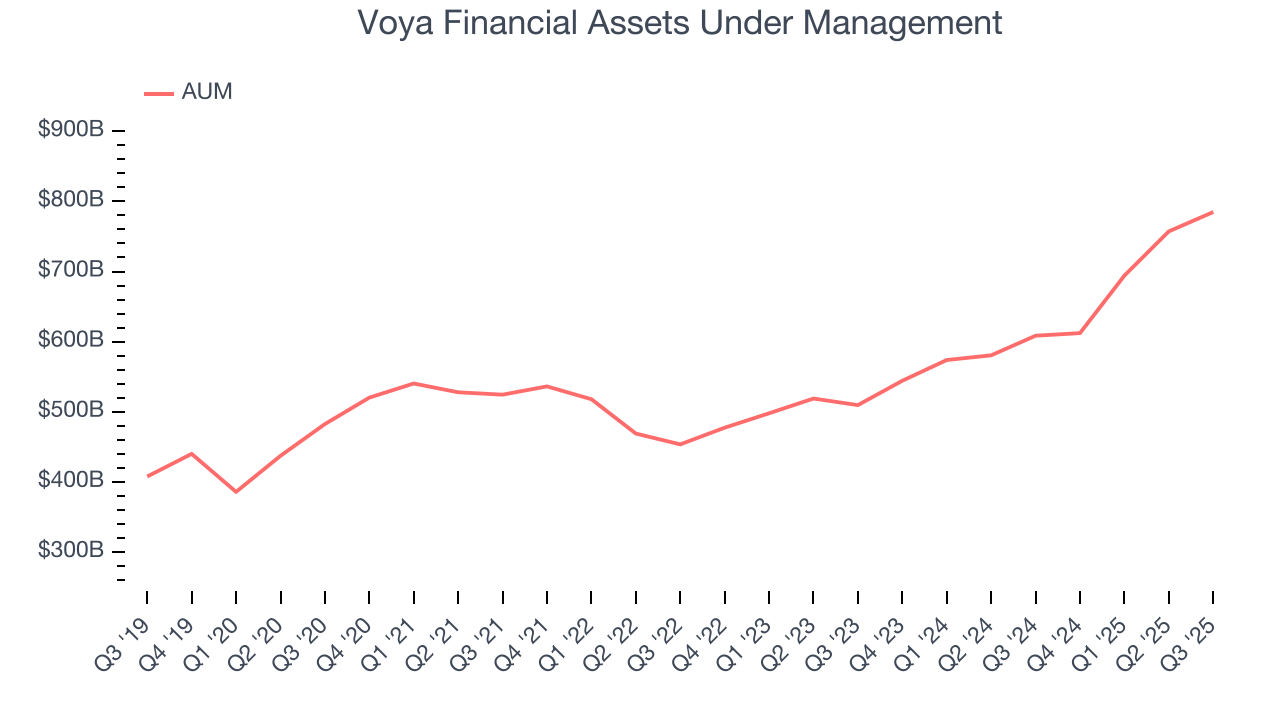

6. Assets Under Management (AUM)

Assets Under Management (AUM) is the total capital a firm oversees or manages on behalf of clients. Fees on this AUM, typically a small percentage, are contractually recurring and provide a high level of stability to revenue even if investment performance lags (although too much poor investment performance eventually hurts fundraising ability).

Voya Financial’s AUM has grown at an annual rate of 10.3% over the last five years, slightly better than the broader financials industry and faster than its total revenue. When analyzing Voya Financial’s AUM over the last two years, we can see that growth accelerated to 19.2% annually. Fundraising or short-term investment performance were net contributors for the company over this shorter period since assets grew faster than total revenue. That said, assets aren't the be-all and end-all due to their unpredictable and cyclical nature.

Voya Financial’s AUM punched in at $784.8 billion this quarter, meeting analysts’ expectations. This print was 29% higher than the same quarter last year.

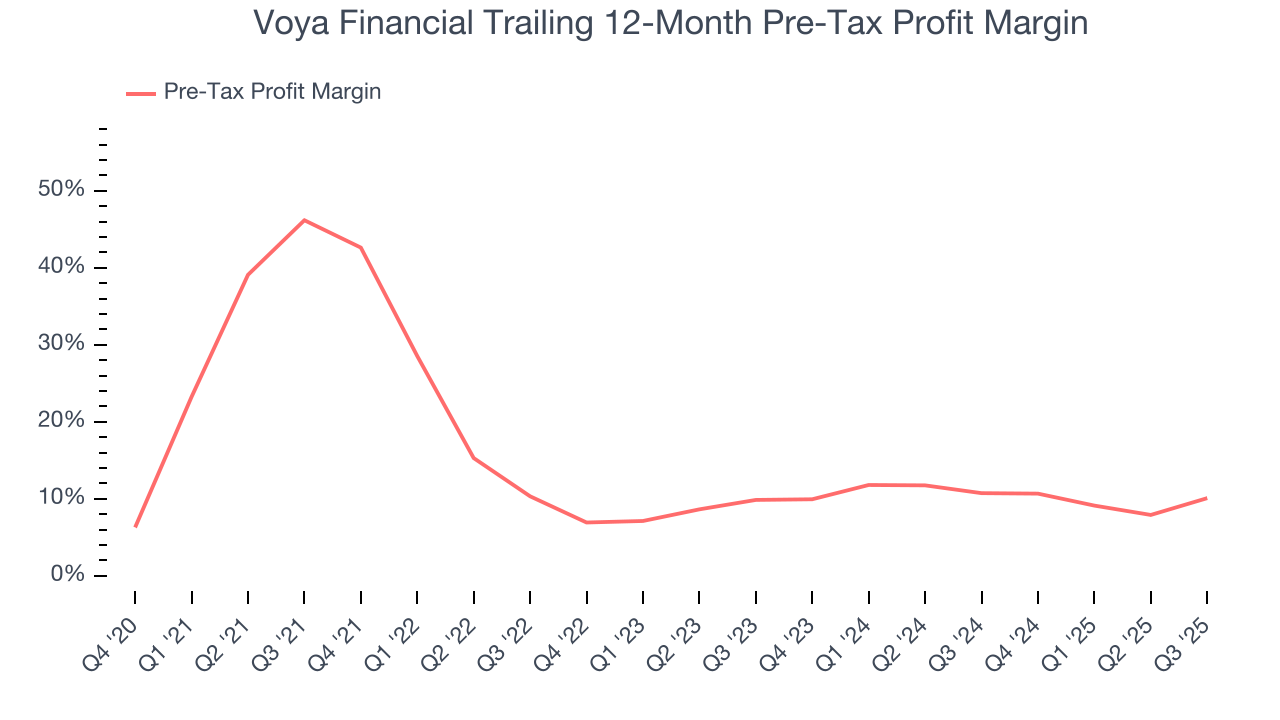

7. Pre-Tax Profit Margin

Revenue growth is one major determinant of business quality, and the efficiency of operations is another. For Custody Bank companies, we look at pre-tax profit rather than the operating margin that defines sectors such as consumer, tech, and industrials.

Financials companies manage interest-bearing assets and liabilities, making the interest income and expenses included in pre-tax profit essential to their profit calculation. Taxes, being external factors beyond management control, are appropriately excluded from this alternative margin measure.

Over the last four years, Voya Financial’s pre-tax profit margin has risen by 36.1 percentage points, going from 46.2% to 10.1%. Expenses have stabilized more recently as the company’s pre-tax profit margin was flat on a two-year basis.

Voya Financial’s pre-tax profit margin came in at 14.4% this quarter. This result was 8.2 percentage points better than the same quarter last year.

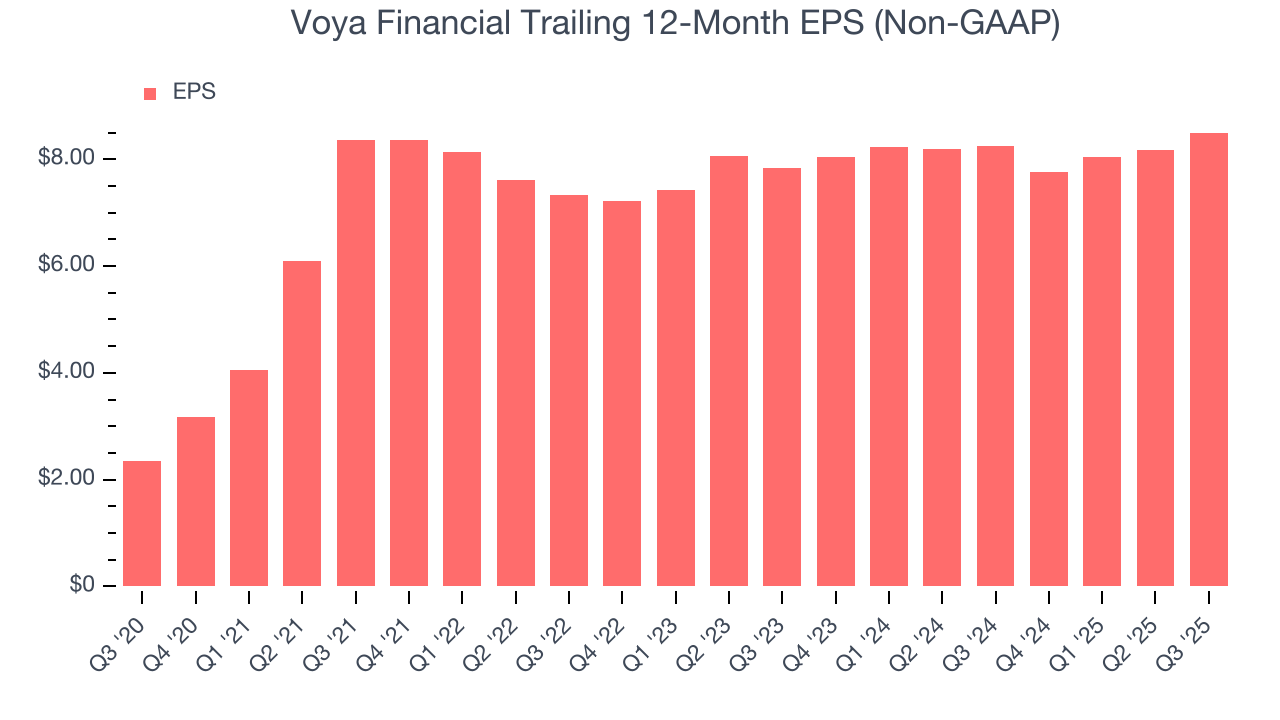

8. Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Voya Financial’s EPS grew at an astounding 29.3% compounded annual growth rate over the last five years, higher than its 7.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

For Voya Financial, its two-year annual EPS growth of 4.1% was lower than its five-year trend. We hope its growth can accelerate in the future.

In Q3, Voya Financial reported adjusted EPS of $2.45, up from $2.12 in the same quarter last year. This print beat analysts’ estimates by 8.9%. Over the next 12 months, Wall Street expects Voya Financial’s full-year EPS of $8.50 to grow 15.9%.

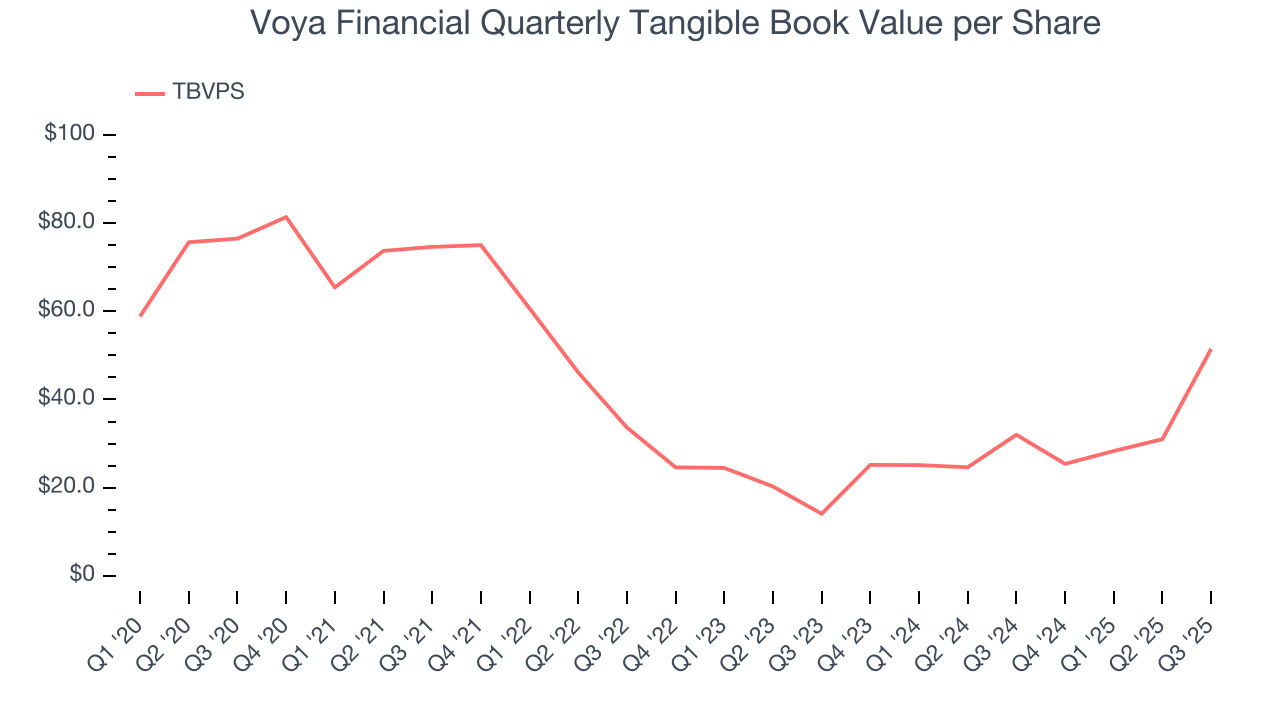

9. Tangible Book Value Per Share (TBVPS)

Diversified financial companies operate across multiple business segments, from investment banking and trading to wealth management and specialized lending. Their valuations hinge on balance sheet quality and the ability to compound shareholder equity across these diverse operations.

When analyzing this sector, tangible book value per share (TBVPS) takes precedence over many other metrics. This measure isolates genuine per-share value and provides insight into the institution’s capital position across diverse operations. On the other hand, EPS is often distorted by the diverse nature of operations, mergers, and various accounting treatments across different business units. Book value provides clearer performance insights.

Voya Financial’s TBVPS declined at a 7.6% annual clip over the last five years. However, TBVPS growth has accelerated recently, growing by 91.2% annually over the last two years from $14.08 to $51.45 per share.

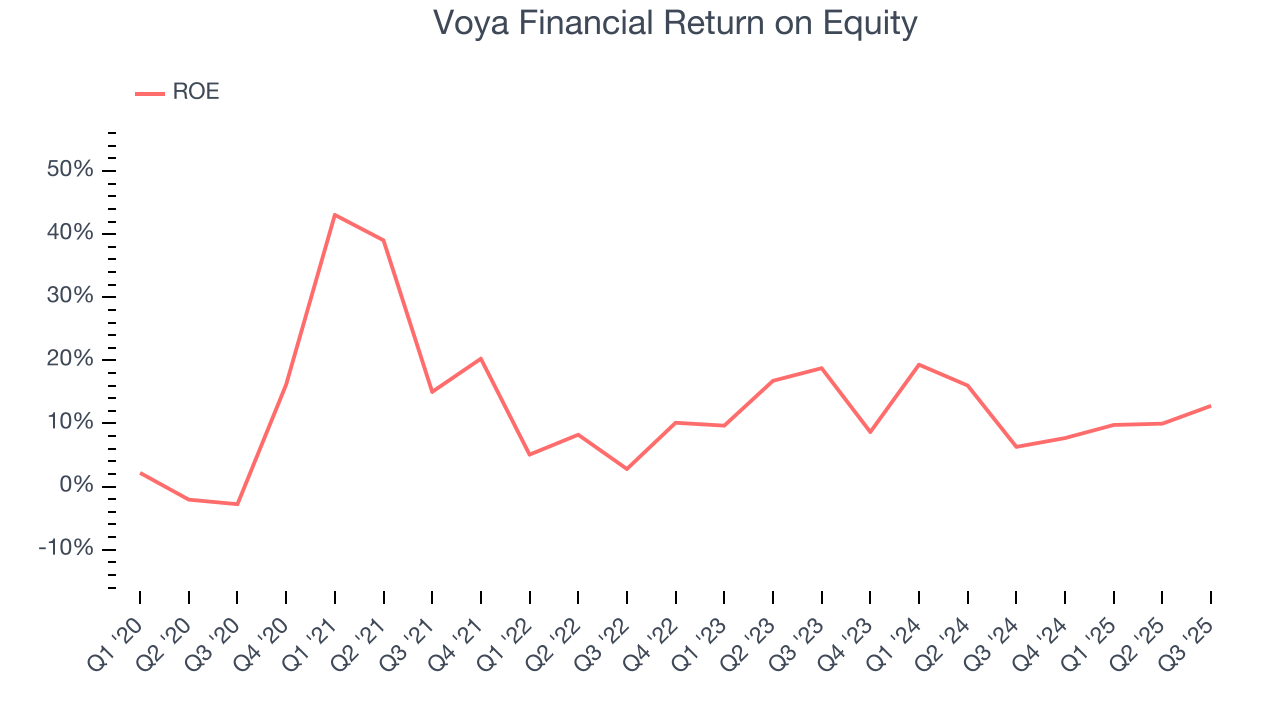

10. Return on Equity

Return on equity (ROE) measures how effectively banks generate profit from each dollar of shareholder equity - a critical funding source. High-ROE institutions typically compound shareholder wealth faster over time through retained earnings, share repurchases, and dividend payments.

Over the last five years, Voya Financial has averaged an ROE of 14.8%, healthy for a company operating in a sector where the average shakes out around 10% and those putting up 25%+ are greatly admired. This is a bright spot for Voya Financial.

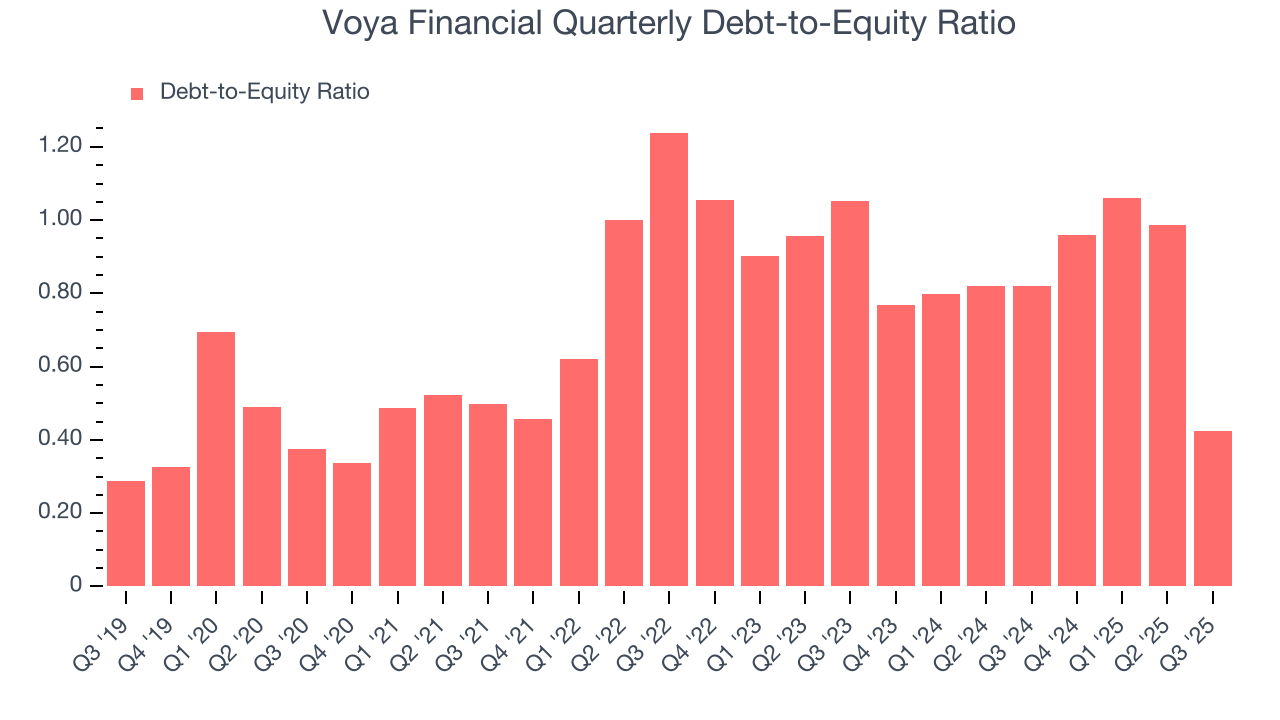

11. Balance Sheet Assessment

The debt-to-equity ratio is a widely used measure to assess a company's balance sheet health. A higher ratio means that a business aggressively financed its growth with debt. This can result in higher earnings (if the borrowed funds are invested profitably) but also increases risk.

If debt levels are too high, there could be difficulties in meeting obligations, especially during economic downturns or periods of rising interest rates if the debt has variable-rate payments.

Voya Financial currently has $2.10 billion of debt and $4.96 billion of shareholder's equity on its balance sheet, and over the past four quarters, has averaged a debt-to-equity ratio of 0.9×. We think this is safe and raises no red flags. In general, we’re comfortable with any ratio below 3.5× for a financials business.

12. Key Takeaways from Voya Financial’s Q3 Results

We were impressed by how significantly Voya Financial blew past analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 2% to $75.09 immediately following the results.

13. Is Now The Time To Buy Voya Financial?

Updated: January 26, 2026 at 11:10 PM EST

When considering an investment in Voya Financial, investors should account for its valuation and business qualities as well as what’s happened in the latest quarter.

Voya Financial isn’t a terrible business, but it doesn’t pass our quality test. To kick things off, its revenue growth was mediocre over the last five years, and analysts expect its demand to deteriorate over the next 12 months. And while Voya Financial’s astounding EPS growth over the last five years shows its profits are trickling down to shareholders, its TBVPS has declined over the last five years.

Voya Financial’s P/E ratio based on the next 12 months is 8x. This valuation multiple is fair, but we don’t have much faith in the company. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $86.80 on the company (compared to the current share price of $76.16).