Williams-Sonoma (WSM)

We’re skeptical of Williams-Sonoma. Not only is its demand weak but also its falling returns on capital suggest it’s becoming less profitable.― StockStory Analyst Team

1. News

2. Summary

Why We Think Williams-Sonoma Will Underperform

Started in 1956 as a store specializing in French cookware, Williams-Sonoma (NYSE:WSM) is a specialty retailer of higher-end kitchenware, home goods, and furniture.

- Products aren't resonating with the market as its revenue declined by 3.2% annually over the last three years

- Ongoing store closures and lackluster same-store sales indicate sluggish demand and a focus on consolidation

- A positive is that its disciplined cost controls and effective management have materialized in a strong operating margin

Williams-Sonoma’s quality doesn’t meet our hurdle. There are superior stocks for sale in the market.

Why There Are Better Opportunities Than Williams-Sonoma

Williams-Sonoma is trading at $180.23 per share, or 20.6x forward P/E. This multiple expensive for its subpar fundamentals.

Paying up for elite businesses with strong earnings potential is better than investing in lower-quality companies with shaky fundamentals. That’s how you avoid big downside over the long term.

3. Williams-Sonoma (WSM) Research Report: Q4 CY2025 Update

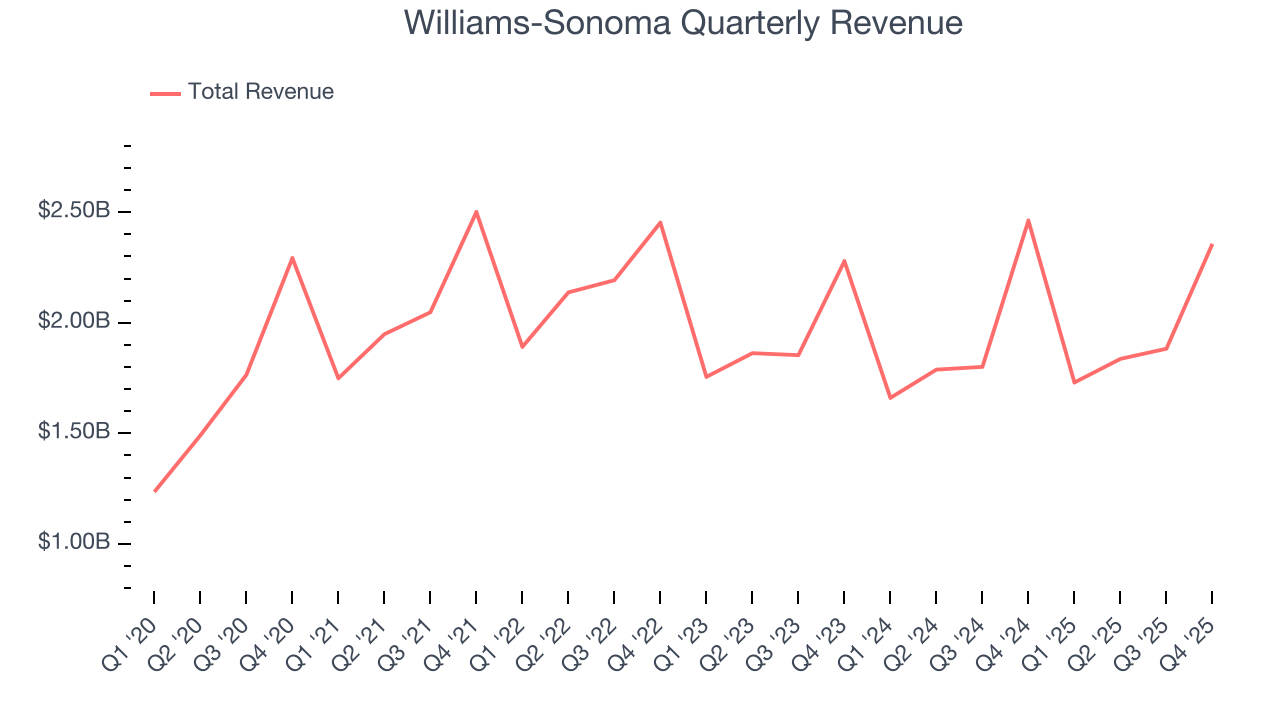

Kitchenware and home goods retailer Williams-Sonoma (NYSE:WSM) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 4.3% year on year to $2.36 billion. Its GAAP profit of $3.04 per share was 4.5% above analysts’ consensus estimates.

Williams-Sonoma (WSM) Q4 CY2025 Highlights:

- Revenue: $2.36 billion vs analyst estimates of $2.42 billion (4.3% year-on-year decline, 2.5% miss)

- EPS (GAAP): $3.04 vs analyst estimates of $2.91 (4.5% beat)

- Adjusted EBITDA: $568 million vs analyst estimates of $535.5 million (24.1% margin, 6.1% beat)

- Operating Margin: 20.3%, down from 21.5% in the same quarter last year

- Free Cash Flow Margin: 21.9%, down from 23% in the same quarter last year

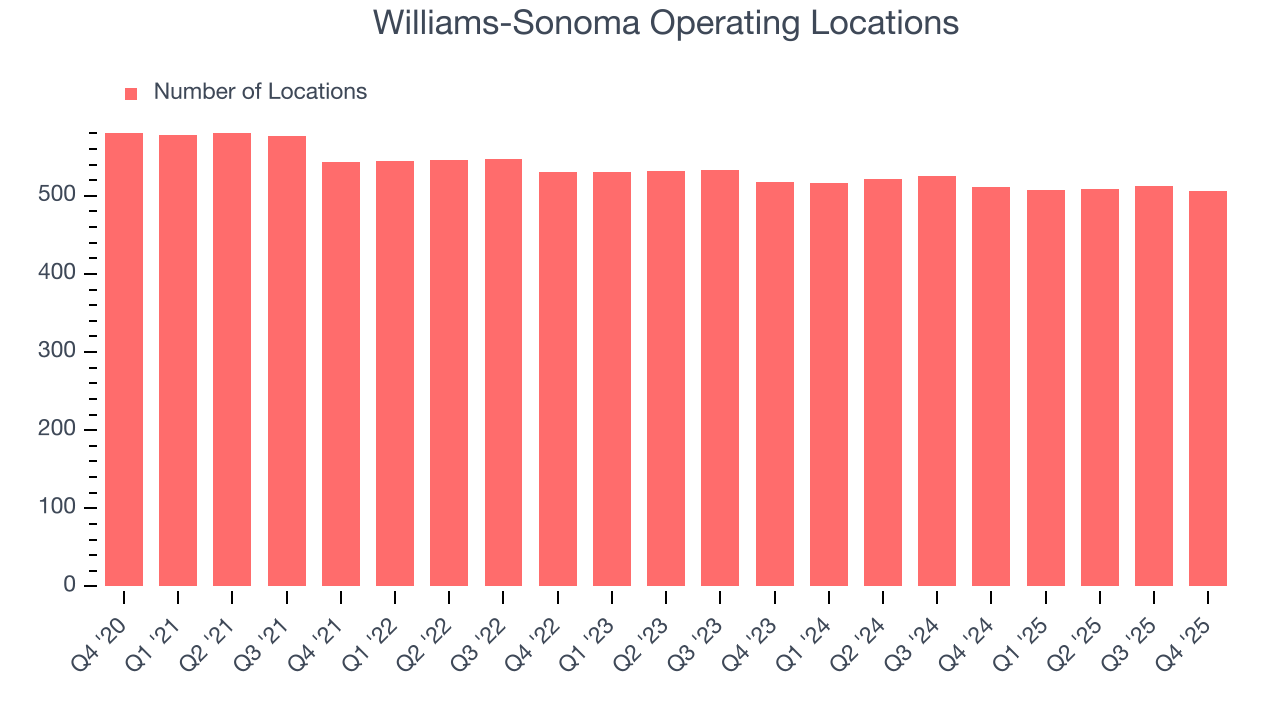

- Locations: 506 at quarter end, down from 512 in the same quarter last year

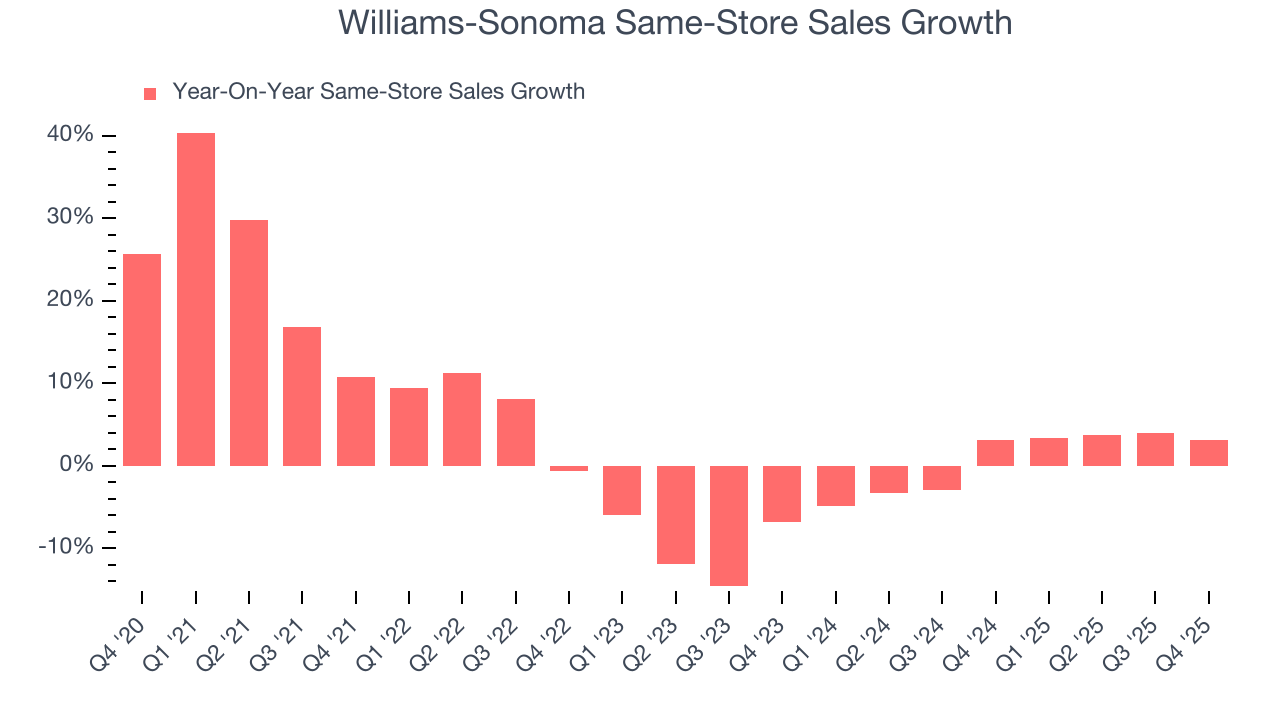

- Same-Store Sales rose 3.2% year on year, in line with the same quarter last year

- Market Capitalization: $21.75 billion

Company Overview

Started in 1956 as a store specializing in French cookware, Williams-Sonoma (NYSE:WSM) is a specialty retailer of higher-end kitchenware, home goods, and furniture.

Today, the company has expanded beyond its French cookware roots to offer everything from bedding and bath linens to gourmet food and specialty appliances. The unifying theme in a Williams-Sonoma store is products that are both beautiful and practical.

The core Williams-Sonoma customer is typically a higher-income, educated suburban consumer who values quality and design and isn’t afraid to pay a bit more for it. Some brands that a shopper can find in a Williams-Sonoma store include Le Creuset, KitchenAid, Nespresso, and the company’s own line of kitchenware.

Williams-Sonoma has been one of the more successful retailers to adapt to e-commerce. Before online shopping caught fire, the company was able to build a large database of customer information because of its catalog mailing list. This turned into an email marketing list and a relatively early e-commerce presence.

4. Home Furniture Retailer

Furniture retailers understand that ‘home is where the heart is’ but that no home is complete without that comfy sofa to kick back on or a dreamy bed to rest in. These stores focus on providing not only what is practically needed in a house but also aesthetics, style, and charm in the form of tables, lamps, and mirrors. Decades ago, it was thought that furniture would resist e-commerce because of the logistical challenges of shipping large furniture, but now you can buy a mattress online and get it in a box a few days later; so just like other retailers, furniture stores need to adapt to new realities and consumer behaviors.

Competitors that offer kitchenware and home goods include TJX (NYSE:TJX), Target (NYSE:TGT), and Walmart (NYSE:WMT).

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years.

With $7.81 billion in revenue over the past 12 months, Williams-Sonoma is a mid-sized retailer, which sometimes brings disadvantages compared to larger competitors benefiting from better economies of scale.

As you can see below, Williams-Sonoma’s demand was weak over the last three years. Its sales fell by 3.5% annually as it closed stores.

This quarter, Williams-Sonoma missed Wall Street’s estimates and reported a rather uninspiring 4.3% year-on-year revenue decline, generating $2.36 billion of revenue.

Looking ahead, sell-side analysts expect revenue to grow 4.7% over the next 12 months, an acceleration versus the last three years. This projection is commendable and suggests its newer products will catalyze better top-line performance.

6. Store Performance

Number of Stores

A retailer’s store count influences how much it can sell and how quickly revenue can grow.

Williams-Sonoma operated 506 locations in the latest quarter. Over the last two years, the company has generally closed its stores, averaging 1.9% annual declines.

When a retailer shutters stores, it usually means that brick-and-mortar demand is less than supply, and it is responding by closing underperforming locations to improve profitability.

Same-Store Sales

The change in a company's store base only tells one side of the story. The other is the performance of its existing locations and e-commerce sales, which informs management teams whether they should expand or downsize their physical footprints. Same-store sales is an industry measure of whether revenue is growing at those existing stores and is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Williams-Sonoma’s demand within its existing locations has barely increased over the last two years as its same-store sales were flat. This performance isn’t ideal, and Williams-Sonoma is attempting to boost same-store sales by closing stores (fewer locations sometimes lead to higher same-store sales).

In the latest quarter, Williams-Sonoma’s same-store sales rose 3.2% year on year. This growth was an acceleration from its historical levels, which is always an encouraging sign.

7. Gross Margin & Pricing Power

We prefer higher gross margins because they not only make it easier to generate more operating profits but also indicate product differentiation, negotiating leverage, and pricing power.

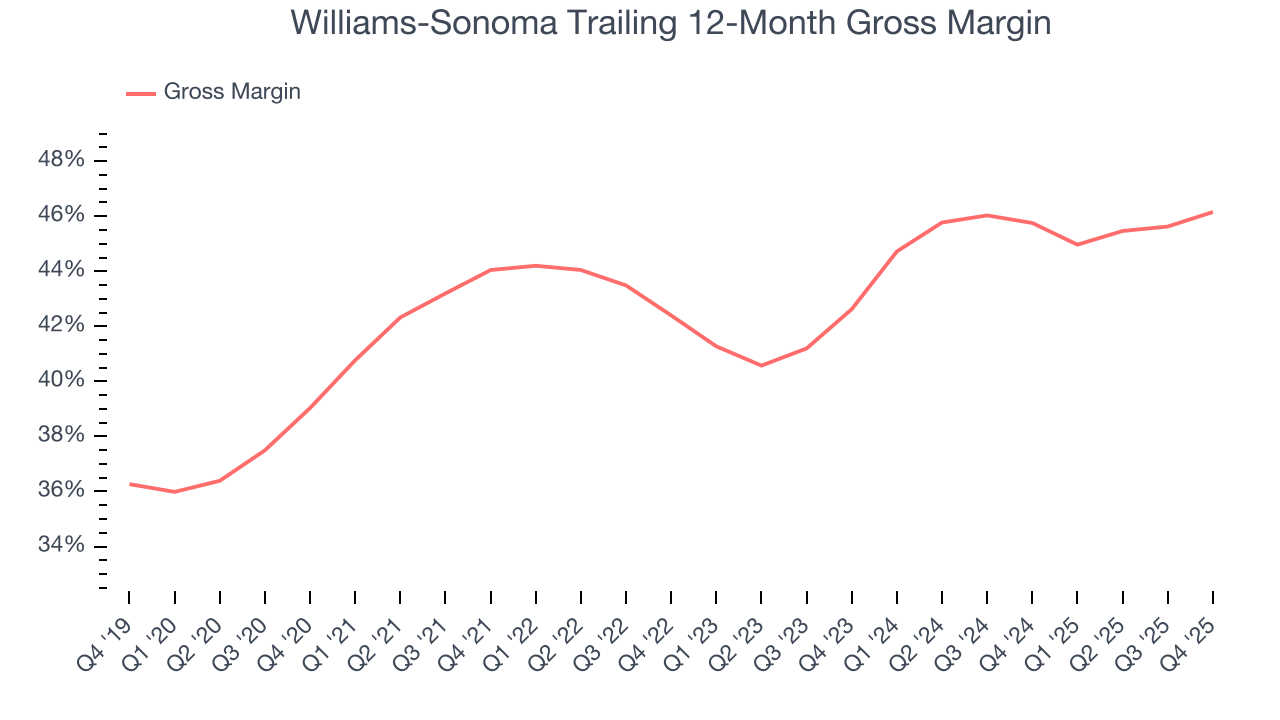

Williams-Sonoma has good unit economics for a retailer, giving it the opportunity to invest in areas such as marketing and talent to stay competitive. As you can see below, it averaged an impressive 46% gross margin over the last two years. That means for every $100 in revenue, $54.04 went towards paying for inventory, transportation, and distribution.

This quarter, Williams-Sonoma’s gross profit margin was 46.9% , marking a 1.7 percentage point increase from 45.2% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting it strives to keep prices low for customers and has stable input costs (such as labor and freight expenses to transport goods).

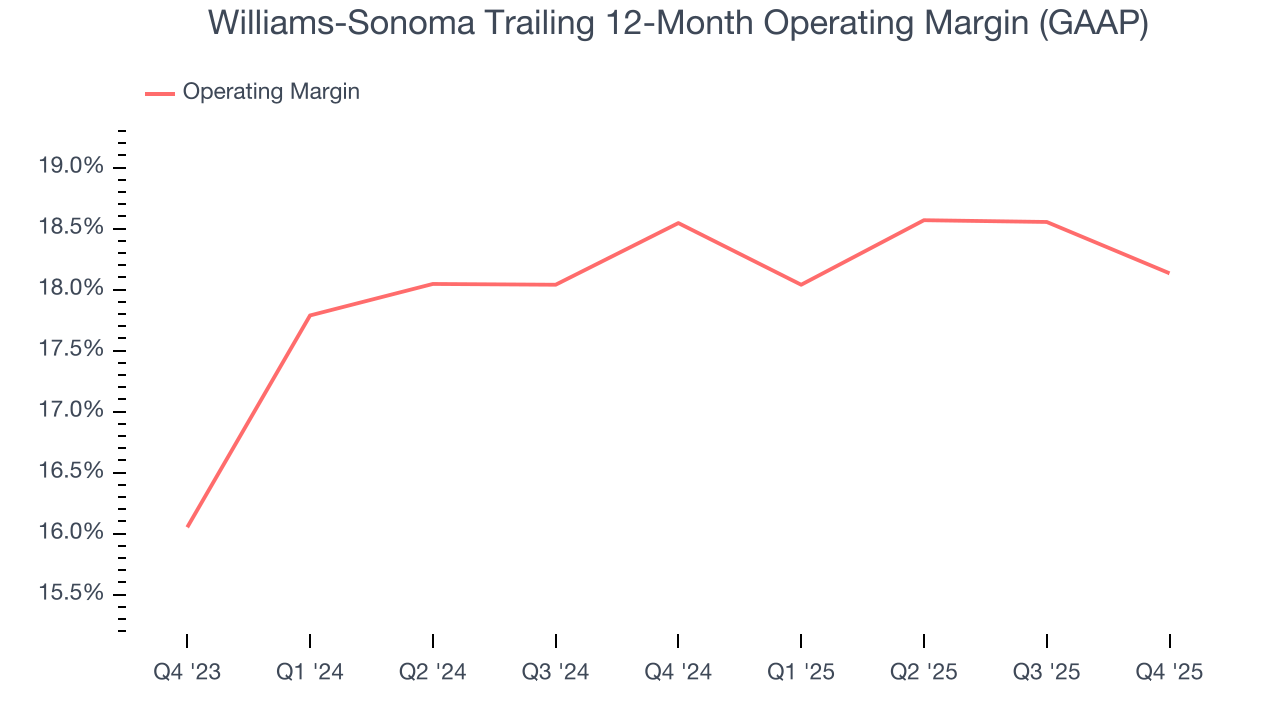

8. Operating Margin

Operating margin is a key profitability metric because it accounts for all expenses necessary to run a store, including wages, inventory, rent, advertising, and other administrative costs.

Williams-Sonoma’s operating margin has generally stayed the same over the last 12 months, averaging 18.3% over the last two years. This profitability was elite for a consumer retail business thanks to its efficient cost structure and economies of scale. This result isn’t too surprising as its gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Williams-Sonoma’s operating margin might fluctuated slightly but has generally stayed the same over the last year, highlighting the consistency of its expense base.

This quarter, Williams-Sonoma generated an operating margin profit margin of 20.3%, down 1.3 percentage points year on year. Conversely, its gross margin actually rose, so we can assume its recent inefficiencies were driven by increased operating expenses like marketing, and administrative overhead.

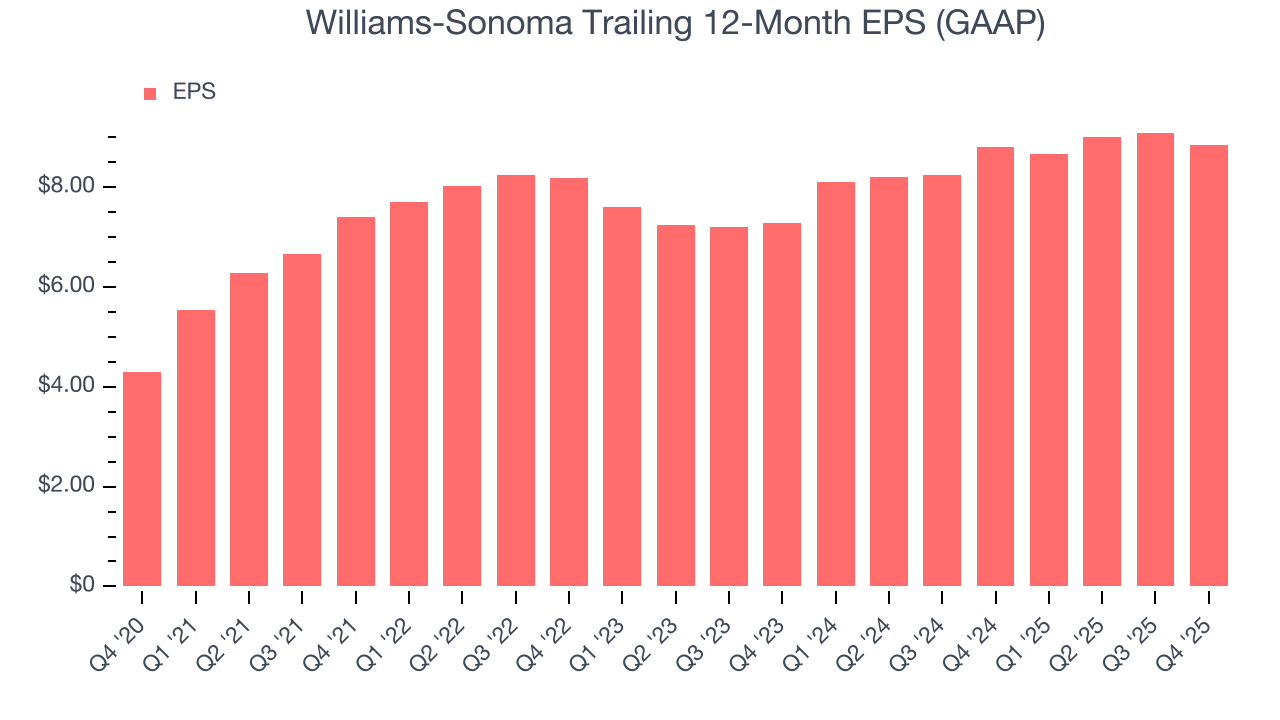

9. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Williams-Sonoma’s EPS grew at 2.7% compounded annual growth rate over the last three years. On the bright side, this performance was better than its 3.5% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

In Q4, Williams-Sonoma reported EPS of $3.04, down from $3.28 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 4.5%. Over the next 12 months, Wall Street expects Williams-Sonoma’s full-year EPS of $8.86 to grow 3.6%.

10. Cash Is King

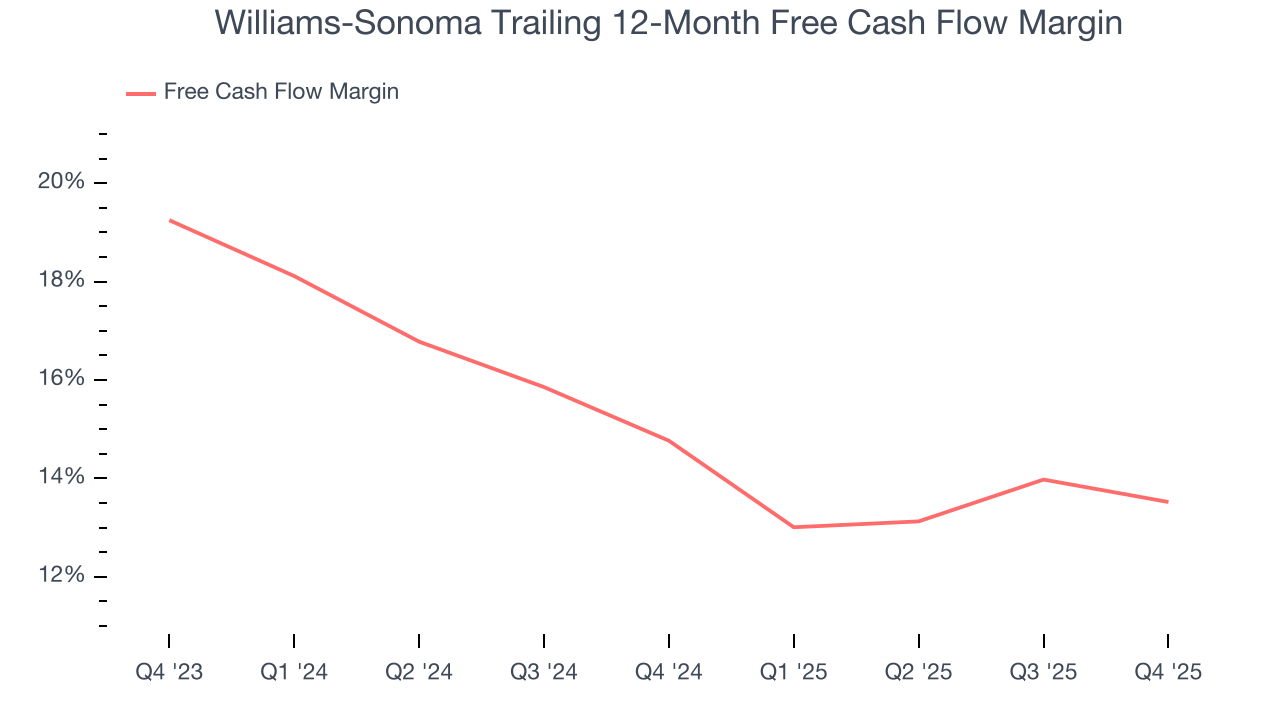

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Williams-Sonoma has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer retail sector, averaging 14.1% over the last two years.

Taking a step back, we can see that Williams-Sonoma’s margin dropped by 1.2 percentage points over the last year. Continued declines could signal it is in the middle of an investment cycle.

Williams-Sonoma’s free cash flow clocked in at $516 million in Q4, equivalent to a 21.9% margin. The company’s cash profitability regressed as it was 1.1 percentage points lower than in the same quarter last year, but it’s still above its two-year average. We wouldn’t put too much weight on this quarter’s decline because capital expenditures can be seasonal and companies often stockpile inventory in anticipation of higher demand, causing short-term swings. Long-term trends are more important.

11. Return on Invested Capital (ROIC)

EPS and free cash flow tell us whether a company was profitable while growing its revenue. But was it capital-efficient? Enter ROIC, a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

Although Williams-Sonoma hasn’t been the highest-quality company lately because of its poor top-line performance, it found a few growth initiatives in the past that worked out wonderfully. Its five-year average ROIC was 44.4%, splendid for a consumer retail business.

12. Balance Sheet Assessment

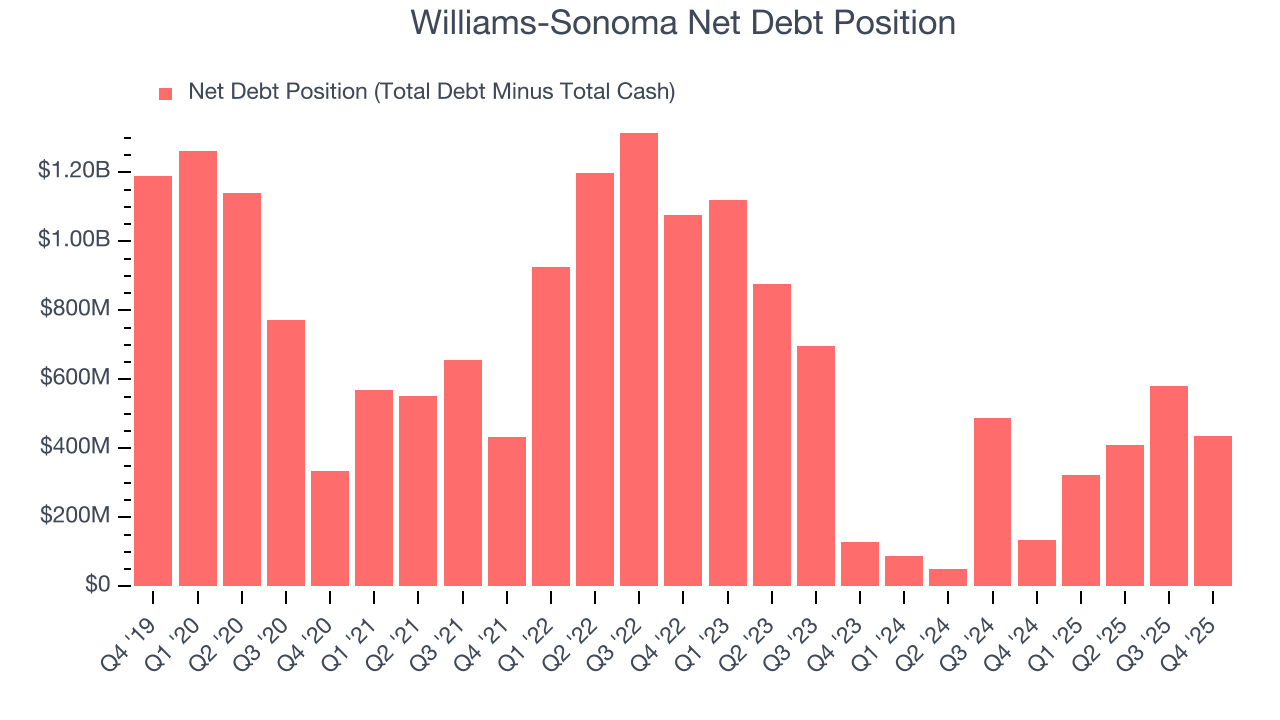

Williams-Sonoma reported $1.02 billion of cash and $1.46 billion of debt on its balance sheet in the most recent quarter. As investors in high-quality companies, we primarily focus on two things: 1) that a company’s debt level isn’t too high and 2) that its interest payments are not excessively burdening the business.

With $1.68 billion of EBITDA over the last 12 months, we view Williams-Sonoma’s 0.3× net-debt-to-EBITDA ratio as safe. We also see its $36.84 million of annual interest expenses as appropriate. The company’s profits give it plenty of breathing room, allowing it to continue investing in growth initiatives.

13. Key Takeaways from Williams-Sonoma’s Q4 Results

We enjoyed seeing Williams-Sonoma beat analysts’ EBITDA expectations this quarter. We were also glad its gross margin outperformed Wall Street’s estimates. On the other hand, its revenue missed. Overall, this print was mixed. The stock remained flat at $181.00 immediately following the results.

14. Is Now The Time To Buy Williams-Sonoma?

A common mistake we notice when investors are deciding whether to buy a stock or not is that they simply look at the latest earnings results. Business quality and valuation matter more, so we urge you to understand these dynamics as well.

Williams-Sonoma isn’t a terrible business, but it isn’t one of our picks. To kick things off, its revenue has declined over the last three years. While its impressive operating margins show it has a highly efficient business model, the downside is its declining physical locations suggests its demand is falling. On top of that, its poor same-store sales performance has been a headwind.

Williams-Sonoma’s P/E ratio based on the next 12 months is 19.9x. Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere.

Wall Street analysts have a consensus one-year price target of $206.37 on the company (compared to the current share price of $181.00).