Amplitude's (NASDAQ:AMPL) Q2 Sales Top Estimates, Provides Optimistic Full-Year Guidance

Kayode Omotosho /

August 8, 2023

Data analytics software provider Amplitude (NASDAQ:AMPL) reported Q2 FY2023 results exceeding Wall Street analysts' expectations, with revenue up 16.6% year on year to $67.8 million. Guidance for next quarter's revenue was also optimistic $70 million at the midpoint, 4.5% above analysts' estimates. Amplitude made a GAAP loss of $27.8 million, down from its loss of $24.6 million in the same quarter last year.

Is now the time to buy Amplitude? Find out in our full research available to StockStory Edge members.

Amplitude (AMPL) Q2 FY2023 Highlights:

- Revenue: $67.8 million vs analyst estimates of $66.9 million (1.31% beat)

- EPS (non-GAAP): $0.02 vs analyst estimates of $0.02 (16.1% beat)

- Revenue Guidance for Q3 2023 is $70 million at the midpoint, above analyst estimates of $67 million

- The company lifted revenue guidance for the full year from $267.5 million to $274.6 million at the midpoint, a 2.65% increase

- Free Cash Flow of $19.3 million is up from -$5.84 million in the previous quarter

- Net Revenue Retention Rate: 108%, down from 114% in the previous quarter

- Customers: 2,344, up from 2,175 in the previous quarter

- Gross Margin (GAAP): 74.6%, up from 70.7% in the same quarter last year

Born out of a failed voice recognition startup by founder Spenser Skates, Amplitude (NASDAQ:AMPL) is data analytics software helping companies improve and optimize their digital products.

Organizations generate a lot of data that is stored in silos, often in incompatible formats, making it slow and costly to extract actionable insights, which in turn drives demand for modern cloud-based data analysis platforms that can efficiently analyze the silo-ed data.

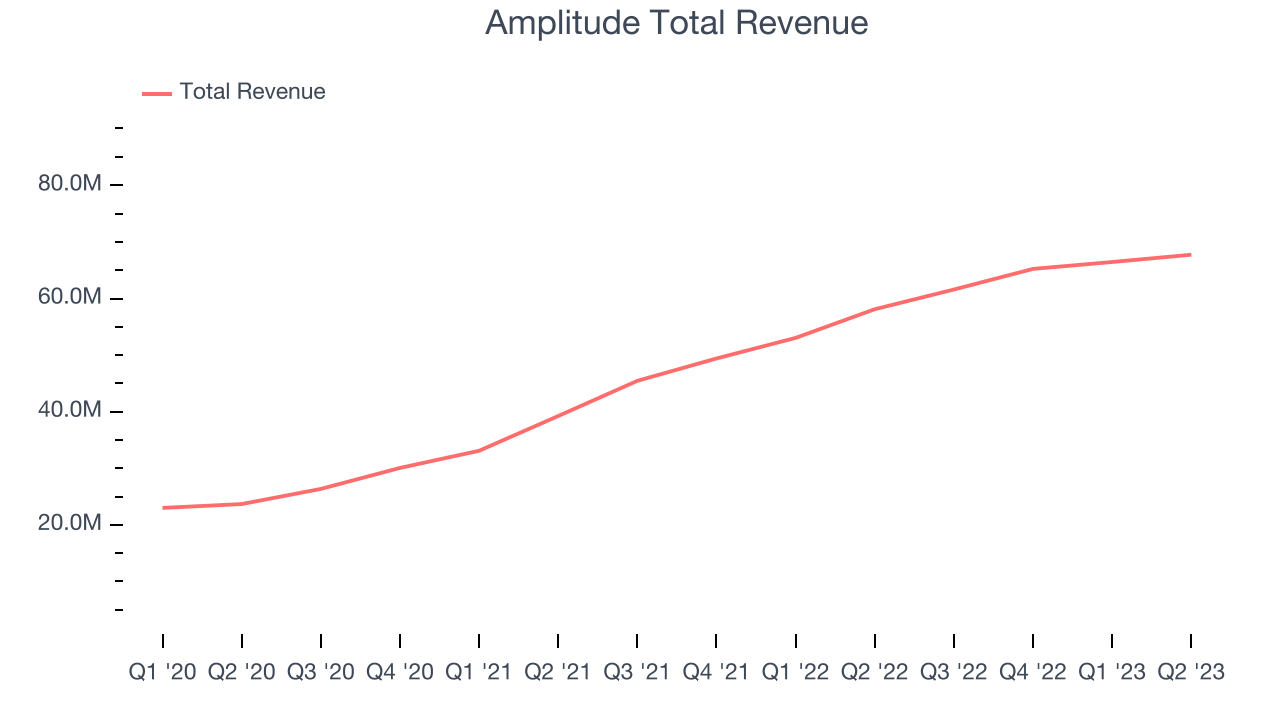

Sales Growth

As you can see below, Amplitude's revenue growth has been impressive over the last two years, growing from $39.3 million in Q2 FY2021 to $67.8 million this quarter.

This quarter, Amplitude's quarterly revenue was once again up 16.6% year on year. We can see that Amplitude's revenue increased by $1.29 million in Q2, up from $1.22 million in Q1 2023. While we've no doubt some investors were looking for higher growth, it's good to see that quarterly revenue is accelerating.

Next quarter's guidance suggests that Amplitude is expecting revenue to grow 13.6% year on year to $70 million, slowing down from the 35.5% year-on-year increase it recorded in the same quarter last year. Ahead of the earnings results announcement, the analysts covering the company were expecting sales to grow 6.7% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

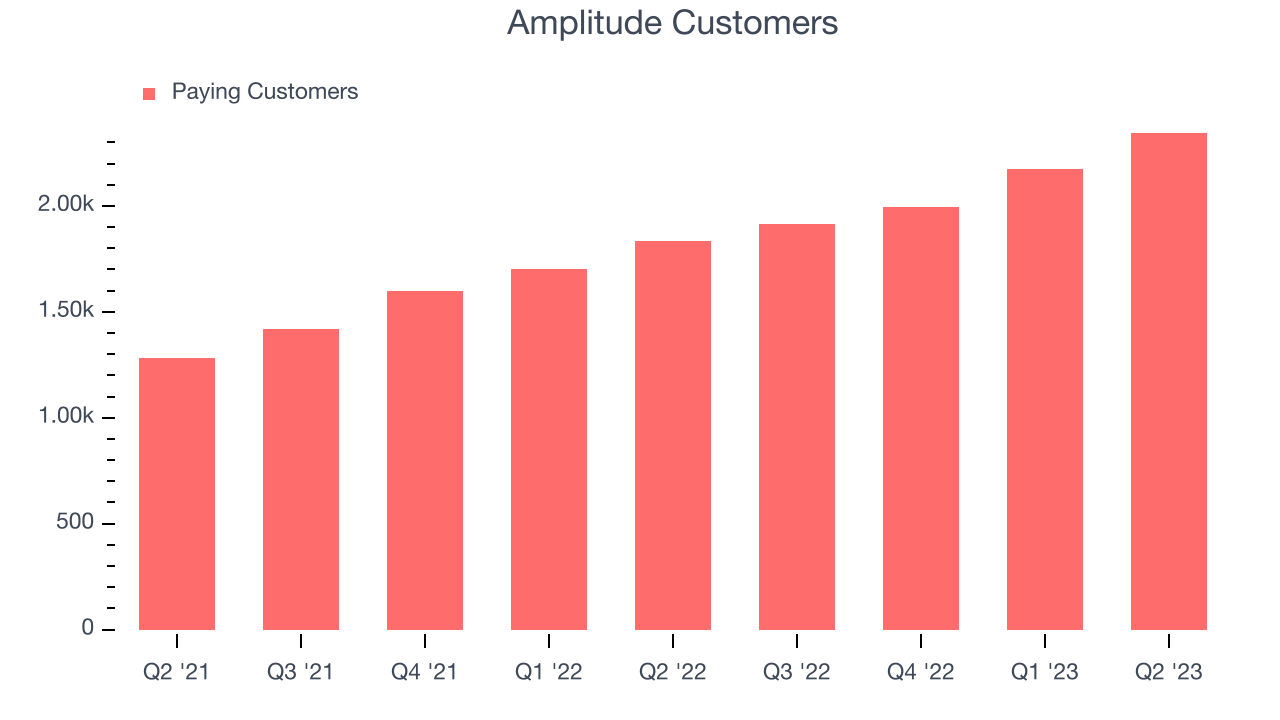

Customer Growth

Amplitude reported 2,344 customers at the end of the quarter, an increase of 169 from the previous quarter. That's roughly the same customer growth as we observed last quarter and quite a bit above what we've typically seen over the last year, confirming that the company is sustaining a good sales pace.

Key Takeaways from Amplitude's Q2 Results

With a market capitalization of $1.25 billion, Amplitude is among smaller companies, but its $290.4 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

We were impressed by Amplitude's strong user growth. We were also glad that next quarter's revenue guidance came in higher than Wall Street's expectations. Overall, this quarter's results seemed fairly positive and shareholders should feel optimistic. The stock is flat after reporting and currently trades at $10.69 per share.

So should you invest in Amplitude right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.