Duolingo (NASDAQ:DUOL) Posts Better-Than-Expected Sales In Q4, Stock Jumps 20%

Kayode Omotosho /

February 28, 2024

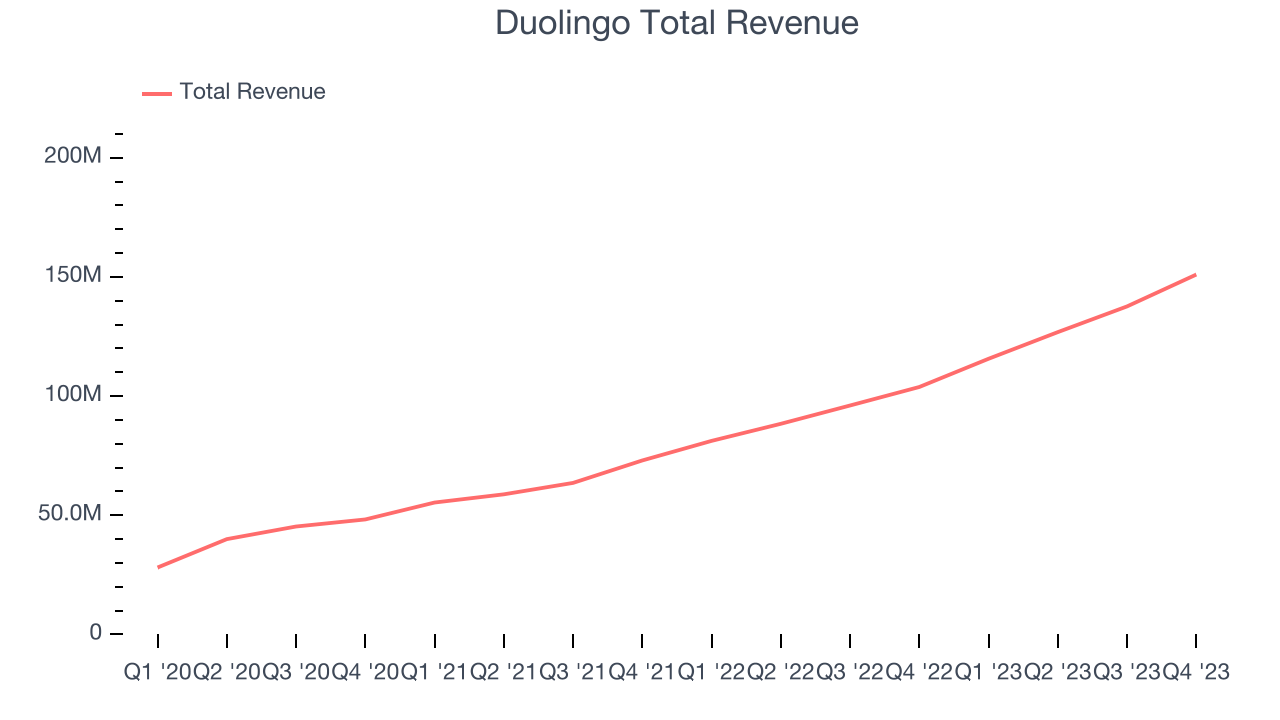

Language-learning app Duolingo (NASDAQ:DUOL) reported Q4 FY2023 results exceeding Wall Street analysts' expectations, with revenue up 45.4% year on year to $151 million. Guidance for next quarter's revenue was also optimistic at $165.5 million at the midpoint, 3.9% above analysts' estimates. It made a GAAP profit of $0.26 per share, improving from its profit of $0.19 per share in the same quarter last year.

Is now the time to buy Duolingo? Find out in our full research report.

Duolingo (DUOL) Q4 FY2023 Highlights:

- Revenue: $151 million vs analyst estimates of $148.4 million (1.8% beat)

- EPS: $0.26 vs analyst estimates of $0.16 ($0.10 beat)

- Revenue Guidance for Q1 2024 is $165.5 million at the midpoint, above analyst estimates of $159.4 million (adjusted EBITDA guidance for the period also ahead of expectations)

- Management's revenue guidance for the upcoming financial year 2024 is $723.5 million at the midpoint, beating analyst estimates by 3.2% and implying 36.2% growth (vs 43.6% in FY2023) (adjusted EBITDA guidance for the period also ahead of expectations)

- Free Cash Flow of $47.67 million, up 42.4% from the previous quarter

- Gross Margin (GAAP): 73.1%, in line with the same quarter last year

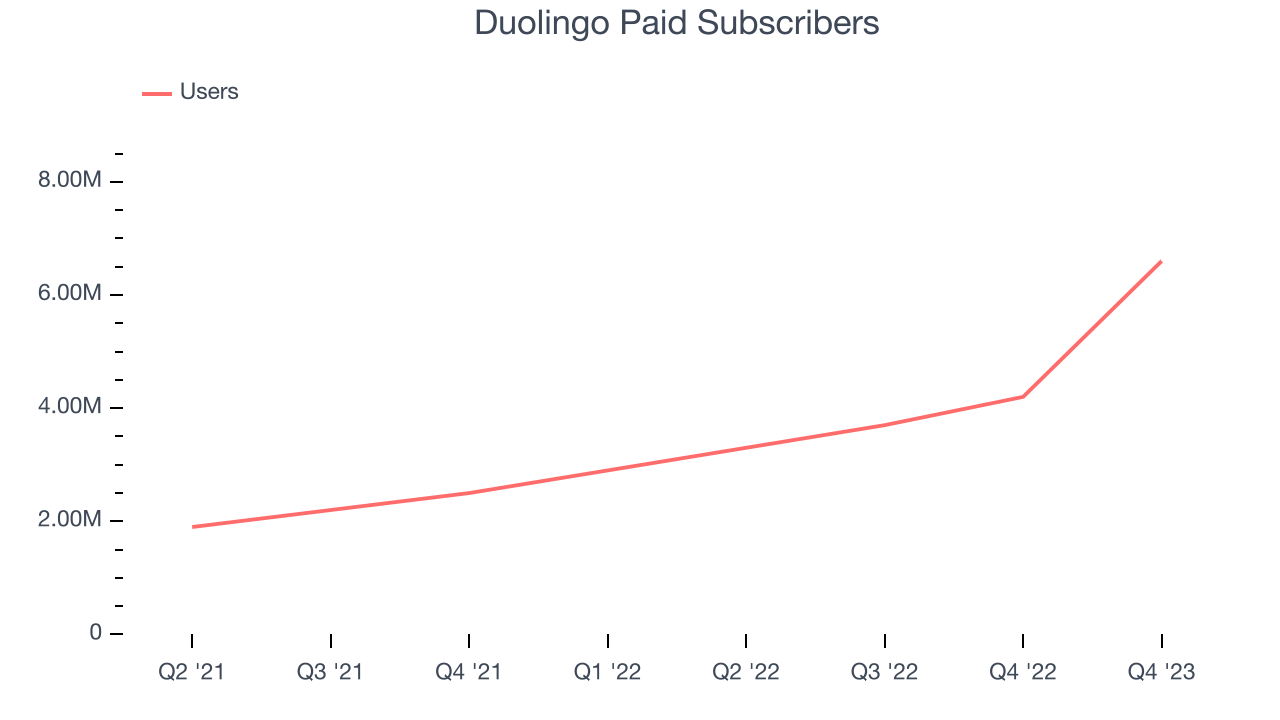

- Paid Subscribers: 6.6 million, up 2.4 million year on year

- Market Capitalization: $8.17 billion

“2023 was an exceptional year that exceeded our own high expectations. It was capped off with a very strong Q4 that saw us achieve record bookings, revenue and profitability,” said Luis von Ahn, Co-Founder and CEO of Duolingo.

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ:DUOL) is a mobile app helping people learn new languages.

Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Sales Growth

Duolingo's revenue growth over the last three years has been exceptional, averaging 50% annually. This quarter, Duolingo beat analysts' estimates and reported excellent 45.4% year-on-year revenue growth.

Guidance for the next quarter indicates Duolingo is expecting revenue to grow 43.1% year on year to $165.5 million, in line with the 42.4% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to reach $723.5 million at the midpoint, representing 36.2% growth compared to the 43.6% increase in FY2023.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Usage Growth

As a subscription-based app, Duolingo generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Duolingo's users, a key performance metric for the company, grew 66.8% annually to 6.6 million. This is among the fastest growth rates of any consumer internet company, indicating that users are excited about its offerings.

In Q4, Duolingo added 2.4 million users, translating into 57.1% year-on-year growth.

Revenue Per User

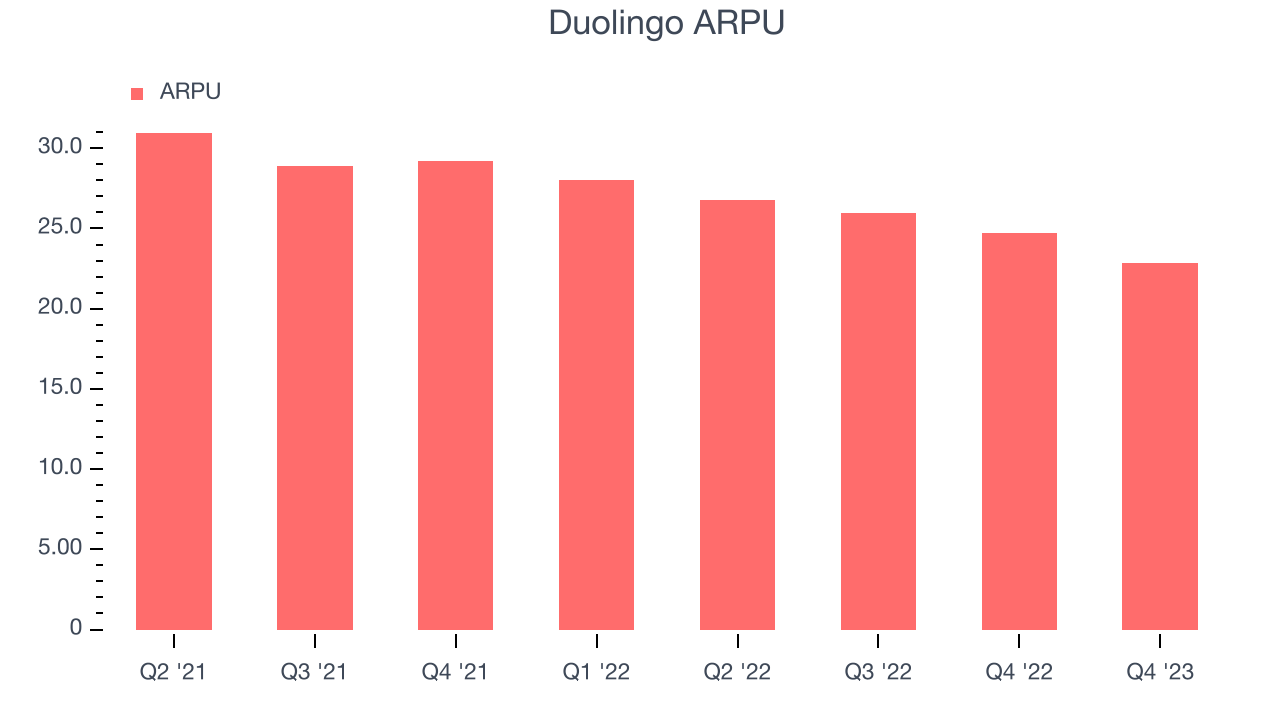

Average revenue per user (ARPU) is a critical metric to track for consumer internet businesses like Duolingo because it measures how much the average user spends. ARPU is also a key indicator of how valuable its users are (and can be over time).

Duolingo's ARPU has declined over the last two years, averaging 11.6%. Although it's unfortunate to see the company lose its pricing power, it was still able to achieve strong user growth. This quarter, ARPU declined 7.5% year on year to $22.88 per user.

Key Takeaways from Duolingo's Q4 Results

We were very impressed by Duolingo's robust user growth this quarter. We were also excited it produced strong revenue growth. Lastly, guidance for next quarter and the full year were ahead of expectations for both revenue and adjusted EBITDA. Zooming out, we think this was a great quarter that shareholders will appreciate. The stock is up 19.7% after reporting and currently trades at $234.43 per share.

Duolingo may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.