Duolingo (DUOL)

Duolingo is a great business. Its combination of fast growth, robust profitability, and superb prospects makes it a coveted asset.― StockStory Analyst Team

1. News

2. Summary

Why We Like Duolingo

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ:DUOL) is a mobile app helping people learn new languages.

- Remarkable 41.1% revenue growth over the last three years demonstrates its ability to capture significant market share

- Disciplined cost controls and effective management have materialized in a strong EBITDA margin, and its profits increased over the last few years as it scaled

- Impressive free cash flow profitability enables the company to fund new investments or reward investors with share buybacks/dividends, and its growing cash flow gives it even more resources to deploy

We’re optimistic about Duolingo. The price seems reasonable based on its quality, so this could be a favorable time to invest in some shares.

Why Is Now The Time To Buy Duolingo?

Duolingo’s stock price of $97.67 implies a valuation ratio of 11.3x forward EV/EBITDA. This valuation is fair - even cheap depending on how much you like the story - for the quality you get.

Our analysis and backtests show high-quality businesses routinely outperform the market over a multi-year period, especially when priced like this.

3. Duolingo (DUOL) Research Report: Q4 CY2025 Update

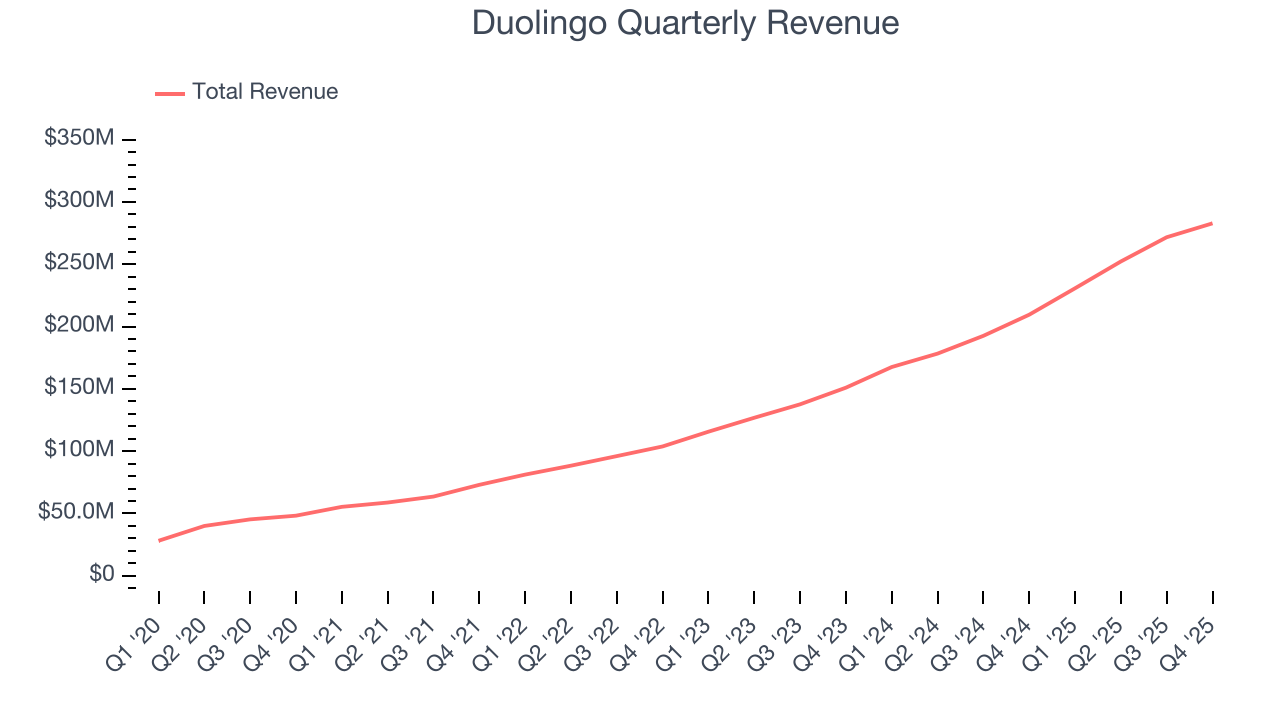

Language-learning app Duolingo (NASDAQ:DUOL) reported Q4 CY2025 results exceeding the market’s revenue expectations, with sales up 35% year on year to $282.9 million. On the other hand, next quarter’s revenue guidance of $288.5 million was less impressive, coming in 0.9% below analysts’ estimates.

Duolingo (DUOL) Q4 CY2025 Highlights:

- Revenue: $282.9 million vs analyst estimates of $275.9 million (35% year-on-year growth, 2.5% beat)

- Adjusted EBITDA: $84.35 million vs analyst estimates of $78.24 million (29.8% margin, 7.8% beat)

- Revenue Guidance for Q1 CY2026 is $288.5 million at the midpoint, below analyst estimates of $291.2 million

- EBITDA guidance for the upcoming financial year 2026 is $302 million at the midpoint, below analyst estimates of $385 million

- Operating Margin: 15.4%, up from 6.6% in the same quarter last year

- Free Cash Flow Margin: 33.1%, up from 28.5% in the previous quarter

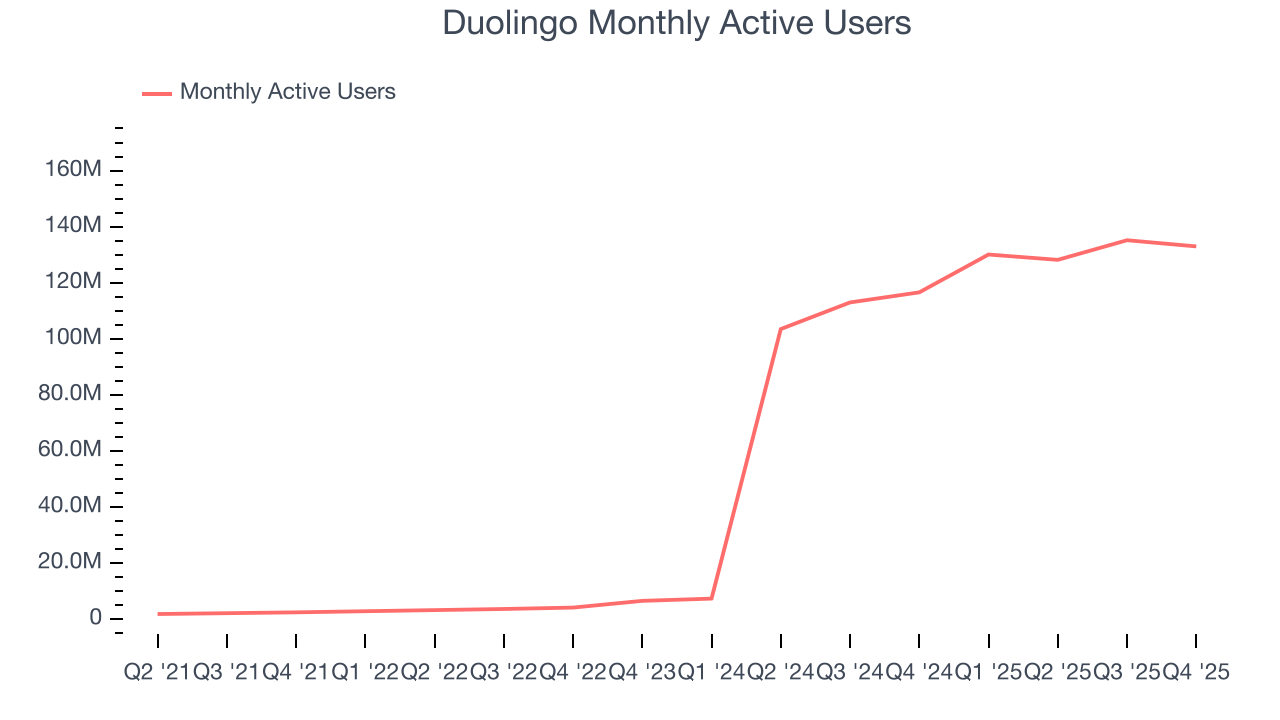

- Monthly Active Users: 133.1 million, up 16.4 million year on year

- Market Capitalization: $5.16 billion

Company Overview

Founded by a Carnegie Mellon computer science professor and his Ph.D. student, Duolingo (NASDAQ:DUOL) is a mobile app helping people learn new languages.

The company offers courses in widely-spoken languages such as Spanish, Mandarin, and French as well as less-known ones like Navajo. Duolingo primarily operates through a mobile app that can be downloaded on the app store and uses gamification to engage its users - for example, the app motivates users by awarding points for streaks of consistent practice. Additionally, adaptive learning is used to personalize the learning experience, where content and difficulty are adjusted based on the student's progress and performance.

The pain points Duolingo addresses are the difficulty and expense of learning new languages. Traditional language courses require people to be physically present at a scheduled time and can really put a dent in the wallet. Classes might also move at a certain speed, which can be too fast or slow for certain learners. With Duolingo, users can learn wherever there is an internet connection, on their own schedule, and at their own pace. All this for free (ad-supported tier) or a reasonable cost.

The company utilizes both a free version (ad-supported tier) and a paid version. Its main source of revenue is from subscriptions, and there are various tiers with more expensive ones providing more courses, features, and practice or assessment materials. Duolingo also generates revenue through advertising, partnerships, and language proficiency tests where the company offers assessments that are accepted by many universities and institutions around the world. For example, the Duolingo English Test is used by thousands of universities and institutions worldwide as a measure of proficiency.

4. Consumer Subscription

Consumers today expect goods and services to be hyper-personalized and on demand. Whether it be what music they listen to, what movie they watch, or even finding a date, online consumer businesses are expected to delight their customers with simple user interfaces that magically fulfill demand. Subscription models have further increased usage and stickiness of many online consumer services.

Competitors offering language-learning services include Coursera (NYSE:COUR) and private companies Rosetta Stone, Babbel, Busuu, and Lingvist.

5. Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Duolingo grew its sales at an incredible 41.1% compounded annual growth rate. Its growth surpassed the average consumer internet company and shows its offerings resonate with customers, a great starting point for our analysis.

This quarter, Duolingo reported wonderful year-on-year revenue growth of 35%, and its $282.9 million of revenue exceeded Wall Street’s estimates by 2.5%. Company management is currently guiding for a 25% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 21.4% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is noteworthy and indicates the market is baking in success for its products and services.

6. Monthly Active Users

User Growth

As a subscription-based app, Duolingo generates revenue growth by expanding both its subscriber base and the amount each subscriber spends over time.

Over the last two years, Duolingo’s monthly active users, a key performance metric for the company, increased by 677% annually to 133.1 million in the latest quarter. This growth rate is among the fastest of any consumer internet business and indicates its offerings have significant traction.

In Q4, Duolingo added 16.4 million monthly active users, leading to 14.1% year-on-year growth. The quarterly print was lower than its two-year result, suggesting its new initiatives aren’t accelerating user growth just yet.

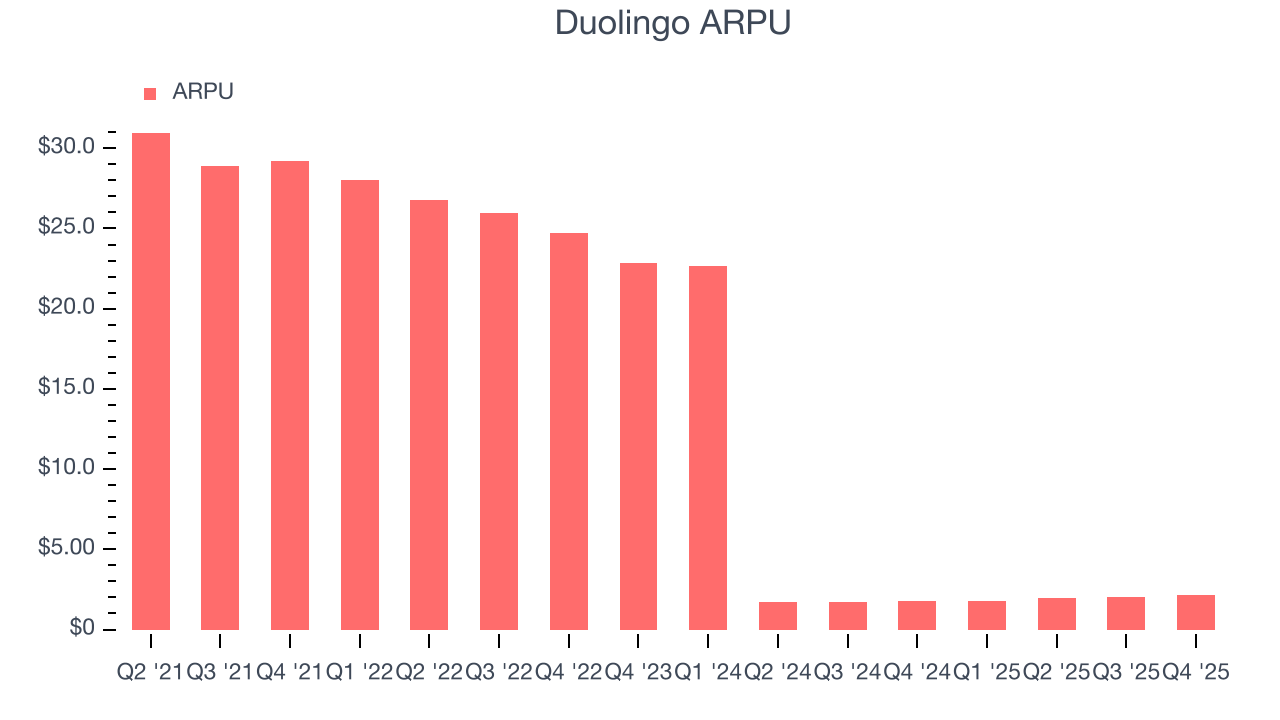

Revenue Per User

Average revenue per user (ARPU) is a critical metric to track because it measures how much the average user spends. ARPU is also a key indicator of how valuable its users are (and can be over time).

Duolingo’s ARPU fell over the last two years, averaging 26.8% annual declines. This isn’t great, but the increase in monthly active users is more relevant for assessing long-term business potential. We’ll monitor the situation closely; if Duolingo tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether users can continue growing at the current pace.

This quarter, Duolingo’s ARPU clocked in at $2.13. It grew by 18.4% year on year, faster than its monthly active users.

7. Gross Margin & Pricing Power

A company’s gross profit margin has a significant impact on its ability to exert pricing power, develop new products, and invest in marketing. These factors can determine the winner in a competitive market.

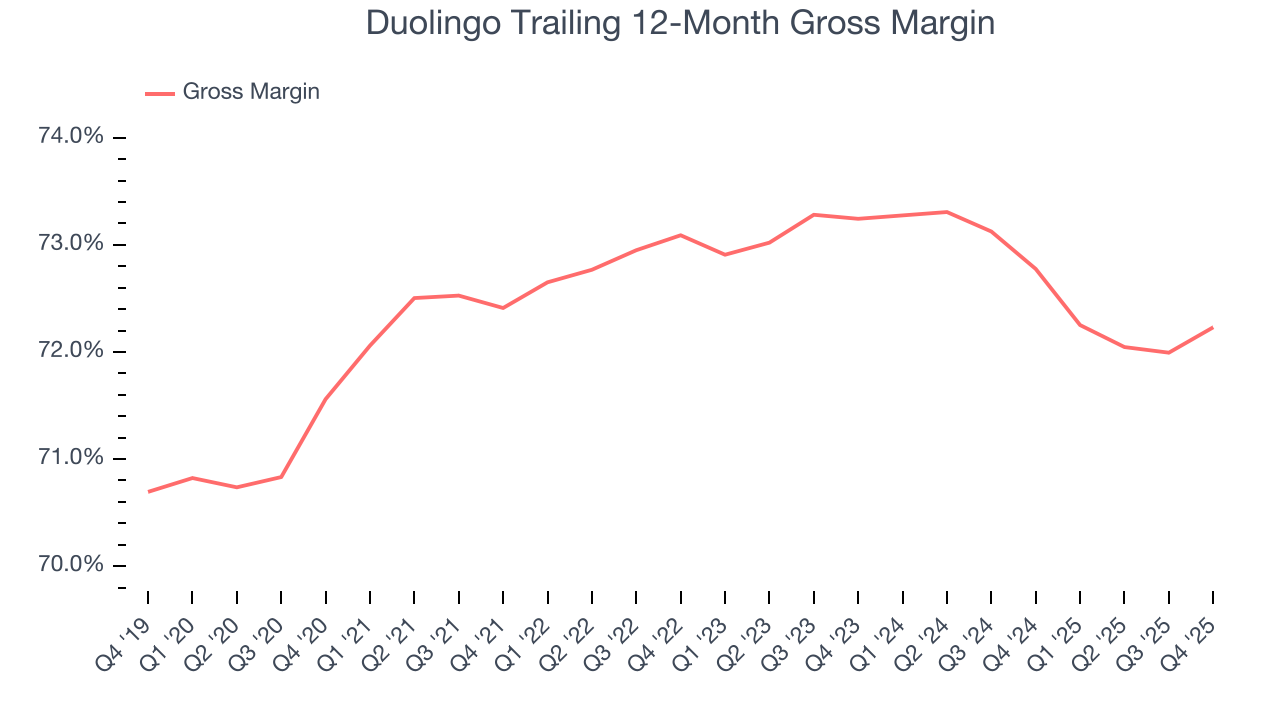

For internet subscription businesses like Duolingo, gross profit tells us how much money the company gets to keep after covering the base cost of its products and services, which typically include customer service, data center and infrastructure expenses, royalties, and other content-related costs if the company’s offerings include features such as video or music.

Duolingo has robust unit economics, an output of its asset-lite business model and pricing power. Its margin is better than the broader consumer internet industry and enables the company to fund large investments in new products and marketing during periods of rapid growth to achieve higher profits in the future. As you can see below, it averaged an excellent 72.5% gross margin over the last two years. That means Duolingo only paid its providers $27.54 for every $100 in revenue.

Duolingo’s gross profit margin came in at 72.8% this quarter, in line with the same quarter last year. Zooming out, the company’s full-year margin has remained steady over the past 12 months, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

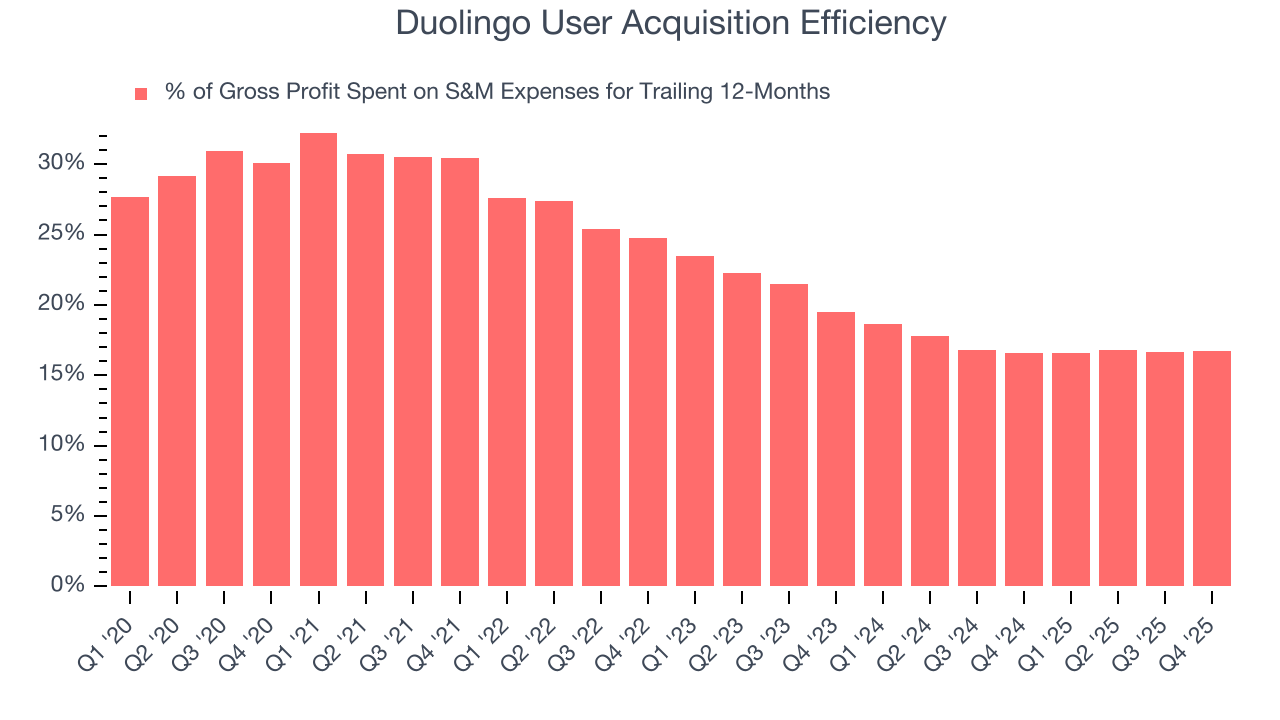

8. User Acquisition Efficiency

Unlike enterprise software that’s typically sold by dedicated sales teams, consumer internet businesses like Duolingo grow from a combination of product virality, paid advertisement, and incentives.

Duolingo is extremely efficient at acquiring new users, spending only 16.7% of its gross profit on sales and marketing expenses over the last year. This efficiency indicates that it has a highly differentiated product offering and strong brand reputation, giving Duolingo the freedom to invest its resources into new growth initiatives while maintaining optionality.

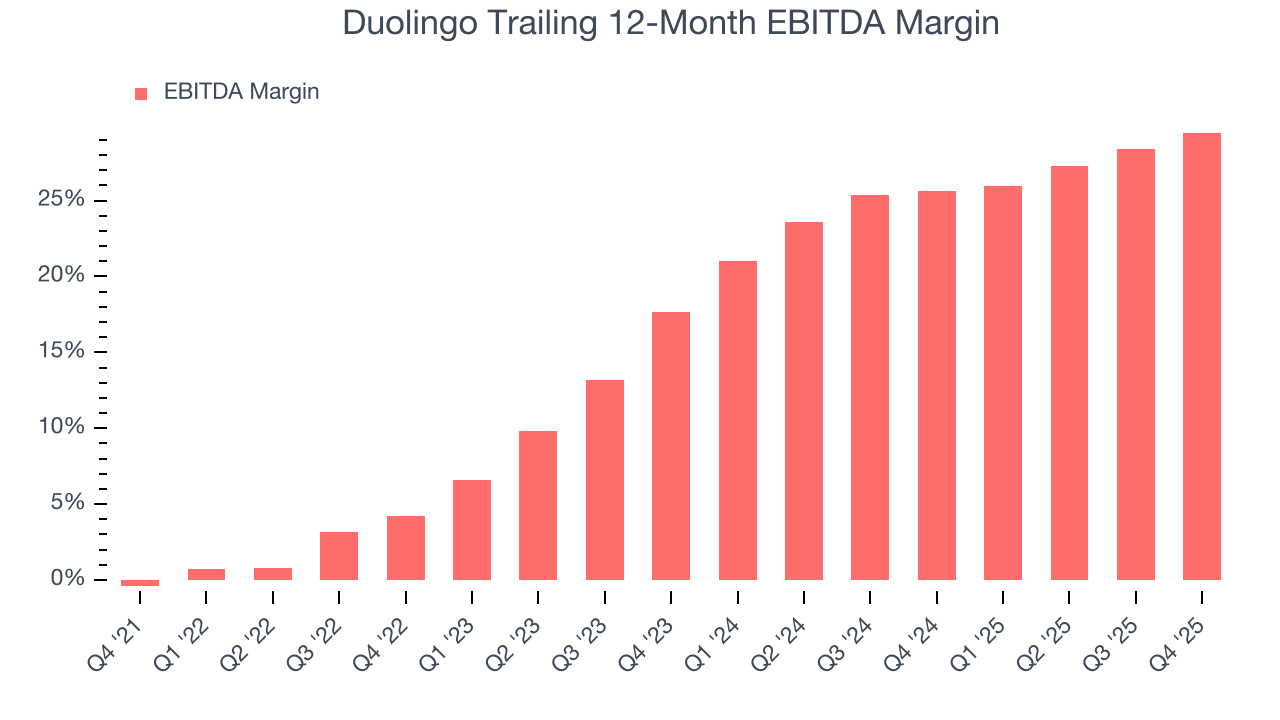

9. EBITDA

Duolingo has been a well-oiled machine over the last two years. It demonstrated elite profitability for a consumer internet business, boasting an average EBITDA margin of 27.9%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Duolingo’s EBITDA margin rose by 25.3 percentage points over the last few years, as its sales growth gave it immense operating leverage.

This quarter, Duolingo generated an EBITDA margin profit margin of 29.8%, up 4.9 percentage points year on year. The increase was encouraging, and because its EBITDA margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

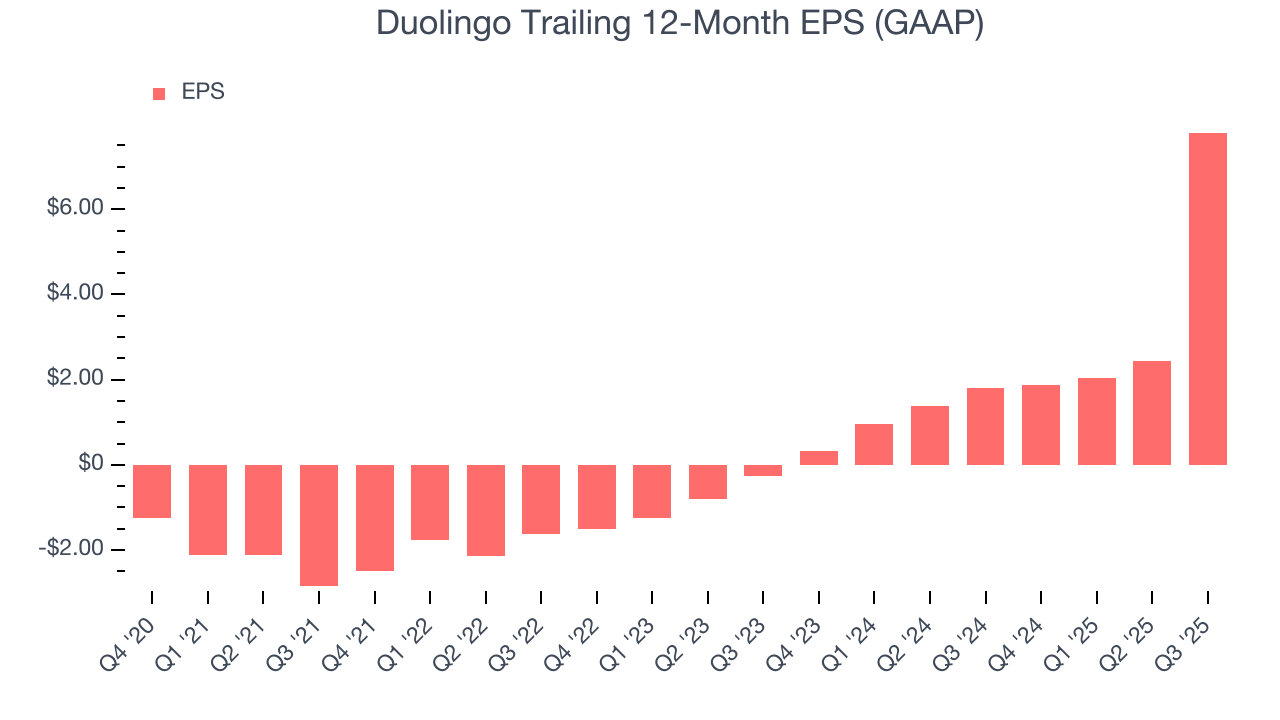

10. Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Duolingo’s full-year earnings are still negative, it reduced its losses and improved its EPS by 104% annually over the last three years. The next few quarters will be critical for assessing its long-term profitability. We hope to see an inflection point soon.

11. Cash Is King

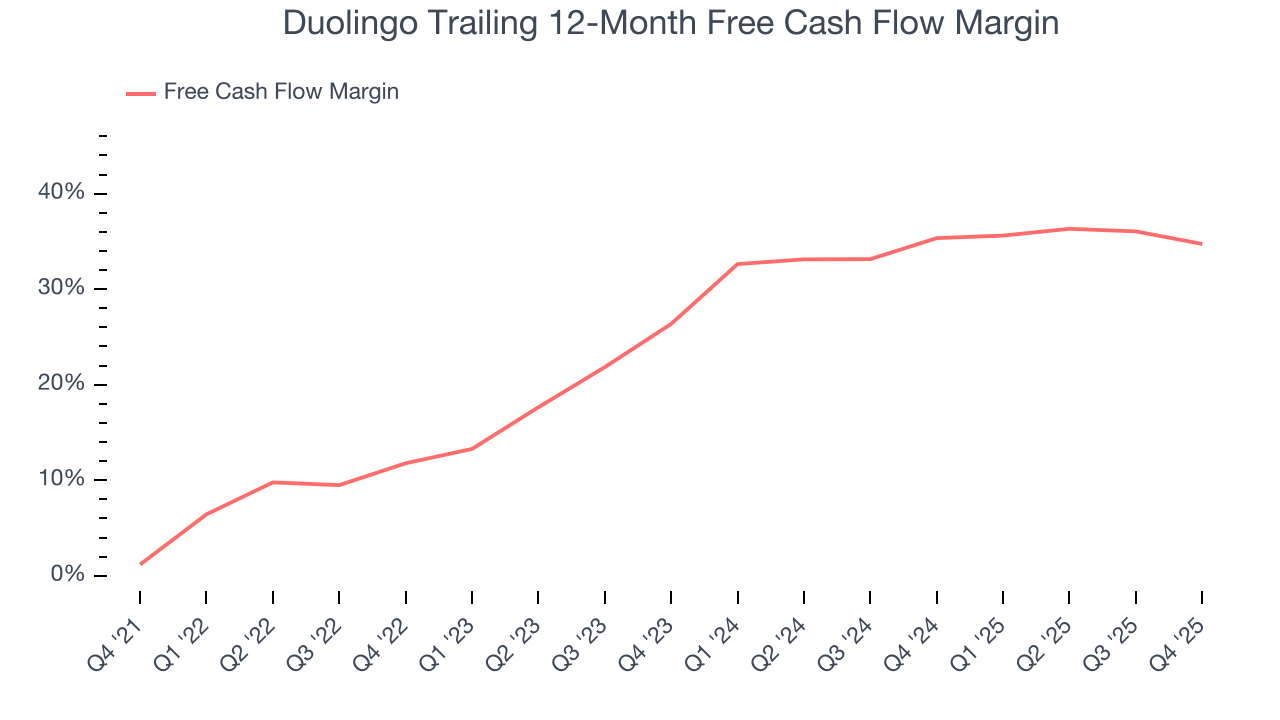

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Duolingo has shown terrific cash profitability, driven by its lucrative business model and cost-effective customer acquisition strategy that enable it to stay ahead of the competition through investments in new products rather than sales and marketing. The company’s free cash flow margin was among the best in the consumer internet sector, averaging an eye-popping 35% over the last two years.

Taking a step back, we can see that Duolingo’s margin expanded by 23 percentage points over the last few years. This is encouraging because it gives the company more optionality.

Duolingo’s free cash flow clocked in at $93.73 million in Q4, equivalent to a 33.1% margin. The company’s cash profitability regressed as it was 5.5 percentage points lower than in the same quarter last year, but we wouldn’t read too much into the short term because investment needs can be seasonal, causing temporary swings. Long-term trends are more important.

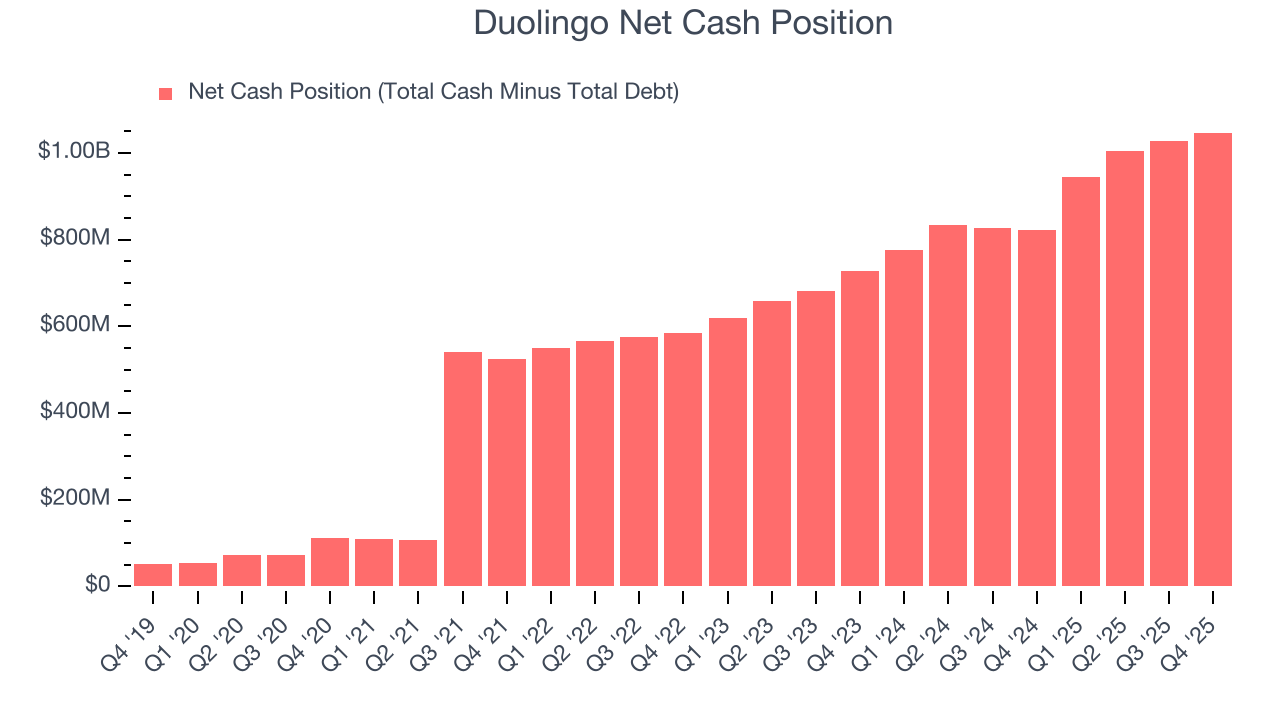

12. Balance Sheet Assessment

One of the best ways to mitigate bankruptcy risk is to hold more cash than debt.

Duolingo is a profitable, well-capitalized company with $1.14 billion of cash and $93.78 million of debt on its balance sheet. This $1.05 billion net cash position is 20.3% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

13. Key Takeaways from Duolingo’s Q4 Results

We were impressed by how significantly Duolingo blew past analysts’ EBITDA expectations this quarter. We were also glad it expanded its number of users. On the other hand, its full-year revenue guidance missed and its full-year EBITDA guidance fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock traded down 22.5% to $91.61 immediately following the results.

14. Is Now The Time To Buy Duolingo?

Updated: March 15, 2026 at 10:23 PM EDT

Are you wondering whether to buy Duolingo or pass? We urge investors to not only consider the latest earnings results but also longer-term business quality and valuation as well.

There is a lot to like about Duolingo. First of all, the company’s revenue growth was exceptional over the last three years. And while its ARPU has declined over the last two years, its powerful free cash flow generation enables it to stay ahead of the competition through consistent reinvestment of profits. On top of that, Duolingo’s impressive EBITDA margins show it has a highly efficient business model.

Duolingo’s EV/EBITDA ratio based on the next 12 months is 11.3x. Looking at the consumer internet landscape today, Duolingo’s fundamentals really stand out, and we like it at this price.

Wall Street analysts have a consensus one-year price target of $105.73 on the company (compared to the current share price of $97.67), implying they see 8.2% upside in buying Duolingo in the short term.