Entegris (NASDAQ:ENTG) Exceeds Q2 Expectations But Quarterly Guidance Underwhelms

Kayode Omotosho /

August 3, 2023

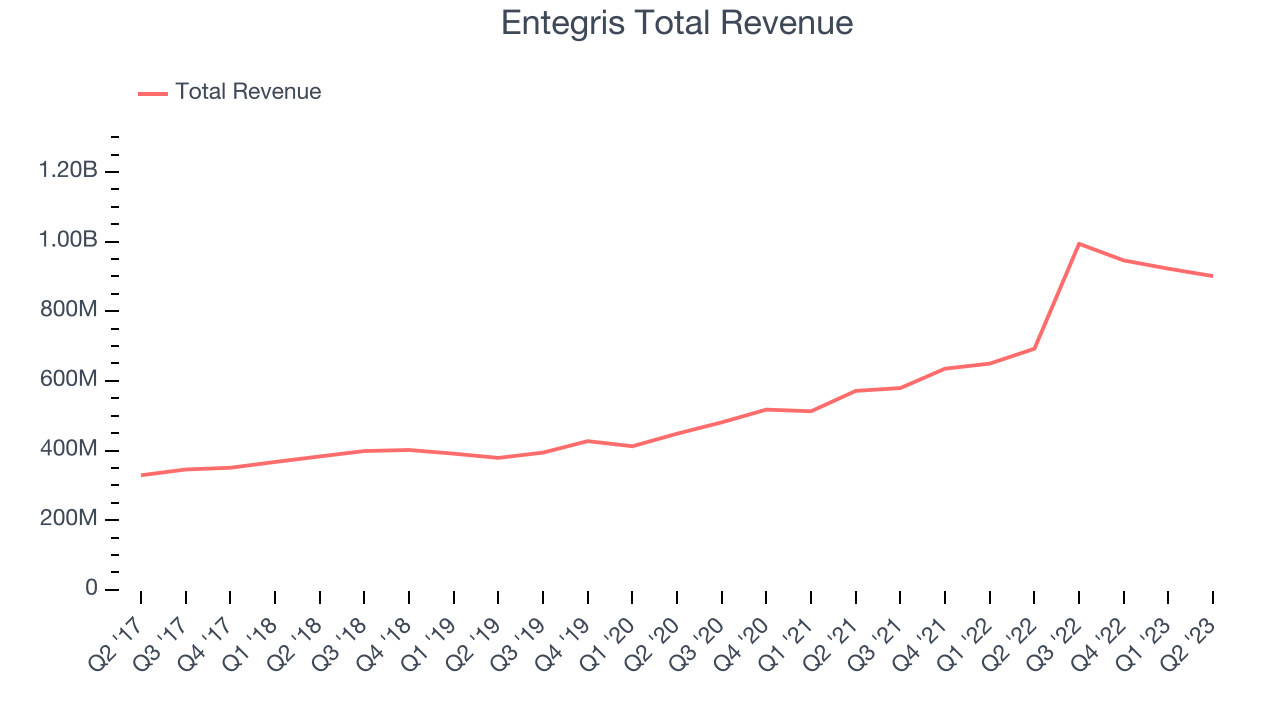

Semiconductor materials supplier Entegris (NASDAQ:ENTG) reported Q2 FY2023 results topping analysts' expectations, with revenue up 30.1% year on year to $901 million. The company also expects next quarter's revenue to be around $887.5 million, roughly in line with analysts' estimates. Entegris made a GAAP profit of $197.6 million, improving from its profit of $99.5 million in the same quarter last year.

Is now the time to buy Entegris? Find out by accessing our full research report free of charge.

Entegris (ENTG) Q2 FY2023 Highlights:

- Revenue: $901 million vs analyst estimates of $886.8 million (1.6% beat)

- EPS (non-GAAP): $0.66 vs analyst estimates of $0.57 (16.4% beat)

- Revenue Guidance for Q3 2023 is $887.5 million at the midpoint, below analyst estimates of $896.3 million

- Free Cash Flow of $11 million, down 38.7% from the previous quarter

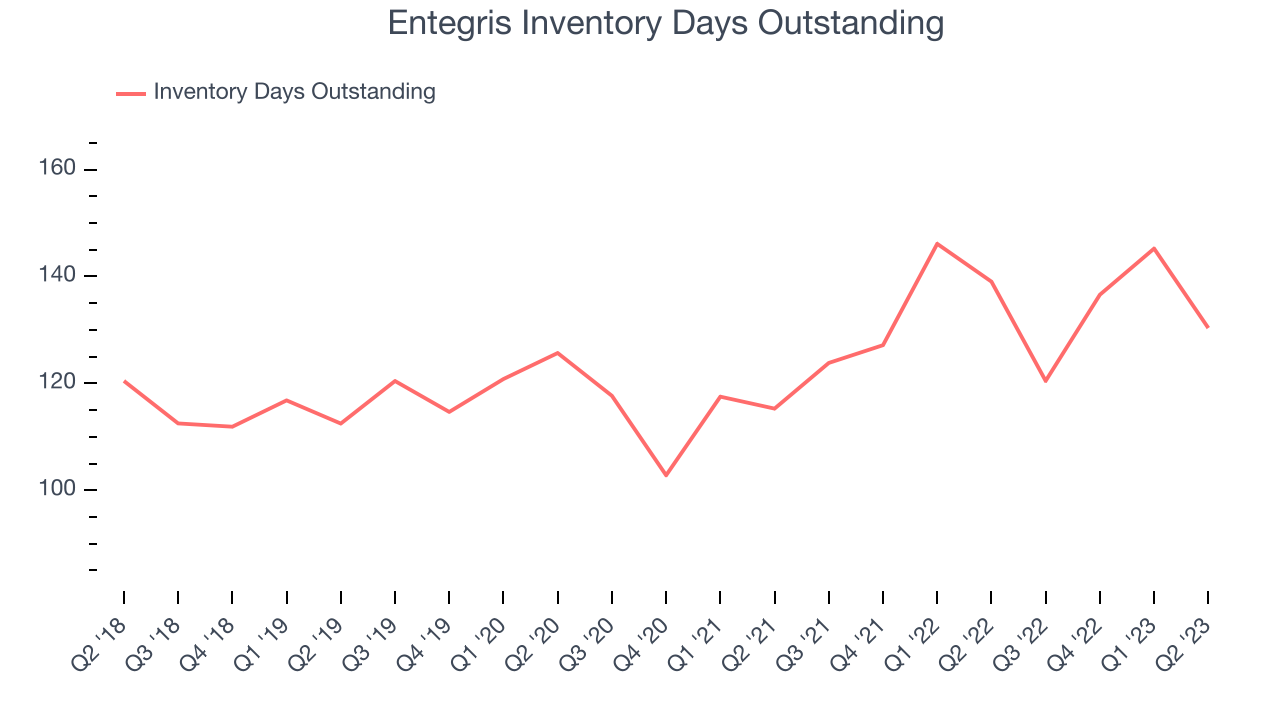

- Inventory Days Outstanding: 130, down from 145 in the previous quarter

- Gross Margin (GAAP): 42.6%, down from 44.8% in the same quarter last year

Bertrand Loy, Entegris’ president and chief executive officer, said: “Our performance and execution in the second quarter was solid and showcased the resilience of our unit driven model. Sales were down sequentially as expected, but we did see growth in product lines that are of increasing importance to our customers’ technology roadmaps.

With fabs representing the company’s largest customer type, Entegris (NASDAQ:ENTG) supplies products that purify, protect, and generally ensure the integrity of raw materials needed for advanced semiconductor manufacturing.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers and data storage. The growth of data and technologies like artificial intelligence, 5G networks and smart cars are also creating a next wave of growth for the industry. To keep up with ever changing customer needs requires new tools that can design, fabricate and test at ever smaller sizes and more complex architectures, and that is driving the demand for semiconductor capital manufacturing equipment.

Sales Growth

Entegris's revenue growth over the last three years has been very strong, averaging 31.6% annually. As you can see below, this quarter was especially strong, with revenue growing from $692.5 million in the same quarter last year to $901 million. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions (which can sometimes offer opportune times to buy).

Entegris had a strong quarter as its revenue grew 30.1% year on year, topping analysts' estimates by 1.6%. However, this was its third consecutive quarter of decelerating growth, potentially indicating a coming cycle downturn.

Entegris's management team projects growth to turn negative next quarter. As such, the company is guiding for a 10.7% year-on-year revenue decline while analysts are expecting a 4.66% drop over the next 12 months.While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Product Demand & Outstanding Inventory

Days Inventory Outstanding (DIO) is an important metric for chipmakers, as it reflects a business' capital intensity and the cyclical nature of semiconductor supply and demand. In a tight supply environment, inventories tend to be stable, allowing chipmakers to exert pricing power. Steadily increasing DIO can be a warning sign that demand is weak, and if inventories continue to rise, the company may have to downsize production.

This quarter, Entegris's DIO came in at 130, which is 7 days above its five-year average. These numbers suggest that despite the recent decrease, the company's inventory levels are higher than what we've seen in the past.

Key Takeaways from Entegris's Q2 Results

With a market capitalization of $15.5 billion, a $567 million cash balance, and near-breakeven free cash flow status, we're confident that Entegris is in a healthy financial position.

We were impressed by Entegris's strong improvement in inventory levels. We were also excited that its earnings growth outperformed Wall Street's expectations. On the other hand, its revenue guidance for next quarter was underwhelming and its operating margin declined. Overall, the results could have been better. The stock is flat after reporting and currently trades at $104.05 per share.

So should you invest in Entegris right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.