Monster (NASDAQ:MNST) Misses Q3 Sales Targets

Max Juang /

November 7, 2024

Energy drink company Monster Beverage (NASDAQ:MNST) missed Wall Street’s revenue expectations in Q3 CY2024 as sales only rose 1.3% year on year to $1.88 billion. Its GAAP profit of $0.38 per share was also 10.6% below analysts’ consensus estimates.

Is now the time to buy Monster? Find out in our full research report.

Monster (MNST) Q3 CY2024 Highlights:

- Revenue: $1.88 billion vs analyst estimates of $1.91 billion (1.6% miss)

- EPS: $0.38 vs analyst expectations of $0.43 (10.6% miss)

- Gross Margin (GAAP): 53.2%, in line with the same quarter last year

- Operating Margin: 25.5%, down from 27.5% in the same quarter last year

- Market Capitalization: $53.33 billion

Hilton H. Schlosberg, Vice Chairman and Co-Chief Executive Officer, said, “The energy drink category continues to grow globally and has demonstrated resilience. In the United States, the energy drink category continued to experience slower growth rates. However, in all measured channels excluding convenience, the energy drink category is growing at a faster rate. In the United States, the energy drink category in the convenience channel is beginning to show some improvement in October. A number of other consumer packaged goods companies have also seen a tighter consumer spending environment for certain income groups and weaker demand in the quarter.

Company Overview

Founded in 2002 as a natural soda and juice company, Monster Beverage (NASDAQ:MNST) is a pioneer of the energy drink category, and its Monster Energy brand targets a young, active demographic.

Beverages, Alcohol and Tobacco

These companies' performance is influenced by brand strength, marketing strategies, and shifts in consumer preferences. Changing consumption patterns are particularly relevant and can be seen in the rise of cannabis, craft beer, and vaping or the steady decline of soda and cigarettes. Companies that spend on innovation to meet consumers where they are with regards to trends can reap huge demand benefits while those who ignore trends can see stagnant volumes. Finally, with the advent of the social media, the cost of starting a brand from scratch is much lower, meaning that new entrants can chip away at the market shares of established players.

Sales Growth

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years.

Monster is one of the larger consumer staples companies and benefits from a well-known brand that influences consumer purchasing decisions.

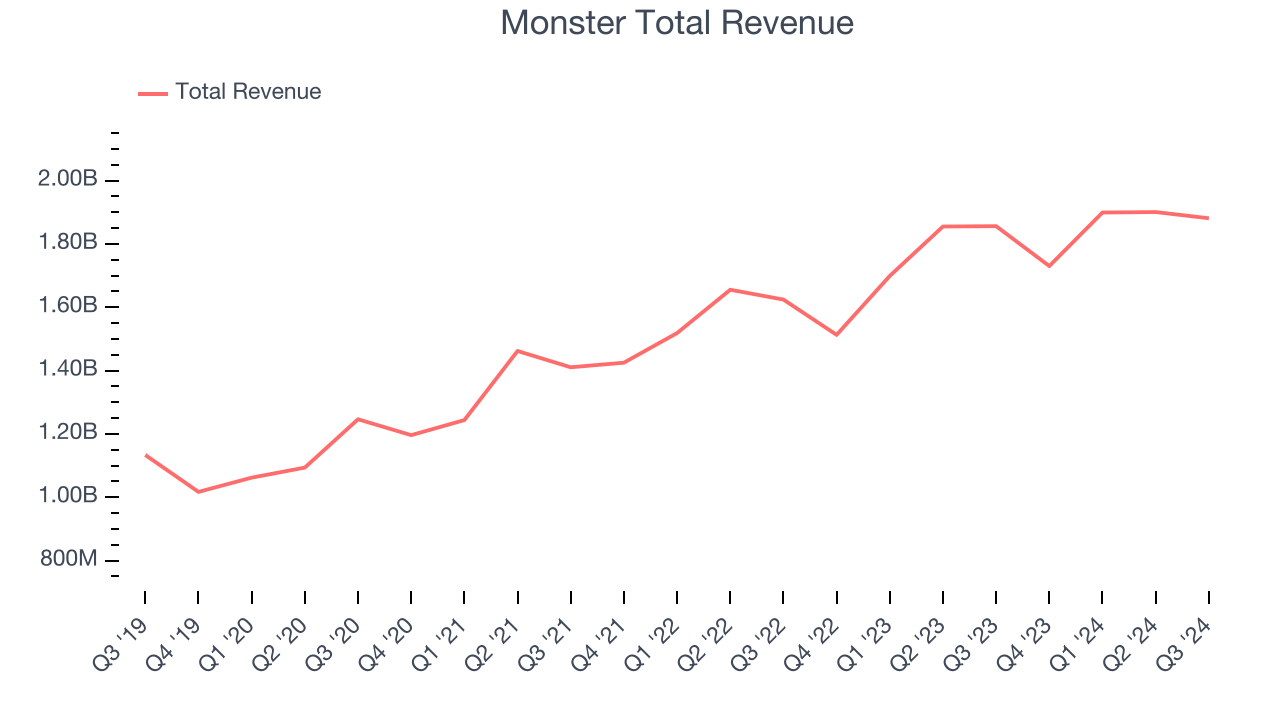

As you can see below, Monster grew its sales at a solid 11.7% compounded annual growth rate over the last three years. This is encouraging because it shows Monster had stronger demand than most consumer staples companies.

This quarter, Monster’s revenue grew 1.3% year on year to $1.88 billion, falling short of Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 8% over the next 12 months, a deceleration versus the last three years. Still, this projection is above average for the sector and indicates the market is factoring in some success for its newer products.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Cash Is King

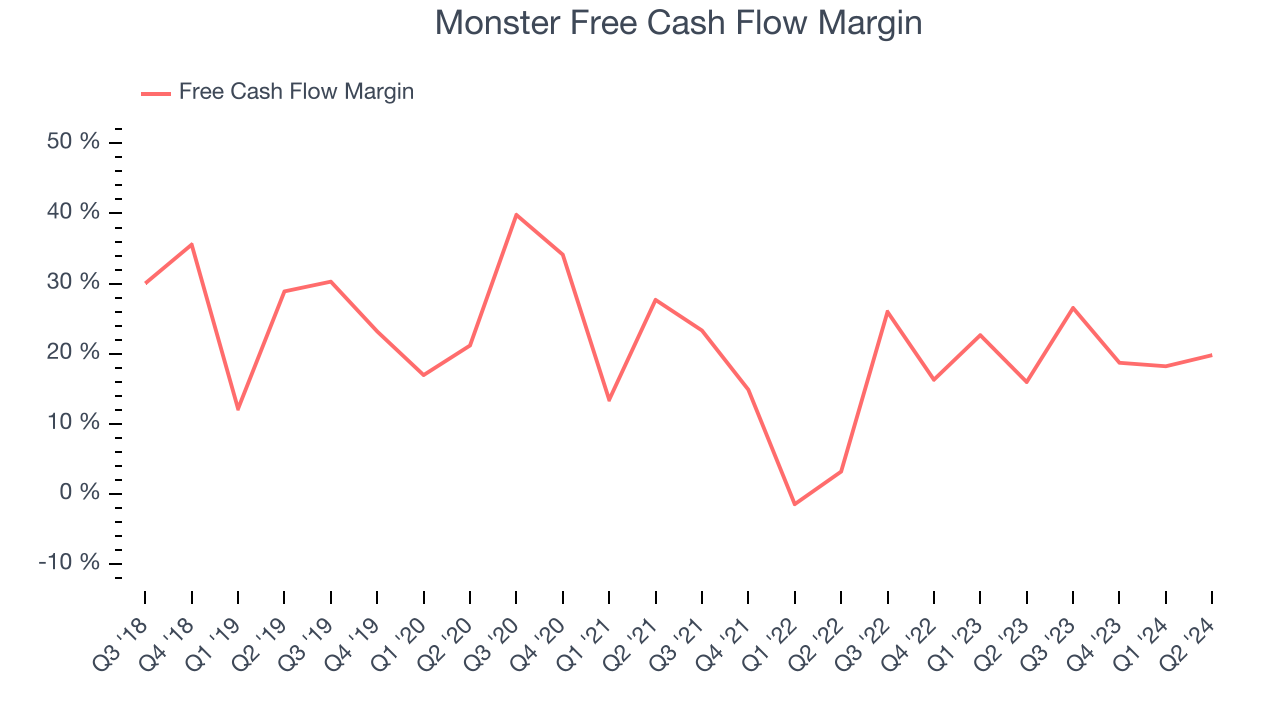

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Monster has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition. The company’s free cash flow margin was among the best in the consumer staples sector, averaging 19.8% over the last two years.

Key Takeaways from Monster’s Q3 Results

We struggled to find many strong positives in these results. Its EPS missed analysts’ expectations and its revenue missed Wall Street’s estimates. Overall, this quarter could have been better. The stock traded down 2.3% to $53.50 immediately following the results.

Monster’s latest earnings report disappointed. One quarter doesn’t define a company’s quality, so let’s explore whether the stock is a buy at the current price. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.